|

市場調查報告書

商品編碼

2063354

印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

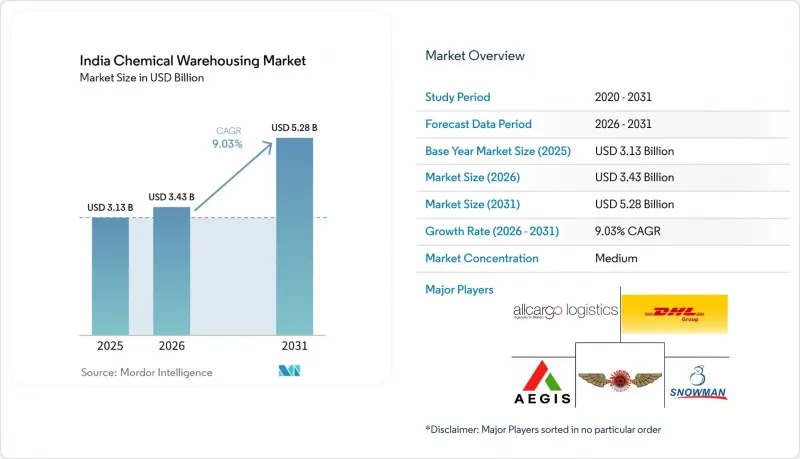

據 Mordor Intelligence 稱,印度化學品倉庫市場預計將從 2025 年的 31.3 億美元成長到 2026 年的 34.3 億美元,到 2031 年達到 52.8 億美元,2026 年至 2031 年的複合年成長率為 9.03%。

庫存擴張主要受以下因素驅動:高達200億美元的特種化學品資本投資、國家物流政策中的成本削減目標,以及縮短港口至內陸地區運輸時間的專用貨運走廊。本報告按倉庫類型(普通倉庫、特殊化學品倉庫、危險品倉庫、溫控化學品倉庫)、化學品類型(易燃液體、腐蝕性物質、有毒物質、氧化劑及其他)和終端用戶行業(基礎化學品製造等)進行細分。市場預測以美元計價。

印度化學品倉庫市場的趨勢與洞察

2024-2028年間,特種化學品領域將迎來200億美元的資本投資浪潮。

隨著生產商向上游工程一體化轉型並追求出口成長,過去幾年投資激增正在重塑區域倉儲需求。例如,戈德拉格工業公司(Godrage Industries)正在其瓦里亞(Varia)工廠投資5,950萬美元,將年產能提升至27.5萬噸,並新增一條特種酒精生產線。塔塔化工(Tata Chemicals)在泰米爾納德邦的坦法克(Tanfak)和拉馬納塔普拉姆(Ramanathapuram)也進行了類似的投資,將新工廠定位在以港口為中心的物流走廊地帶。這些擴張正在將印度的化學品倉儲市場集中到哈吉拉(Hajira)、達赫傑(Dahej)和卡達洛爾(Kaddalore)等地區,這些地區擁有專用鐵路和沿海運輸,縮短了貨物停留時間。同時,營運商面臨原料價格波動和潛在的關稅變化,迫使他們謹慎分階段進行投資。產業預測,到2028年,印度化工產業的規模將達到3,000億美元,這進一步強化了增加危險品(HAZMAT)儲存能力的長期合理性。

國家物流政策:A級危險物品設施的稅收優惠

在州層級,產業政策提供稅收優惠,有效降低了符合《國家建築標準法》消防安全法規和危險物品許可證(PESO)要求的A級倉庫的資本成本。在聯邦層面,統一物流介面平台目前連接了36個政府系統,顯著縮短了港口文件處理週期,減少了貨物停留時間。印度倉儲協會發布的新電子手冊整合了各種法規和標準,降低了開發商的資訊搜尋成本。像Allcargo這樣的營運商正在積極回應,部署配備貨架噴灌和泡沫滅火系統的多危險品倉庫,而三個聯邦政府資助的散裝藥品園區則在分擔部分合規負擔。另一方面,計劃在2025年底前廢除20項化學品品管令,降低了認證成本,並暫時提高了小規模第三方物流供應商的營運利潤率。

提高散裝化學品海運貨物保險附加費。

預計到2025年,紅海和波斯灣航線的戰爭保險保費將上漲15%至30%,將推高進口溶劑的接收成本,並提高信用證的抵押要求。目前,每批價值595萬美元的貨物需要支付約7,800美元的保險費,這給依賴進出口業務的印度化學品倉儲市場營運商的利潤空間帶來了壓力。雖然Aegis透過長期租船合約對沖了部分風險,但小規模的第三方物流公司卻面臨著營運資金緊張的困境,這可能會減緩它們的擴張速度。像瓦達萬港這樣的深水港計畫預計將在2029年後帶來一些緩解,但在此之前,保險費的波動仍將繼續拖累資本配置。

