|

市場調查報告書

商品編碼

2063713

英國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)United Kingdom Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

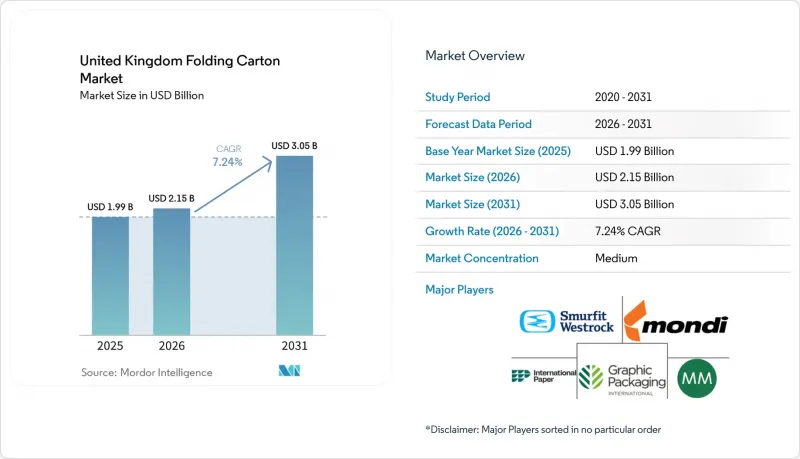

據 Mordor Intelligence 稱,2025 年英國折疊式紙盒市場價值 19.9 億美元,預計到 2031 年將從 2026 年的 21.5 億美元成長到 30.5 億美元,預測期(2026-2031 年)複合年成長率為 7.24%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙板、未漂白塗佈牛皮紙等)、印刷技術(膠印、柔版印刷、數位印刷、凹版印刷等)和終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)進行細分。市場預測以美元計價。

英國折疊式紙盒市場趨勢與洞察

英國的塑膠包裝稅正在加速淘汰一次性塑膠製品。

2026年4月,含再生塑膠比例低於30%的包裝稅率提高至每噸228.82英鎊(291美元),這立即增加了帶有塑膠窗口和阻隔膜的混合紙盒的合規成本,促使品牌商重新設計包裝,轉向單一材料紙板解決方案。自2027年4月起,將引入化學回收塑膠的物料平衡配額制度,預計這將減輕負擔,但額外的審計負擔可能會繼續推動向纖維材料的轉變。在冷凍蔬菜和糖果甜點等類別中,分散塗層瓦楞紙板正逐漸被採用,這種紙板既滿足防潮和防油阻隔性,又不影響可回收性。英國稅務海關總署(HMRC)預計,這些政策將使英國包裝中再生塑膠的使用量增加約40%,從而每年減少約20萬噸二氧化碳排放。因此,能夠證明其塑膠使用量接近零的加工商正在逐步擴大其在超級市場和直銷平台上的貨架空間。

電子商務的成長推動了對輕巧、適合郵箱使用的紙箱的需求。

預計2023年至2030年間,歐洲電子商務的二次包裝用量將成長45%,是整體包裝需求成長的四倍。高度小於25毫米的郵箱相容包裝規格可以減少投遞失敗率並控制物流排放,但需要在緩衝性能和材料用量之間取得平衡。在英國的履約中心,尺寸合適的自動化設備和動態包裝尺寸設定已成為標準配置,使加工商能夠在24小時內交貨客製化的瓦楞紙板坯料。歐盟即將推出的新規將團體包裝和電商包裝的空隙率限制在50%以內,加劇了英國經銷商跨境貿易的迫切性。這也進一步推動了輕質折疊式瓦楞紙板的應用,這種紙板兼顧了結構強度和可回收性。

原生紙漿價格波動給加工商的利潤率帶來了壓力。

儘管能源和運輸成本不斷上漲,瓦楞紙板價格在2026年初仍持續面臨下行壓力。這主要是由於需求疲軟以及來自亞洲的廉價進口產品。 Graphic Packaging公司2025年的財務表現顯示,由於價格下跌和有意減產,EBITDA獲利率下降至16.2%。除非加工商能夠獲得長期紙漿合約或整合上游工程,否則利潤率的壓力可能會導致其對數位印刷機和阻隔塗層生產線的投資延遲。

