|

市場調查報告書

商品編碼

2063335

非洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Africa Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

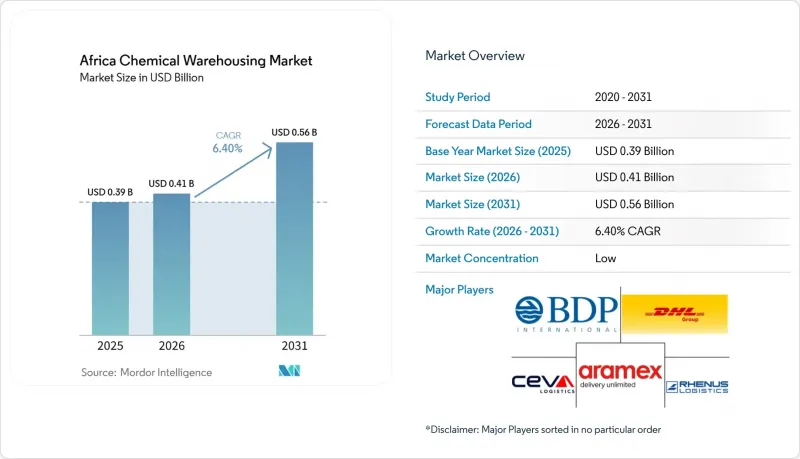

據 Mordor Intelligence 稱,2025 年非洲化學品倉庫市場價值 3.9 億美元,預計到 2031 年將達到 5.6 億美元,而 2026 年為 4.1 億美元,預測期(2026-2031 年)複合年成長率為 6.40%。

本報告按倉庫類型(普通倉庫、特殊化學品倉庫等)、化學品類型(易燃液體、腐蝕性物質等)、終端用戶行業(基礎化學品製造、特種化學品製造等)和地區(奈及利亞、摩洛哥、肯亞等)進行細分。市場預測以美元計價。

非洲化學品倉庫市場的趨勢與洞察

採礦業對化學品的需求成長

根據非洲聯盟的《綠色礦產戰略》,在燃料、潤滑油和電力之後,礦山消耗的大量物品包括炸藥、試劑、氰化物及相關化學品,凸顯了在礦山和港口附近倉庫進行專門儲存的必要性。在南非,預計2025年基礎化學品成本將上漲,電費和水費也將出現兩位數的成長,因此礦業公司已開始儲備硫酸、鹽酸、氫氧化鈉和氯氣,以避免供應中斷。這些成本和可靠性方面的趨勢,使得符合規範的倉庫的角色日益凸顯。這些倉庫不僅可以隔離和儲存腐蝕性和有毒物質,還能確保向選礦廠和冶煉廠穩定運輸這些物質。南非的重型貨運鐵路支持與採礦價值鏈相關的散裝液體和危險品的長途運輸,並與豪登省和誇祖魯-納塔爾省周邊的倉儲網路連接。隨著採礦作業轉向低品位礦石,試劑用量不斷增加,這推動了非洲化學品倉庫市場對配備完善通風系統、二級防護和事故響應標準的設施的需求。這促使倉庫佈局和監控系統不斷升級,以應對高周轉率,並在整個運輸過程中確保符合安全、健康、環境和品質 (SHEQ) 標準。

農業材料市場的擴張

西非地區對氮肥和氨/尿素生產能力的大規模投資正在擴大區域化肥原料供應基礎,推動了對尿素、氨和甲醇等受監管儲存設施的需求,包括適用於氧化劑和有毒物質的獨立儲存和庫存管理。隨著非洲大陸自由貿易區(AfCFTA)取消大部分商品的關稅,農藥跨境貿易預計將會增加。這促使倉庫佈局轉向連接主要港口和內陸門戶的走廊式綜合樞紐。港口靈活的液體散貨處理能力,可同時容納食用油和化學品貨物,為需要嚴格遵守衛生和洩漏預防措施的常溫和危險品儲存的農產品提供支援。在肯亞,蒙巴薩附近和奧爾卡里亞新建的經濟區以及一座地熱發電廠旨在吸引農產品加工企業,從而增加了對農作物保護產品溫濕度控制設施的需求。這些趨勢有利於非洲化學品倉儲市場的營運商,他們能夠將低溫運輸能力與危險品監管文件相結合,以應對季節性需求激增以及從港口到內陸地區的物流運輸。一套涵蓋標籤、監控和緊急應變的綜合合規體係有助於農藥儲存適應關鍵市場不斷變化的標準。

