|

市場調查報告書

商品編碼

2063710

義大利折疊式紙盒:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Italy Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

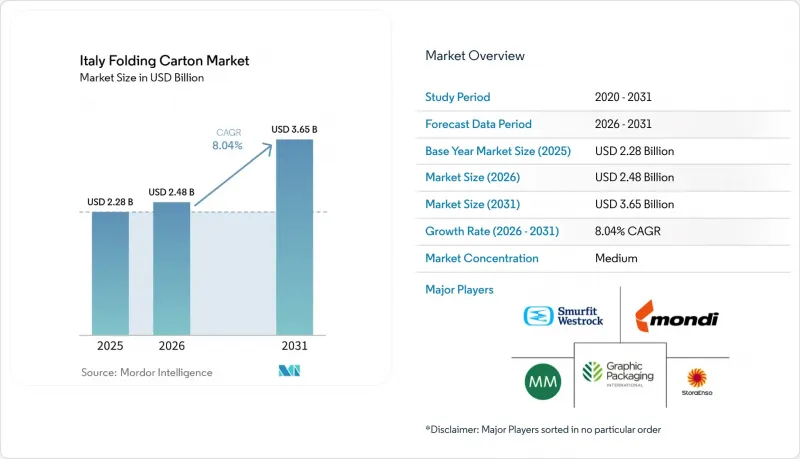

根據 Mordor Intelligence 預測,義大利折疊式紙匣市場規模將從 2025 年的 22.8 億美元成長到 2026 年的 24.8 億美元,到 2031 年將達到 36.5 億美元,2026 年至 2031 年的複合年預計成長率為 8.04%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙板、塗佈未漂白牛皮紙、白線塑合板等)、印刷技術(膠印、柔版印刷、數位印刷等)和終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品等)進行細分。市場預測以價值(美元)表示。

義大利折疊式紙盒市場的趨勢與洞察

人們越來越偏好可回收包裝

CONAI的延伸生產者責任制(EPR)費用對不可回收的結構進行處罰,促使品牌所有者迅速用單一材料瓦楞紙箱取代貼合加工塑膠,因為後者適用較低的關稅。消費者調查顯示,77%的義大利人在購買決策中會考慮包裝的永續性,促使零售商優先銷售標明處理方法明確的SKU。 Fedrigoni計劃在2025年前投資Papkot,這表明加工商正在將符合可回收性指南且保持耐油性的無PFAS塗層商業化。國家回收計畫撥款15億歐元(17億美元)用於回收中心和數位化追溯系統,一旦運作,將增加廢棄紡織品的供應。這些因素表明,至少到2031年,對基礎材料的需求將保持在市場平均以上。

高階快速消費品的成長

高階食品、飲料和化妝品品牌正擴大採用耐燙金、壓花和柔觸上光工藝的固態漂白硫酸漿(SBS)和鍍金屬紙板。價值25億歐元(28.3億美元)的調理食品餐盒需要耐油且可微波加熱的瓦楞紙板,其價格比普通瓦楞紙板高出兩位數。儘管自有品牌零售商的市場滲透率在2024年達到了32%,但超級市場正透過改進包裝設計來凸顯其在高階市場的差異化優勢。採用線上分光光度計和自動化檢測設備(例如博斯特的QualiTronic系統)的加工商能夠滿足高階品牌對色彩精準度的更高要求。隨著自由裁量權支配支出的復甦,預計高檔包裝盒的出貨量成長速度將超過義大利整體折疊式紙盒市場的成長速度。

原生紙漿價格波動

2024年,牛皮紙襯紙價格上漲超過20%,北歐漂白軟木漿價格也上漲了17.6%。由於價格轉嫁條款落後現貨價格長達90天,加工業者的利潤空間受到擠壓。強制性再生紙含量規定加劇了再生紙市場的競爭,預計2025年義大利北部再生紙的平均價格將達到每噸120至150歐元(136至170美元)。南部地區較低的再生紙回收率迫使造紙商將紙包從北向南運輸,增加了物流成本。雖然像RDM和Burgo這樣的垂直整合集團透過自有紙漿和脫墨設施來規避價格波動風險,但許多中小企業仍只能被動承受價格上漲,這抑制了投資意願。