細分市場分析

預計到2025年,SBS(固態漂白硫酸漿)將佔據英國折疊式瓦楞紙板市場38.41%的佔有率。這主要歸功於其高白度和醫藥級純度,滿足了嚴格的監管和品牌要求。同時,由於有機食品和牛皮紙食品品牌重視其天然的棕色和食品接觸相容性,預計到2031年,未漂白牛皮紙的複合年成長率將達到6.80%。英國折疊式瓦楞紙板市場的主要驅動力是品牌對永續性的視覺傳達需求,而牛皮紙基材無需二次標籤即可傳遞此訊息。此外,採用FiberLight Tec技術(例如Performa Nova系列)實現的輕量化設計,在保持紙箱抗壓強度的同時,減少了材料用量。

消費者願意為優質環保包裝買單,這推動了冷凍食品和巧克力什錦包裝中未漂白內襯紙的試用,儘管在印刷複雜圖案方面,SBS紙板仍然具有優勢。再生白紋紙板在日用品領域仍具有價格競爭力,但其較低的剛性使其難以打入高階貨架。總體而言,卡夫食品的進展表明,纖維的外觀不再是缺陷,而是一種行銷優勢,這使得未漂白紙板有望在英國折疊式紙盒市場擴大市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速英國塑膠包裝稅框架下一次性塑膠的淘汰進程

- 電子商務的成長推動了對輕便、郵箱大小的瓦楞紙箱的需求。

- 引入數位印刷技術,實現小批量生產並增加 SKU。

- 品牌優質化提高了對高品質包裝盒的需求。

- 投資研發可回收的阻隔塗層,使塑膠層壓板能夠取代瓦楞紙板。

- 政府獎勵,加強國內回收能力,以擴大再生纖維的供應。

- 市場限制因素

- 原生紙漿價格的波動給造紙企業的利潤率帶來了壓力。

- 與食品用軟塑膠包裝袋的競爭。

- 英國白色纖維回收基礎設施的處理能力受限

- 印刷和加工行業技能的缺乏阻礙了數位瓦楞紙板生產的擴張。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊式紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Mayr-Melnhof Karton AG

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Saica Group

- Coveris Holdings SA

- Qualvis Print & Packaging Ltd

- Glossop Cartons Ltd

- Curtis Print & Packaging Ltd

- The Alexir Partnership Ltd

- Benson Box Holdings Ltd

- Multi Packaging Solutions International Ltd

- Cepac Ltd

- BoxMart Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom folding carton market size was valued at USD 1.99 billion in 2025 and is estimated to grow from USD 2.15 billion in 2026 to reach USD 3.05 billion by 2031, at a CAGR of 7.24% during the forecast period (2026-2031).

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Folding Carton Market Trends and Insights

Accelerated Phase-Out of Single-Use Plastics Under the UK Plastic Packaging Tax

The April 2026 tax hike to GBP 228.82 (USD 291) per tonne on packaging containing less than 30% recycled plastic has raised immediate compliance costs for hybrid carton with plastic windows or barrier films, prompting brand owners to redesign packs in favor of mono-material board solutions. From April 2027, a mass-balance allowance for chemically recycled plastic will provide relief, but the additional auditing burden is likely to keep the momentum of fiber substitution intact. Categories such as frozen vegetables and confectionery have begun migrating from plastic pouches to dispersion-coated carton that meet moisture and grease barriers without compromising recycling yields. HM Revenue and Customs expects the policy mix to lift recycled plastic use in UK packaging by roughly 40%, saving nearly 200,000 t of CO2 annually. Converters that can certify near-zero plastic inputs are therefore winning incremental shelf space in supermarkets and on direct-to-consumer platforms.

E-Commerce Growth Fueling Demand for Lightweight Letterbox-Friendly Carton

Secondary packaging volumes for European e-commerce are projected to climb 45% between 2023 and 2030, outpacing overall packaging demand by a factor of four. Letterbox-compatible formats under 25 mm in height reduce delivery failures and curb logistics emissions, but still need to balance cushioning with material minimization. Right-sizing automation and dynamic pack-dimensioning have become standard investments at UK fulfillment centers, enabling converters to deliver custom carton blanks in 24 hours. Upcoming EU rules capping empty space to 50% for grouped and e-commerce packs add cross-border urgency for UK sellers, reinforcing the adoption of lightweight folding cartonboard that delivers both structural integrity and recyclability.

