|

市場調查報告書

商品編碼

2063711

法國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)France Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

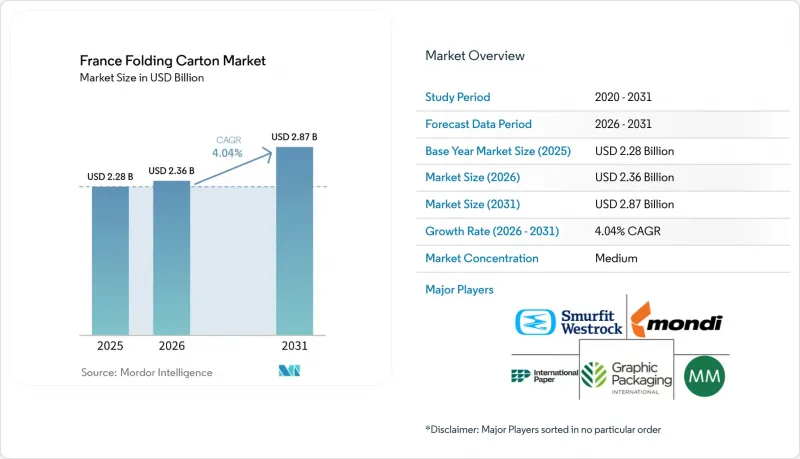

根據 Mordor Intelligence 預測,法國折疊式紙匣市場規模將從 2025 年的 22.8 億美元成長到 2026 年的 23.6 億美元,到 2031 年將達到 28.7 億美元,2026 年至 2031 年的複合年預計成長率為 4.04%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙盒用紙板、未漂白塗佈牛皮紙等)、印刷技術(膠印、柔版印刷、數位印刷、凹版印刷等)和終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)進行細分。市場預測以美元計價。

法國折疊式紙盒市場的趨勢與洞察

禁止使用一次性塑膠製品,改用紡織包裝。

法國已設定目標,力爭在2025年前減少一次性塑膠的使用,並制定了全面的淘汰藍圖圖,目標是在2040年前逐步淘汰一次性塑膠。歐盟法規也施加了進一步的壓力,該法規將於2026年8月12日生效,強制要求到2030年,歐盟境內銷售的所有包裝都必須具備經濟可回收性。因此,品牌商正在重新設計包裝,將多層薄膜包裝替換為單一材料的瓦楞紙包裝,用於糖果甜點重疊包裝、調理食品餐盒和個人保健產品套袋。雀巢法國公司已將部分糖果甜點改用瓦楞紙套袋包裝,以降低合規風險並提升產品在商店的吸引力。目前,加工商的研發重點是水性塗料、聚乙烯醇(PVOH)分散體和纖維素基阻隔材料,這些材料能夠在高蒸汽環境下保持良好的可回收性。隨著監管合規期限的臨近,基材創新正從實驗室規模走向商業印刷,提高了每噸價值,並鞏固了法國在法國折疊式紙盒市場的高階地位。

電子商務和配送服務的成長

2024年,法國電子商務市場規模達1,753億歐元(1,981億美元),62%的消費者每月至少網路購物一次。零售商目前指定使用折疊式瓦楞紙箱,這種紙箱既可用作最後一公里配送包裝,也可用作商店展示,其特點是加固邊角、可拆卸前板和整合提手。雖然這種混合包裝形式縮短了門市補貨時間,並提高了到貨時的品牌識別度,但同時也需要較小的印刷量和頻繁的設計修改。數位印刷機可以在幾分鐘內完成圖案更換,使加工商能夠根據季節性宣傳活動客製化外包裝箱,同時保持基本批量印刷所需的膠印工藝。同時,法國郵政(La Poste)和法國時運公司(Chronoposte)等快遞公司正在收緊體積重量限制,迫使企業採用合適的尺寸,並增加了對小尺寸空白紙箱的需求。這也進一步推動了法國折疊式瓦楞紙箱市場的發展。

原生紙漿和再生紙價格的波動

由於北歐紙漿和再生紙價格暴跌,下游客戶紛紛削減庫存,法國紙板製造商撤回了原定於2025年宣布的兩項提價計畫。 2026年4月,索諾科宣布,無塗布再生紙板價格每噸上漲80歐元(90美元),紙管和紙芯產品價格上漲8%,理由是能源和化學產品價格飆升。這些價格波動給加工商帶來了壓力,儘管他們多年來的短纖維紙漿(SBS)採購量固定,但仍需應對每季紙漿價格的調整。到2025年底,缺乏對沖手段的小規模家族式工廠累計虧損,合約被垂直整合的競爭對手搶走,原計劃的設備升級被推遲,法國折疊式板市場的產能擴張也受到限制。