細分市場分析

到2025年,折疊紙板將佔義大利折疊式紙盒市場38.56%的佔有率。這主要歸功於其在主流食品應用中兼具的剛性、印刷性和成本優勢。隨著化妝品和製藥品牌對適用於燙金、壓花和阻隔塗層等製程的高光澤表面的需求,預計固態漂白硫酸紙漿的複合年成長率將達到9.21%。由再生纖維製成的Whiteline塑合板在電子產品和家居用品行業的需求不斷成長,因為在這些行業中,表面美觀性並非首要考慮因素。 RDM公司將於2026年推出的「Vincicoat PLUS」產品,在強度提升15-20%的同時,也採用了85%的再生纖維,展現了向輕量化和循環利用基材發展的創新路徑。

製造商正在重組其造紙廠,以生產高比例再生纖維的產品,力爭在PPWR(義大利紙盒製造商協會)設定的30%再生纖維目標之前實現。預計這一轉變將重塑提供檢驗的閉合迴路纖維的造紙廠的採購格局。競爭的焦點正轉向能夠保持可回收性的塗層,Papkot公司的奈米結構襯紙在保持耐油性的同時,提供了一種替代PFAS(全氟烷基和多氟烷基物質)的選擇。非纖維素層含量低於5%的基材屬於CONAI(義大利紙盒製造商協會)的最低價格等級,促使買家轉向分散塗層和生物基替代品。隨著品牌所有者揭露其碳足跡,能夠提供生產階段排放數據的製造商在採購中受到優先考慮,從而強化了一個良性循環,支持義大利折疊式紙盒市場中高可回收等級產品的發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人們越來越偏好可回收包裝

- 快速消費品高階定位產品的成長

- 電子商務和小訂單的快速成長

- 品牌所有者從塑膠到紙板的轉型

- 義大利即食食品市場的擴張

- 零售商對可直接上架的多包裝產品的需求

- 市場限制因素

- 原生紙漿價格波動

- 高階數位印刷機的資本密集特性

- 義大利南部缺乏折疊式紙盒回收基礎設施

- 中小企業遵守嚴格的食品接觸法規的成本。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 可折疊紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit WestRock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International LLC

- International Paper Company

- RDM Group

- GPack Group

- Lucaprint Group

- Box Marche SpA

- Pozzoli SpA

- Burgo Group SpA

- Metsa Board Corporation

- Schur Pack Italy Srl

- Stora Enso Oyj

- Fedrigoni Group

- Seda International Packaging Group SpA

- Artigrafiche Reggiane & Lai SpA

- Italpack Cartons Srl

- Mondi plc

第7章 市場機會與未來展望

According to Mordor Intelligence, the italy folding carton market size is expected to increase from USD 2.28 billion in 2025 to USD 2.48 billion in 2026 and reach USD 3.65 billion by 2031, growing at a CAGR of 8.04% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Italy Folding Carton Market Trends and Insights

Increasing Preference for Recyclable Packaging

Extended Producer Responsibility fees imposed by CONAI penalize non-recyclable structures, so brand owners are rapidly substituting laminated plastics with mono-material cartons that qualify for lower tariffs. Consumer polling shows that 77% of Italians factor packaging sustainability into their purchase decisions, prompting retailers to favor SKUs with clear disposal labels. Fedrigoni's 2025 investment in Papkot demonstrates how converters are commercializing PFAS-free coatings that pass recyclability guidelines while retaining grease resistance. The national recovery plan earmarks EUR 1.5 billion (USD 1.70 billion) for reuse centers and digital traceability, which will raise post-consumer fiber availability once projects come online. These factors are expected to underpin above-trend substrate demand through at least 2031.

Growth of Premium-Positioned FMCG Products

Premium food, beverage, and cosmetics lines increasingly specify solid bleached sulfate or metalized boards that tolerate hot-foil stamping, embossing, and soft-touch varnishes. Ready-to-eat meal kits valued at EUR 2.5 billion (USD 2.83 billion) require grease-resistant, microwave-safe cartons that command double-digit price premiums over commodity grades. Retail private-label penetration reached 32% in 2024, yet supermarkets differentiate premium tiers through upgraded pack aesthetics. Converters that add inline spectrophotometers and automated inspection, such as Bobst QualiTronic systems, achieve the tighter color tolerances demanded by luxury brands. As discretionary spending recovers, volumes in high-decor segments are expected to outpace the overall Italy folding carton market.