細分市場分析

至2025年,普通倉儲將佔印度化學品倉儲市場的37.47%,主要處理僅需常溫儲存的散裝貨物的配送。儘管普通倉儲佔據主導地位,但對生物製藥、藥物活性成分和溫度敏感催化劑的需求預計將推動溫控化學品倉儲的強勁成長,到2031年複合年成長率將達到12.11%。為了滿足良好分銷規範(GDP)的要求,營運商正擴大採用專用冷藏室、乙二醇冷卻器和隔熱裝卸平台門。 AllCargo佔地16萬平方英尺的鈾倉庫便是這一趨勢的典型例證,該倉庫將低於25°C的儲藏室與防爆照明相結合,是服務於70多家公司的全國性網路的一部分。

配備惰性氣體充裝、高效能空氣過濾器 (HEPA) 和 ISO 9001 工作流程的特殊化學品倉庫正成為市場價值轉移的焦點。哈吉拉 (Hajira) 和達赫傑 (Dahej) 附近的土地價格如今已大幅上漲,開發商競相收購可直達西部專用貨運走廊的鐵路專用線地塊。 Celsius 物流計劃於 2025 年推出的符合 GDP 標準的藥品交叉轉運網路,標誌著低溫運輸和危險品 (HAZMAT) 的融合。同時,實施經認證的消防系統可降低 15-30% 的保險費,這也是獎勵企業從 B 級倉庫升級到 A 級設施的另一個重要因素。這些因素共同為印度化學品倉庫市場的長期擴大策略奠定了基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 特種化學品資本投資將激增200億美元(2024-2028年)

- 國家物流政策:A級危險物品設施的稅收優惠

- Bharatmala貨運走廊的鐵路支線:擴大散裝化學品的內陸運輸通道。

- 鋰離子電池原料的進口正在推動對 3 級和 8 級儲能設備的需求。

- 與農藥生產連結獎勵計畫機制擴大了當地倉庫的需求。

- 基於QR碼的危險廢棄物電子追蹤系統(NHWIS-2025)正在加速數位化WMS的普及。

- 市場限制因素

- 提高散裝化學品海運貨物保險的附加保險費。

- 商業資訊系統 (BIS) 的強制性品管指令正在推高第三方物流供應商的合規成本。

- 由於供不應求不含 PFAS 的滅火系統,倉庫維修被推遲。

- 內河航道吃水深度的波動阻礙了駁船運輸液態化學品。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模及成長預測(價值,10億印度盧比)

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學物質類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料和黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Aegis Logistics Ltd

- Allcargo Logistics

- DHL Group

- Den Hartogh Logistics

- Snowman Logistics Ltd

- Adani Logistics Ltd

- BEST Roadways Ltd.

- Swift Cargo

- IMC Logistics

- Tankstore Ltd

- Noatum Logistics

- Vopak India

- Mahindra Logistics

- Kiran Group

- Apollo Supply Chain

- Seashell Logistics

- DSV

- BDP International

- Yusen Logistics

- Rhenus Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the india chemical warehousing market size is expected to increase from USD 3.13 billion in 2025 to USD 3.43 billion in 2026 and reach USD 5.28 billion by 2031, growing at a CAGR of 9.03% over 2026-2031.

Inventory expansion is being fueled by a USD 20 billion specialty-chemical capital-expenditure wave, the National Logistics Policy's cost-reduction targets, and Dedicated Freight Corridors that shorten port-to-hinterland transit. This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials Warehouses, Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, Others), and by End-User Industry (Basic Chemicals Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Chemical Warehousing Market Trends and Insights

USD 20 Billion Specialty-Chemical CAPEX Wave (2024-28)

A multi-year investment surge is reshaping regional warehouse demand as producers back-integrate and chase export growth Godrej Industries, for example, is injecting USD 59.5 million into its Valia plant to lift capacity to 275,000 tons per year and add specialty alcohol lines. Similar outlays by Tanfac in Tamil Nadu and Tata Chemicals in Ramanathapuram are aligning new plants with port-centric logistics corridors. These expansions draw the India chemical warehousing market toward Hazira, Dahej, and Cuddalore, where rail sidings and coastal shipping compress dwell times. Operators are simultaneously exposed to raw-material volatility and possible tariff shifts, prompting cautious phase-wise spending. Industry forecasts that India's chemicals sector could touch USD 300 billion by 2028 bolster the long-term case for additional HAZMAT capacity.

National Logistics Policy Tax Holidays for Grade A HAZMAT Facilities

State-level industrial policies are offering tax incentives that cut the effective cost of capital for Grade A warehouses that comply with the National Building Code fire-safety schedule and PESO licensing. At the federal level, the Unified Logistics Interface Platform now links 36 government systems to significantly shrink port document cycles and reduce dwell times.A new e-Handbook from the Warehousing Association of India has consolidated codes and standards, lowering search costs for developers. Operators such as Allcargo have responded by rolling out multi-hazard complexes with in-rack sprinklers and foam suppression, while three federally funded Bulk Drug Parks socialize part of the compliance burden.Conversely, the late-2025 rollback of 20 Chemical Quality-Control Orders has lightened certification overhead, temporarily widening operating margins for smaller 3PL providers.

