|

市場調查報告書

商品編碼

2063325

德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germany Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

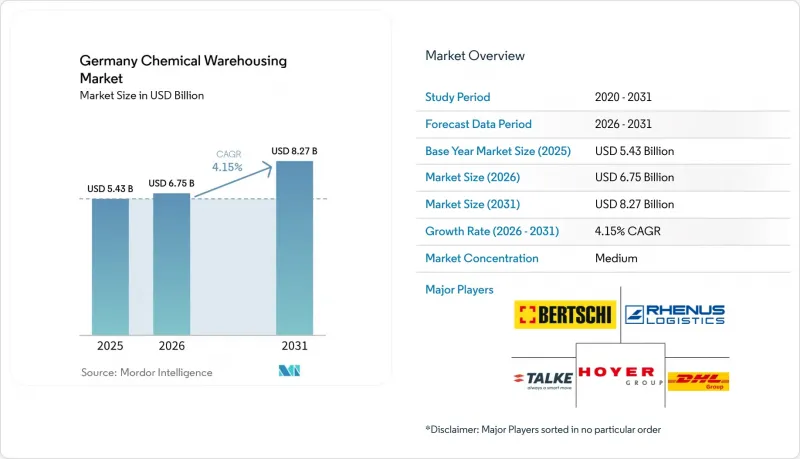

據 Mordor Intelligence 稱,德國化學品倉庫市場預計將從 2025 年的 54.3 億美元成長到 2026 年的 67.5 億美元,到 2031 年達到 82.7 億美元,預計 2026 年至 2031 年的複合年成長率為 4.15%。

德國化學成分的變化、REACH法規附件八的更嚴格規定以及電池材料叢集的崛起,正在以遠超傳統石化和特種化學品庫存管理的方式重塑儲存需求。本報告按倉庫類型(普通倉庫、特種化學品倉庫等)、化學品類型(易燃液體、腐蝕性物質等)和終端用戶行業(基礎化學品製造、特種化學品製造、製藥和生命科學、農業化學品等)進行細分。市場預測以美元計價。

德國化學品倉儲市場的趨勢與洞察

由於 REACH 附件 VIII 對儲存實施了更嚴格的規定,需求增加。

自2024年1月起,歐洲化學品管理局加強了審核力度,以檢驗倉庫是否能夠按批次分離和追蹤混合物,這要求倉庫升級庫存管理軟體、引入RFID標籤並安裝專用通風區域。到2025年,德國34%的受檢設施未能通過分離測試,導致每個中型設施的維修成本高達120萬至180萬歐元(13億至20億美元)。大規模第三方物流(3PL)公司正在其全國網路中分攤這些成本,從而增強了自身的定價能力。同時,小規模倉庫的利潤率面臨壓力,甚至被迫退出德國化學品倉儲市場。基於區塊鏈的儲存歷史管理模組正逐漸成為倉庫管理系統的標準配置,為大型營運商的業務收益。

東德電池材料產業的蓬勃發展帶動了對溶劑和電解倉庫的需求。

BASF位於施瓦茨海德的陰極材料工廠和諾斯沃特的超級工廠建設計畫,正在推動對鋰鹽和電解溶劑存儲的需求,這些存儲介質需要在濕度低於100ppm且充滿氮氣的環境下儲存。薩克森州和勃蘭登堡州的土地價格比西部低30-40%,這吸引了眾多開發商,他們渴望建造可與ISO標準儲罐清洗站整合的客製化「乾燥室」倉庫。隨著汽車製造商推行在地化供應鏈,連接東部化工中心和組裝廠的綜合運輸路線正在推動德國化學品倉儲市場向東轉移。

能源價格波動推高了冷氣和通風設備的運作成本。

2025年,歐洲工業用電價格依然高漲且波動劇烈,顯著推高了溫控倉庫和低溫倉庫的營運成本。與前一年相比,這導致冷凍和能源相關成本大幅增加。一些中型醫藥級物流業者難以重新談判長期固定價格能源契約,被迫退出部分德國化學品倉庫市場。雖然現場太陽能發電和電池儲能解決方案有助於減少對電網的依賴並提高效率,但其高昂的初始投資成本限制了這些方案的應用,目前主要僅限於資金雄厚的大型營運商。