細分市場分析

法國折疊式紙板市場中,固態漂白硫酸紙漿的市場規模預計將以5.19%的複合年成長率成長,其價值將主要來自高階化妝品、藥品和高級糖果甜點等應用領域。到2025年,折疊式紙板將保持其在法國折疊式紙盒市場42.25%的佔有率。這是因為在穀物、冷凍食品和家用清潔劑等領域,成本和供應比白度更為重要。在有機食品領域,棕色纖維的質感迎合了自然的生活方式,因此對塗佈未漂白牛皮紙的需求日益成長。同時,在玩具和DIY金屬製品產品領域,白色塑合板仍然是一種低成本的選擇。北歐供應商計劃在2027年運作95萬噸新的SBS和FBB產能,這將使法國加工商能夠規避北美供應短缺和前置作業時間縮短的風險。這款創新產品將紙張重量從 350 克/平方米降低到 280 克/平方米,在不影響抗壓強度的前提下進一步減少了材料的使用,符合獎勵輕量化設計的環境貢獻累積機制。

同時加工通用和高階瓦楞紙板的加工商正巧妙地利用兩極化的原料市場。 Smurfit Westrock公司在SBS等級紙板的前置作業時間方面面臨長期限制,迫使一些品牌不得不從歐洲多家造紙廠採購。同時,Meyer Melnhoff公司在2025年上半年於法國的銷售額達到4.367億歐元(約4.94億美元),該公司警告稱,庫存調整壓力將影響折疊式瓦楞紙板的出貨量。在不同等級之間柔軟性切換SKU是法國折疊式紙盒市場服務競爭力的基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 禁止使用一次性塑膠製品,改用紡織包裝。

- 電子商務和配送服務的成長

- 對高檔包裝食品和化妝品的需求不斷成長

- 數位印刷和柔版印刷技術的進步

- 推出帶有QR碼。

- 擴大模塑纖維阻隔塗層在冷藏食品的應用規模。

- 市場限制因素

- 原生紙漿和再生紙價格的波動

- 與軟塑膠的競爭

- 法國加工廠生產能力受限

- 對 MOSH/MOAH 的合規要求更加嚴格

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊式紙盒用紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- Graphic Packaging Holding Company

- International Paper Company

- Mayr-Melnhof Karton AG

- Mondi plc

- Stora Enso Oyj

- Metsa Board Corporation

- Sonoco Products Company

- Holmen AB(Iggesund Paperboard)

- Saica Group

- Autajon Group

- Groupe Rossmann

- Hinojosa Packaging Group

- Allard Emballages SAS

第7章 市場機會與未來展望

According to Mordor Intelligence, the france folding carton market size is expected to increase from USD 2.28 billion in 2025 to USD 2.36 billion in 2026 and reach USD 2.87 billion by 2031, growing at a CAGR of 4.04% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Folding Carton Market Trends and Insights

Ban on Single-Use Plastics and Shift to Fiber-Based Packaging

France set a 20% reduction target for single-use plastics by 2025, backed by a comprehensive phase-out roadmap toward 2040. The European Union regulation, which comes into force on 12 August 2026, intensifies pressure by requiring all packaging sold in the bloc to be economically recyclable by 2030. Brand owners are therefore re-engineering multilayer films into mono-material carton solutions for confectionery overwraps, ready-meal trays, and personal-care sleeves. Nestle France has already switched several confectionery SKUs to carton sleeves, citing reduced compliance risks and gains in shelf appeal. Converter R&D now focuses on aqueous coatings, PVOH dispersions, and cellulose-based barriers that can withstand high-water-vapor environments without compromising recyclability. As compliance deadlines loom, substrate innovations are migrating from lab scale to commercial print runs, lifting value per tonne and reinforcing the premium position of the French folding carton market.

