|

市場調查報告書

商品編碼

2063350

中國化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

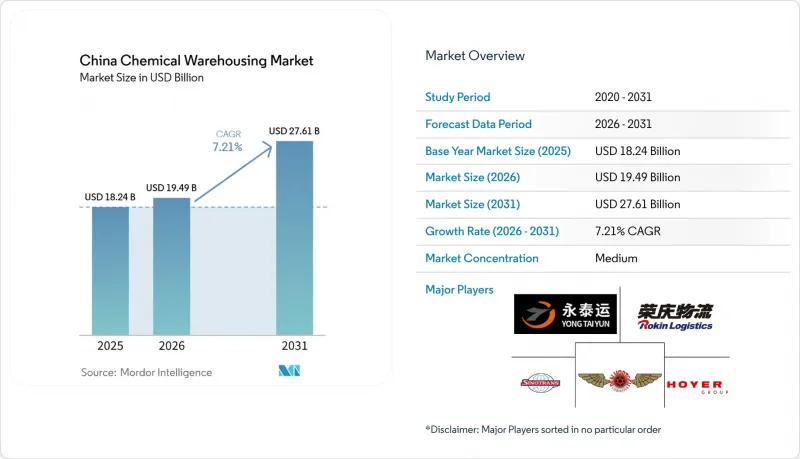

根據 Mordor Intelligence 預測,中國化學品倉庫市場規模預計到 2025 年將達到 182.4 億美元,到 2026 年將達到 194.9 億美元,到 2031 年將達到 276.1 億美元,2026 年至 2031 年的複合成長率為 7.21%。

本報告按倉庫類型(普通倉庫、特殊化學品倉庫、危險品倉庫等)、化學品類型(易燃液體、腐蝕性物質、有毒物質等)和終端用戶行業(基礎化學品製造、特種化學品製造等)進行細分。市場預測以以金額為準(十億美元)表示。

中國化工倉儲市場趨勢與洞察

化工製造地快速擴張

在2025年至2026年穩定成長規劃的指導下,中國石化化工產業預計到2026年將維持年均5%以上的增加值成長速度,重點發展高階聚烯、電子化學品和新能量成分。大規模專案持續擴大產能,並吸引對易燃有毒物質儲存要求日益嚴格的專業倉庫。包括投資4.75億美元的無錫計畫在內的生命科學和特種化學品平台的外商直接投資,進一步推動了符合GDP標準的倉儲物流業務的發展。隨著電子級溶劑和需要在惰性氣氛下無污染儲存的工程材料的需求量不斷成長,中國化學品倉儲市場也從中受益。這種向上游工程的轉變,透過縮短倉儲停留時間和提高自動化價值,提高了認證營運商的運轉率,並穩定了利潤率。

嚴格的化學品安全法規

《危險化學品安全法》將於2026年5月1日生效,該法共127條,規定高毒性和極度危險物質必須由兩人操作和儲存,並要求至少保存三年記錄。 GB 45673-2025標準將於2025年11月1日生效,該標準要求高風險流程的所有環節必須自動化,並規定對安全儀器進行持續監測和升級。倉庫正在與政府機構合作,部署物聯網感測器、符合規定的噴灌和控制系統,以獲得認證並通過審核。缺乏維修資金的小規模設施正在面臨合併或關閉的選擇,這推動了對完全符合標準的認證園區和綜合平台的需求。隨著監管力道在2026年加強,中國化學品倉庫市場正朝著更自動化和可追溯的設施方向發展,儘管數量可能較少。

限制性土地利用政策,以遏止有害物質的蔓延

《危險化學品安全法》規定了危險物質倉儲設施與易受污染接收區域之間指定的安全距離,引導新計畫於已經過核准並接受定期審查的化學產業園區。新的污染物環境影響法規加強了審查力度,要求與生態學分區和產業園區層級的環境影響評估(EIA)保持一致。這些法規導致合格的土地供應減少,核准時間延長,並將專案推向交通和緊急服務不如沿海樞紐完善的地區。到2026年,隨著位置限制和緩衝區範圍的擴大,中國化工倉儲市場的每噸資本密集度將持續提高。開發商正透過優先選擇核准流程更可預測、安全措施更完善、緊急應變的指定園區來應對這項挑戰。

