|

市場調查報告書

商品編碼

2063338

日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Japan Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

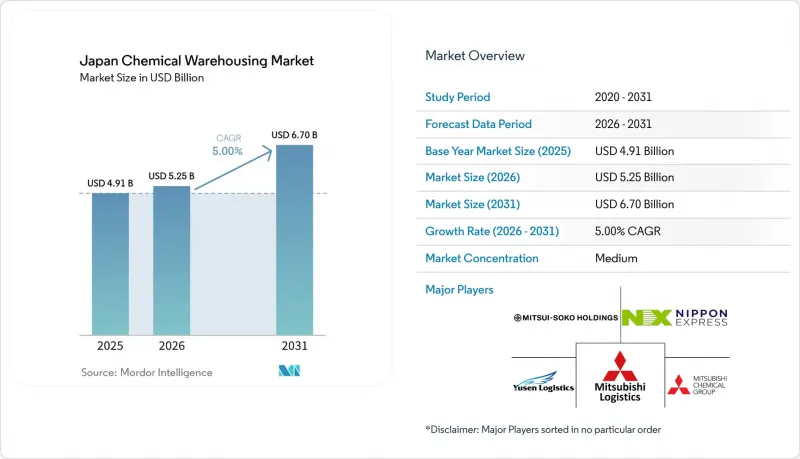

根據 Mordor Intelligence 預測,日本化學品倉庫市場規模將從 2025 年的 49.1 億美元和 2026 年的 52.5 億美元成長到 2031 年的 67 億美元,2026 年至 2031 年的複合年成長率為 5%。

本報告按倉庫類型(普通倉庫、特殊化學品倉庫、危險品倉庫等)、化學品類型(易燃液體、腐蝕性物質、氧化劑等)和終端用戶行業(基礎化學品製造、特種化學品製造、農藥等)進行細分。市場預測以以金額為準(十億美元)表示。

日本化學品倉儲市場的趨勢與洞察

在先進材料製造領域處於領先地位

日本向高附加價值特種化學品和醫藥中間體轉型,正在改變倉庫的設計和流程,經過驗證的環境和強大的可追溯性比倉儲容量本身更為阻礙因素。日本觸媒株式會社計畫到2027年將其吹田工廠的核酸原料藥產能提高十倍,這就需要更靠近生產車間的GMP級倉儲空間,以及延伸至倉庫的嚴格操作規範。FUJIFILM純藥株式會社計劃在2024年將其符合GMP標準的原料產能提高三倍,這強化了對溫度控制、製程分離和環境條件電子記錄等在地化需求。東和製藥的目標是到2026年實現年產175億片藥片,這將增加對毗鄰潔淨室的倉庫空間以及批次級精確存儲記錄的需求,以確保產品品質並滿足出貨時間。隨著生產轉向中高活性產品,倉儲價值密度增加,溫度偏差和操作失誤帶來的經濟風險也隨之增大,而數位追蹤正成為日常倉庫營運不可或缺的一部分。

製藥和生命科學領域的擴張

人口老化以及生物製藥和核酸療法的穩定發展,推動了對藥品倉庫的強勁需求,這需要品質保證、經過驗證的流程和冗餘系統來降低廢物風險。日本觸媒株式會社計劃在2027年前建立大規模的核酸原料藥GMP生產線,這表明不斷擴大的生產規模正與日益成長的合規存儲、數據完整性和清潔物流介面的需求相契合。處理高活性化合物以及藥品生產中常用溶劑和試劑的設施,也需要專門的危險物品區域和增強的通風系統。倉庫營運模式正在不斷發展,包括經過驗證的溫度監控、即時警報和符合審計要求的電子記錄,以滿足文件和運輸流程的需求。大阪和茨城等區域叢集正在工廠附近增加儲存容量,以支援與臨床和商業性時間表一致的準時制物流,同時確保合規性。

