|

市場調查報告書

商品編碼

2061698

醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Folding Carton In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

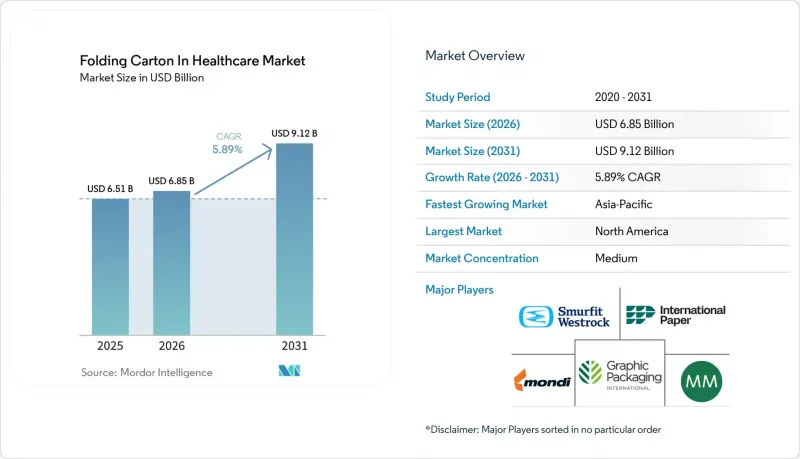

根據 Mordor Intelligence 預測,醫療保健用折疊式紙盒的市場規模預計將從 2025 年的 65.1 億美元成長到 2026 年的 68.5 億美元,到 2031 年達到 91.2 億美元,2026 年至 2031 年的複合年成長率預計為 5.89%。

本報告按材料類型(固態漂白硫酸紙漿、折疊紙盒用紙板、未漂白塗佈牛皮紙等)、印刷技術(膠印、柔版印刷等)、應用領域(製藥企業、醫療設備企業、營養補充劑公司等)和地區進行細分。市場預測以美元計價。

面向醫療保健行業的折疊式紙盒市場趨勢與洞察

需要單劑量治療的慢性疾病病例增加

醫療保健折疊式紙盒市場受到持續需求的支撐,這主要得益於需要重複給藥的慢性疾病數量不斷增加以及用藥依從性管理日益嚴格。單劑量泡殼包裝和壓延紙盒因其有助於患者堅持用藥方案,並便於在配藥點進行核對,在糖尿病、循環系統疾病和腫瘤治療領域得到越來越廣泛的應用。因此,製藥公司正在指定能夠容納28天和90天泡殼包裝,且即使經過反覆開合也能保持折疊強度的紙盒結構。龍沙公司已擴大了位於印度雷瓦里工廠和中國蘇州工廠的膠囊產能。兩家工廠均已於2024年底運作,另有多條生產線計劃於2025年第三季投入運作,這將加速亞太地區向單劑量包裝的全面轉型。印度藥品市場預計將從2024年的613.6億美元成長到2033年的1,300億美元,中國市場預計將從2024年的804億美元成長到2030年的1,266億美元,這將推動醫療保健領域對折疊式紙盒的長期需求。這種需求正促使醫療保健折疊式紙盒市場銷售成長不再那麼依賴價格週期,而是更多地與強調治療方案和用藥依從性的包裝設計相關。

序列化法規將鼓勵增加紙箱上的展示面積。

醫療保健折疊式紙盒市場的發展也受到序列化法規的推動,這些法規要求更大的紙盒空間和更高的印刷精度。歐盟的《反假藥指令》自2019年起強制要求在處方藥包裝上印製唯一的2D資料矩陣碼,而美國的《藥品供應鏈安全法》則要求產品識別碼、序號、批號和有效期限必須以機器可讀格式印刷。歐盟委員會第2016/161號授權條例規定,資料矩陣碼的最小尺寸為8mm x 8mm,四周留有1mm的空白區域。對於單劑量管瓶和預填充式注射器過程中保持平整。 2026年3月,安姆科在其義大利工廠推出了可回收薄膜。該薄膜採用與生產線相容的塗層,可減少高速檢驗過程中油墨滲漏問題。歐洲藥品檢驗系統 (EMVS) 目前每天處理超過4000萬檢驗,這對醫療保健折疊式紙盒提出了越來越大的壓力,要求其保持更嚴格的印刷公差和更可靠的基材性能。

