|

市場調查報告書

商品編碼

2063322

北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

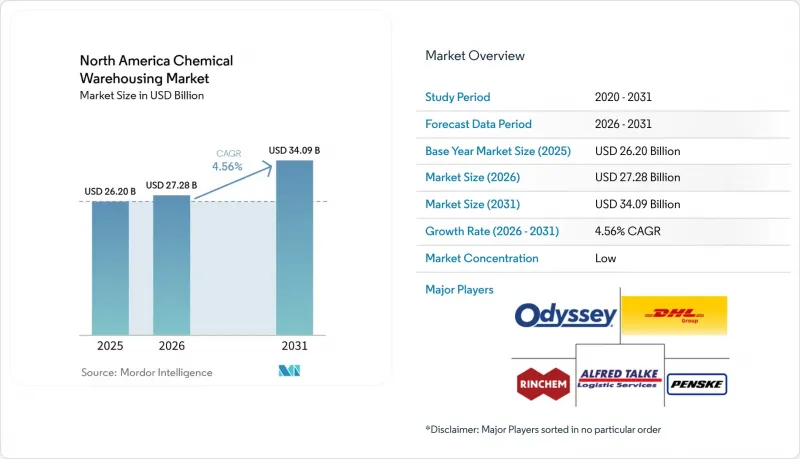

根據 Mordor Intelligence 預測,北美化學品倉儲市場規模將從 2025 年的 262 億美元和 2026 年的 272.8 億美元成長到 2031 年的 340.9 億美元,2026 年至 2031 年的複合年成長率為 4.56%。

對獲得永續發展認證的倉儲設施的需求不斷成長、電池級鋰化合物的成長以及近岸外包向墨西哥北部地區的推進,正在重塑北美化學品倉儲市場的服務需求和設施位置。本報告按倉庫類型(普通倉儲、特種化學品倉儲、危險品倉儲及其他)、化學品類型(易燃液體、腐蝕性物質及其他)、終端用戶行業(基礎化學品製造、特種化學品製造及其他)和國家/地區(美國、加拿大、墨西哥)進行細分。市場預測以美元(USD)為單位。

北美化學品倉庫市場的趨勢與洞察

為了實現碳中和,各方都在大力努力,這推動獲得 LEED 和 ISO 14001 認證的化學品倉庫的需求。

企業永續發展目標現已涵蓋範圍 3 物流排放,托運人也越來越要求第三方設施符合 LEED 和 ISO 14001 標準。採用太陽能屋頂、高效能暖通空調系統和現場水循環利用的營運商有資格獲得綠色貸款,並在北美化學品倉庫市場獲得更高的租金。由於墨西哥灣沿岸地區的平均能源成本為每千瓦時 6.6 美分,可再生能源維修投資的投資回收期進一步縮短。這些認證構成了實實在在的進入門檻,推動市場需求流向資金雄厚、成熟的營運商。隨著各州監管機構將建築規範與氣候政策相協調,永續發展認證預計將成為北美化學品倉庫市場的基本要求,而非差異化因素。

電池級和儲能化學品的快速成長需要溫度控制、隔離儲存。

由於電解溶劑和氫氧化鋰對水分和微量金屬極為敏感,因此倉庫中必須配備露點監測、惰性氣體密封和隔離室。 Linkhem位於亞利桑那州的12.3萬平方英尺的倉庫便是先進通風系統和感測器陣列的典範,這些系統和陣列如今已成為該行業的標準配置。這種精確的控制降低了批次缺陷的風險,並促成了多年合約的簽訂,從而穩定了運轉率。隨著汽車OEM廠商宣布計畫在2027年新建15座電池工廠,預計對這種專用儲存空間的需求成長速度將超過北美化學品倉儲市場的整體成長趨勢。

主要終端市場經濟週期波動所導致的衰退風險,造成了倉庫運轉率。

油漆、塑膠和建築添加劑的庫存與住宅開工量和汽車產量密切相關,景氣衰退期間庫存會下降。在新澤西州,由於4000萬平方英尺的投機性建築竣工後未能找到租戶,預計到2024年,該州的倉庫空置率將上升至9%。北美化學品倉庫市場也出現了類似的波動,給固定成本資產的獲利能力帶來了壓力。因此,營運商被迫轉向受經濟波動影響較小的行業,例如製藥業,以分散其投資組合風險。

細分市場分析

北美化學品倉儲市場正經歷顯著成長,其中溫控化學品倉儲預計到2031年將以5.59%的複合年成長率成長,超過整體市場成長率。這凸顯了市場對專業儲存解決方案日益成長的需求。預計到2025年,專業化學品倉儲將佔據34.25%的市場佔有率,反映出該行業對品質和合規性的日益重視。客戶願意投資經過認證、記錄在案且檢驗的監控系統,以確保安全和符合法規要求。這些因素共同推動了該地區化學品倉儲市場的變革。