土地嚴重短缺和高成本

石化產業叢集和深水碼頭周邊適宜土地的匱乏限制了新建倉庫的建設,迫使開發商考慮位置以降低成本,但代價是犧牲了位置的便利性。工業區的城市規劃和建築法規持續對設計方案和工期施加壓力,尤其是對於需要不透水地面和洩漏控制系統的單層防火危險品設施而言。營運商正透過垂直儲存系統和提高自動化密度來增加有限用地面積內的處理能力,以此來應對挑戰。雖然這提高了經濟效益,但也增加了資本投入,並使未來的租戶變更更加複雜。擁有化學品回收資產的工業港口正在崛起為循環經濟中心,提升了附近保稅倉庫的價值,並增強了對進貨原料預分揀的能力。這些趨勢提升了維修多式聯運樞紐和棕地(可透過檢驗的消防措施和分區改造使其符合標準)的戰略價值。

細分市場分析

預計到2025年,特種化學品倉庫將佔日本化學品倉儲市場的41.24%。這反映了市場向高附加價值化合物產品轉型以及對嚴格安全規程日益成長的需求。將特種化學品存放在靠近生產線的位置,可以縮短生產週期,並嚴格區分不同批次和產品系列,這兩點對於符合GMP規範的原料和先進材料至關重要。雖然普通倉庫仍然處理散裝聚合物和通用原料,但營運商正在實施倉庫管理系統(WMS)和感測器,以滿足汽車和建設產業客戶精益補貨的需求。危險物品處理設施必須遵守《消防法》規定的特定數量標準,並根據需要採用不透水地板、泡沫滅火系統和防雷系統,因此其建造成本高於標準普通倉庫。對於需要檢驗的儲存環境、完整的儲存歷史記錄以及涵蓋物流流程中各個倉庫環節的可審計記錄的客戶而言,此類設施配置會增加轉換成本。

在日本化學品倉儲市場,溫控化學品倉庫佔據主導地位,預計2031年將以5.78%的強勁年複合成長率(CAGR)成長。這些設施憑藉其獨特的優勢脫穎而出,與獲得危險品認證的設施並駕齊驅,尤其注重防火結構、冗餘溫控系統和嚴格的可追溯性。目前的營運架構包括具備自動容錯移轉功能的備用發電機、持續的溫濕度監測、警報協議以及滿足審計要求的電子記錄。在多租戶設施中,為了應對因貨物混合存放而導致的危險品分類重疊,需要進行隔離,因此增設了自動防火百葉窗門和隔間式貨位。日本化學品倉儲產業在裝卸平台和高密度通道中也擴大採用機器人技術。這有助於緩解人事費用上升帶來的利潤壓力,並有助於恢復因2024年司機加班限制而損失的處理能力。這些投資共同重塑了所有類型倉庫的競爭格局。因為成熟的能力能夠實現溢價,而溢價反過來又支持再投資和合規性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在先進材料製造領域處於領先地位

- 製藥和生命科學領域的擴張

- 物流自動化與機器人簡介

- 精細化學品及中間體的成長

- 監管部門為促進安全基礎設施建設所做的努力

- 化學工業的重組

- 市場限制因素

- 土地嚴重短缺和高成本

- 勞動力老化和人手不足

- 遵守嚴格規定的負擔

- 高昂的能源成本和營運成本

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 地緣政治事件對市場的影響

- 循環經濟中的化學品回收

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學物質類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mitsubishi Logistics Corporation

- Mitsui-Soko Holdings Co., Ltd.

- Nippon Express Holdings

- Yusen Logistics Co., Ltd.(NYK Line)

- Mitsubishi Chemical Logistics Corp.(Subsidiary of Mitsubishi Chemical Corporation)

- LOGISTEED, Ltd

- SENKO Group Holdings Co., Ltd.

- Sanwa Soko Co., Ltd.

- Tatsumi Co., Ltd.