紙板價格波動

由於紙漿和紙板成本波動,醫療保健折疊式紙盒市場面臨明顯的限制。 2024年至2025年,北美漂白軟木牛皮紙漿的價格在每噸1050美元至1350美元之間波動,而斯堪地那維亞造紙廠的能源價格波動則持續推高生產成本。固態紙板和折疊紙盒的價格通常落後60至90天,這使得與製藥客戶簽訂固定價格供應合約的加工商面臨風險。在醫療保健折疊紙盒市場,這種價格滯後可能會進一步擠壓利潤空間,而此時合規、印刷品質和認證成本已經飆升。由於缺乏與紙漿的後向整合,區域性中小型加工商面臨的風險更大。此外,由於紙漿價格超過每噸1,300美元,一些歐洲專業製造商已將2025年下半年的運轉率降至70%-75%。製藥採購商正在透過採用雙重採購和紙漿價格掛鉤條款來應對,這將提高供應穩定性,但也會加劇醫療保健用折疊式紙盒的價格競爭,使中小獨立供應商處於不利地位。

細分市場分析

到2025年,固態漂白硫酸紙漿將佔醫療保健折疊式紙盒市場43.28%的佔有率,這主要得益於其高不透明度、高白度和在高速膠印機上可靠的印刷性能。預計到2031年,折疊紙盒市場將以7.06%的複合年成長率成長,成為醫療保健折疊式紙盒市場中成長最快的材料類別。 Metsa Board的生命週期評估(LCA)表明,與塗佈未漂白牛皮紙板相比,使用新鮮纖維的紙板二氧化碳排放降低了50%至60%,從而提高了其應用率。更長的纖維也允許在不影響抗穿刺性的前提下,將紙張重量降低15%至20%。塗佈未漂白牛皮紙板仍用於外包裝和二次包裝,在這些應用中,結構強度比優異的印刷性能更為重要。白色襯裡的塑合板僅限於注重成本的機能性食品應用,在這些應用中,回收材料強化了永續性訊息,並且印刷要求沒有那麼嚴格。

在醫療保健行業,折疊式紙盒的買家越來越傾向於選擇既符合監管規定的印刷要求又具備可回收性的紙板。斯特拉勒恩索位於奧盧的生產線計劃於2025年第二季開始交付,這表明供應商正在擴大其醫藥級消費紙板的產能以滿足這一需求。此外,歐盟的《包裝和包裝廢棄物法規》正促使加工商放棄使用聚乙烯或聚丙烯層的複合紙板結構,因為這些結構會降低可回收性。雖然水性阻隔材料的重要性日益凸顯,但對於對濕度敏感的生物製藥產品而言,其性能仍然存在不足,因此一些低溫運輸應用仍然使用傳統的蠟塗層和其他高防護等級的材料。這種平衡促使醫療保健折疊式紙盒朝著更乾淨、更輕的基材發展,同時又不影響藥物的穩定性或運輸安全性。

區域分析

截至2025年,北美地區佔據醫療保健折疊式紙盒市場34.63%的佔有率,而亞太地區預計到2031年將以6.57%的複合年成長率(CAGR)實現最高成長。北美地區的市場地位反映了美國對藥品包裝的巨大需求,以及口服固體製劑領域對瓶裝和紙盒包裝系統的持續使用。此外,由於主流藥品分銷管道對兒童安全標準、序列化合規性和高品質印刷要求的嚴格執行,該地區在醫療保健折疊式紙盒市場也繼續保持核心地位。亞太地區的成長速度更快,這得益於藥品生產的擴張、本地產能的提升以及人口密集地區單劑量製劑的日益普及。印度藥品市場預計將從2024年的613.6億美元成長到2033年的1,300億美元,中國市場規模將從2024年的804億美元成長到2030年的1,266億美元。

