|

市場調查報告書

商品編碼

2073618

中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)China Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

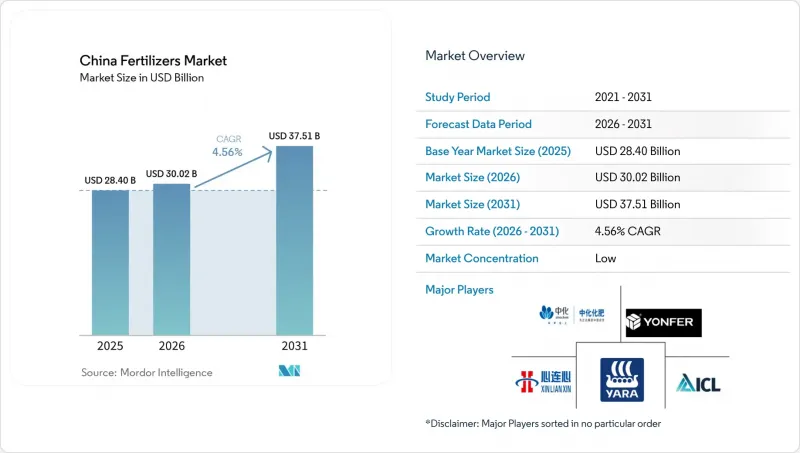

根據 Mordor Intelligence 預測,中國化肥市場規模將從 2025 年的 284 億美元成長到 2026 年的 300.2 億美元,然後在 2031 年達到 375.1 億美元,2026 年至 2031 年的複合年成長率為 4.56%。

本報告按類型(複合肥和單方肥)、形態(常規型和特種型)、施用方法(灌溉施肥、葉面噴布、土壤施用)和作物類型(田間作物、園藝作物、草坪和觀賞作物)進行分類。市場預測以價值(美元)和數量(公噸)表示。

中國化肥市場趨勢與洞察

政府對化肥使用的補貼計劃

基於農業農村部相關計劃,政府對均衡施肥和土壤改良的直接補貼正在加速中國各地農業區對養分的需求。農業機械購置補貼計畫已擴大範圍,將精準施肥設備納入其中,預計2024年,符合資格的農民的補貼率將達到30%。這些政策干預人為地提高了需求彈性,從而支撐了效率提升型產品的高價,同時也促進了特定養分類別產品的銷售量。此補貼機制尤其有利於緩釋肥和水溶肥,因為與傳統肥料相比,這些肥料的效率提升更為顯著。然而,各省的政策執行差異很大,主要糧食產區獲得的補貼比例更高,導致區域競爭出現扭曲。

提高作物產量和品質的長期壓力

中國國家農業戰略中蘊含的糧食安全義務,正持續推高各類作物的化肥施用量。國務院發布的《關於糧食多樣化供給體系的意見》強調,應最大限度地提高單位面積產量,以彌補有限耕地面積的擴張,這直接導致養分投入的增加。這個政策框架獨立於市場價格訊號運行,即使在農產品價格波動時期,也降低了化肥產品的需求彈性。在地方層面,政策實施的重點是縮小平均產量與潛在產量之間的差距,特別關注構成國家糧食安全目標基礎的穀類作物。在都市化導致耕地面積減少的地區,這種壓力更為顯著,要求剩餘耕地透過密集施肥來提高產量。

更嚴格的營養物質洩漏控制和檢查系統

新的土壤品質標準「GB 15618」對硝酸鹽淋溶和磷流失過量施以罰款,導致合規成本增加,從而限制了全部區域的化肥施用。生態環境部透過引入流域養分負荷即時監測系統,加強了監管力度,迫使農民降低施肥量,否則將面臨高額罰款。這些監管限制獨立於農藥最佳化之外,導致為了最大化產量而採用的施肥量超過了法定允許限值。雖然合規要求傾向於使用低用量即可提供同等營養價值的高效產品,但在過渡期內,由於農民需要調整施肥方法,市場正面臨混亂。

