|

市場調查報告書

商品編碼

2063337

義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Italy Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

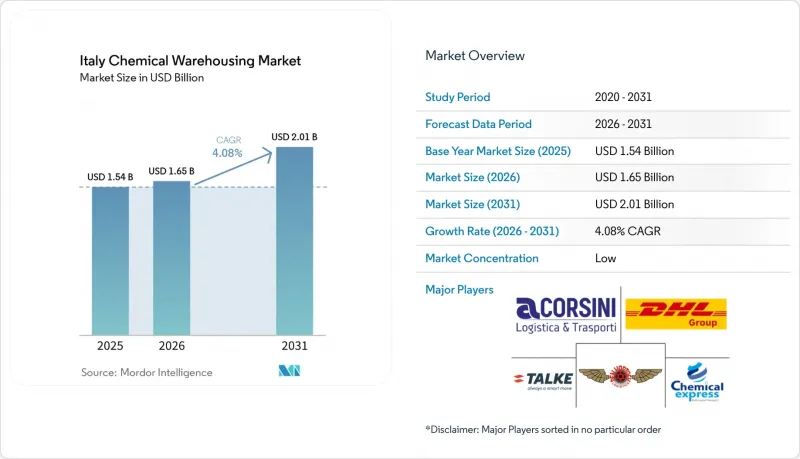

根據 Mordor Intelligence 預測,義大利化學品倉庫市場規模將從 2025 年的 15.4 億美元成長到 2026 年的 16.5 億美元,到 2031 年達到 20.1 億美元,預計 2026 年至 2031 年的複合年成長率為 4.08%。

本報告按倉庫類型(普通倉庫、特殊化學品倉庫、危險品倉庫及其他)、化學品類型(易燃液體、腐蝕性物質、有毒物質及其他)和終端用戶行業(基礎化學品製造、農藥、食品和飼料添加劑及其他)進行細分。市場預測以以金額為準(十億美元)呈現。

義大利化學品倉庫市場的趨勢與洞察

在製藥和精細化工領域主導作用

義大利出口主導製藥業及其在精細特種化學品領域的專業技術,持續推動義大利化學品倉儲市場對高規格倉儲設施的需求,包括符合序列化和產品完整性要求的溫控和GMP合規區域。到2025年,出口導向業務將佔製藥業的90%,這將持續支撐對檢驗的倉儲設施、保稅區以及與全球航運路線相銜接的品管轉運點的需求。義大利CDMO(合約研發生產組織)產能的擴張,導致產品上市更加頻繁,小批量生產的複雜性也隨之增加。這使得義大利化學品倉儲市場對具備可追溯性、監控能力以及針對原料藥藥(API)和精密中間體進行專業處理的倉庫產生了需求。第三方物流商正利用Lombardia生命科學和化學工業中心的優勢,在關鍵研發和製造地附近建立專用的醫藥級倉儲設施。藥品和精細化學品的出口總額不斷成長,使得義大利叢集化學品倉儲市場對高品質倉儲設施的需求日益凸顯。

在地中海貿易的戰略定位

港口主導的產能擴張正在鞏固義大利在化學品倉儲市場中的地位,使其成為中東、歐洲和北美之間化學品及中間體的進口和轉運樞紐。熱那亞的「新防波堤」計畫投資13億歐元(14.3億美元),旨在提升超大型貨櫃船的接收和裝卸能力。預計這將帶來大規模的船舶停靠和更大的船舶帶來的規模經濟效益。鑑於義大利相當一部分化學原料以石腦油為基礎,並與中東供應鏈緊密相連,這種進口結構與原料的實際情況密切相關,從而支撐了義大利化學品倉儲市場港口區域對倉儲和陸路運輸的穩定需求。位於利沃諾的Dalsena Europa擴建計畫由歐洲投資銀行提供的9,000萬歐元(9,900萬美元)貸款資助,為托斯卡納和義大利中部的特種化學品製造商提供額外的貨櫃運力和物流選擇。的里雅斯特的鐵路基礎設施由歐洲計劃共同出資建設,將亞得里亞海沿岸的物流與中東歐走廊連接起來,為義大利化學品倉儲市場的化學品倉儲企業創造了跨境分銷機會。

官僚主義作風複雜,辦理許可證耗時過長

在義大利化學品倉庫市場,危險物品處理設施的許可審核流程仍然十分漫長。這是因為營運商必須接受多個機構的審核,並符合SEVESO III法規規定的外部緊急時應對計畫的要求。 2026年是更高等級SEVESO設施安全報告更新的最後期限,這進一步加劇了內部資源的壓力,短期內合規性優先於擴張。處理易燃、腐蝕性或有毒物質的倉庫必須考慮風險情境和外部事件建模,這使得義大利化學品倉庫市場的批准和檢查更加複雜。這些義務可能會延長工程的關鍵路徑,尤其是在待開發區中,因為新建案也需要特殊的土地使用許可和與地方當局的協調。因此,為了保持發展勢頭,義大利化學品倉庫市場通常更傾向於對現有場地進行棕地和擴建。