基礎設施和物流網路不足

基礎設施不足和氣候變遷的影響導致持續的成本增加和延誤,氣候相關事件造成的年均損失嚴重影響了運輸和倉儲企業的財務表現。這種情況加劇了危險物品的風險,因為延誤增加了港口和內陸倉庫(這些倉庫並非為長期儲存而設計)的安全和合規負擔。將貨運量轉移到鐵路並加強貨櫃安全的多模態試點項目可以降低長途運輸路線的風險,但這些網路在特定走廊之外仍處於發展階段。主要樞紐對燃料和原料進口的高度依賴維持了對儲槽區和專用儲存能力的需求,同時也加劇了對外匯波動的敏感性,進而影響庫存融資。這些結構性障礙阻礙了先進倉儲技術的應用,並限制了地方城市的冗餘設施建設,而隨著非洲化學品倉儲市場區域貿易的擴張,冗餘設施的建設至關重要。

細分市場分析

到2025年,特種化學品倉庫將佔市場佔有率的37.41%,這反映出非洲化學品倉庫市場正朝著以合規為導向的儲存模式轉變,以支持配方、添加劑和聚合物等高價值產品的儲存。受藥品和農藥處理標準本地化導致對檢驗的冷藏和濕度控制的需求不斷成長的推動,溫控化學品倉庫預計將在2026年至2031年間以6.74%的複合年成長率成長。預計到2031年,非洲該細分市場的化學品倉庫規模將以6.74%的複合年成長率成長。危險物品設施對於易燃、氧化性和有毒物質仍然至關重要,尤其是在國家標準參考與國際基準一致的分類、包裝和緊急應變規範的地區。主要托運人使用SQAS-AFRICA認證來選擇能夠在處理、儲存和事故回應過程中確保危險物品安全運作的供應商。同時,普通倉庫仍在進行常溫存儲,但由於隔離客戶、消防系統和門禁控制等要求,其利潤率受到擠壓,而這些要求是區域城市傳統規模的倉庫無法滿足的。因此,非洲的化學品倉儲行業更傾向於採用自動化和可審計流程相結合的設施,以確保與跨國公司簽訂長期合約。

2026年至2031年間,隨著非洲大陸自由貿易區(AfCFTA)支援原料藥、添加劑和高級農藥的區域分銷(這些產品依賴經認證的倉儲管理鏈),預計倉儲設施的配置將轉向專用和溫控設施。肯亞新建的經濟特區(SEZ)和南非的鐵路連接碼頭便是例證,說明政策和基礎設施的結合如何吸引那些需要在港口和鐵路附近建立合規倉儲模式的化學品密集型製造商。毗鄰港口的液體散貨碼頭,例如德班擁有10萬立方米容量的碼頭,也在強化更廣泛的樞紐輻射式庫存佈局模式,以服務於食用油和化學品貨物。那些能夠按照危險品分類規則對標籤檢視、監測和空氣採樣進行標準化的營運商,在非洲化學品倉儲市場中更有利於滿足全球買家的審計要求。這種結構將縮小合規差距,並將採購轉向那些整合了安全措施、可視性和敏感貨物資料收集的認證供應商。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 採礦業對化學品的需求成長

- 農業投入品市場的擴張

- 石油和天然氣產業的發展

- 製造業多角化

- 港口基礎設施現代化

- 藥品生產的本地化

- 市場限制因素

- 基礎設施和物流網路不足

- 法規碎片化和執法不力。

- 專業倉儲設施短缺

- 高度依賴進口和外匯波動

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學物質類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

