|

市場調查報告書

商品編碼

2063327

中東化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Middle East Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

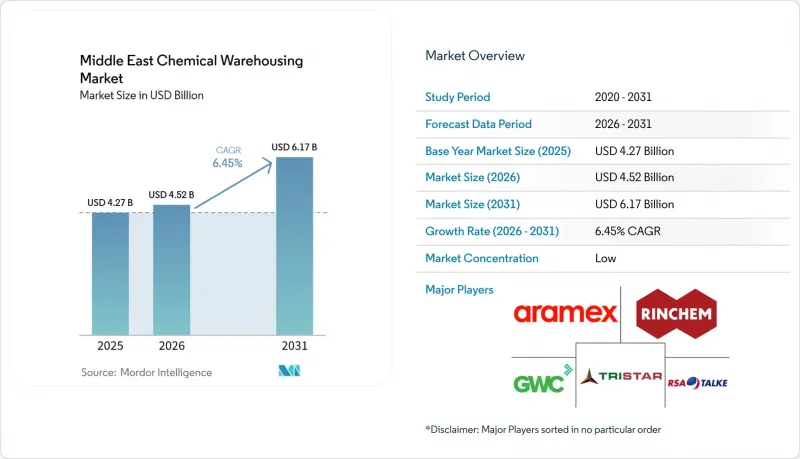

根據 Mordor Intelligence 預測,中東化學品倉庫市場規模將從 2025 年的 42.7 億美元成長到 2026 年的 45.2 億美元,到 2031 年將達到 61.7 億美元,2026 年至 2031 年的複合年成長率預計為 6.45%。

本報告按倉庫類型(普通倉庫、特種化學品倉庫等)、化學品類型(易燃液體、腐蝕性物質等)、終端用戶行業(基礎化學品製造等)和地區(沙烏地阿拉伯、阿拉伯聯合大公國、卡達、阿曼、科威特、巴林及其他中東國家)進行細分。市場預測以美元計價。

中東化學品倉庫市場趨勢與洞察

石化產業的主導正在推動對專用儲存的需求。

沿岸地區已運作的大規模綜合化工項目持續推動原料和聚合物的加工量成長,進而增加了對受監管的散裝和包裝化學品儲存的需求。在沙烏地阿拉伯,一家合資企業新建的混合原料裂解和下游裝置即將投入運作將產生大量的乙烯和聚乙烯產能,由此產生的危險材料、易燃液體和成品樹脂將需要港口和鐵路沿線的獨立儲存設施。在卡達,拉斯拉凡石化計畫將為出口市場供應乙烯和聚乙烯,因此需要符合危險品分類標準的儲槽設施、容器化樹脂儲存設施以及裝卸區域。中東化學品倉儲市場正透過提高消防系統密度、加強蒸氣管理以及升級公路和鐵路連接來應對工廠和港口之間的雙向物流需求。第三方倉儲業者也正在增加保稅區域和包裝線,以便根據全球出口文件和客戶規範對樹脂進行袋裝和桶裝包裝。這些努力確保中東化學品倉儲市場繼續與該地區主要的石化投資週期保持一致。

自由區和經濟城的發展將加速基礎建設。

專用物流區透過提供預建公用設施、簡化許可程序以及直接通往泊位和堆場的通道,加快了新建倉儲設施的專案進度。在沙烏地阿拉伯,NEOM 的 Oxagon 公司正在建立一個綜合價值鏈平台,該平台將貨運代理、倉儲和履約與自動化運輸和數位化視覺化相結合,從而減少化學品貨物流轉過程中的介面摩擦。 NEOM 港的 T1 碼頭計劃於 2026 年運作,屆時將配備自動化起重機和溫控存儲區,成為高價值、易碎貨物(需要穩定環境和快速閘口轉運)的關鍵樞紐。在卡達,自由區管理局透過吸引全球貨運代理商入駐拉斯布豐塔斯,擴展了物流生態系統。這為尋求跨境網路和可靠飛機貨艙空間(用於時效性要求高的貨物)的化學品處理商提供了更多選擇。這些措施正在促進自由區內混合、重新包裝和檢測能力的集中,為中東化學品倉儲市場創造了有利環境。