對露點控制、惰性氣體吹掃和間歇式電源的需求不斷成長,導致資本密集度增加,但也促使企業與電子和生命科學公司簽訂多年期合約。為了滿足更嚴格的氣候敏感度標準,漢森倉儲公司已將其冷凍庫容量加倍,達到60萬平方英尺。在北美化學品倉儲市場,隨著托運人將高級產品轉移到專用區域,普通倉儲正面臨商品化趨勢,迫使非專業倉儲企業要么加入價格戰,要么退出市場。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 為了實現碳中和,各方都在大力努力,這推動獲得 LEED 和 ISO 14001 認證的化學品倉庫的需求。

- 電池和儲能化學品的快速成長需要溫度控制、隔離儲存。

- 美國和加拿大內陸港口的擴建:鐵路、駁船和管道基礎設施的連接,以及專用危險物品碼頭的整合。

- 人工智慧驅動的安全分析可以降低事故率和保險需求,並加快設施核准速度。

- 生物基和發酵衍生化學品的成長,為無過敏原和污染控制的倉庫創造了一個利基市場。

- 隨著美墨加協定近岸外包熱潮的到來,特種化學品庫存正向南轉移到墨西哥北部的物流走廊。

- 市場限制因素

- 主要終端市場(建築業、塑膠業)的景氣衰退風險導致倉庫運轉率。

- 新興市場對全氟烷基物質的禁令給長尾化學品的庫存和責任管理增加了不確定性。

- 主要化工叢集內鐵路連接的指定危險品運輸路段短缺

- 物聯網整合危險材料設施面臨的網路安全威脅日益增加,導致合規和風險緩解成本上升。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Rinchem Company, Inc.

- Odyssey Logistics and Technology

- ALFRED TALKE

- Penske Logistics

- Quantix Quantix供應鏈解決方案(前身為AandR物流)

- Porter Logistics

- Weber Logistics

- North American Warehousing Co.

- Metrix Logistics Group

- Buske Logistics

- Evans Distribution Systems

- FW Warehousing

- Rhenus Logistics

- ADLI Logistics

- GXO Logistics

- XPO, Inc.

- CH Robinson

- DSV A/S

- Kuehne+Nagel

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america chemical warehousing market size is projected to expand from USD 26.2 billion in 2025 and USD 27.28 billion in 2026 to USD 34.09 billion by 2031, registering a 4.56% CAGR between 2026 and 2031.

Rising demand for sustainability-certified storage, growth in battery-grade lithium compounds, and ongoing nearshoring into Northern Mexico are reshaping service requirements and facility locations across the North America chemical warehousing market. This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, HAZMAT Warehouses, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Country (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Chemical Warehousing Market Trends and Insights

Surge in Carbon-Neutral Pledges Driving Demand for LEED and ISO 14001-Certified Chemical Warehouses

Corporate sustainability targets now include Scope 3 logistics emissions, prompting shippers to insist that third-party facilities meet LEED and ISO 14001 benchmarks. Operators adopting solar roofs, high-efficiency HVAC and on-site water recycling qualify for green loans and command premium rent in the North America chemical warehousing market. Energy costs averaging 6.6 cents /kWh along the Gulf Coast further improve payback periods for renewable retrofits. These certifications create tangible barriers to entry that channel volume toward well-capitalized incumbents. As state regulators align building codes with climate policy, sustainability credentials are expected to become a baseline requirement rather than a differentiator across the North America chemical warehousing market.

Rapid Expansion of Battery-Grade and Energy-Storage Chemicals Requiring Segregated Temperature-Controlled Storage

Electrolyte solvents and lithium hydroxide are hypersensitive to moisture and trace metals, forcing warehouses to add dew-point monitoring, inert gas blanketing, and isolated rooms. Rinchem's 123,000 ft2 Arizona site illustrates the upgraded ventilation and sensor arrays now standard for this trade. Precision helps reduce batch-failure risk, enabling multi-year contracts that lock in utilization. With automotive OEMs announcing 15 new battery plants by 2027, demand for such dedicated capacity is set to rise more quickly than overall activity in the North America chemical warehousing market.