龍沙在印度雷瓦里和中國蘇州的產能擴張表明,跨國供應商正在調整其生產系統,以適應區域內向單劑量包裝和旨在提高用藥依從性的包裝形式的轉變。這對醫療保健折疊式紙盒具有重大意義,因為對二級包裝的需求通常與劑型生產量和藥品生產的局部化密切相關。歐洲雖然並非最大的銷售佔有率,但由於其嚴格的序列化要求以及對可回收紙板結構和環保包裝系統的強勁需求,仍然是一個至關重要的地區。 《反仿冒藥品指令》和《包裝及包裝廢棄物條例》迫使歐洲藥品採購商同時重新評估紙板選擇、印刷版面和阻隔設計。這些因素共同作用,使歐洲成為醫療保健折疊式紙盒行業受監管影響最大的地區之一,也使其成為希望銷售優質、永續基材的供應商的重要市場。

在南美洲、中東和非洲,由於當地折疊式紙盒產能有限以及在地採購。印度的原料藥(API)產業預計到2024年將達到135億美元,自2017年以來年複合成長率達7%,該產業正在減少對中國進口的依賴,這為國內瓦楞紙板供應商向製藥生產基地靠攏創造了空間。印度預計將佔據美國製造業回流潮25%至30%的佔有率,而這一回流潮預計將涉及約2,700億美元的投資,這將進一步推動亞太地區包裝的在地化進程。在這些持續變化中,醫療保健用折疊式紙盒的生產可能會變得更加區域平衡,即使需求仍然集中在北美、歐洲和成長最快的亞洲醫藥市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 食品飲料加工部門的擴張

- 電子商務包裝需求不斷成長

- 對永續包裝解決方案的需求日益成長

- 擴大數位印刷在小批量瓦楞紙箱中的應用。

- 政府對塑膠包裝徵收銷售稅,這促使包裝材料轉向紙板。

- 雲端廚房和食材自煮包新創公司的快速發展,推動了對小批量瓦楞紙箱的需求增加。

- 市場限制因素

- 紙板價格波動

- 來自軟性包裝替代品的競爭

- 國內紙漿產量有限,導致對進口的依賴性日益增強。

- 停電增加了轉換器的生產成本。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依材料類型

- 固態漂白硫酸漿

- 折疊紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 透過使用

- 製藥公司

- 醫療設備製造商

- 營養保健品和營養補充品公司

- 獸醫醫療服務提供者

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit WestRock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc.

- American Carton Company

- Packaging Corporation of America

- Edelmann GmbH

- CCL Industries Inc.

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray, LP

- Klabin SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the folding carton in healthcare market size is expected to increase from USD 6.51 billion in 2025 to USD 6.85 billion in 2026 and reach USD 9.12 billion by 2031, growing at a CAGR of 5.89% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic Printing, Flexographic Printing, and More), Application (Pharmaceutical Manufacturers, Medical Device Companies, Nutraceutical and Dietary Supplement Firms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Folding Carton In Healthcare Market Trends and Insights

Growth of Chronic Diseases Requiring Unit-Dose Treatments

The folding carton in healthcare market is seeing steady support from the rise in chronic diseases that require repeat dosing and tighter adherence controls. Unit-dose blister packs and calendar cartons are increasingly used for therapies in diabetes, cardiovascular care, and oncology because these formats make dosing schedules easier to follow and verify at dispensing points. Drug makers are therefore specifying carton structures that can hold 28-day and 90-day blister formats without losing crease strength after repeated opening and closing cycles. Lonza expanded capsule manufacturing capacity at its Rewari facility in India and its Suzhou facility in China, with both sites active in late 2024 and additional lines commissioned in Q3 2025, supporting the wider move toward unit-dose formats in Asia-Pacific. India's pharmaceutical market was projected to rise from USD 61.36 billion in 2024 to USD 130 billion by 2033, while China's market was projected to increase from USD 80.4 billion in 2024 to USD 126.6 billion by 2030, reinforcing long-term demand for folding cartons in the healthcare market. This demand is making volume growth in the folding carton market in healthcare less dependent on pricing cycles and more tied to treatment patterns and adherence-focused packaging design.