- 國家

- 奈及利亞

- 摩洛哥

- 肯亞

- 南非

- 衣索比亞

- 阿爾及利亞

- 其他非洲國家

- 地緣政治事件對市場的影響

- 循環經濟中的化學品回收

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- BDP International

- CEVA Logistics

- Aramex

- Rhenus Logistics

- Transnet Freight and Warehousing

- Hellmann Worldwide Logistics

- DSV

- Worldwide Logistics Group

- Unitrans Africa

- Robeck International Freight

- Value Chemical Logistics

- Impro Logistics

- Xeon

- SAS Logistics Ltd

- DACHSER

- Noatum Logistics

- Toll Group

- Fracht and Fracht Group

- DP World(Imperial Logistics)

第7章 市場機會與未來展望

According to Mordor Intelligence, the africa chemical warehousing market size was valued at USD 0.39 billion in 2025 and is estimated to grow from USD 0.41 billion in 2026 to reach USD 0.56 billion by 2031, at a CAGR of 6.40% during the forecast period (2026-2031).

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Geography (Nigeria, Morocco, Kenya, and More). The Market Forecasts are Provided in Terms of Value (USD).

Africa Chemical Warehousing Market Trends and Insights

Mining Sector Chemical Demand Growth

The African Union's Green Minerals Strategy shows that mines consume significant quantities of explosives, reagents, cyanide, and related chemical inputs after fuel, lubricants, and power, reinforcing the need for specialized storage at mine-adjacent and port-proximate depots. In South Africa, basic chemical input costs rose in 2025 alongside double-digit increases in electricity and water tariffs, which encouraged mining operators to maintain buffer stocks of sulfuric acid, hydrochloric acid, sodium hydroxide, and chlorine to avoid disruptions. These cost and reliability dynamics increase the role of compliant warehouses capable of segregating corrosives and toxics while supporting steady outbound flows to concentrators and smelters. South Africa's heavy-haul rail supports long-distance movement of bulk liquids and hazardous cargoes tied to mining value chains, aligning with storage networks around Gauteng and KwaZulu-Natal. As mines process lower-grade ores, their reagent intensity increases, which sustains demand for capacity with robust ventilation, secondary containment, and incident response standards in the Africa chemical warehousing market. This supports a steady pipeline of upgrades to warehousing layouts and monitoring systems to manage higher turnover and maintain SHEQ compliance across corridors.

Agricultural Input Market Expansion

Large-scale investments in nitrogen and ammonia-urea capacity in West Africa are expanding the regional supply base for fertilizer inputs and driving demand for compliant storage of urea, ammonia, and methanol, including segregation and inventory controls suited to oxidizers and toxics. As AfCFTA eliminates tariffs on most goods, cross-border flows of agrochemicals are expected to rise, which shifts warehousing footprints toward integrated, corridor-based nodes linked to major ports and inland gateways. Port-side liquid bulk capacity that can flex between edible oils and chemical cargoes supports agribusinesses that need both ambient and hazardous storage with strict hygiene and spill-control protocols. In Kenya, new special economic zones near Mombasa and in geothermal-powered Olkaria are designed to attract agro-processing, which raises the requirement for temperature-controlled and humidity-managed facilities for crop protection products. These trends favor operators that can pair cold-chain capabilities with regulatory documentation for dangerous goods to serve seasonal surges and port-to-inland distribution in the Africa chemical warehousing market. Compliance architectures that integrate labeling, monitoring, and emergency response help align agricultural chemical storage with evolving standards in key markets.

Inadequate Infrastructure and Logistics Networks

Infrastructure gaps and climate exposure generate sustained costs and delays, with average annual losses linked to climate-related events that weigh on the financial performance of transport and storage operations. These conditions magnify risks for hazardous cargo, where delays increase safety and compliance burdens in port yards and inland depots that are not designed for prolonged dwell. Multimodal pilots that shift volume toward rail with enhanced container security can reduce exposure on long-haul routes, but these networks remain nascent outside select corridors. High import reliance on fuel and feedstocks in major hubs sustains the need for tank farms and specialized storage capacity, while also increasing sensitivity to exchange rate swings that affect inventory financing. These systemic hurdles slow the diffusion of advanced warehousing technologies and limit redundancy in secondary cities that the Africa chemical warehousing market will need as regional trade grows.

