|

市場調查報告書

商品編碼

2073652

德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germany Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

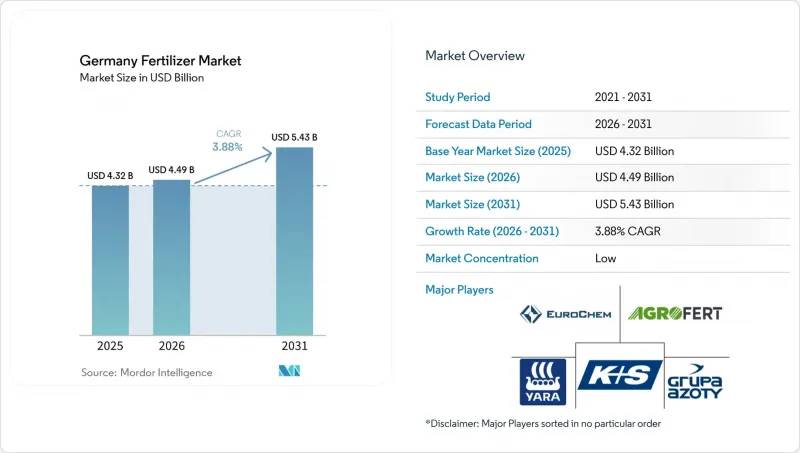

根據 Mordor Intelligence 估計,德國化肥市場在 2026 年的價值為 43.2 億美元,高於 2025 年的 44.9 億美元,預計到 2031 年將達到 54.3 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 3.88%。

本報告按類型(複合肥和單質肥)、形態(常規型和特種型)、施用方法(施肥/灌溉、葉面噴布、土壤施用)和作物類型(田間作物、園藝作物、草坪和觀賞作物)進行分類。市場預測以價值(美元)和數量(公噸)表示。

德國化肥市場的趨勢與洞察

精密農業中施肥和灌溉的蓬勃發展

德國的精密農業革命正在從根本上改變肥料的施用方式,商業農場採用肥料和灌溉系統的比例也達到了前所未有的高度。物聯網感測器、GPS導航施肥設備和變數施肥技術的整合,使農民能夠以前所未有的精準度最佳化養分輸送,在最大限度提高作物產量的同時降低投入成本。如今,數位化農業平台能夠即時監測土壤狀況,並根據天氣模式、作物生長階段和養分有效性動態調整肥料用量。

對高效肥料的需求

含有緩釋穩定氮和硝化抑制劑的產品能夠防止養分揮發和淋溶,這在硝酸鹽脆弱性土地佔農地28%的地區尤其重要。BASF在路德維希港投資1.5億歐元(1.63億美元)擴大了當地尿素酶抑制劑包衣的供應。同時,隨著農民逐漸意識到減少施肥頻率和提高產量穩定性的優勢,高價產品的價格差距正在縮小。高效能肥料的溢價通常比傳統產品高出20-30%,但其減少施肥頻率和提高作物產量可以抵消此溢價,使這些技術對先進農戶而言具有經濟可行性。

更嚴格限制硝酸鹽的使用。

在德國,修訂後的肥料法規正日益限制硝酸鹽的使用,約束傳統的肥料使用模式,迫使農民調整養分管理策略。隨著硝酸鹽敏感區域的增加,目前約有28%的德國農地受到影響,這意味著氮肥施用量需比作物需求量減少高達20%。這些法規對傳統上依賴大量氮肥投入以實現產量最大化的集約化作物生產系統構成了特別嚴峻的挑戰。

細分市場分析

到2025年,單一營養素肥料將佔德國肥料市場佔有率的65.8%,反映出德國農民偏好能夠實現精準養分管理和成本最佳化的單營養素產品。此細分市場的主導地位歸功於其施肥方案的靈活性,可以根據土壤分析結果和作物特定需求進行客製化。尿素因其高養分含量和與精準施肥設備的兼容性,仍是主要的氮肥來源。另一方面,氯化鉀(MoP)作為主要的鉀肥,仍然保持著穩固的地位。此外,隨著土壤分析計畫不斷發現集約化農業系統中存在的養分缺乏問題,對鋅、硼和錳等單微量元素肥料的需求也不斷成長。

複合肥料佔據剩餘的市場佔有率,並且在那些出於人事費用考慮而傾向於採用單一施肥方案而非多次施用單一肥料的地區,複合肥越來越受歡迎。預計該細分市場將實現最快成長,2026年至2031年的複合年成長率預計將達到4.7%。這一成長主要得益於市場對均衡營養配方、更高施肥效率和簡化養分管理的需求不斷成長。 DAP和NPK複合肥料等產品受益於強調最佳化養分供應的綜合養分管理方法和精密農業系統的應用。預計德國各地對營運效率和作物營養均衡的日益重視將進一步推動複合肥料的需求。