細分市場分析

預計到2025年,特種化學品倉庫將佔德國化學品倉庫市場44.65%的佔有率,這得益於德國2,000億歐元(約2,343.6億美元)的化工產業基礎。溫控倉庫雖然規模較小,但預計將以5.77%的複合年成長率成長,這主要得益於生物製藥、mRNA疫苗以及需要-80°C至25°C多溫區儲存的高價值添加劑等產品的市場需求。節能型冷凍設備、機器人穿梭車和物聯網氣候感測器正使市場領導脫穎而出,而小規模的普通倉庫則難以獲得升級至DIN 14096標準的資金,並在德國化學品倉庫市場中不斷失去市場佔有率。

目前,第二波投資的重點是智慧低溫運輸樞紐,這類樞紐將-80°C的冷凍庫和2-8°C的儲藏室整合在同一設施內,從而降低細胞治療產品的運輸風險。業者若能將這些儲藏區與催化劑及電化學品專用部位結合,則可提升交叉銷售潛力。隨著產業持續整合,多溫區大型樞紐正逐漸成為製藥和特種化學品客戶的一站式服務中心。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於 REACH 附件 VIII 對儲存實施了更嚴格的規定,需求增加。

- 東德電池材料產業的蓬勃發展推高了對溶劑和電解倉儲空間的需求。

- 生化規模化生產需要隔離非基因改造儲存區域

- 在創新園區周圍安裝模組化「ChemCube」微型倉庫。

- 透過碳捕獲與利用(CCU)先導工廠創造對液態二氧化碳和暫時儲存的需求

- 鐵路港口(Vetwe路線和內陸地區之間)的電氣化將促進多模態化工樞紐的發展。

- 市場限制因素

- 能源價格波動推高了冷氣和通風設備的運作成本。

- DIN 14096 防火安全標準的收緊導致認證週期延長。

- 大規模鋰離子儲能領域監管規定的不明確性正在延緩投資決策。

- 由於公民舉措主導的反對運動,危險廢棄物處理設施的許可核准程序陷入停滯。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學物質類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Rhenus Logistics

- HOYER Group

- TALKE Logistics

- Bertschi AG

- Kuehne+Nagel

- Den Hartogh Logistics

- DSV

- Hellmann Worldwide Logistics

- CMA CGM Group(Including CEVA Logistics)

- Infraserv Logistics

- NOSTA Group

- DACHSER

- Yusen Logistics

- Nippon Express

- H.Essers

- Mainfreight

- C. Steinweg Group

- LogCoop GmbH

- WEILKE Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany chemical warehousing market size is expected to increase from USD 5.43 billion in 2025 to USD 6.75 billion in 2026 and reach USD 8.27 billion by 2031, growing at a CAGR of 4.15% over 2026-2031.

Germany's evolving chemicals mix, tighter REACH Annex VIII rules, and the rise of battery-materials clusters are reshaping storage requirements well beyond traditional petrochemical and specialty-chemical inventories. This report is Segmented by Warehouse Type (General Warehousing, Speciality Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, and More ). The Market Forecasts are Provided in Terms of Value (USD).

Germany Chemical Warehousing Market Trends and Insights

Enforcement-Driven Demand for REACH Annex VIII Compliant Storage

Since January 2024, the European Chemicals Agency has intensified audits that test whether warehouses can segregate and trace mixtures at the batch level, compelling upgrades in inventory software, RFID tagging, and dedicated ventilation zones. In 2025, 34% of inspected German facilities failed segregation tests, triggering retrofit bills of EUR 1.2-1.8 million (USD 1.3-2.0 billion) per mid-sized site. Larger 3PLs amortize these costs across national networks, gaining price power, while smaller depots face margin compression or forced exit from the Germany chemical warehousing market. Blockchain-based chain-of-custody modules are becoming standard add-ons to warehouse-management systems, creating a new tech-service revenue stream for leading operators.

East-German Battery-Materials Boom Boosting Solvent & Electrolyte Warehousing

BASF's cathode plant in Schwarzheide and Northvolt's gigafactory pipeline ignite demand for lithium-salt and electrolyte solvent storage engineered for <100 ppm humidity and nitrogen blanketing. Land in Saxony and Brandenburg costs 30-40% below western zones, drawing developers eager to supply bespoke "dry-room" warehouses that interface with ISO tank cleaning stations. As automotive OEMs push for regionalized supply chains, intermodal routes linking eastern chemical hubs to final assembly plants reinforce the Germany chemical warehousing market's eastward shift.