- Sankyu Logistics

- DHL Group

- Chikko Corporation

- Kuehne+Nagel

- Rhenus Logistics

- CEVA Logistics

- DSV

- Yasuda Logistics

- Tosoh Logistics Corporation

- AIT Worldwide Logistics, Inc.

- Odyssey Logistics and Technology(Japan)

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan chemical warehousing market size is projected to expand from USD 4.91 billion in 2025 and USD 5.25 billion in 2026 to USD 6.70 billion by 2031, registering a CAGR of 5% between 2026 to 2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and More), by Chemical Type (Flammable Liquids, Corrosives, Oxidizers, and More), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Agrochemicals, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

Japan Chemical Warehousing Market Trends and Insights

Advanced Materials Manufacturing Leadership

Japan's tilt toward high-value specialty chemicals and pharma intermediates is changing warehouse design and procedures, with validated environments and robust traceability becoming the constraint rather than bulk capacity. Nippon Shokubai plans to expand nucleic acid API capacity tenfold at its Suita site by 2027, which requires GMP-grade storage close to production and rigorous handling rules that extend into the warehouse. FUJIFILM Wako tripled its output capacity for GMP-compliant raw materials in 2024, strengthening local needs for temperature control, process segregation, and electronic documentation of environmental conditions. Towa Pharmaceutical targets 17.5 billion tablets annually by fiscal 2026, which will increase demand for cleanroom-adjacent warehousing and accurate lot-level custody logs to protect quality and meet release schedules. As production shifts to medium- and high-potency products, storage value density rises, increasing the financial stakes of temperature deviations and handling errors and pushing digital tracking into everyday warehousing practices.

Pharmaceutical and Life Sciences Expansion

An aging population and steady progress in biologics and nucleic acid therapies keep pharma warehousing demand resilient, requiring climate assurance, validated processes, and redundant systems to cut spoilage risk. Nippon Shokubai's program to install a large GMP production line for nucleic acid APIs by 2027 shows how manufacturing scales translate into heightened needs for compliant storage, data integrity, and clean logistics interfaces. Dedicated HAZMAT zones and enhanced ventilation are also relevant, as facilities handle higher-potency compounds alongside solvents and reagents common to pharma manufacturing. Warehouse operating models evolve to include validated temperature monitoring, real-time alerts, and audit-ready electronic records to satisfy documentation and release processes. Regional clusters in Osaka and Ibaraki are adding capacity near plants, supporting just-in-time flows for clinical and commercial timelines without compromising compliance.

Severe Land Scarcity and High Costs

Scarcity of suitable plots near petrochemical clusters and deep-water terminals constrains new warehouse construction and prompts developers to consider inland locations that trade proximity for lower costs. City planning and building rules in industrial belts keep pressure on design choices and timelines, especially for single-story fire-resistant HAZMAT facilities that require impermeable floors and spill containment. Operators respond with vertical storage systems and higher automation density to increase throughput within constrained footprints, improving economics but increasing capital requirements and complexity for future tenant changes. Circular-economy hubs are emerging at industrial ports that host chemical-recycling assets, thereby increasing the value of nearby bonded warehousing and pre-sorting capacity for inbound feedstock. These dynamics lift the strategic value of intermodal nodes and brownfield upgrades that can be brought up to code with validated fire protection and segregation.

Other drivers and restraints analyzed in the detailed report include:

- Logistics Automation and Robotics Adoption

- Regulatory Push for Safety Infrastructure

- Aging Workforce and Labor Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses held 41.24% of the Japan chemical warehousing market share in 2025, underscoring the country's shift toward high-value formulations and strict safety protocols. Specialty chemical storage near production lines supports fast cycle times and strict segregation between lots and product families, both of which are essential for GMP-compliant inputs and advanced materials. General warehousing still supports bulk polymers and commodity inputs, though operators are adding WMS and sensors to align with lean replenishment cycles for automotive and construction customers.HAZMAT sites follow Fire Service Act thresholds for designated quantities and adopt impermeable floors, foam suppression, and lightning protection, as relevant, which push construction costs beyond general warehouse norms. This mix increases switching costs for customers that require validated storage, a documented chain of custody, and audit-ready records covering the warehouse segment of the flow.