預計到2025年,傳統肥料將佔德國肥料市場81.1%的佔有率,顯示傳統的顆粒狀和微量複合肥料在德國農業中仍然佔據重要地位。這一市場的穩定性反映了農民對傳統肥料的熟悉程度,以及這些肥料與現有施肥設備和儲存設施的高度相容性。顆粒狀尿素、磷酸二銨和鉀肥產品仍然是德國作物生產的主要肥料,以具有競爭力的價格提供可靠的養分供應。傳統肥料受益於成熟的供應鏈、標準化的品質規範和廣泛的分銷網路,確保了產品在所有農業地區的供應。

特種肥料是成長最快的細分市場,預計到2031年將以5.2%的複合年成長率成長,這主要受監管壓力和農民對更佳性能需求的推動。緩釋肥(CRF)在高價值作物生產中的市佔率不斷擴大,其高價位得益於其能根據植物吸收模式精準調節養分釋放。水溶性肥料在溫室栽培和施肥/灌溉領域呈現強勁成長勢頭,精準的養分管理和植物的快速反應是成功的關鍵因素。在注重環保的地區,由於硝酸鹽淋溶法規的限制,緩釋配方更受青睞,因此緩釋肥(SRF)也得到了廣泛應用。液體肥料的應用範圍正從傳統的葉面噴布噴施擴展到土壤注射和施肥/灌溉系統,與乾粉產品相比,液體肥料具有更好的混合性能和更低的搬運成本。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 大田作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 主要營養素

- 田間作物

- 園藝作物

- 次要營養元素

- 田間作物

- 園藝作物

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 精密農業中施肥和灌溉的蓬勃發展

- 對高效肥料的需求

- 溫室和水耕種植的擴張

- 農產品價格上漲和農業收入增加

- 聯邦腐殖質碳權計劃

- 綠色氨進口路線

- 市場限制因素

- 更嚴格限制硝酸鹽的使用。

- 天然氣和磷礦石價格波動。

- 抗議活動引發的政策不確定性

- 蛋白質作物的輪作正在降低氮的需求。

第5章 市場規模與成長預測

- 類型

- 複雜類型

- 直的

- 微量營養素

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 氮基

- 尿素

- 其他

- 磷酸鹽基

- DAP

- MAP

- SSP

- TSP

- 鉀基

- MoP

- SoP

- 次要大量營養元素

- 鈣

- 鎂

- 硫

- 微量營養素

- 形式

- 傳統的

- 專業領域

- CRF

- 液體肥料

- SRF

- 水溶性

- 應用模式

- 施肥和灌溉

- 葉面噴布

- 土壤

- 農作物種類

- 田間作物

- 園藝作物

- 草坪和觀賞植物

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- AGLUKON Spezialduenger GmbH & Co. KG

- AGROFERT AS(AGROFERT Group)

- BASF SE

- Bayer AG

- CF Industries Holdings Inc.

- EuroChem Group AG

- Grupa Azoty SA

- Haifa Group

- ICL Group Ltd.

- Kingenta Ecological Engineering Group Co., Ltd.(Kingenta Group)

- K+S Aktiengesellschaft

- Mosaic Company

- Nutrien Ltd.

- PhosAgro PJSC

- Yara International ASA

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, germany fertilizer market size in 2026 is estimated at USD 4.32 billion, growing from 2025 value of USD 4.49 billion with 2031 projections showing USD 5.43 billion, growing at 3.88% CAGR over 2026-2031.

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Germany Fertilizer Market Trends and Insights

Precision-ag fertigation boom

Germany's precision agriculture revolution is fundamentally reshaping fertilizer application methods, with fertigation systems experiencing unprecedented adoption rates among commercial growers. The integration of IoT sensors, GPS-guided application equipment, and variable-rate technology enables farmers to optimize nutrient delivery with unprecedented precision, reducing input costs while maximizing crop yields. Digital agriculture platforms now monitor soil conditions in real-time, allowing for dynamic fertilizer adjustments based on weather patterns, crop growth stages, and nutrient availability.

Demand for enhanced-efficiency fertilizers

Controlled-release, stabilized nitrogen, and nitrification-inhibitor products shield nutrients from volatilization and leaching, a key advantage as nitrate-vulnerable zones rise to 28% of farmland. BASF's investment of EUR 150 million (USD 163 million) at Ludwigshafen expands the local supply of urease-inhibitor coatings, while premium pricing gaps tighten as growers factor in fewer passes and higher yield stability. The premium pricing of enhanced-efficiency fertilizers, typically 20-30% higher than conventional products, is being offset by reduced application frequency and improved crop performance, making these technologies economically viable for progressive farmers.

Stricter Nitrate Application Caps

Germany's implementation of increasingly restrictive nitrate application limits under the revised Fertilizer Ordinance is constraining traditional fertilizer usage patterns and forcing farmers to reconsider their nutrient management strategies. The designation of additional nitrate-vulnerable zones, now covering approximately 28% of German agricultural land, imposes mandatory reductions in nitrogen application rates of up to 20% compared to crop requirements. These restrictions are particularly challenging for intensive crop production systems that have historically relied on high nitrogen inputs to maximize yields.

