|

市場調查報告書

商品編碼

2063712

德國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

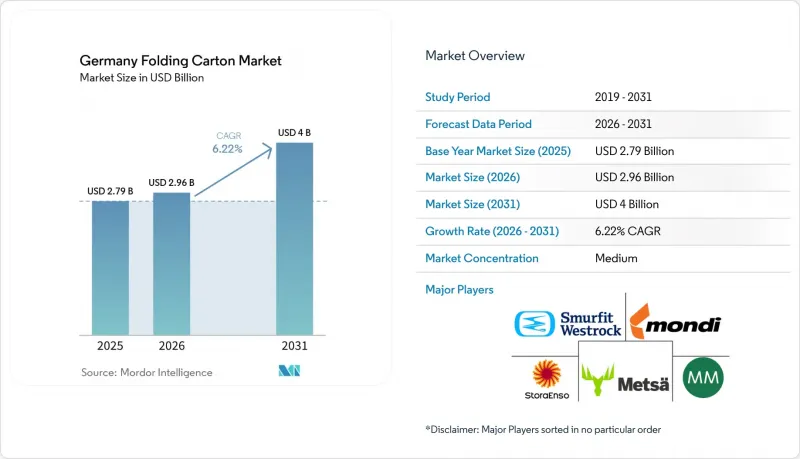

根據 Mordor Intelligence 預測,德國折疊式紙盒市場預計將從 2025 年的 27.9 億美元成長到 2026 年的 29.6 億美元,到 2031 年達到 40 億美元,2026 年至 2031 年的複合年成長率預計為 6.22%。

本報告按材料類型(固態漂白硫酸漿、折疊紙盒用紙板、未漂白塗佈牛皮紙等)、印刷技術(膠印、柔版印刷、數位印刷、凹版印刷等)和終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)進行細分。市場預測以美元計價。

德國折疊式紙盒市場的趨勢與洞察

食品飲料產業對永續包裝的需求日益成長

食品飲料製造商正加速從多層薄膜包裝轉向纖維紙盒,以滿足零售商的永續性評估標準和消費者對易於回收包裝的期望。檢驗的生命週期評估 (LCA) 數據顯示,2021 年至 2024 年間,每噸紙盒的化石二氧化碳當量排放量減少了 8%,這促使採購決策將包裝與範圍 3 的脫碳承諾掛鉤。德國乳製品和烘焙品牌在其年度 ESG 報告中重點強調了這些成果,將紙盒的採用轉化為一項可推廣的氣候變遷減緩成就。該產業在歐洲的回收率已達 87%,超過了德國包裝回收法 (VerpackG) 的目標,並有望達到 90%。這使得紙盒在使用後的基礎設施方面比柔軟性塑膠更具優勢。能夠出具第三方審核的產銷監管鏈 (CoC) 文件的加工商也在注重成本的自有品牌管道中獲得了訂單。這是因為零售商將透明的數據視為避免未來因「綠色清洗」(偽造環境聲明)而遭受罰款的保障。

政府法規鼓勵使用可回收材料

德國的「生產者延伸責任制」(EPR)下,難以回收的包裝包裝方法收費大幅上漲,這使得單一材料折疊式紙盒在整體系統成本方面更具優勢。歐盟將於2026年8月起禁止在食品接觸包裝中使用全氟烷基和多氟烷基物質(PFAS),這將消除含氟聚合物塗層薄膜的決定性性能優勢,迫使加工商採用水性或生物聚合物塗層,以在不使用含氟化學品的情況下保持耐油性。那些早期與化學品製造商合作實施無PFAS解決方案的公司,如今已獲得批准的生產能力,並正在製定溢價。除了國內法規外,歐盟的包裝和包裝廢棄物法規還規定,到2030年,市場上所有包裝都必須可回收利用,除非化學回收規模擴大,否則大多數多層軟性包裝結構將退出市場。積極應對這些法規的德國加工商已與希望避免在2020年代中期進行成本高昂的包裝轉換的跨國快餐連鎖店簽訂了長期合約。