Volatile Energy Tariffs Inflating Refrigeration & Ventilation Opex

Industrial electricity prices in 2025 remained highly volatile and elevated across Europe, significantly increasing operating costs for temperature-controlled and sub-zero warehousing. This led to a meaningful rise in refrigeration and energy-related expenses year over year. Some mid-sized pharma-grade logistics operators were forced to exit parts of the German chemical warehousing market after struggling to renegotiate long-term fixed energy contracts. Although onsite solar and battery storage solutions help reduce grid dependence and improve efficiency, their high upfront capital requirements limit adoption mainly to larger, well-capitalized players.

Other drivers and restraints analyzed in the detailed report include:

- Biochemical Scale-Ups Requiring Segregated GMO-Free Storage Zones

- Deployment of Modular "ChemCube" Micro-Warehouses Near Innovation Campuses

- Stricter DIN 14096 Fire-Protection Code Prolonging Certification Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses represented 44.65% of the Germany chemical warehousing market size in 2025, anchored by the country's EUR 200 billion (USD 234.36 billion) chemicals base. Temperature-controlled depots, although smaller, are projected to grow at a 5.77% CAGR, driven by biologics, mRNA vaccines, and high-value excipients requiring -80 °C to 25 °C multipoint storage. Energy-efficient refrigeration, robotic shuttles, and IoT climate sensors differentiate market leaders, while smaller general warehouses struggle to finance DIN 14096 upgrades and lose share inside the Germany chemical warehousing market.

A second wave of investment now targets smart cold-chain nodes that co-locate -80 °C freezers and 2-8 °C rooms under one roof, cutting transit risks for cell therapies. Operators that combine these zones with specialty bays for catalysts or electronic chemicals increase cross-selling potential. As consolidation proceeds, multi-temperature mega-sites position themselves as one-stop hubs for pharmaceutical and specialty clients.

List of Companies Covered in this Report:

- DHL Group

- Rhenus Logistics

- HOYER Group

- TALKE Logistics

- Bertschi AG

- Kuehne+Nagel

- Den Hartogh Logistics

- DSV

- Hellmann Worldwide Logistics

- CMA CGM Group (Including CEVA Logistics)

- Infraserv Logistics

- NOSTA Group

- DACHSER

- Yusen Logistics

- Nippon Express

- H.Essers

- Mainfreight

- C. Steinweg Group

- LogCoop GmbH

- WEILKE Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enforcement-driven demand for REACH Annex VIII compliant storage

- 4.2.2 East-German battery-materials boom boosting solvent & electrolyte warehousing

- 4.2.3 Biochemical scale-ups requiring segregated GMO-free storage zones

- 4.2.4 Deployment of modular "ChemCube" micro-warehouses near innovation campuses

- 4.2.5 CCU pilot plants creating need for liquid CO2 and intermediate storage

- 4.2.6 Railport electrification (Betuweroute & Hinterland) catalysing multimodal chem hubs

- 4.3 Market Restraints

- 4.3.1 Volatile energy tariffs inflating refrigeration & ventilation Opex

- 4.3.2 Stricter DIN 14096 fire-protection code prolonging certification cycles

- 4.3.3 Regulatory limbo on Li-ion bulk storage delaying investment decisions

- 4.3.4 Burgerinitiative-led opposition stalling hazmat site permitting

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Rhenus Logistics

- 6.4.3 HOYER Group

- 6.4.4 TALKE Logistics

- 6.4.5 Bertschi AG

- 6.4.6 Kuehne+Nagel

- 6.4.7 Den Hartogh Logistics

- 6.4.8 DSV

- 6.4.9 Hellmann Worldwide Logistics

- 6.4.10 CMA CGM Group (Including CEVA Logistics)

- 6.4.11 Infraserv Logistics

- 6.4.12 NOSTA Group

- 6.4.13 DACHSER

- 6.4.14 Yusen Logistics

- 6.4.15 Nippon Express

- 6.4.16 H.Essers

- 6.4.17 Mainfreight

- 6.4.18 C. Steinweg Group

- 6.4.19 LogCoop GmbH

- 6.4.20 WEILKE Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)