Other drivers and restraints analyzed in the detailed report include:

- Oil and Gas Sector Development

- Manufacturing Sector Diversification

- Regulatory Fragmentation and Weak Enforcement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty Chemical Warehouses accounted for 37.41% in 2025, reflecting a clear shift toward compliance-intensive storage that supports higher value products across formulations, additives, and polymers in the Africa chemical warehousing market. Temperature-Controlled Chemical Warehouses are projected to grow at 6.74% during 2026-2031 as pharma localization and agrochemical handling standards push demand for validated cold rooms and humidity control, and the Africa chemical warehousing market size for this segment is expected to expand at a 6.74% CAGR through 2031. Hazardous Materials facilities remain essential for flammables, oxidizers, and toxics, particularly where national standards reference classification, packaging, and emergency response codes aligned with international benchmarks. SQAS-AFRICA certification is being used by leading shippers to screen providers that can maintain safe operations for dangerous goods across handling, storage, and incident response. In parallel, general warehousing continues to serve ambient commodities, though margins face pressure as clients require segregation, fire suppression, and access control that exceed legacy footprints in secondary cities. The Africa chemical warehousing industry is therefore favoring facilities that combine automation with audit-ready processes to win long-term contracts from multinationals.

Over 2026-2031, the mix is expected to tilt toward specialty and temperature-controlled sites as AfCFTA supports intra-regional distribution of APIs, excipients, and high-spec agrochemicals that rely on certified chains of custody. New SEZs in Kenya, alongside rail-linked terminals in South Africa, illustrate how policy and infrastructure combine to attract chemical-intensive manufacturing that requires compliant storage models near ports and rail. Port-adjacent liquid bulk terminals, such as Durban's 100,000 cubic meters of capacity, also reinforce a broader hub-and-spoke approach to inventory positioning for both edible oils and chemical cargoes. Operators that standardize labeling, monitoring, and air sampling per hazard-class rules are better positioned to meet audit requirements of global buyers in the Africa chemical warehousing market. This structure narrows the compliance gap and shifts procurement toward certified providers that integrate safety with visibility and data capture for sensitive cargo.

List of Companies Covered in this Report:

- DHL Group

- BDP International

- CEVA Logistics

- Aramex

- Rhenus Logistics

- Transnet Freight and Warehousing

- Hellmann Worldwide Logistics

- DSV

- Worldwide Logistics Group

- Unitrans Africa

- Robeck International Freight

- Value Chemical Logistics

- Impro Logistics

- Xeon

- SAS Logistics Ltd

- DACHSER

- Noatum Logistics

- Toll Group

- Fracht and Fracht Group

- DP World (Imperial Logistics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mining Sector Chemical Demand Growth

- 4.2.2 Agricultural Input Market Expansion

- 4.2.3 Oil and Gas Sector Development

- 4.2.4 Manufacturing Sector Diversification

- 4.2.5 Port Infrastructure Modernization

- 4.2.6 Pharmaceutical Manufacturing Localization

- 4.3 Market Restraints

- 4.3.1 Inadequate Infrastructure and Logistics Networks

- 4.3.2 Regulatory Fragmentation and Weak Enforcement

- 4.3.3 Shortage of Specialized Warehousing Facilities

- 4.3.4 High Import Dependency and Forex Volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 Nigeria

- 5.4.2 Morocco

- 5.4.3 Kenya

- 5.4.4 South Africa

- 5.4.5 Ethiopia

- 5.4.6 Algeria

- 5.4.7 Rest of Africa

- 5.5 Impact of Geopolitical Events on the Market

- 5.6 Circular Economy Chemical Recycling

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 BDP International

- 6.4.3 CEVA Logistics

- 6.4.4 Aramex

- 6.4.5 Rhenus Logistics

- 6.4.6 Transnet Freight and Warehousing

- 6.4.7 Hellmann Worldwide Logistics

- 6.4.8 DSV

- 6.4.9 Worldwide Logistics Group

- 6.4.10 Unitrans Africa

- 6.4.11 Robeck International Freight

- 6.4.12 Value Chemical Logistics

- 6.4.13 Impro Logistics

- 6.4.14 Xeon

- 6.4.15 SAS Logistics Ltd

- 6.4.16 DACHSER

- 6.4.17 Noatum Logistics

- 6.4.18 Toll Group

- 6.4.19 Fracht and Fracht Group

- 6.4.20 DP World (Imperial Logistics)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)