再生纖維價格波動

2025年4月,出口需求下降和國內回收量減少的雙重影響導致再生紙價格每噸上漲20-30歐元(22-33美元),擠壓了加工商在含再生紙等級產品上的利潤空間。折疊式紙板和白紙塑合板的合約價格上限迫使中型加工商承擔暫時性虧損,導致其可自由支配的資本投資減少。現貨市場波動影響了供應鏈負責人的預測準確性,促使品牌所有者透過採購不同原料(包括原生和再生原料)來分散風險。大規模集團透過自有紙漿生產線減輕了價格波動的影響,而獨立的德國加工商則面臨採購風險和複雜的長期生產力計畫。纖維價格的持續波動仍然是德國折疊式紙盒市場最難預測的阻礙因素。

細分市場分析

未漂白塗佈牛皮紙市場佔有率的成長反映了快餐店和工業供應商擴大採用天然棕色纖維,將其作為永續性的視覺象徵。該規格預計年複合成長率達7.18%,使其成為德國折疊式板市場材料成長的主要引擎。斯道拉恩索等供應商在輕量化方面的進步,已將紙張重量擴大至205-310克/平方米,從而在不影響剛性的前提下降低了物流成本。相較之下,固態漂白硫酸漿在高檔巧克力和香水禮盒中仍保持著其高階地位,但隨著品牌所有者在追求光澤潔白的同時兼顧脫碳承諾,其成長速度正在放緩。雖然Whiteline塑合板價格具有競爭力,但隨著再生紙價格指數飆升,其利潤率面臨壓力,凸顯了先前已指出的價格波動限制。折疊紙盒紙板仍佔34.91%的核心市場佔有率,兼顧了印刷性和成本,但其市場佔有率正逐漸被牛皮紙托盤蠶食,後者質地自然,更能滿足功能需求。在德國折疊式紙盒市場,特種金屬化紙板仍屬於小眾產品,主要用於冷凍主菜和家用刀具包裝盒,這些產品需要雙面阻隔性,但單價可以接受。

第二代塗佈生產線直接在牛皮紙基材上塗覆防水、防油、防油脂塗層,無需額外的複合工序,從而縮短了生產週期。 Meyer-Mellnhof 的生命週期審計量化結果顯示,與歐洲平均生產水準相比,碳排放減少了 16% 至 30%,加工商可以在為品牌所有者進行 RFP 評估時使用這些數據。隨著碳排放會計法規的日益嚴格,德國折疊式紙盒市場對具有從原料開採到最終交付全程透明檢驗以及使用壽命結束後可回收利用的產品的需求不斷成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 食品飲料產業對永續包裝的需求日益成長

- 政府法規促進可再生資源

- 電子商務領域的擴張

- 數位印刷客製化技術的進步

- 品牌擁有者對優質化的日益重視

- 向輕量化轉型以提高物流效率

- 市場限制因素

- 再生纖維價格波動

- 與軟質塑膠包裝的競爭

- 對先進印刷機進行大量資本投資

- 特種塗料供應鏈中斷

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊式紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- Mondi plc

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Metsa Board Corporation

- Graphic Packaging Holding Company

- Klingele Paper & Packaging Group

- Edelmann Group

- Thimm Group

- Schumacher Packaging GmbH

- Faller Packaging GmbH

- Model AG

- Rondo Ganahl AG

- All4Labels Group GmbH

- Christiansen Print GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany folding carton market size is expected to increase from USD 2.79 billion in 2025 to USD 2.96 billion in 2026 and reach USD 4.00 billion by 2031, growing at a CAGR of 6.22% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Folding Carton Market Trends and Insights

Growing Demand For Sustainable Packaging In Food And Beverage

Food and beverage producers are accelerating the switch from multilayer films to fiber-based carton to satisfy retailer sustainability scorecards and consumer expectations for readily recyclable packaging. Verified lifecycle-assessment data shows an 8% drop in fossil CO2 equivalent per tonne of carton between 2021 and 2024, reinforcing procurement decisions that link packaging to Scope 3 decarbonization commitments. German dairies and bakery brands highlight these gains in annual ESG reports, translating carton adoption into marketable climate credentials. The sector's 87% European recycling rate already surpasses the VerpackG target and is moving toward 90%, giving carton an end-of-life infrastructure advantage over flexible plastics. Converters capable of issuing third-party-audited chain-of-custody documents now win volume even in cost-sensitive private-label channels because retailers view transparent data as insurance against future greenwashing fines.

