|

市場調查報告書

商品編碼

2063324

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Europe Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

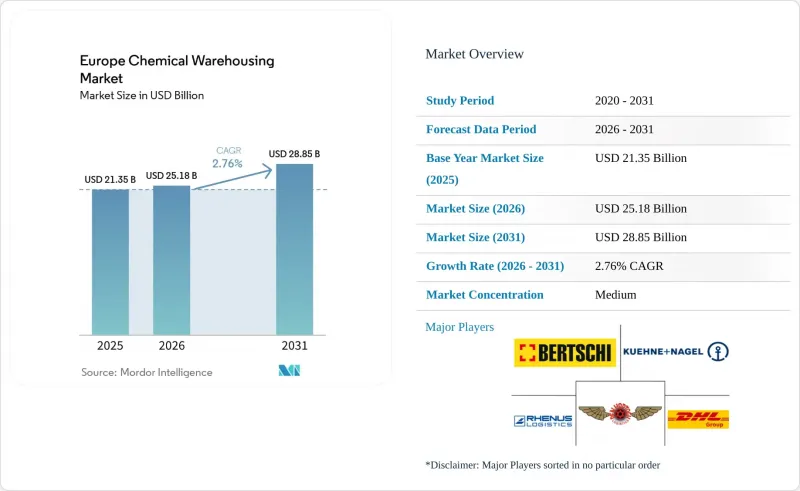

根據 Mordor Intelligence 預測,歐洲化學品倉庫市場規模將從 2025 年的 213.5 億美元成長到 2026 年的 251.8 億美元,到 2031 年將達到 288.5 億美元,2026 年至 2031 年的複合年成長率為 2.76%。

本報告按倉庫類型(普通倉庫、特殊化學品倉庫、危險品倉庫及其他)、化學品類型(易燃液體及其他)、終端用戶行業(基礎化學品製造、特種化學品製造及其他)和國家/地區(德國、西班牙及其他)進行細分。市場預測以美元計價。

歐洲化學品倉庫市場的趨勢與洞察

超級工廠電池級化學品生產的擴張推高了對受 ADR 管制物質儲存的需求。

歐洲電池生產的快速擴張帶動了對氫氧化鋰、NMP溶劑和PVDF黏合劑的需求激增,這些產品均受ADR 8類法規的約束。光是Northvolt公司計畫在2026年將其位於埃特(Ett)的工廠產能擴建至60吉瓦時(GWh),就需要在方圓50公里範圍內新建溫控儲存設施,到2028年,該區域的總儲存容量將超過50萬平方公尺。與標準設施相比,升級消防系統、建造危險物品專用倉庫以及實現±2°C的溫度控制將使投資成本增加30%至45%。空間短缺在德國東部、瑞典北部和匈牙利的汽車產業走廊最為嚴重,能夠快速獲得SEVESO III許可證並部署模組化倉庫的營運商將擁有顯著優勢。

歐盟將與CBAM相關的基本化學品運回國內,造成了對緩衝庫存倉庫的需求。

對進口氨和甲醇徵收碳關稅,使得歐盟的生產在20年來首次獲利,促使BASF和雅苒等公司計劃恢復在歐洲的生產能力。為了對沖供應風險,製造商目前持有相當於30至45天用量的原料——是2023年基準水準的兩倍——路德維希港、安特衛普港口以及地中海沿岸的倉儲面積正在擴張。隨著柔軟性優先於規模,配備靈活倉庫管理系統(WMS)的多組分倉庫正在取代單組分儲罐,並不斷擴大市場佔有率。義大利和西班牙尤其受益於碳氫化合物替代能源(CBAM),因為從北非進口的綠色氫氣具有成本優勢,導致碼頭附近儲存需求激增。

港口擁擠和繞道紅海導致貨物滯留時間延長,庫存風險增加。

2025年,經好望角的航線將使亞洲至歐盟的運輸時間延長至多14天。鹿特丹港的平均貨櫃停留時間從4天增加到10天,迫使進口商將安全庫存增加一倍,並支付更高的倉儲費用。對於那些沒有替代供應商的特殊商品進口商而言,他們必須承擔15%至20%的物流成本成長,這導致利潤率下降,並促使生產能力回流至國內。

細分市場分析

至2031年,溫控化學品倉庫將佔歐洲化學品倉庫市佔率成長軌跡的5.62%。這反映了對生物製藥和電池電解的需求激增,這些產品僅能耐受±2°C的狹窄溫度範圍。與這些高規格設施相關的歐洲化學品倉庫市場規模正在擴大。這是因為營運商正在維修現有倉庫,並安裝多區域空調、濕度控制和惰性氣體滅火系統,以滿足GDP(良好生產規範)和ADR(替代性爭議解決機制)的要求。每平方公尺高達1200至1800歐元(1411至2117美元)的高昂建設成本,正擴大被長達五年的生物類似藥研發合約期限所抵消,這使得業主能夠獲得更高的回報並加快債務償還速度。