Serialization Mandates Driving Larger Carton Real Estate

The folding carton in healthcare market is also being pushed by serialization rules that require more carton space and better print accuracy. The European Union Falsified Medicines Directive has required a unique 2D DataMatrix code on prescription drug packs since 2019, while the U.S. Drug Supply Chain Security Act requires product identifiers, serial numbers, lot numbers, and expiration dates in machine-readable form. Commission Delegated Regulation 2016/161 specified a minimum 8-millimeter-by-8-millimeter DataMatrix area with a 1-millimeter quiet zone on all sides, which can consume 12% to 15% of usable carton surface on compact packs for single-dose vials and pre-filled syringes. As a result, converters in the folding carton market for healthcare are seeing increased demand for premium boards that can withstand sharp codes, prevent ink bleed, and remain flat during inspection and scanning. Amcor launched recycle-ready films at its Italian facility in March 2026 with serialization-compatible coatings that reduced a failure point linked to ink smudging during high-speed verification. The European Medicines Verification System now processes more than 40 million verification events each day, which keeps pressure on the folding carton in healthcare market to maintain tighter print tolerances and more reliable substrate performance.

Volatility in Paperboard Prices

The folding carton in healthcare market faces a clear restraint from unstable pulp and paperboard costs. Northern bleached softwood kraft pulp prices ranged from USD 1,050 to USD 1,350 per metric ton during 2024 and 2025, while energy swings in Scandinavian mills kept production costs under pressure. Solid bleached board and folding boxboard prices usually lag by 60 to 90 days, leaving converters exposed when they have fixed-price supply contracts with pharmaceutical customers. In the folding carton market for healthcare, that lag can compress margins at exactly the point when compliance, print quality, and certification costs are already high. Smaller regional converters are more exposed because they lack backward integration into pulp, and several European specialists lowered utilization to 70%-75% in H2 2025 as pulp prices rose above USD 1,300 per metric ton. Pharmaceutical buyers are responding by adopting dual sourcing and pulp-linked price clauses, which improve supply security but make folding cartons in the healthcare market more price-competitive and less favorable to smaller independent suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Child-Resistant Pharmaceutical Packaging

- Shift Toward Sustainable and Recyclable Paperboard

- Competition from Flexible Packaging Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid bleached sulfate accounted for 43.28% share of the folding carton in healthcare market size in 2025, reflecting its strong opacity, high brightness, and reliable print performance on high-speed offset presses. Folding boxboard is projected to grow at a 7.06% CAGR through 2031, making it the fastest-growing material segment in the folding carton market for healthcare. Fresh-fiber grades are gaining ground because life-cycle assessments from Metsa Board showed carbon emissions 50% to 60% lower than those of coated unbleached kraftboard, while longer fibers also supported 15% to 20% basis-weight reductions without sacrificing puncture resistance. Coated unbleached kraftboard continues to serve outer shipping and secondary pack formats where structural strength matters more than premium printability. White-lined chipboard remains limited to more cost-sensitive nutraceutical applications where recycled content supports sustainability messaging and print requirements are less demanding.

In the healthcare industry, folding carton buyers are increasingly favoring boards that meet both compliance printing requirements and recyclability expectations. Stora Enso's Oulu line, with first deliveries in Q2 2025, shows how suppliers are expanding pharmaceutical-grade consumer board capacity to meet this demand. The European Union's Packaging and Packaging Waste Regulation is also pushing converters away from laminated paperboard structures that use polyethylene or polypropylene layers that reduce recyclability. Water-based barriers are becoming more relevant, but moisture-sensitive biologics still create a performance gap that supports continued use of traditional wax-coated or otherwise more protective grades in some cold-chain uses. That balance means the folding carton in healthcare market is moving toward cleaner and lighter substrates, but not at the expense of drug stability or distribution safety.

