|

市場調查報告書

商品編碼

2072807

飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)Feed Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

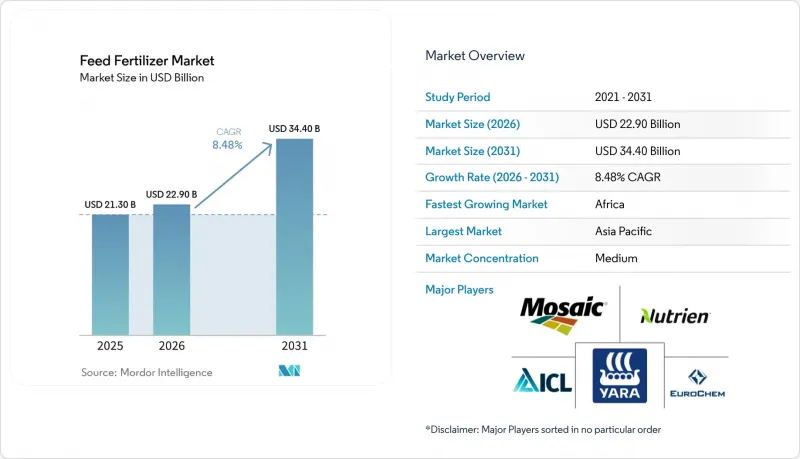

根據 Mordor Intelligence 預測,飼料飼料肥料的市場規模預計將從 2025 年的 213 億美元和 2026 年的 229 億美元成長到 2031 年的 344 億美元,2026 年至 2031 年的複合年成長率為 8.48%。

本報告按產品類型(氮肥、磷肥等)、形態(乾燥顆粒等)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元計價。

全球飼料肥料市場趨勢及洞察

政府關於永續畜牧業生產力的法規

2025年,歐盟通用農業政策引入了關於養分平衡管理的強制性法規,要求農場根據土壤閾值值限制記錄肥料使用情況。同樣,美國和加拿大也實施了將補貼資格與養分審計結果掛鉤的合規措施,從而促進了具有完全可追溯性的精準肥料產品的採用。這些法律規範正在推動農業領域的創新,例如雅苒國際於2025年推出的YaraPlus平台。該平台提供符合監管要求的即時建議,並創造了新的基於服務的商機。為了配合這些全球舉措,印度也在同年推出了發酵有機肥計劃,為小規模酪農提供50%的實施成本補貼。這些措施凸顯了全球向永續畜牧業實踐的轉變,推動了對精密農業和有機材料的需求成長,同時也符合環境和經濟目標。

新興經濟體對高蛋白飲食的需求日益成長

亞太地區飲食習慣的改變,特別是肉類、魚類和蛋類消費量的增加,正在推動複合飼料需求的成長,進而影響飼料和肥料市場。印尼、孟加拉和越南等國可支配所得的成長進一步加劇了這一趨勢,加速了集約化蝦類養殖的擴張,而集約化蝦類養殖需要精準施用氮磷肥。雖然家禽飼料仍佔主導地位,但在泰國等成熟的出口國,其成長已趨於穩定,投資者正將資金轉向魚蝦產業鏈。因此,不斷成長的蛋白質需求正推動市場轉向適用於閉合迴路系統的液態濃縮飼料,逐漸取代傳統的用於大面積養殖的顆粒飼料,從而適應這些新興經濟體不斷變化的需求。

主要原物料價格波動

磷酸鹽和硝酸鹽價格的波動正在擾亂採購計劃,並降低飼料和化肥供應商的營業利潤率。 Nutrien公司決定於2025年關閉其位於特立尼達的氮肥生產設施,並將氨產量削減70萬噸,這凸顯了持續的成本上漲正迫使企業縮減產能的現實。同時,中國於2025年實施的磷酸鹽出口配額限制措施收緊了全球供應,導致非洲和南美洲的價格飆升。缺乏垂直整合或長期合約的小規模生產商受到這些衝擊的嚴重影響,導致創新投資減少、畜牧養殖戶成本增加,並最終限制了市場成長。