Growth of E-Commerce and Delivery Services

E-commerce in France generated EUR 175.3 billion (USD 198.1 billion) during 2024, and 62% of consumers shop online at least monthly. Retailers now specify folding carton that work as both last-mile shipping containers and shelf-ready displays, combining reinforced corners, peel-away fronts, and integrated handles. These hybrid formats shorten store replenishment times and boost brand visibility on arrival, but they require shorter print runs and frequent artwork revisions. Digital presses can swap graphics in minutes, letting converters tailor outer carton for seasonal campaigns while holding litho for base volumes. Carriers such as La Poste and Chronopost are simultaneously tightening dimensional weight rules, which forces right-sizing and drives unit growth for smaller blank sizes, further supporting the French folding carton market.

Volatility in Virgin Fiber and Recovered Paper Prices

French cartonboard producers withdrew listed price increases twice in 2025 after downstream customers destocked inventories in response to sharply falling Nordic pulp and recovered-paper quotations. In April 2026, Sonoco announced an EUR 80 (USD 90) per tonne rise for uncoated recycled paperboard alongside an 8% uplift for tube and core products, citing energy and chemical inflation. Such swings squeeze converters that lock in multi-year SBS volumes yet still face quarterly pulp resets. Smaller family-owned plants, lacking hedging tools, reported negative margins in late 2025 and lost contracts to vertically integrated rivals, delaying planned machinery upgrades and constraining capacity additions within the French folding carton market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Premium Packaged Food and Cosmetics

- Advances in Digital and Flexographic Printing

- Competition From Flexible Plastic Pouches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The France folding carton market size for solid bleached sulfate is projected to expand at a 5.19% CAGR, capturing incremental value from luxury cosmetics, pharmaceuticals, and gourmet confectionery applications. Folding boxboard retained 42.25% France folding carton market share in 2025 because cereals, frozen meals, and household cleaners prioritize cost and availability over brightness. Demand for coated unbleached kraft is rising in organic food segments that communicate natural positioning through a brown-fiber aesthetic, while white line chipboard remains the low-cost option for toys and DIY hardware. Nordic suppliers are bringing 950,000 tonnes of new SBS and FBB capacity online by 2027, allowing French converters to hedge against North American supply tightness and slim lead times. Lighter-basis-weight innovations, dropping from 350 GSM to 280 GSM, further lower material use without compromising compression strength, aligning with eco-contribution fee structures that reward low-mass designs.

Converters that straddle commodity and premium lines exploit the bifurcated substrate landscape. Smurfit Westrock has recurring lead-time constraints on SBS grades, which pushes some brands to dual source with European mills, while Mayr-Melnhof recorded EUR 436.7 million (USD 494 million) in France sales for H1 2025 yet warned of destocking pressure that hit folding boxboard volumes. The flexibility to switch SKUs between grades underpins service competitiveness in the France folding carton market.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Graphic Packaging Holding Company

- International Paper Company

- Mayr-Melnhof Karton AG

- Mondi plc

- Stora Enso Oyj

- Metsa Board Corporation

- Sonoco Products Company

- Holmen AB (Iggesund Paperboard)

- Saica Group

- Autajon Group

- Groupe Rossmann

- Hinojosa Packaging Group

- Allard Emballages SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ban on Single-Use Plastics and Shift to Fiber-Based Packaging

- 4.2.2 Growth of E-Commerce and Delivery Services

- 4.2.3 Rising Demand for Premium Packaged Food and Cosmetics

- 4.2.4 Advances in Digital and Flexographic Printing

- 4.2.5 Adoption of Smart Anti-Counterfeit Inks and QR-Coded Carton

- 4.2.6 Scaling of Molded Fiber Barrier Coatings for Chilled Meals

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin Fiber and Recovered Paper Prices

- 4.3.2 Competition From Flexible Plastic Pouches

- 4.3.3 Capacity Constraints in French Converting Plants

- 4.3.4 Stricter MOSH/MOAH Compliance Requirements

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-Commerce and Retail-Ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Graphic Packaging Holding Company

- 6.4.3 International Paper Company

- 6.4.4 Mayr-Melnhof Karton AG

- 6.4.5 Mondi plc

- 6.4.6 Stora Enso Oyj

- 6.4.7 Metsa Board Corporation

- 6.4.8 Sonoco Products Company

- 6.4.9 Holmen AB (Iggesund Paperboard)

- 6.4.10 Saica Group

- 6.4.11 Autajon Group

- 6.4.12 Groupe Rossmann

- 6.4.13 Hinojosa Packaging Group

- 6.4.14 Allard Emballages SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)