Volatility in Virgin Fiber Pulp Prices

Kraftliner rose more than 20% in 2024, while northern bleached softwood pulp climbed 17.6%, compressing converter margins because pass-through clauses lag spot prices by up to 90 days. Recycled-content mandates intensify competition for recovered paper, which averaged EUR 120-150 (USD 136-170) per tonne in Northern Italy during 2025. Southern regions' lower collection rates force mills to truck bales north-to-south, adding logistics premiums. Vertically integrated groups like RDM and Burgo hedge volatility through captive pulp and deinking capacity, but most SMEs remain price takers, dampening investment appetite.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Boom and Small-Batch Custom Runs

- Brand Owner Migration from Plastics to Paperboard

- Capital-Intensive Nature of High-End Digital Presses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard accounted for 38.56% of the Italian folding carton market size in 2025, favored for balanced stiffness, printability, and cost in mainstream food applications. Solid bleached sulfate is forecast to post a 9.21% CAGR as cosmetics and pharma brands demand high-brightness surfaces compatible with hot-foil, emboss, and barrier coatings. White line chipboard, produced from recycled fibers, is gaining traction in electronics and household goods where surface aesthetics are secondary. RDM's Vincicoat PLUS, launched in 2026, incorporates 85% recycled fibers yet delivers 15-20% greater strength, illustrating the innovation trajectory toward lightweight, circular substrates.

Producers recasting mills for higher recycled-content output are pre-positioning for the PPWR's 30% post-consumer target, a shift expected to realign procurement toward mills offering validated closed-loop fibers. Competitive emphasis is moving to coatings that preserve recyclability, with Papkot's nanostructured liner replacing PFAS while maintaining grease resistance. Substrates with non-cellulosic layers below 5% qualify for CONAI's lowest fee bracket, nudging buyers toward dispersion-coated or bio-based alternatives. As brand owners publish carbon footprints, mills offering cradle-to-gate emissions data gain sourcing preference, reinforcing a virtuous cycle that favors high-recycled-content grades within the Italy folding carton market.

List of Companies Covered in this Report:

- Smurfit WestRock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International LLC

- International Paper Company

- RDM Group

- GPack Group

- Lucaprint Group

- Box Marche SpA

- Pozzoli SpA

- Burgo Group S.p.A.

- Metsa Board Corporation

- Schur Pack Italy Srl

- Stora Enso Oyj

- Fedrigoni Group

- Seda International Packaging Group SpA

- Artigrafiche Reggiane & Lai SpA

- Italpack Cartons Srl

- Mondi plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Preference for Recyclable Packaging

- 4.2.2 Growth of Premium-Positioned FMCG Products

- 4.2.3 E-commerce Boom and Small-Batch Custom Runs

- 4.2.4 Brand Owner Migration From Plastics to Paperboard

- 4.2.5 Expansion of Italy's Ready-to-Eat Meal Segment

- 4.2.6 Retailer Demand for Shelf-Ready Multipacks

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin Fiber Pulp Prices

- 4.3.2 Capital-Intensive Nature of High-End Digital Presses

- 4.3.3 Limited Folding Carton Recycling Infrastructure in Southern Italy

- 4.3.4 Stringent Food-Contact Compliance Costs for SMEs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Graphic Packaging International LLC

- 6.4.4 International Paper Company

- 6.4.5 RDM Group

- 6.4.6 GPack Group

- 6.4.7 Lucaprint Group

- 6.4.8 Box Marche SpA

- 6.4.9 Pozzoli SpA

- 6.4.10 Burgo Group S.p.A.

- 6.4.11 Metsa Board Corporation

- 6.4.12 Schur Pack Italy Srl

- 6.4.13 Stora Enso Oyj

- 6.4.14 Fedrigoni Group

- 6.4.15 Seda International Packaging Group SpA

- 6.4.16 Artigrafiche Reggiane & Lai SpA

- 6.4.17 Italpack Cartons Srl

- 6.4.18 Mondi plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)