Cyclical Downturn Risk in Key End-Markets Causing Volatile Warehouse Utilization

Paints, plastics and construction additives cycle with housing starts and auto output, shrinking inventories during recessions. New Jersey's warehouse vacancy climbed to 9% in 2024 after 40 million ft2 of speculative builds came online without committed tenants. Similar swings in the North America chemical warehousing market squeeze margin on fixed-cost assets, compelling operators to court counter-cyclical sectors such as pharmaceuticals to balance portfolio risk.

Other drivers and restraints analyzed in the detailed report include:

- United States-Canada Inland-Port Build-Outs Integrating Rail, Barge and Pipeline Links with Dedicated Hazmat Terminals

- AI-Powered Safety Analytics Lowering Incident Rates and Insurance Prerequisites

- Emerging PFAS Bans Adding Uncertainty to Long-Tail Inventories and Liability Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The North America chemical warehousing market is witnessing notable growth, with Temperature-Controlled Chemical Warehouses projected to expand at a CAGR of 5.59% through 2031, surpassing the market's overall growth rate. This highlights the increasing demand for specialized storage solutions. Specialty Chemical Warehouses, holding a 34.25% market share in 2025, reflect the industry's emphasis on quality and compliance. Customers are demonstrating a willingness to invest in certifications, documentation, and validated monitoring systems to ensure safety and regulatory adherence. These factors collectively drive the evolution of the chemical warehousing market in the region.

Demand for dew-point control, inert gas purging, and backup power makes capital intensity high, yet also locks in multi-year contracts from electronics and life-science firms. Hansen Storage doubled freezer capacity to 600,000 ft2 to meet stricter climate-sensitivity standards. General Warehousing faces commoditization as shippers shift premium products into purpose-built zones across the North America chemical warehousing market, forcing non-specialists to compete on price or exit.

List of Companies Covered in this Report:

- DHL Group

- Rinchem Company, Inc.

- Odyssey Logistics and Technology

- ALFRED TALKE

- Penske Logistics

- Quantix Quantix Supply Chain Solutions (Formerly AandR Logistics)

- Porter Logistics

- Weber Logistics

- North American Warehousing Co.

- Metrix Logistics Group

- Buske Logistics

- Evans Distribution Systems

- FW Warehousing

- Rhenus Logistics

- ADLI Logistics

- GXO Logistics

- XPO, Inc.

- C.H. Robinson

- DSV A/S

- Kuehne+Nagel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Carbon-Neutral Pledges Driving Demand for LEED- and ISO 14001-Certified Chemical Warehouses

- 4.2.2 Rapid Expansion of Battery-Grade and Energy-Storage Chemicals Requiring Segregated Temperature-Controlled Storage

- 4.2.3 US-Canada Inland-Port Build-Outs Integrating Rail, Barge and Pipeline Links with Dedicated Hazmat Terminals

- 4.2.4 AI-Powered Safety Analytics Lowering Incident Rates and Insurance Prerequisites, Accelerating Facility Approvals

- 4.2.5 Growth of Bio-Based and Fermentation-Derived Chemicals Creating Allergen-Free, Contamination-Controlled Warehousing Niches

- 4.2.6 Post-CUSMA Near-Shoring Boom Shifting Specialty-Chemical Inventory South to Northern Mexico Logistics Corridors

- 4.3 Market Restraints

- 4.3.1 Cyclical Downturn Risk in Key End-Markets (Construction, Plastics) Causing Volatile Warehouse Utilization

- 4.3.2 Emerging PFAs Bans Adding Uncertainty to Long-Tail Chemical Inventories and Liability Management

- 4.3.3 Scarcity of Rail-Connected Hazmat-Zoned Land Parcels within Tier-1 Chemical Clusters

- 4.3.4 Rising Cyber-Security Threats to IoT-Integrated Hazmat Facilities Increasing Compliance and Mitigation Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings and Adhesives

- 5.3.6 Food and Feed Additives

- 5.3.7 Oil and Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Rinchem Company, Inc.

- 6.4.3 Odyssey Logistics and Technology

- 6.4.4 ALFRED TALKE

- 6.4.5 Penske Logistics

- 6.4.6 Quantix Quantix Supply Chain Solutions (Formerly AandR Logistics)

- 6.4.7 Porter Logistics

- 6.4.8 Weber Logistics

- 6.4.9 North American Warehousing Co.

- 6.4.10 Metrix Logistics Group

- 6.4.11 Buske Logistics

- 6.4.12 Evans Distribution Systems

- 6.4.13 FW Warehousing

- 6.4.14 Rhenus Logistics

- 6.4.15 ADLI Logistics

- 6.4.16 GXO Logistics

- 6.4.17 XPO, Inc.

- 6.4.18 C.H. Robinson

- 6.4.19 DSV A/S

- 6.4.20 Kuehne+Nagel

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)