Other drivers and restraints analyzed in the detailed report include:

- Greenhouse and hydroponic expansion

- Rising crop prices and farm income

- Volatile Gas and Phosphate-Rock Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers command 65.8% of Germany fertillizers market share in 2025, reflecting German farmers' preference for single-nutrient products that enable precise nutrient management and cost optimization. The segment's dominance stems from the flexibility it provides in customizing fertilizer programs based on soil testing results and crop-specific requirements. Urea remains the leading nitrogen source due to its high nutrient content and compatibility with precision application equipment, while muriate of potash (MoP) maintains a strong position as the primary potassium fertilizer. Demand for straight micronutrient fertilizers, including zinc, boron, and manganese products, is also increasing as soil testing programs continue to identify nutrient deficiencies in intensive cropping systems.

Complex fertilizers account for the remaining market share and are gaining popularity in regions where single-application nutrient programs are preferred over multiple straight fertilizer treatments due to labor cost considerations. The segment is projected to be the fastest-growing, registering a CAGR of 4.7% from 2026 to 2031. Growth is driven by increasing demand for balanced nutrient formulations, improved application efficiency, and simplified nutrient management. Products such as DAP and NPK formulations are benefiting from the adoption of integrated nutrient management practices and precision farming systems that emphasize optimized nutrient delivery. The growing focus on operational efficiency and balanced crop nutrition is anticipated to further support demand for complex fertilizers across Germany.

Conventional fertilizers maintain 81.1% of the Germany fertillizers market size in 2025, demonstrating the continued importance of traditional granular and prilled formulations in German agriculture. The segment's stability reflects farmers' familiarity with conventional products and their compatibility with existing application equipment and storage infrastructure. Granular urea, DAP, and potash products remain the workhorses of German crop production, offering reliable nutrient delivery at competitive prices. Conventional fertilizers benefit from established supply chains, standardized quality specifications, and widespread dealer networks that ensure product availability across all agricultural regions.

Specialty fertilizers represent the fastest-growing segment, with a 5.2% CAGR through 2031, driven by regulatory pressures and farmer demand for enhanced performance characteristics. Controlled-release fertilizers (CRF) are gaining market share in high-value crop production, where their ability to synchronize nutrient release with plant uptake patterns justifies premium pricing. Water-soluble fertilizers are experiencing robust growth in greenhouse and fertigation applications, where precise nutrient control and rapid plant response are critical success factors. Slow-release fertilizers (SRF) are finding applications in environmentally sensitive areas where nitrate leaching restrictions favor extended-release formulations. Liquid fertilizers are expanding beyond their traditional foliar application niche into soil injection and fertigation systems, offering improved mixing capabilities and reduced handling costs compared to dry products.

Complete Report Scope:

- Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Urea

- Others

- Phosphatic

- DAP

- MAP

- SSP

- TSP

- Potassic

- MoP

- SoP

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- Form

- Conventional

- Speciality

- CRF

- Liquid Fertilizer

- SRF

- Water Soluble

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

List of Companies Covered in this Report:

- AGLUKON Spezialduenger GmbH & Co. KG

- AGROFERT A.S. (AGROFERT Group)

- BASF SE

- Bayer AG

- CF Industries Holdings Inc.

- EuroChem Group AG

- Grupa Azoty S.A.

- Haifa Group

- ICL Group Ltd.

- Kingenta Ecological Engineering Group Co., Ltd. (Kingenta Group)

- K+S Aktiengesellschaft

- Mosaic Company

- Nutrien Ltd.

- PhosAgro PJSC

- Yara International ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-ag fertigation boom

- 4.6.2 Demand for enhanced-efficiency fertilizers

- 4.6.3 Greenhouse and hydroponic expansion

- 4.6.4 Rising crop prices and farm income

- 4.6.5 Federal Humus carbon-credit scheme

- 4.6.6 Green-ammonia import corridors

- 4.7 Market Restraints

- 4.7.1 Stricter nitrate application caps

- 4.7.2 Volatile gas and phosphate-rock costs

- 4.7.3 Protest-driven policy uncertainty

- 4.7.4 Protein-crop rotation cannibalizing N demand

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Urea

- 5.1.2.2.2 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AGLUKON Spezialduenger GmbH & Co. KG

- 6.4.2 AGROFERT A.S. (AGROFERT Group)

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 CF Industries Holdings Inc.

- 6.4.6 EuroChem Group AG

- 6.4.7 Grupa Azoty S.A.

- 6.4.8 Haifa Group

- 6.4.9 ICL Group Ltd.

- 6.4.10 Kingenta Ecological Engineering Group Co., Ltd. (Kingenta Group)

- 6.4.11 K+S Aktiengesellschaft

- 6.4.12 Mosaic Company

- 6.4.13 Nutrien Ltd.

- 6.4.14 PhosAgro PJSC

- 6.4.15 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)