到2025年,特用化學品倉庫仍將佔歐洲化學品倉庫市場38.58%的佔有率,主要面向需要隔離隔間、導電地板塗層和ISO潔淨室輔助設施的小批量電子化學品和功能性添加劑。普通倉庫(主要由散裝貨物倉庫組成)的定價權正在下降,因為客戶轉向升級後的特殊設施所提供的高價值混合和預稀釋服務。危險品倉庫對於石化產品的分銷仍然至關重要,但由於對PFAS污染的擔憂導致保險成本上升,其利潤率面臨壓力。這促使小規模企業轉向合資企業,利用「數位歐洲」津貼升級消防水儲存設施。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超級工廠電池化學品生產的擴張正在推高ADR的儲能需求。

- 歐盟將與CBAM相關的基本化學品運回國內,為緩衝庫存創造了倉庫空間。

- 歐盟「數位歐洲」補貼正在加速倉庫中機器人和自主系統的應用。

- 北海沿岸港口附近離岸風力發電用樹脂和固化劑的出貨量激增。

- 歐盟化學品策略強制使用QR碼進行可追溯性,這推動了倉庫管理系統 (WMS) 的升級。

- 合約合成新創企業的興起需要靈活的、多租戶的危險物質儲存空間。

- 市場限制因素

- 與逐步淘汰 PFA 相關的債務,這需要高成本的淨化能力。

- 綠色金融分類和不斷上漲的利率正在增加維修的進入門檻。

- 港口擁擠和繞道紅海導致貨物滯留時間延長,庫存風險增加。

- 要求具備應對極端天氣事件能力的法規正在推動營運層面出現計畫外資本投資。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

- 國家

- 德國

- 英國

- 俄羅斯

- 義大利

- 荷蘭

- 西班牙

- 波蘭

- 法國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Kuehne+Nagel

- Rhenus Logistics

- Bertschi AG

- Den Hartogh Logistics

- Talke Logistics

- HOYER Group

- Broekman Logistics

- Odyssey Logistics & Technology Corporation

- Mainfreight

- NTG Nordic Transport Group A/S

- HW Coates

- TIBA Group

- H.Essers

- DSV A/S

- 達飛集團(包括CEVA物流)

- BDP International

- GEODIS

- CH Robinson

- XPO, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe chemical warehousing market size is projected to expand from USD 21.35 billion in 2025 USD 25.18 billion in 2026 to USD 28.85 billion by 2031, growing at a CAGR of 2.76% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and More), by Chemical Type (Flammable Liquids, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Country (Germany, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Chemical Warehousing Market Trends and Insights

Gigafactory Battery-Grade Chemical Buildouts Elevating ADR Storage Demand

Europe's rapid battery-cell scale-up drives clustered demand for lithium hydroxide, NMP solvents, and PVDF binders that fall under ADR Class 8 regulations. Northvolt's Ett expansion to 60 GWh by 2026 alone requires new temperature-controlled storage within a 50 km radius, pushing regional capacity past 500,000 m2 by 2028. Facility investments are 30-45% costlier than standard sites because of fire-suppression upgrades, segregated hazmat bays, and +-2 °C climate control. Spatial pressure is most acute in eastern Germany, northern Sweden, and Hungary's automotive corridor, favoring operators that can fast-track SEVESO-III permits and deploy modular warehouses.

EU CBAM-Linked Reshoring of Basic Chemicals Creating Buffer-Stock Warehousing

Carbon tariffs on imported ammonia and methanol make EU production financially viable for the first time in two decades, prompting BASF and Yara to plan continental capacity restarts. Manufacturers now hold 30-45 days of feedstock double the 2023 norm to hedge supply risks, swelling warehousing footprints around Ludwigshafen, Antwerp, and Mediterranean ports. Flexibility trumps scale, so multi-product warehouses with agile WMS gain share over single-commodity tanks. Italy and Spain stand out as CBAM beneficiaries because green-hydrogen imports from North Africa offer cost advantages, sending berth-proximate storage demand surging.

Port Congestion and Red-Sea Rerouting Inflating Dwell-Time and Inventory Risk

Cape-of-Good-Hope routing lengthened Asian-to-EU voyages by up to 14 days in 2025. Rotterdam's average container dwell stretched from 4 days to 10 days, forcing importers to double safety stocks and pay higher demurrage fees. Specialty importers lacking secondary suppliers must absorb 15-20% logistics-cost inflation, shrinking margins, and nudging procurement toward reshored capacity.