Government Regulations Encouraging Recyclable Materials

Extended producer-responsibility fees under the German Packaging Act rise sharply for formats deemed hard to recycle, tilting total system costs in favor of mono-material folding carton. The August 2026 EU ban on PFAS in food-contact packaging removes a critical barrier performance edge that fluoropolymer-coated films held, compelling converters to adopt water-based or bio-polymer coatings that preserve oil resistance without fluorinated chemistry. Early movers who partnered with chemical suppliers for PFAS-free solutions now control approved capacity and command premium pricing. On top of national rules, the EU Packaging and Packaging Waste Regulation will require every package on the market to be recyclable by 2030, effectively sidelining most multilayer flexible structures unless chemical recycling scales up. German converters' early compliance secures long-term contracts from multinational quick-service restaurants aiming to avoid costly mid-decade package transitions.

Volatility In Recycled Fiber Prices

Recovered-paper prices spiked by EUR 20-30 (USD 22-33) per tonne in April 2025 when export demand collided with a domestic collection dip, cutting converters' margins on recycled-content grades. Because folding boxboard and white-line chipboard carry contract ceilings on price pass-through, mid-tier converters absorbed temporary losses, which curbed discretionary capital spending. Spot-market swings also destabilized forecast accuracy for supply-chain planners, leading brand owners to hedge their exposure by splitting volumes between virgin and recycled substrates. Larger integrated groups blunted volatility through captive pulp lines, but independent German converters faced procurement risk that complicated long-term capacity planning. Continuing fiber price sensitivity remains the most unpredictable constraint on the German folding carton market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of E-Commerce Sector

- Advancements In Digital Printing Customization

- Competition From Flexible Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coated Unbleached Kraft's share acceleration reflects quick-service restaurants and industrial suppliers embracing natural-brown fibers as visual shorthand for sustainability. The format's 7.18% forecast CAGR positions it as the growth engine of the German folding carton market size for materials. Lightweighting advances from suppliers such as Stora Enso push grammage into the 205-310 g/m2 range, translating into logistics savings without sacrificing stiffness. In contrast, Solid Bleached Sulfate holds premium ground in luxury chocolate and fragrance gift sets, but its uptick slows as brand owners reconcile glossy whiteness with decarbonization pledges. White Line Chipboard, though price-competitive, faces margin pressure when recovered-paper indices surge, underscoring the volatility restraint already noted. Folding Boxboard remains the anchor at 34.91% market share, straddling printability and cost but facing incremental loss to kraft, where natural-look trays meet functional needs. The German folding carton market share for specialty metalized boards remains niche, serving frozen entrees and household blade cartridges that demand dual-side barrier yet accept higher unit prices.

Second-generation coating lines now integrate water-based oil- and grease-resistance directly into kraft substrates, eliminating an extra laminating pass and shortening cycle time. Mayr-Melnhof's lifecycle audit quantifies 16-30% carbon savings compared with average European production, arming converters with data for brand-owner RFP scoring. As carbon accounting tightens, the German folding carton market gravitates toward grades that offer verified cradle-to-gate transparency and end-of-life recyclability.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Mondi plc

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Metsa Board Corporation

- Graphic Packaging Holding Company

- Klingele Paper & Packaging Group

- Edelmann Group

- Thimm Group

- Schumacher Packaging GmbH

- Faller Packaging GmbH

- Model AG

- Rondo Ganahl AG

- All4Labels Group GmbH

- Christiansen Print GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Sustainable Packaging in Food and Beverage

- 4.2.2 Government Regulations Encouraging Recyclable Materials

- 4.2.3 Expansion of E-commerce Sector

- 4.2.4 Advancements in Digital Printing Customization

- 4.2.5 Rising Brand Owner Focus on Premiumization

- 4.2.6 Shift Toward Lightweighting for Logistics Efficiency

- 4.3 Market Restraints

- 4.3.1 Volatility in Recycled Fiber Prices

- 4.3.2 Competition from Flexible Plastic Packaging

- 4.3.3 High Capital Expenditure for Advanced Printing Presses

- 4.3.4 Supply-Chain Disruptions for Specialty Coatings

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Mondi plc

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 Stora Enso Oyj

- 6.4.5 Metsa Board Corporation

- 6.4.6 Graphic Packaging Holding Company

- 6.4.7 Klingele Paper & Packaging Group

- 6.4.8 Edelmann Group

- 6.4.9 Thimm Group

- 6.4.10 Schumacher Packaging GmbH

- 6.4.11 Faller Packaging GmbH

- 6.4.12 Model AG

- 6.4.13 Rondo Ganahl AG

- 6.4.14 All4Labels Group GmbH

- 6.4.15 Christiansen Print GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)