極端天氣條件會損害儲存設備的完整性並增加冷卻成本。

2025年,全部區域極端高溫和乾旱的疊加效應,加上超出歷史基準值的極端天氣和降雨不足,將給冷卻系統和電網帶來巨大壓力。對於倉庫業者而言,持續高溫會增加易燃液體的蒸氣風險,並加速儲存槽腐蝕,從而導致檢查頻率和維護工作量增加。用於存放醫藥中間體和特殊農藥的溫控室必須維持嚴格的溫度範圍,這會增加能源消耗,並需要在用電高峰期制定冗餘計畫。風險管理現在更加重視隔熱、蒸氣管理以及對危險物品區域進行主動氣體檢測。擾亂燃料和電力供應的地緣政治事件將進一步加劇氣候帶來的負擔。例如,2026年3月阿曼發生的事件迫使碼頭作業規模縮減,貨物運輸路線也被迫改變。這些情況提高了安全至關重要的倉儲設施的營運標準,並推動了中東化學品倉庫市場對高容錯冷卻和保護系統的投資。

細分市場分析

2025年,危險物品設施將佔據39.41%的市場。這主要得益於對易燃、腐蝕性、氧化性和有毒物質的安全要求,而這些物質正是該地區產品組合的特徵。在這一類別中,受該地區生命科學和特殊原料需求不斷成長的推動,預計2026年至2031年間,中東化學品倉庫市場中溫控設施的市場規模將以7.14%的複合年成長率成長。新建的貨櫃碼頭正在整合大規模溫控區、電氣設備和岸電,以便在處理易碎貨物的同時減少排放。第三方物流商正在實施保稅冷藏和合格流程,以滿足醫藥中間體和高純度化學品的審計追蹤要求。危險物品處理設施持續投資於泡沫滅火系統、氣體偵測裝置和隔離設施,以確保符合點火和暴露風險的要求。這些升級將加強中東化學品倉庫市場的加值服務水平,並降低高風險地區發生事故的機率。

通用化學品倉庫處理散裝非危險化學品、包裝材料和低風險配方,而特殊化學品設施則專注於塗料、黏合劑和電子級溶劑,並具備污染控制和可追溯性。具備溫控功能的業者正在擴展溫度映射、驗證和警報管理,以維持各區域之間嚴格的溫度控制。對於聚集在港口和自由區附近的跨國製造商而言,配備冷藏庫、塑膠袋包裝設施和品質檢查室的綜合危險品(HAZMAT)園區能夠最佳化從工廠到出口的流程。這些綜合設施與沙烏地阿拉伯和卡達的新生產佈局相契合,在這些國家,乙烯和聚乙烯產品在出口前將經過受監管的儲存場所。隨著產品系列朝向高價值、安全關鍵型中間體多元化發展,危險物品領域將持續成為中東化學品倉儲市場的基石。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 海灣合作理事會國家石化工廠擴建

- 「2030願景」大型企劃帶動建築化學品需求成長

- 根據ADR和IMO的規定,對危險物質進行更嚴格的合規性審核。

- 特種化學品分銷領域電子商務的成長

- 用於綠色氫氣和氨氣的先導工廠需要專用的倉儲設施

- 免稅區和自由貿易區細胞和基因治療的低溫運輸

- 市場限制因素

- 維修無氟滅火系統需要大量資金投入。

- 具備危險物品處理資格的倉庫工人短缺

- 沙塵暴造成的腐蝕風險導致保險免賠額增加。

- 區域內不含OFAS的泡騰發泡濃縮液供不應求

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學物質類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

- 國家

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 阿曼

- 科威特

- 巴林

- 其他中東國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- RSA TALKE

- Tristar Group

- Gulf Warehousing Company(GWC)