細分市場分析

氮基飼料肥料佔最大的市場佔有率,預計到2025年將佔飼料肥料銷售額的42.5%。這反映了它們在蛋白質合成中的關鍵作用以及與全球氨網路的整合。雖然生物基飼料肥料的市場佔有率有限,但預計在2026年至2031年間的複合年成長率將達到12.7%,顯示市場對低碳投入品的需求不斷成長。磷基飼料肥料也佔據了相當大的市場佔有率,這主要得益於家禽和豬骨骼生長所需營養物質的需求。另一方面,鉀基肥料則主要用於反芻動物。因此,該領域的趨勢是氮基肥料將繼續保持其主導地位,而生物基產品則將成為高階細分市場。

繼Gromor Bio Organic上市後,Coromandel International在2025會計年度第三季實現了18%的特種營養品業務成長,充分展現了對印度酪農產業的強勁支持。 YaraBasa TURBO於2025年在巴西上市,該產品添加了尿素酶抑制劑,可減少30%的氨損失,這表明老牌企業正透過改進化學技術來維持其市場佔有率。由於中國對磷酸鹽的出口配額限制導致磷酸鹽供應緊張,價格差異不斷擴大,買家正轉向氮鉀混合肥料。預計2026年至2031年,氮基飼料肥料市場將維持強勁成長,產品組合成長將轉向包含排碳權收入的生物基創新產品。

區域分析

到2025年,亞太地區將以38.2%的市佔率引領全球市場。這主要得益於中國集約化叢集的蓬勃發展、印度酪農行業的擴張以及越南和印尼蝦類養殖業的強勁成長。中國磷酸鹽出口配額的收緊促使企業轉向氮肥和生物基混合肥料,從而提高了單位產品的附加價值。預計2026年至2031年,非洲的複合年成長率將達到9.4%,主要得益於政府為促進蛋白質自給自足和飼料基礎設施建設而採取的各項措施。儘管物流挑戰依然存在,但隨著行動支付和合作社樞紐的建立,分銷系統正在不斷改進。

在北美,支持畜禽糞便衍生肥料的碳權貨幣化正在推動市場穩步成長;而在南美,最佳化投入成本的垂直整合的家禽和生豬供應鏈也促進了市場成長。歐洲的成長仍然受到營養預算緊張的限制,但高效的高級產品正在緩解銷售量下滑的局面。在中東,市場正透過投資國內營養複合體以保障糧食安全而不斷擴張;而在俄羅斯,由於制裁限制了精密農業技術的獲取,重組畜牧業的努力正在放緩。

在永續性需求和蛋白質消費量不斷成長的推動下,全球需求持續攀升。亞太地區的規模可作為價格標桿,非洲的快速成長創造了新的銷售量機會,而源自北美和南美的創新正透過夥伴關係在全球傳播。這些相互關聯的區域趨勢,在協調一致的政策獎勵和數位化平台的支持下,有望縮小市場普及差距,並推動全球飼料和肥料市場的發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府關於永續畜牧業生產力的法規

- 新興國家對高蛋白飲食的需求日益成長

- 水產養殖業的擴張需要水溶性飼料肥料

- 擴大精密農業在畜牧業的應用

- 藻類生物肥料正在提高其轉化飼料的轉換率。

- 將畜禽糞便衍生肥料的排碳權貨幣化

- 市場限制因素

- 主要原物料價格波動

- 動物性產品殘留物標準嚴格

- 新型微生物肥料法規核准延遲

- 農場層級抵制數據共用以進行精密農業規劃

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 用於飼料的氮肥

- 磷酸鹽基飼料肥料

- 鉀基複合肥

- 生物基飼料肥料

- 按形式

- 乾顆粒

- 濃縮液

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Yara International ASA

- Nutrien Ltd.

- The Mosaic Company

- ICL Group Ltd.

- EuroChem Group AG

- OCP SA

- Koch Agronomic Services, LLC(Koch Industries Inc.)

- CF Industries Holdings, Inc.

- Wilbur-Ellis Nutrition, LLC(Wilbur-Ellis Holdings, Inc.)

- Coromandel International Ltd.(Murugappa Group)

- Haifa Negev Technologies Ltd.