Rising Marine-Cargo Insurance Surcharges on Bulk Chemicals

War-risk premiums on Red Sea and Persian Gulf routes climbed 15-30% in 2025, lifting the landed cost of imported solvents and raising collateral requirements for letters of credit.A single USD 5.95 million cargo now pays nearly USD 7,800 in total cover, eroding throughput margins for India chemical warehousing market operators that rely on import-export flows. Aegis has hedged part of this exposure via long-term charter-party deals, but smaller 3PLs face working-capital squeezes that could delay expansion. Deep-draft projects such as Vadhavan Port promise partial relief post-2029, yet until then, premium volatility remains a drag on capital deployment.

Other drivers and restraints analyzed in the detailed report include:

- Bharatmala Freight-Corridor Rail Sidings Unlocking Bulk-Chemical Reach

- Lithium-Ion Battery Raw-Material Imports Spurring Class 3 & 8 Storage Demand

- Mandatory BIS Quality-Control Orders Raising Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General warehousing captured 37.47% of the India chemical warehousing market in 2025, serving bulk commodity flows that need only ambient storage. Despite this lead, temperature-controlled chemical warehouses will register a brisk 12.11% CAGR through 2031 due to biologics, active pharmaceutical ingredients, and temperature-sensitive catalysts. Operators are adding dedicated cold rooms, glycol chillers, and insulated dock doors to meet Good Distribution Practice requirements. Allcargo's 160,000-square-foot Uran site illustrates the trend, blending sub-25 °C chambers with explosion-proof lighting as part of a broader national network that serves more than 70 companies.

Specialty chemical warehouses configured for inert-gas blanketing, HEPA filtration, and ISO 9001 workflows have emerged as the market's value-migration zone. Land near Hazira and Dahej now commands significant price premiums as developers bid for rail-siding parcels that link directly to the Western Dedicated Freight Corridor. Celcius Logistics' 2025 launch of a GDP-compliant cross-dock network for pharma exemplifies convergence between cold chain and HAZMAT, while insurer premium reductions of 15-30% for certified fire systems create an added incentive to shift from Grade B sheds to Grade A facilities. Collectively, these factors anchor the long-term expansion strategy of the India chemical warehousing market.

List of Companies Covered in this Report:

- Aegis Logistics Ltd

- Allcargo Logistics

- DHL Group

- Den Hartogh Logistics

- Snowman Logistics Ltd

- Adani Logistics Ltd

- BEST Roadways Ltd.

- Swift Cargo

- IMC Logistics

- Tankstore Ltd

- Noatum Logistics

- Vopak India

- Mahindra Logistics

- Kiran Group

- Apollo Supply Chain

- Seashell Logistics

- DSV

- BDP International

- Yusen Logistics

- Rhenus Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 USD 20 Billion Specialty-Chemical CAPEX Wave (2024-28)

- 4.2.2 National Logistics Policy Tax Holidays for Grade-A Hazmat Facilities

- 4.2.3 Bharatmala Freight-Corridor Rail Sidings Unlocking Bulk-Chemical Hinterland Reach

- 4.2.4 Lithium-Ion Battery Raw-Material Imports Spurring Class 3 & 8 Storage Demand

- 4.2.5 Agro-Pesticide Production-Linked Incentive Scheme Amplifying Regional Warehouse Needs

- 4.2.6 QR-Based Hazardous-Waste E-Tracking (NHWIS-2025) Accelerating Digital WMS Adoption

- 4.3 Market Restraints

- 4.3.1 Rising Marine-Cargo Insurance Surcharges on Bulk Chemicals

- 4.3.2 Mandatory BIS Quality-Control Orders Raising Compliance Costs for 3PL Operators

- 4.3.3 Short Supply of PFAS-Free Fire-Suppression Systems Delaying Warehouse Retrofits

- 4.3.4 Variable Inland-Waterway Draft Hindering Barge Logistics for Liquid Chemicals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, INR Bn)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings and Adhesives

- 5.3.6 Food and Feed Additives

- 5.3.7 Oil and Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Aegis Logistics Ltd

- 6.4.2 Allcargo Logistics

- 6.4.3 DHL Group

- 6.4.4 Den Hartogh Logistics

- 6.4.5 Snowman Logistics Ltd

- 6.4.6 Adani Logistics Ltd

- 6.4.7 BEST Roadways Ltd.

- 6.4.8 Swift Cargo

- 6.4.9 IMC Logistics

- 6.4.10 Tankstore Ltd

- 6.4.11 Noatum Logistics

- 6.4.12 Vopak India

- 6.4.13 Mahindra Logistics

- 6.4.14 Kiran Group

- 6.4.15 Apollo Supply Chain

- 6.4.16 Seashell Logistics

- 6.4.17 DSV

- 6.4.18 BDP International

- 6.4.19 Yusen Logistics

- 6.4.20 Rhenus Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)