Other drivers and restraints analyzed in the detailed report include:

- Offshore-Wind Resin and Hardener Volume Surge Near North Sea Ports

- EU Digital Europe Subsidies Accelerating Warehouse Robotics and Autonomy Adoption

- PFAS Phase-Out Liabilities Requiring Costly Decontamination Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Temperature-controlled chemical warehouses captured 5.62% of the Europe chemical warehousing market share growth trajectory through 2031, reflecting surging biologics and battery-grade electrolyte demand that tolerates temperature windows of only +-2 °C. The Europe chemical warehousing market size linked to these high-specification sites is climbing as operators retrofit legacy rooms with multi-zone HVAC, humidity scrubbers, and inert-gas fire suppression to satisfy GDP and ADR rules in a single footprint. Premium build costs of EUR 1,200-1,800 (USD 1411-2117) per m2 are increasingly offset by contract lengths stretching to five years for biosimilar pipelines, enabling landlords to lock in higher yields and speed debt pay-down schedules.

Specialty chemical warehouses still controlled 38.58% of the Europe chemical warehousing market size in 2025, anchored by micro-batch electronic chemicals and performance additives that demand segregated bays, conductive-floor coatings, and ISO Clean Room annexes. General warehouses, largely bulk commodity halls, are losing pricing power as clients gravitate toward value-added blending or pre-dilution services now offered inside upgraded specialty facilities. Hazmat-only buildings remain a staple for petrochemical flows but face margin squeeze from mounting insurance premiums after PFAS contamination scares, pushing small operators toward joint-venture fire-water containment upgrades funded under Digital Europe grants.

List of Companies Covered in this Report:

- DHL Group

- Kuehne + Nagel

- Rhenus Logistics

- Bertschi AG

- Den Hartogh Logistics

- Talke Logistics

- HOYER Group

- Broekman Logistics

- Odyssey Logistics & Technology Corporation

- Mainfreight

- NTG Nordic Transport Group A/S

- H.W. Coates

- TIBA Group

- H.Essers

- DSV A/S

- CMA CGM Group (Including CEVA Logistics)

- BDP International

- GEODIS

- C.H. Robinson

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Gigafactory Battery-Grade Chemical Buildouts Elevating ADR Storage Demand

- 4.2.2 EU CBAM-Linked Reshoring of Basic Chemicals Creating Buffer-Stock Warehousing

- 4.2.3 EU Digital Europe Subsidies Accelerating Warehouse Robotics and Autonomy Adoption

- 4.2.4 Offshore-Wind Resin and Hardener Volume Surge Near North Sea Ports

- 4.2.5 Mandatory QR-Traceability under EU Chemicals Strategy Boosting WMS Upgrades

- 4.2.6 Rise of Contract Synthesis Start-Ups Needing Flexible Multi-Tenant Hazmat Space

- 4.3 Market Restraints

- 4.3.1 PFAs Phase-Out Liabilities Requiring Costly Decontamination Capacity

- 4.3.2 Green-Finance Taxonomy and Higher Rates Raising Retrofit Hurdle Costs

- 4.3.3 Port Congestion and Red-Sea Rerouting Inflating Dwell-Time and Inventory Risk

- 4.3.4 Extreme-Weather Resilience Mandates Driving Unplanned Capex on Sites

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings and Adhesives

- 5.3.6 Food and Feed Additives

- 5.3.7 Oil and Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 Russia

- 5.4.4 Italy

- 5.4.5 Netherlands

- 5.4.6 Spain

- 5.4.7 Poland

- 5.4.8 France

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne + Nagel

- 6.4.3 Rhenus Logistics

- 6.4.4 Bertschi AG

- 6.4.5 Den Hartogh Logistics

- 6.4.6 Talke Logistics

- 6.4.7 HOYER Group

- 6.4.8 Broekman Logistics

- 6.4.9 Odyssey Logistics & Technology Corporation

- 6.4.10 Mainfreight

- 6.4.11 NTG Nordic Transport Group A/S

- 6.4.12 H.W. Coates

- 6.4.13 TIBA Group

- 6.4.14 H.Essers

- 6.4.15 DSV A/S

- 6.4.16 CMA CGM Group (Including CEVA Logistics)

- 6.4.17 BDP International

- 6.4.18 GEODIS

- 6.4.19 C.H. Robinson

- 6.4.20 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告

2026年全球多深度穿梭系統市場報告 北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)