- Rinchem Company

- Aramex

- BDP International Logistic Services

- HOYER Group

- DHL Group

- Bertschi AG

- TLM International Freight Services LLC

- Kuehne+Nagel

- CEVA Logistics

- DSV

- Den Hartogh Logistics

- Noatum Holdings

- Azka Logistics

- Clarion Shipping

- Kanoo Logistics

- Geodis

- CH Robinson

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east chemical warehousing market size is expected to increase from USD 4.27 billion in 2025 to USD 4.52 billion in 2026 and reach USD 6.17 billion by 2031, growing at a CAGR of 6.45% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, and Specialty Chemical Warehouse and More), by Chemical Type (Flammable Liquids, Corrosives and More), by End-User Industry (Basic Chemicals Manufacturing, and More), and by Geography (Saudi Arabia, United Arab Emirates, Qatar, Oman, Kuwait, Bahrain, Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

Middle East Chemical Warehousing Market Trends and Insights

Petrochemical Industry Leadership Drives Specialized Storage Demand

Large integrated complexes commissioning across the Gulf are translating into sustained throughput of feedstocks and polymers, which lifts demand for compliant bulk and packaged chemical storage. In Saudi Arabia, new mixed feed cracking and downstream units under joint ventures are scheduled to bring high volume ethylene and polyethylene capacity online, which adds steady flows of flammable liquids and finished resins that need hazardous and segregated warehousing near port and rail links. In Qatar, the Ras Laffan petrochemicals project will supply ethylene and polyethylene volumes to export markets, which creates a requirement for tankage, containerized resin storage, and handling areas that meet hazardous classification standards. The Middle East chemical warehousing market is responding with higher fire suppression densities, vapor control, and road rail interface upgrades to handle two way flows between plants and ports. Third party storage providers are also adding bonded zones and packaging lines to support resin bagging and drumming that align with export documentation and global customer specs. These actions ensure the Middle East chemical warehousing market stays synchronized with the region's core petrochemical investment cycle.

Free Zone and Economic City Development Accelerates Infrastructure Build Out

Purpose-built logistics precincts are compressing project timelines for new storage capacity by providing ready utilities, simplified licensing, and direct access to berth and yard space. In Saudi Arabia, Oxagon at NEOM is building a unified supply chain platform that combines forwarding, warehousing, and fulfillment with automated handling and digital visibility, which reduces interface friction for chemical cargo flows. The Port of NEOM's T1 terminal, targeted for 2026, will introduce automated cranes and temperature-controlled storage areas, creating an anchor node for high-value and sensitive shipments that need stable conditions and fast gate moves. In Qatar, the free zones authority has expanded its logistics ecosystem by onboarding global freight integrators to Ras Bufontas, which raises the available options for chemical handlers seeking cross-border reach and reliable belly capacity for time-sensitive consignments. These initiatives encourage the co-location of blending, repacking, and testing capabilities inside free zones, which is a favorable setup for the Middle East chemical warehousing market.

Extreme Climate Conditions Compromise Storage Integrity and Escalate Cooling Costs

Compound heat and dryness events intensified across the region in 2025, with anomalies above historical baselines and concurrent precipitation deficits that stressed cooling systems and power grids. For warehouse operators, persistent heat increases vapor pressure risks for flammable liquids and accelerates corrosion in storage vessels, which raises inspection frequency and maintenance scope. Temperature-controlled rooms for pharmaceutical intermediates and specialty agrochemicals must hold tight bands, which lift energy draw and require redundancy planning for peak months. Risk controls now place greater emphasis on insulation, vapor management, and active monitoring for gas detection across HAZMAT zones. Geopolitical events that disrupt fuel and power supply compound climate stress, as seen with the March 2026 incident in Oman that reduced terminal operations and rerouted cargo. These dynamics increase the operating baseline for safety critical storage and push the Middle East chemical warehousing market to invest in resilient cooling and protection systems.