細分市場分析

截至2025年,特種化學品倉庫將佔據倉庫類型中最大的佔有率,達到38.94%。這反映了義大利對精細化學品和特種化學品的重視,以及義大利化學品倉庫市場對獨立、品質保證的儲存空間的需求。溫控設施的成長速度最快,複合年成長率達5.64%。這是因為醫藥相關貨物需要2-8°C的穩定溫度環境、檢驗的儲存區域以及可追溯的審計記錄,這些都有助於支持義大利化學品倉庫市場的出口流通以及從臨床階段到商業階段的過渡。營運商透過專門的危險品管理、文件管理以及針對生物技術和先進療法等小批量、高價值貨物的產品完整性保證來脫穎而出。這些要求與北部叢集的情況相符,該地區的生命科學和特殊化學品製造商正在擴大其生產和出口週期。在義大利化學品倉庫市場,能夠將GMP標準、危險品風險管理和快速服務水準相結合,以應對頻繁的產品更新和短生命週期庫存的設施仍然備受青睞。

危險物品倉庫對於易燃、腐蝕性、有毒和氧化性物質的儲存至關重要,管理體制正在推動需求成長,同時也促進了義大利化學品倉庫市場的循環經濟發展。 2025年5月,TALKE在科思創化學園區的菲拉戈開設了一座佔地2萬平方公尺的危險品儲存設施。目前正在進行根據《塞維索法案》獲得許可的準備工作,並計劃未來擴建儲罐和筒倉,這凸顯了Lombardia經認證的危險品儲存設施的長期發展趨勢。向循環聚合物和化學品回收的轉型正在增加義大利化學品倉庫市場的入庫和中間物流流量,尤其是在煉油廠和聚合物製造地附近,這需要進行分類、追溯和品管。通用倉庫對於預包裝助劑和消費化學品仍然十分重要,但物流房地產的競爭正在推動主要交通走廊附近棕地的再開發。因此,義大利化學品倉儲產業正在努力平衡高價值儲存空間(需要符合監管規定)與靈活的普通儲存空間(以適應不斷變化的產品系列)。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在製藥和精細化工領域處於領先地位

- 在地中海的戰略貿易地位

- 特種化學品產業的成長

- 北部工業三角區的發展

- 農化製造地

- 綠色轉型與生物基化學品

- 市場限制因素

- 官僚主義作風複雜,辦理許可證耗時過長

- 分散的物流網路

- 高昂的人事費用和合規成本

- 缺乏可用的未開發土地

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 地緣政治事件對市場的影響

- 循環經濟中的化學品回收

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學類型

- 易燃液體

- 腐蝕性物質

- 有毒物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 殺蟲劑

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Talke Logistics

- Den Hartogh Logistics

- Corsini Srl

- Chemical Express

- Kuehne+Nagel

- DSV

- Brenntag Italia

- Rhenus Logistics

- CEVA Logistics

- CH Robinson

- HOYER Group

- Bertschi AG

- Savino Del Bene

- Geodis

- Dachser Logistics

- Gruber Logistics

- Yusen Logistics

- Due Torri

- AIT Worldwide Logistics, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the italy chemical warehousing market size is expected to increase from USD 1.54 billion in 2025 to USD 1.65 billion in 2026 and reach USD 2.01 billion by 2031, growing at a CAGR of 4.08% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, and More), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, and More), and by End-User Industry (Basic Chemicals Manufacturing, Agrochemicals, Food & Feed Additives, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

Italy Chemical Warehousing Market Trends and Insights

Pharmaceutical and Fine Chemicals Leadership

Export-led pharmaceuticals and Italy's specialization in fine and specialty chemicals continue to propel high-spec storage, including temperature-controlled and GMP-compliant areas that meet serialization and product integrity requirements in the Italy chemical warehousing market. In 2025, the pharmaceutical sector's 90% export orientation supported recurring demand for validated storage, customs-bonded zones, and quality-controlled staging aligned with global shipping lanes. CDMO capacity in Italy added higher-frequency product launches and small-batch complexity, requiring warehouses to add traceability, monitoring, and specialized handling for APIs and sensitive intermediates in the Italy chemical warehousing market. Third-party logistics providers are capitalizing on Lombardy's life sciences and chemical hubs by setting up dedicated pharma-grade operations near key research and manufacturing sites. The combined weight of pharma exports and fine chemicals strengthens demand visibility for premium storage across northern clusters in the Italy chemical warehousing market.

Strategic Mediterranean Trade Position

Port-led capacity additions reinforce Italy's import and transshipment role for chemicals and intermediates flowing between the Middle East, Europe, and North America in the Italy chemical warehousing market. Genoa's New Breakwater project is sized to accommodate ultra-large container vessels and increase throughput, with an investment of EUR 1.3 billion (USD 1.43 billion), supporting larger call sizes and scale economies from vessel upsizing. The import footprint ties into feedstock realities, given that a material share of Italy's chemical inputs are naphtha-based and linked to Middle Eastern supply chains, which underpins consistent inbound demand for port-area storage and drayage in the Italy chemical warehousing market. Livorno's Darsena Europa expansion, financed by the European Investment Bank at EUR 90 million (USD 99 million), provides additional container capacity and logistics optionality for specialty producers in Tuscany and central Italy. Trieste's rail-linked infrastructure, co-financed through European programs, aligns Adriatic flows with Central and Eastern European corridors, creating cross-border distribution opportunities for chemical warehousing in the Italy chemical warehousing market.