In the Japan chemical warehousing market, temperature-controlled chemical warehouses are leading the charge, boasting a robust 5.78% CAGR projected through 2031. These facilities, alongside HAZMAT-certified counterparts, stand out for their unique capabilities. Notably, they emphasize fire-resistant construction, climate redundancy, and meticulous traceability. The operational stack now spans backup generation with automatic failover, continuous temperature and humidity monitoring, alerting protocols, and electronic records that meet audit needs. Multi-tenant campuses add automated fire shutters and segregated bays because mixed stored goods bring overlapping hazard classifications that must be isolated. The Japan chemical warehousing industry is also lifting robotics adoption at docks and high-density aisles, which offsets margin pressure from rising wages and helps recover capacity lost to the 2024 driver overtime rules. Together, these investments are reshaping competitive positioning across warehouse types because validated capabilities command premium rates that support reinvestment and compliance upkeep.

List of Companies Covered in this Report:

- Mitsubishi Logistics Corporation

- Mitsui-Soko Holdings Co., Ltd.

- Nippon Express Holdings

- Yusen Logistics Co., Ltd. (NYK Line)

- Mitsubishi Chemical Logistics Corp. (Subsidiary of Mitsubishi Chemical Corporation)

- LOGISTEED, Ltd

- SENKO Group Holdings Co., Ltd.

- Sanwa Soko Co., Ltd.

- Tatsumi Co., Ltd.

- Sankyu Logistics

- DHL Group

- Chikko Corporation

- Kuehne + Nagel

- Rhenus Logistics

- CEVA Logistics

- DSV

- Yasuda Logistics

- Tosoh Logistics Corporation

- AIT Worldwide Logistics, Inc.

- Odyssey Logistics and Technology (Japan)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advanced Materials Manufacturing Leadership

- 4.2.2 Pharmaceutical and Life Sciences Expansion

- 4.2.3 Logistics Automation and Robotics Adoption

- 4.2.4 Fine Chemicals and Intermediates Growth

- 4.2.5 Regulatory Push for Safety Infrastructure

- 4.2.6 Chemical Industry Consolidation

- 4.3 Market Restraints

- 4.3.1 Severe Land Scarcity and High Costs

- 4.3.2 Aging Workforce and Labor Shortage

- 4.3.3 Stringent Regulatory Compliance Burden

- 4.3.4 High Energy and Operating Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geopolitical Events on the Market

- 4.9 Circular Economy Chemical Recycling

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Mitsubishi Logistics Corporation

- 6.4.2 Mitsui-Soko Holdings Co., Ltd.

- 6.4.3 Nippon Express Holdings

- 6.4.4 Yusen Logistics Co., Ltd. (NYK Line)

- 6.4.5 Mitsubishi Chemical Logistics Corp. (Subsidiary of Mitsubishi Chemical Corporation)

- 6.4.6 LOGISTEED, Ltd

- 6.4.7 SENKO Group Holdings Co., Ltd.

- 6.4.8 Sanwa Soko Co., Ltd.

- 6.4.9 Tatsumi Co., Ltd.

- 6.4.10 Sankyu Logistics

- 6.4.11 DHL Group

- 6.4.12 Chikko Corporation

- 6.4.13 Kuehne + Nagel

- 6.4.14 Rhenus Logistics

- 6.4.15 CEVA Logistics

- 6.4.16 DSV

- 6.4.17 Yasuda Logistics

- 6.4.18 Tosoh Logistics Corporation

- 6.4.19 AIT Worldwide Logistics, Inc.

- 6.4.20 Odyssey Logistics and Technology (Japan)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)