細分市場分析

到2025年,特種化學品倉庫將佔據中國化學品倉儲市場36.42%的最大佔有率。這主要歸因於客戶轉向精細化學品和電子化學品,這些產品需要隔離儲存和污染控制。這些設施採用惰性氣體氣氛控制來儲存對氧敏感的化合物,採用濕度控制來儲存吸濕性材料,並採用基於RFID的批次追蹤技術來滿足半導體和生物製藥的儲存歷史要求。溫控化學品倉庫是成長最快的細分市場,預計到2031年將以8.62%的複合年成長率成長,這主要得益於更嚴格的GDP(倉儲和分銷標準)法規以及原料藥(原料藥)和特種中間體低溫運輸物流的日益普及。這進一步強化了合規主導的差異化優勢。普通化學品倉庫繼續處理穩定性高、完整性風險低的散裝產品,但由於托運人傾向於優先考慮敏感物品的責任保護,其利潤率正面臨越來越大的壓力。在中國的化學品倉儲市場,在更嚴格的監管下,將專業基礎設施與數位化整合相結合,以提高周轉率和服務品質的營運商正在獲得優勢。

該領域的成長與2026年前技術應用和監管合規的進展密切相關。處理易燃、腐蝕性和有毒物質的危險物品倉庫正在升級為符合GB標準和法律要求(例如「雙人管理」和「即時追蹤」)的防爆和自動化滅火系統。營運商正在試點應用數位雙胞胎和人工智慧驅動的調度系統,以最佳化倉位分配和提高勞動效率,並表示儘管合規成本不斷上升,但仍透過提高生產力來維持獲利能力。到2026年,中國化學品倉儲產業正朝著標準化自動化和整合監控的方向發展,以確保獲得許可並與政府平台互通性。中國化學品倉儲市場憑藉其專業技術、對良好倉儲規範(GDP)的應對力以及降低客戶風險的快速審核,持續保持差異化優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 化工製造地快速擴張

- 嚴格的化學品安全法規

- 「一帶一路」計劃推動物流成長

- 特種化學品和精細化學品行業的成長

- 長江經濟帶發展

- 智慧倉庫技術的整合

- 市場限制因素

- 有關危險物質的土地利用法規

- 高昂的合規成本和基礎設施成本

- 法規的頻繁變更和執行

- 來自化學工業的傳遞壓力

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 地緣政治事件對市場的影響

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學物質類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料和黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sinotrans Ltd.

- Yongtaiyun Chemical Logistics

- Rokin Logistics

- Den Hartogh Logistics

- Hoyer Group

- Milkyway Intelligent Supply Chain

- COSCO Shipping Group(COSCO Shipping Chemical)

- Sumisho Global Logistics(China)Co.,Ltd

- Bertschi

- Sunward logistics co. ltd

- SF Express

- Kerry Logistics Network

- BDP International

- Rhenus Logistics

- DHL Group

- CEVA Logistics

- Broekman Logistics

- Yusen Logistics

- Odyssey Logistics and Technology Corporation

- DSV

第7章 市場機會與未來展望

According to Mordor Intelligence, the china chemical warehousing market size is projected to be USD 18.24 billion in 2025, USD 19.49 billion in 2026, and reach USD 27.61 billion by 2031, growing at a CAGR of 7.21% from 2026 to 2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and More), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, and More), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

China Chemical Warehousing Market Trends and Insights

Rapid Expansion of Chemical Manufacturing Base

China's petrochemical and chemical sector is set to deliver value-added growth above 5% annually through 2026, with emphasis on high-end polyolefins, electronic chemicals, and new-energy feedstocks under the 2025 to 2026 stable growth plan. Large-scale programs continue to add capacity and draw in specialized warehousing for flammable and toxic materials with tighter custody needs. Foreign direct investment in life sciences and specialty platforms, including the USD 475 million Wuxi site, adds momentum to GDP-compliant storage and distribution. The China chemical warehousing market benefits as throughput rises for electronic-grade solvents and engineered materials that require inert-atmosphere, contamination-free storage. This upstream shift compresses dwell times and raises the value of automation, raising utilization and stabilizing margins for certified operators.

Stringent Chemical Safety Regulations

The Dangerous Chemicals Safety Law, effective May 1, 2026, sets a 127-article framework that enforces dual-person receipt and dual-person custody for highly toxic and major-hazard materials, with records kept for at least three years. The GB 45673-2025, which took effect on November 1, 2025, mandates full-process automation for high-risk processes and upgrades continuous monitoring and safety instrumentation. Warehouses are adding IoT sensors, compliant sprinklers, and government-interconnected control systems to meet approvals and pass audits. Smaller facilities without the capital to retrofit are either consolidating or exiting, which tilts demand to certified parks and integrated platforms with high compliance readiness. The Chinese chemical warehousing market shifts toward fewer but more automated and traceable sites as enforcement intensifies in 2026.