Volatility in Virgin Pulp Prices Squeezing Converter Margins

Cartonboard prices stayed under downward pressure through early 2026, even as energy and transport costs climbed, reflecting soft demand and discount imports from Asia. Graphic Packaging's FY 2025 results showed EBITDA margins slipping to 16.2% on weaker pricing and deliberate production curtailments. Unless converters secure long-term pulp contracts or integrate backward, margin squeeze risks delaying capex on digital presses and barrier-coating lines.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Digital Printing for Short Runs and SKU Proliferation

- Brand Premiumization Raising Demand for High-Quality Graphic Carton

- Investments in Recyclable Barrier Coatings Enabling Carton Replacement of Plastic Laminates

- Government Incentives for Domestic Recycling Capacity Boosting Supply of Recycled Fiber

- Competition From Flexible Plastic Pouches for Food Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid Bleached Sulfate captured 38.41% of the United Kingdom folding carton market in 2025, thanks to its high whiteness and pharmaceutical-grade purity, which meet stringent regulatory and branding requirements. Coated Unbleached Kraft is on track for a 6.80% CAGR to 2031 as organic and craft food brands embrace its natural brown hue and food-contact compliance. The United Kingdom folding carton market benefits from brands seeking visible sustainability cues, and kraft substrates deliver that message without secondary labeling. In addition, lighter grammages enabled by FiberLight Tec technology in grades such as Performa Nova trim material inputs while maintaining box compression strength.

Consumer willingness to pay for premium, eco-friendly packaging is fueling trials of unbleached liners in frozen meals and chocolate assortments, although printability trade-offs still favor SBS for intricate graphics. Recycled White Line Chipboard remains a price fighter in household goods, yet limited stiffness bars it from premium shelves. Overall, Kraft's advance signals that visible fiber identity is now a marketing feature, not a defect, positioning unbleached grades to lift unit share within the UK folding carton market.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Mayr-Melnhof Karton AG

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Saica Group

- Coveris Holdings S.A.

- Qualvis Print & Packaging Ltd

- Glossop Cartons Ltd

- Curtis Print & Packaging Ltd

- The Alexir Partnership Ltd

- Benson Box Holdings Ltd

- Multi Packaging Solutions International Ltd

- Cepac Ltd

- BoxMart Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Phase-Out of Single-Use Plastics Under the UK Plastic Packaging Tax

- 4.2.2 E-Commerce Growth Fueling Demand for Lightweight Letterbox-Friendly Carton

- 4.2.3 Adoption of Digital Printing for Short Runs and SKU Proliferation

- 4.2.4 Brand Premiumization Raising Demand for High-Quality Graphic Carton

- 4.2.5 Investments in Recyclable Barrier Coatings Enabling Carton Replacement of Plastic Laminates

- 4.2.6 Government Incentives for Domestic Recycling Capacity Boosting Supply of Recycled Fiber

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin Pulp Prices Squeezing Converter Margins

- 4.3.2 Competition From Flexible Plastic Pouches for Food Products

- 4.3.3 Capacity Constraints in UK White-Fiber Recycling Infrastructure

- 4.3.4 Skill Shortages in Print and Converting Labor Limiting Scaling of Digital Carton Production

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-Commerce and Retail-Ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Graphic Packaging International, LLC

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 Mondi plc

- 6.4.5 International Paper Company

- 6.4.6 Stora Enso Oyj

- 6.4.7 Saica Group

- 6.4.8 Coveris Holdings S.A.

- 6.4.9 Qualvis Print & Packaging Ltd

- 6.4.10 Glossop Cartons Ltd

- 6.4.11 Curtis Print & Packaging Ltd

- 6.4.12 The Alexir Partnership Ltd

- 6.4.13 Benson Box Holdings Ltd

- 6.4.14 Multi Packaging Solutions International Ltd

- 6.4.15 Cepac Ltd

- 6.4.16 BoxMart Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)