細分市場分析

複合肥料是最大的細分市場,預計到2025年將佔中國化肥市場佔有率的56.2%,並將維持最高的成長率,到2031年複合年成長率將達到6.0%。複合肥料市場受益於精密農業的發展趨勢,精準農業強調根據特定作物和土壤條件的需求客製化營養配比。 NPK複合肥在複合肥類別中佔據主導地位,這得益於成熟的農化規範,這些規範定義了主要作物類別的均衡營養配比。添加微量元素和次要大量元素的專用複合肥價格較高,因為它們可以解決透過土壤檢測發現的特定營養缺乏問題。

該領域之所以備受關注,主要原因在於其高效性,一次施用即可為農民提供多種營養元素。複合肥在中國城市綠化領域尤其重要,在養護觀賞樹木、優質草坪以及溫室花卉方面發揮關鍵作用。氮磷鉀複合肥(NPK)的日益普及(約佔中國肥料總消費量的一半)進一步推動了該領域的發展。造粒已成為主要的生產方式,反映了中國高度發展的肥料生產體系。

預計到2025年,傳統肥料產品將佔總銷售額的74.0%,這得益於其完善的生產基礎設施和成本優勢,尤其適合對價格敏感的農業市場。傳統肥料包括傳統的顆粒狀和晶體狀肥料,這些肥料透過成熟的施用方法和與設備的兼容性,能夠可靠地輸送養分。傳統肥料產品散裝運輸的優勢,有助於建立高效的分銷系統,服務於大規模農業生產,同時最大限度地降低物流複雜性。傳統肥料生產的規模經濟效益,使其成本結構在對價格敏感的細分市場中保持著相對於特種肥料的競爭優勢。

預計到2031年,特種肥料細分市場將以6.1%的複合年成長率快速成長,成為成長最快的領域。精密農業和現代灌溉技術的日益普及推動了該細分市場的快速成長。水溶性肥料約佔特種肥料細分市場的一半,因其卓越的養分輸送效率而備受關注。農民對緩釋肥料優勢及其在永續農業中的作用認知不斷提高,進一步促進了該細分市場的成長。中國政府對環境保護的重視以及提高肥料利用率的需求,正在推動特種肥料配方的創新。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:執行摘要和主要發現

第3章:本報告的內容

第4章:主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 微量營養素

- 主要營養素

- 田間作物

- 園藝作物

- 次要營養元素

- 田間作物

- 園藝作物

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 政府對化肥使用的補貼計劃

- 提高作物產量和品質的長期壓力

- 特種肥料消費量激增

- 擴大保護性耕作面積需要施肥和灌溉

- 能夠實現精準施肥的數位化農業平台的出現。

- 儘早引進低碳綠色氨生產線

- 市場限制因素

- 加強營養物質洩漏方面的法規和檢查制度。

- 主要糧食產區對主要營養素的需求已趨於穩定。

- 隨著土壤檢測服務的普及,農民們正逐漸摒棄統一的氮磷鉀肥施用方式。

- 碳定價試點實施正在增加高排放發電廠的生產成本。

第5章 市場規模與成長預測

- 類型

- 複雜類型

- 直的

- 微量營養素

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 氮基

- 尿素

- 其他

- 磷酸鹽基

- DAP

- MAP

- SSP

- TSP

- 鉀基

- MoP

- SoP

- 其他

- 次要大量營養元素

- 鈣

- 鎂

- 硫

- 微量營養素

- 形式

- 傳統的

- 專業領域

- CRF

- 液體肥料

- SRF

- 水溶性

- 使用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介。

- Sinofert Holdings Limited

- Xinyangfeng Agricultural Technology Co., Ltd.

- Henan XinlianXin Chemicals Group Company Limited

- Yara International ASA

- ICL Group Ltd

- Kingenta Ecological Engineering Group Co., Ltd.

- Compo Expert GmbH

- Haifa Chemicals Ltd.

- Nutrien Ltd.