- Innophos Holdings, Inc.(One Rock Capital Partners)

- Phosphea(Groupe Roullier)

- JR Simplot Company

- Grupa Azoty SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the feed fertilizer market size is projected to expand from USD 21.3 billion in 2025 and USD 22.9 billion in 2026 to USD 34.4 billion by 2031, registering a CAGR of 8.48% during 2026-2031.

This report is Segmented by Product Type (Nitrogen-Based, Phosphate-Based, and More), by Form (Dry Granules, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Feed Fertilizer Market Trends and Insights

Government Mandates on Sustainable Livestock Productivity

In 2025, the European Union Common Agricultural Policy introduced mandatory nutrient budgeting rules, requiring farms to document fertilizer usage in accordance with soil threshold limits. Similarly, in the United States and Canada, compliance measures tie subsidy eligibility to nutrient audits, encouraging the adoption of precision-dosed products with full traceability. These regulatory frameworks have driven innovation in the agricultural sector, as seen with Yara International's launch of the YaraPlus platform in 2025, which provides real-time recommendations aligned with regulatory requirements and creates new service-based revenue opportunities. Complementing these global efforts, India introduced a fermented organic manure program in the same year, subsidizing 50% of setup costs for smallholder dairy farmers. Together, these initiatives highlight a global shift towards sustainable livestock practices, fostering increased demand for precision agriculture and organic inputs while aligning with environmental and economic goals.

Growing Demand for High-Protein Diets in Emerging Economies

Dietary shifts in the Asia-Pacific region toward higher consumption of meat, fish, and eggs are driving growth in compound feed volumes, subsequently impacting the feed fertilizer market. This trend is further supported by rising disposable incomes in countries such as Indonesia, Bangladesh, and Vietnam, which are fueling the expansion of intensive shrimp farming operations requiring precise nitrogen and phosphate applications. While poultry remains dominant, its growth is stabilizing in mature exporting countries like Thailand, prompting investors to redirect capital toward fish and shrimp value chains. Consequently, the increasing demand for protein is steering the market toward liquid concentrates optimized for closed-loop systems, marking a shift away from traditional broad-acre granules and aligning with the evolving needs of these emerging economies.

Price Volatility of Key Raw Materials

Fluctuations in phosphate and nitrate prices disrupt procurement planning and reduce operating margins for feed fertilizer suppliers. Nutrien's 2025 closure of its Trinidad nitrogen facility, cutting 0.7 million metric tons of ammonia production, underscores how sustained cost inflation forces capacity reductions. Simultaneously, China's 2025 phosphate export quota tightened global supply, driving price surges in Africa and South America. Smaller producers, lacking vertical integration or long-term contracts, face the full impact of these shocks, leading to reduced innovation spending and higher costs for livestock farmers, ultimately constraining market growth.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Aquaculture Requiring Water-Soluble Feed Fertilizers

- Rising Adoption of Precision Farming in Animal Husbandry

- Stringent Residue Limits in Animal-Source Foods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nitrogen-based feed fertilizers held the largest share, accounting for 42.5% of 2025 revenue in the feed fertilizer market, reflecting their critical role in protein synthesis and their linkage to global ammonia networks. Bio-based feed fertilizers held only a limited share yet posted the fastest 12.7% CAGR through 2026-2031, suggesting a rising appetite for carbon-friendly inputs. Phosphate-based feed fertilizers captured a prominent share of the market, driven by skeletal growth requirements in poultry and swine, while potash served ruminants. The segment narrative, therefore, revolves around nitrogen defending its dominant position while bio-based lines become premium niches.

Coromandel International recorded 18% specialty-nutrient growth in Q3 FY 2025 after the launch of Gromor Bio Organic, indicating tangible traction among Indian dairies. YaraBasa TURBO, launched in Brazil in 2025, integrates urease inhibitors that reduce ammonia loss by 30%, illustrating how incumbents defend their share via upgraded chemistries. China's export quotas pressure phosphate availability, widening price differentials, and nudging buyers toward nitrogen-potash blends. Over 2026-2031, the feed fertilizer market for nitrogen remains sturdy, but portfolio growth will tilt toward bio-based innovations that bundle carbon credit revenue.