Other drivers and restraints analyzed in the detailed report include:

- Downstream Chemical Integration Creates Captive Warehousing Demand

- Vision 2030 Economic Diversification Underpins Long Term Policy Support

- Water Scarcity and Desalination Dependency Inflate Industrial Operating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hazardous materials facilities commanded 39.41% in 2025, supported by safety requirements for flammables, corrosives, oxidizers, and toxic substances that define the region's product mix. Within this category, the Middle East chemical warehousing market size for temperature-controlled facilities is projected to expand at a 7.14% CAGR between 2026 and 2031 as life sciences and specialty inputs scale in the region. New container terminals are incorporating large temperature-controlled zones, electric equipment, and shore power, which supports the handling of sensitive cargo with lower emissions. Third-party logistics providers are adding bonded cold rooms and qualification protocols to meet audit trails for pharmaceutical intermediates and high-purity chemicals. HAZMAT sites continue to invest in foam-based fire suppression, gas detection, and segregated containment to maintain compliance against ignition and exposure risks. These upgrades reinforce premium service tiers in the Middle East chemical warehousing market and reduce incident probability in high-hazard zones.

General chemical warehouses serve bulk non-hazardous chemicals, packaging inputs, and lower-risk formulations, while specialty chemical facilities cater to coatings, adhesives, and electronic-grade solvents with contamination controls and traceability. Operators pursuing temperature-controlled business are expanding mapping, validation, and alarm management to sustain narrow bands across zones. For multinational producers that cluster near ports and free zones, integrated HAZMAT campuses with cold rooms, resin bagging, and quality labs improve flow from plant to export channels. This integrated setup aligns with new production in Saudi Arabia and Qatar, where ethylene and polyethylene output will move through compliant storage nodes before export. The hazardous materials segment will remain the anchor of the Middle East chemical warehousing market as product portfolios diversify into higher value, safety-critical intermediates.

List of Companies Covered in this Report:

- RSA TALKE

- Tristar Group

- Gulf Warehousing Company (GWC)

- Rinchem Company

- Aramex

- BDP International Logistic Services

- HOYER Group

- DHL Group

- Bertschi AG

- TLM International Freight Services LLC

- Kuehne + Nagel

- CEVA Logistics

- DSV

- Den Hartogh Logistics

- Noatum Holdings

- Azka Logistics

- Clarion Shipping

- Kanoo Logistics

- Geodis

- C.H. Robinson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Petrochemical Capacity Build-Outs Across GCC

- 4.2.2 Vision 2030 Mega-Project Demand for Construction Chemicals

- 4.2.3 Tightening ADR/IMO-Aligned Hazmat Compliance Audits

- 4.2.4 E-Commerce Growth in Specialty Chemical Distribution

- 4.2.5 Green-Hydrogen and Ammonia Pilot Plants Needing Dedicated Storage

- 4.2.6 Duty-Free Free-Zone Cold Chains for Cell & Gene Therapies

- 4.3 Market Restraints

- 4.3.1 High Capex for Fluorine-Free Fire-Suppression Retrofits

- 4.3.2 Shortage of DG-Certified Warehouse Labor

- 4.3.3 Sand-Storm Corrosion Risk Raising Insurance Deductibles

- 4.3.4 Limited Regional Supply of OFAS-Free Foam Concentrates

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Oman

- 5.4.5 Kuwait

- 5.4.6 Bahrain

- 5.4.7 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 RSA TALKE

- 6.4.2 Tristar Group

- 6.4.3 Gulf Warehousing Company (GWC)

- 6.4.4 Rinchem Company

- 6.4.5 Aramex

- 6.4.6 BDP International Logistic Services

- 6.4.7 HOYER Group

- 6.4.8 DHL Group

- 6.4.9 Bertschi AG

- 6.4.10 TLM International Freight Services LLC

- 6.4.11 Kuehne + Nagel

- 6.4.12 CEVA Logistics

- 6.4.13 DSV

- 6.4.14 Den Hartogh Logistics

- 6.4.15 Noatum Holdings

- 6.4.16 Azka Logistics

- 6.4.17 Clarion Shipping

- 6.4.18 Kanoo Logistics

- 6.4.19 Geodis

- 6.4.20 C.H. Robinson

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)