- Yara International ASA

- Koch Agronomic Services, LLC

- SQM SA

- Shandong Hualu-Hengsheng Chemical Co., Ltd.

- Florikan ESA LLC

- National Fertilizers Limited

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the china fertilizer market size is projected to grow from USD 28.40 billion in 2025 to USD 30.02 billion in 2026 and is forecast to reach USD 37.51 billion by 2031 at 4.56% CAGR over 2026-2031.

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons)

China Fertilizers Market Trends and Insights

Government Fertilizer-Use Subsidy Schemes

Direct government subsidies for balanced fertilization and soil restoration under the Ministry of Agriculture and Rural Affairs programs are accelerating nutrient demand across China's agricultural regions. The agricultural machinery purchase subsidy program expanded to include precision fertilizer application equipment, with subsidy rates reaching 30% for eligible farmers in 2024. These policy interventions create artificial demand elasticity that supports premium pricing for efficiency-enhancing products while simultaneously driving volume growth in targeted nutrient categories. The subsidy framework particularly benefits controlled-release and water-soluble fertilizers that demonstrate measurable efficiency gains over conventional alternatives. Policy implementation varies significantly across provinces, with major grain-producing regions receiving proportionally higher subsidy allocations that distort regional competitive dynamics.

Chronic Pressure to Raise Crop Yields and Quality

Food security mandates embedded in China's national agricultural strategy create persistent upward pressure on fertilizer application intensity across all crop categories. The State Council's diversified food supply system opinion emphasizes yield maximization per hectare to offset limited arable land expansion, directly translating to increased nutrient input requirements. This policy framework operates independently of market pricing signals, creating inelastic demand for fertilizer products even during periods of agricultural commodity price volatility. Regional implementation focuses on closing yield gaps between average and potential productivity, with particular emphasis on grain crops that underpin national food security objectives. The pressure intensifies in regions where urbanization reduces agricultural land availability, forcing remaining farmland to achieve higher productivity levels through intensive fertilization practices.

Stricter Nutrient-Loss Regulations and Inspection Regimes

New GB 15618 soil quality standards impose penalties for excess nitrate leaching and phosphorus runoff, creating compliance costs that constrain fertilizer application rates across environmentally sensitive agricultural regions. The Ministry of Ecology and Environment has strengthened inspection protocols with real-time monitoring systems that track nutrient loading in watershed areas, forcing farmers to reduce application rates or face significant financial penalties . These regulatory constraints operate independently of agronomic optimization, creating situations where yield-maximizing fertilizer rates exceed legally permissible application levels. Compliance requirements favor efficiency-enhanced products that deliver equivalent nutritional value at lower application rates, but the transition period creates market disruption as farmers adjust application practices.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Specialty Fertilizer Consumption

- Expansion of Protected Cultivation Acreage Needing Fertigation

- Plateauing Macronutrient Demand in Major Grain Belts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Complex fertilizers are the largest segment, holding 56.2% of the China fertilizer market share in 2025, and are projected to register the fastest 6.0% CAGR through 2031. The complex segment benefits from precision agriculture trends that favor customized nutrient ratios matched to specific crop requirements and soil conditions. NPK compound fertilizers dominate the complex category, supported by established agronomic protocols that specify balanced nutrient ratios for major crop categories. Specialty complex formulations incorporating micronutrients and secondary macronutrients command premium pricing while addressing specific nutritional deficiencies identified through soil testing programs.

The segment's prominence is primarily attributed to its ability to provide multiple nutrients in a single application, making it highly efficient for farmers. Complex fertilizers are particularly crucial in China's urban greening sector, playing a vital role in maintaining decorative trees, high-quality grass, and nurturing flowers in greenhouses. The segment's strength is further reinforced by China's increasing reliance on NPK fertilizers, which typically account for about half of total fertilizer consumption. The granulation production method stands as the primary manufacturing approach, reflecting China's sophisticated fertilizer production landscape.