Restrictive Land Use Policies for Hazardous Materials

The Dangerous Chemicals Safety Law requires prescribed safety distances between hazardous storage and sensitive receptors and pushes new projects into approved chemical parks that undergo periodic reviews. Environmental impact rules linked to new pollutants strengthen screening and alignment with ecological zoning and park-level EIAs. These layers reduce eligible land and prolong approvals, sending projects to zones where transport and emergency services lag coastal hubs. The Chinese chemical warehousing market sees higher capital intensity per tonne as siting constraints and buffer areas expand in 2026. Developers navigate this by prioritizing designated parks with built-in safety and response infrastructure where approvals are more predictable.

Other drivers and restraints analyzed in the detailed report include:

- Belt and Road Initiative (BRI) Logistics Growth

- Growth in the Specialty and Fine Chemicals Sector

- High Compliance and Infrastructure Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses held the largest market share of 36.42% of the China chemical warehousing market in 2025, as customers shifted to fine and electronic chemicals that require segregation and contamination control. These sites use inert-gas blanketing for oxygen-sensitive compounds, controlled humidity for hygroscopic materials, and batch genealogy tracked with RFID to meet chain-of-custody needs in semiconductors and biologics. Temperature-controlled chemical warehouses are growing the fastest, with a CAGR of 8.62% through 2031 under stricter GDP rules and rising cold-chain flows of APIs and specialty intermediates, which strengthens compliance-led differentiation. General chemical warehouses continue to serve stable bulk products with fewer integrity risks, although margin pressure is rising as shippers prioritize liability protection in sensitive categories. The Chinese chemical warehousing market favors operators that blend specialty infrastructure and digital orchestration to raise asset turns and service quality under tighter enforcement.

Growth within this segmentation tracks technology deployment and regulatory readiness in 2026. HAZMAT warehouses that manage flammables, corrosives, and toxics are upgrading to explosion-proof systems and automated suppression aligned to GB and legal requirements on dual-person custody and real-time tracking. Operators are piloting digital twins and AI-driven scheduling to improve slotting and labor efficiency, reporting productivity gains that defend margins despite higher compliance costs. The Chinese chemical warehousing industry is moving to standardized automation and integrated monitoring to ensure approvals and to interoperate with government platforms in 2026. The Chinese chemical warehousing market continues to differentiate on specialty readiness, GDP performance, and audit velocity that reduces customer risk.

List of Companies Covered in this Report:

- Sinotrans Ltd.

- Yongtaiyun Chemical Logistics

- Rokin Logistics

- Den Hartogh Logistics

- Hoyer Group

- Milkyway Intelligent Supply Chain

- COSCO Shipping Group (COSCO Shipping Chemical)

- Sumisho Global Logistics (China) Co.,Ltd

- Bertschi

- Sunward logistics co. ltd

- SF Express

- Kerry Logistics Network

- BDP International

- Rhenus Logistics

- DHL Group

- CEVA Logistics

- Broekman Logistics

- Yusen Logistics

- Odyssey Logistics and Technology Corporation

- DSV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Chemical Manufacturing Base

- 4.2.2 Stringent Chemical Safety Regulations

- 4.2.3 Belt and Road Initiative (BRI) Logistics Growth

- 4.2.4 Growth in Specialty and Fine Chemicals Sector

- 4.2.5 Yangtze River Economic Belt Development

- 4.2.6 Smart Warehousing Technology Integration

- 4.3 Market Restraints

- 4.3.1 Restrictive Land Use Policies for Hazardous Materials

- 4.3.2 High Compliance and Infrastructure Costs

- 4.3.3 Frequent Regulatory Changes and Enforcement

- 4.3.4 Chemical Industry Relocation Pressures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings and Adhesives

- 5.3.6 Food and Feed Additives

- 5.3.7 Oil and Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Sinotrans Ltd.

- 6.4.2 Yongtaiyun Chemical Logistics

- 6.4.3 Rokin Logistics

- 6.4.4 Den Hartogh Logistics

- 6.4.5 Hoyer Group

- 6.4.6 Milkyway Intelligent Supply Chain

- 6.4.7 COSCO Shipping Group (COSCO Shipping Chemical)

- 6.4.8 Sumisho Global Logistics (China) Co.,Ltd

- 6.4.9 Bertschi

- 6.4.10 Sunward logistics co. ltd

- 6.4.11 SF Express

- 6.4.12 Kerry Logistics Network

- 6.4.13 BDP International

- 6.4.14 Rhenus Logistics

- 6.4.15 DHL Group

- 6.4.16 CEVA Logistics

- 6.4.17 Broekman Logistics

- 6.4.18 Yusen Logistics

- 6.4.19 Odyssey Logistics and Technology Corporation

- 6.4.20 DSV

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)