Bureaucratic Complexity and Permitting Delays

Permitting timelines for hazardous goods facilities remain lengthy because operators must satisfy multi-agency reviews and external emergency planning requirements under SEVESO III in the Italy chemical warehousing market. The 2026 deadline for upper-tier Seveso establishments to update safety reports adds pressure on internal resources, prioritizing compliance over expansion in the near term. Warehouses that handle flammable, corrosive, or toxic substances must account for risk scenarios and external event modeling, which complicates approvals and inspections in the Italy chemical warehousing market. These obligations can stretch project critical paths, especially for greenfield builds that also need land-use variances and municipal alignment. As a result, brownfield conversions and capacity expansions at existing sites are often favored to maintain momentum in the Italy chemical warehousing market.

Other drivers and restraints analyzed in the detailed report include:

- Specialty Chemicals Sector Growth

- Northern Industrial Triangle Development

- High Labor and Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses held the largest share of 38.94% of the warehouse type in 2025, reflecting Italy's concentration in fine and specialty chemicals and the need for segregated, quality-assured storage in the Italy chemical warehousing market. Temperature-controlled facilities show the fastest expansion with 5.64% CAGR as pharma-related volumes require 2 to 8 degrees Celsius stability, validated storage zones, and audit trails to support export flows and clinical-to-commercial transitions in the Italian chemical warehousing market. Operators differentiate with dedicated Dangerous Goods management, documentation control, and product integrity assurance for small-batch, high-value shipments typical of biotech and advanced therapies. These requirements align with northern clusters where life sciences and specialty chemical producers scale production and export cycles. The Italy chemical warehousing market continues to reward sites that can combine GMP standards, risk controls for hazardous goods, and responsive service levels to manage frequent product refresh and short-lifecycle inventories.

Hazardous materials warehouses are pivotal for flammable, corrosive, toxic, and oxidizing substances, and regulatory regimes reinforce their demand, and circular economy flows in the Italy chemical warehousing market. In May 2025, TALKE opened a 20,000 square meter hazardous goods site at Filago within the Covestro Chemical Park, with preparations for Seveso permits and future tank and silo capacity, which underlines the long-term buildout of certified hazardous storage in Lombardy. The pivot to circular polymers and chemical recycling adds inbound and intermediate flows that require separation, traceability, and quality-control steps near refinery and polymer sites in the Italy chemical warehousing market. General-purpose warehousing remains relevant for packaged auxiliaries and consumer chemicals, although competition for logistics real estate encourages brownfield redevelopment close to major corridors. The Italy chemical warehousing industry, therefore, balances premium, compliance-heavy capacity with flexible general storage to serve a changing product portfolio.

List of Companies Covered in this Report:

- DHL Group

- Talke Logistics

- Den Hartogh Logistics

- Corsini Srl

- Chemical Express

- Kuehne + Nagel

- DSV

- Brenntag Italia

- Rhenus Logistics

- CEVA Logistics

- C.H. Robinson

- HOYER Group

- Bertschi AG

- Savino Del Bene

- Geodis

- Dachser Logistics

- Gruber Logistics

- Yusen Logistics

- Due Torri

- AIT Worldwide Logistics, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pharmaceutical and Fine Chemicals Leadership

- 4.2.2 Strategic Mediterranean Trade Position

- 4.2.3 Specialty Chemicals Sector Growth

- 4.2.4 Northern Industrial Triangle Development

- 4.2.5 Agrochemical Manufacturing Base

- 4.2.6 Green Transition and Bio-Based Chemicals

- 4.3 Market Restraints

- 4.3.1 Bureaucratic Complexity and Permitting Delays

- 4.3.2 Fragmented Logistics Network

- 4.3.3 High Labor and Compliance Costs

- 4.3.4 Limited Greenfield Land Availability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geopolitical Events on the Market

- 4.9 Circular Economy Chemical Recycling

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Talke Logistics

- 6.4.3 Den Hartogh Logistics

- 6.4.4 Corsini Srl

- 6.4.5 Chemical Express

- 6.4.6 Kuehne + Nagel

- 6.4.7 DSV

- 6.4.8 Brenntag Italia

- 6.4.9 Rhenus Logistics

- 6.4.10 CEVA Logistics

- 6.4.11 C.H. Robinson

- 6.4.12 HOYER Group

- 6.4.13 Bertschi AG

- 6.4.14 Savino Del Bene

- 6.4.15 Geodis

- 6.4.16 Dachser Logistics

- 6.4.17 Gruber Logistics

- 6.4.18 Yusen Logistics

- 6.4.19 Due Torri

- 6.4.20 AIT Worldwide Logistics, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)