Conventional products accounted for 74.0% of revenue in 2025, supported by established manufacturing infrastructure and cost advantages that align with price-sensitive agricultural markets. The conventional segment encompasses traditional granular and crystalline formulations that deliver nutrients reliably through proven application methods and equipment compatibility. Bulk handling advantages in conventional products support efficient distribution systems that serve large-scale agricultural operations with minimal logistical complexity. Manufacturing scale economies in conventional fertilizer production create cost structures that maintain competitive advantages over specialty alternatives in price-sensitive market segments.

Specialty variants are forecast to expand at the fastest pace of 6.1% CAGR through 2031. This segment is experiencing rapid advancement due to the increasing adoption of precision agriculture and modern irrigation methods. Water-soluble fertilizers, which account for about half of the specialty segment, are gaining particular traction due to their superior nutrient-delivery efficiency. The segment's growth is further propelled by rising awareness among farmers about the benefits of controlled-release fertilizers and their role in sustainable agriculture. The Chinese government's emphasis on environmental protection and the need for improved fertilizer efficiency are driving innovation in specialty fertilizer formulations.

Complete Report Scope:

- Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Urea

- Others

- Phosphatic

- DAP

- MAP

- SSP

- TSP

- Potassic

- MoP

- SoP

- Others

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- Form

- Conventional

- Speciality

- CRF

- Liquid Fertilizer

- SRF

- Water Soluble

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

List of Companies Covered in this Report:

- Sinofert Holdings Limited

- Xinyangfeng Agricultural Technology Co., Ltd.

- Henan XinlianXin Chemicals Group Company Limited

- Yara International ASA

- ICL Group Ltd

- Kingenta Ecological Engineering Group Co., Ltd.

- Compo Expert GmbH

- Haifa Chemicals Ltd.

- Nutrien Ltd.

- Yara International ASA

- Koch Agronomic Services, LLC

- SQM S.A.

- Shandong Hualu-Hengsheng Chemical Co., Ltd.

- Florikan ESA LLC

- National Fertilizers Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 EXECUTIVE SUMMARY & KEY FINDINGS

3 REPORT OFFERS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Primary Nutrients

- 4.3.1 Field Crops

- 4.3.2 Horticultural Crops

- 4.4 Secondary Macronutrients

- 4.4.1 Field Crops

- 4.4.2 Horticultural Crops

- 4.5 Agricultural Land Equipped For Irrigation

- 4.6 Regulatory Framework

- 4.7 Value Chain & Distribution Channel Analysis

- 4.8 Market Drivers

- 4.8.1 Government fertilizer?use subsidy schemes

- 4.8.2 Chronic pressure to raise crop yields and quality

- 4.8.3 Surge in specialty fertilizer consumption

- 4.8.4 Expansion of protected cultivation acreage needing fertigation

- 4.8.5 Emergence of digital agriculture platforms enabling precision dosing

- 4.8.6 Early adoption of low-carbon green ammonia production lines

- 4.9 Market Restraints

- 4.9.1 Stricter nutrient-loss regulations and inspection regimes

- 4.9.2 Plateauing macronutrient demand in major grain belts

- 4.9.3 Soil-test service bundles shifting farmers away from blanket NPK

- 4.9.4 Carbon-pricing pilots boosting production costs for high-emission plants

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Urea

- 5.1.2.2.2 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Sinofert Holdings Limited

- 6.4.2 Xinyangfeng Agricultural Technology Co., Ltd.

- 6.4.3 Henan XinlianXin Chemicals Group Company Limited

- 6.4.4 Yara International ASA

- 6.4.5 ICL Group Ltd

- 6.4.6 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.7 Compo Expert GmbH

- 6.4.8 Haifa Chemicals Ltd.

- 6.4.9 Nutrien Ltd.

- 6.4.10 Yara International ASA

- 6.4.11 Koch Agronomic Services, LLC

- 6.4.12 SQM S.A.

- 6.4.13 Shandong Hualu-Hengsheng Chemical Co., Ltd.

- 6.4.14 Florikan ESA LLC

- 6.4.15 National Fertilizers Limited

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)