Geography Analysis

North America held 34.63% of the folding carton in healthcare market share in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 6.57% through 2031. North America's position reflects the scale of U.S. pharmaceutical packaging demand and the continued use of bottle-and-carton systems across oral solid dosage categories. The region also remains central to the folding carton in healthcare market because child-resistant standards, serialization compliance, and premium print requirements are tightly enforced in mainstream drug distribution. Asia-Pacific is growing faster because pharmaceutical manufacturing is expanding, local capacity is increasing, and unit-dose formats are becoming more common in large population centers. India's pharmaceutical market was projected to rise from USD 61.36 billion in 2024 to USD 130 billion by 2033, while China's market was projected to increase from USD 80.4 billion in 2024 to USD 126.6 billion by 2030.

Lonza's capacity additions at Rewari, India, and Suzhou, China, show how multinational suppliers are aligning production with the regional shift toward unit-dose packaging and better adherence formats. That matters for the folding carton in healthcare market because secondary packaging demand usually follows dosage-form output and localization of drug manufacturing. Europe remains a critical region even without the top revenue share because it combines strict serialization requirements with strong pressure for recyclable board structures and lower-impact packaging systems. The Falsified Medicines Directive and the Packaging and Packaging Waste Regulation are forcing pharmaceutical buyers in Europe to rethink board selection, print layout, and barrier design at the same time. This combination makes Europe one of the most regulation-shaped parts of the folding carton in healthcare market, especially for suppliers that want to sell premium sustainable substrates.

South America and the Middle East and Africa are expanding more slowly because local folding-carton capacity is limited and healthcare regulations remain more fragmented across countries. Imports from Europe and North America can add 15% to 25% to landed costs in these regions, which affects the competitiveness of locally supplied cartons versus other packaging options. India's active pharmaceutical ingredient sector, valued at USD 13.5 billion in 2024 and growing at 7% CAGR since 2017, is reducing dependence on Chinese imports and opening room for domestic carton suppliers to move closer to pharmaceutical production hubs. The United States' reshoring push, with an estimated USD 270 billion investment pool and India expected to capture 25% to 30% of that allocation, also supports packaging localization in Asia-Pacific. As those shifts continue, the folding carton in healthcare market is likely to become more regionally balanced in production, even if demand remains concentrated in North America, Europe, and the fastest-growing Asian pharmaceutical centers.

- Smurfit WestRock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc.

- American Carton Company

- Packaging Corporation of America

- Edelmann GmbH

- CCL Industries Inc.

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray, L.P.

- Klabin S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Food and Beverage Processing Sector

- 4.2.2 Growth of E-commerce Packaging Demand

- 4.2.3 Rising Demand for Sustainable Packaging Solutions

- 4.2.4 Increased Adoption of Digital Printing for Short-Run Cartons

- 4.2.5 Government Excise Tax on Plastic Packaging Spurring Shift Toward Paperboard

- 4.2.6 Rapid Growth of Cloud Kitchen and Meal-Kit Start-ups Requiring Small-Batch Cartons

- 4.3 Market Restraints

- 4.3.1 Volatility in Paperboard Prices

- 4.3.2 Competition From Flexible Packaging Alternatives

- 4.3.3 Limited Domestic Pulp Production Increasing Import Dependence

- 4.3.4 Power Supply Interruptions Elevating Production Costs for Converters

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By Application

- 5.3.1 Pharmaceutical Manufacturers

- 5.3.2 Medical Device Companies

- 5.3.3 Nutraceutical and Dietary Supplement Firms

- 5.3.4 Veterinary Healthcare Providers

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Graphic Packaging International LLC

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 International Paper Company

- 6.4.5 Stora Enso Oyj

- 6.4.6 Georgia-Pacific LLC

- 6.4.7 Mondi plc

- 6.4.8 Huhtamaki Oyj

- 6.4.9 Seaboard Folding Box Co. Inc.

- 6.4.10 American Carton Company

- 6.4.11 Packaging Corporation of America

- 6.4.12 Edelmann GmbH

- 6.4.13 CCL Industries Inc.

- 6.4.14 Rengo Co., Ltd.

- 6.4.15 Sonoco Products Company

- 6.4.16 Autajon Group

- 6.4.17 Southern Champion Tray, L.P.

- 6.4.18 Klabin S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)