Complete Report Scope:

- By Product Type

- Nitrogen-Based Feed Fertilizers

- Phosphate-Based Feed Fertilizers

- Potash-Based Feed Fertilizers

- Bio-Based Feed Fertilizers

- By Form

- Dry Granules

- Liquid Concentrates

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

In 2025, Asia-Pacific led the market with a 38.2% share, driven by concentrated poultry clusters in China, expanding dairy operations in India, and robust shrimp farming in Vietnam and Indonesia. Tightened phosphate-export quotas in China prompted diversification into nitrogen and bio-based blends, enhancing per-unit value. Africa is projected to grow at a 9.4% CAGR during 2026-2031, is advancing through government initiatives promoting protein self-sufficiency and feed infrastructure upgrades, with mobile payments and cooperative hubs improving distribution despite logistical challenges.

North America's steady growth is fueled by carbon-credit monetization supporting manure-derived fertilizers, while South America benefits from vertically integrated poultry and swine chains that optimize input costs. Europe's growth remains constrained by strict nutrient budgets, though premium enhanced-efficiency products mitigate tonnage declines. The Middle East is expanding through investments in domestic nutrient complexes for food security, while Russia's herd rebuilding efforts are tempered by limited access to precision-farming technologies due to sanctions.

Global demand is rising as sustainability mandates and protein consumption increase. Asia-Pacific's scale sets pricing benchmarks, Africa's rapid growth adds new volume opportunities, and innovation from North and South America spreads globally through partnerships. These interconnected regional dynamics, supported by synchronized policy incentives and digital platforms, are anticipated to narrow adoption gaps and drive the global feed fertilizer market forward.

- Yara International ASA

- Nutrien Ltd.

- The Mosaic Company

- ICL Group Ltd.

- EuroChem Group AG

- OCP S.A.

- Koch Agronomic Services, LLC (Koch Industries Inc.)

- CF Industries Holdings, Inc.

- Wilbur-Ellis Nutrition, LLC (Wilbur-Ellis Holdings, Inc.)

- Coromandel International Ltd. (Murugappa Group)

- Haifa Negev Technologies Ltd.

- Innophos Holdings, Inc. (One Rock Capital Partners)

- Phosphea (Groupe Roullier)

- J. R. Simplot Company

- Grupa Azoty S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government mandates on sustainable livestock productivity

- 4.2.2 Growing demand for high-protein diets in emerging economies

- 4.2.3 Expansion of aquaculture requiring water-soluble feed fertilizers

- 4.2.4 Rising adoption of precision farming in animal husbandry

- 4.2.5 Algae-based biofertilizers are improving feed conversion ratios

- 4.2.6 Carbon-credit monetization of manure-derived fertilizers

- 4.3 Market Restraints

- 4.3.1 Price volatility of key raw materials

- 4.3.2 Stringent residue limits in animal-source foods

- 4.3.3 Slow regulatory approvals for novel microbial fertilizers

- 4.3.4 Farm-level resistance to data-sharing for precision plans

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Nitrogen-Based Feed Fertilizers

- 5.1.2 Phosphate-Based Feed Fertilizers

- 5.1.3 Potash-Based Feed Fertilizers

- 5.1.4 Bio-Based Feed Fertilizers

- 5.2 By Form

- 5.2.1 Dry Granules

- 5.2.2 Liquid Concentrates

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Russia

- 5.3.3.4 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 Nutrien Ltd.

- 6.4.3 The Mosaic Company

- 6.4.4 ICL Group Ltd.

- 6.4.5 EuroChem Group AG

- 6.4.6 OCP S.A.

- 6.4.7 Koch Agronomic Services, LLC (Koch Industries Inc.)

- 6.4.8 CF Industries Holdings, Inc.

- 6.4.9 Wilbur-Ellis Nutrition, LLC (Wilbur-Ellis Holdings, Inc.)

- 6.4.10 Coromandel International Ltd. (Murugappa Group)

- 6.4.11 Haifa Negev Technologies Ltd.

- 6.4.12 Innophos Holdings, Inc. (One Rock Capital Partners)

- 6.4.13 Phosphea (Groupe Roullier)

- 6.4.14 J. R. Simplot Company

- 6.4.15 Grupa Azoty S.A.

7 Market Opportunities and Future Outlook

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)