|

市場調查報告書

商品編碼

2073612

亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Controlled-Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

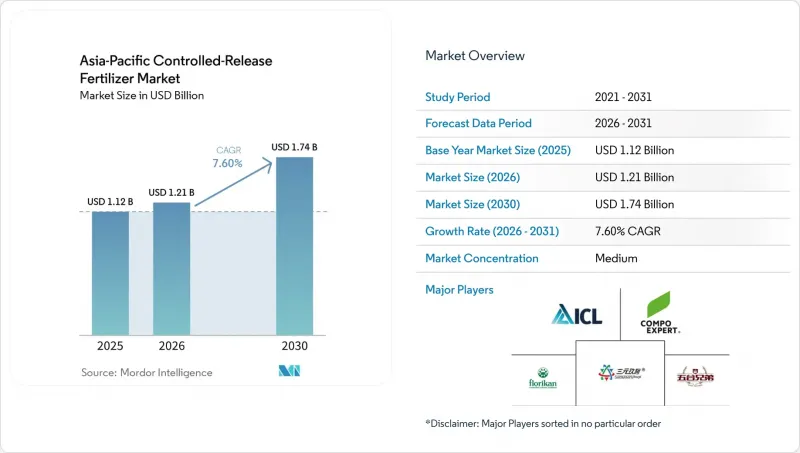

據 Mordor Intelligence 稱,亞太地區緩釋肥料市場預計到 2025 年將達到 11.2 億美元,到 2026 年將達到 12.1 億美元,預計到 2031 年將擴大到 17.4 億美元,2026 年至 2031 年的複合成長率為 7.60%。

本報告按塗料類型(聚合物塗料、聚合物硫塗料及其他)、作物類型(田間作物、園藝作物和草坪/觀賞作物)以及國家/地區(澳洲、孟加拉、中國、印度、印尼、日本、巴基斯坦、菲律賓、泰國、越南及其他亞太地區)進行細分。市場預測以價值(美元)和數量(公噸)呈現。

亞太地區緩釋肥料市場趨勢與洞察

政府加大對環保肥料的補貼力道。

有針對性的財政支持正在重塑亞太地區化肥的經濟效益。印度的營養補貼計畫現已涵蓋緩釋肥,使農民的轉換成本降低了高達40%,並顯著推動了北方邦、旁遮普邦和泰米爾納德邦的銷售量成長。在中國,對生態高效化肥的直接投入補貼和增值稅減免相結合,使生產商在價格和流動性方面都受益匪淺。印尼和越南的農業銀行也推出了專門用於購買緩釋肥的優惠貸款項目,體現了公共部門的持續投入。因此,生產商正在擴大靠近需求中心的生產能力,以滿足補貼訂單的需求,而經銷商在加強農業指導服務,以滿足農村地區日益成長的需求。

保護性耕作面積快速擴大

在都市化和全年生產高價值作物需求的推動下,保護性栽培系統正在全部區域迅速擴張。預計從2024年起,澳洲溫室產業將以每年15%的速度成長。環境可控農業需要精準的養分管理,更傾向於使用緩效肥料而非傳統肥料。這種成長在水耕和氣氣耕系統中尤其顯著,這些系統透過營養液管理實現自動施肥和循環利用,從而將肥料總消耗量減少高達60%。泰國針對水耕蔬菜生產的GAP 9001-2021標準要求定期進行水質監測和化學殘留檢測,這使得監管部門對能夠減少養分淋溶和環境污染的緩釋技術提出了更高的要求。保護性栽培的擴張推動了對用於無土栽培基質的專用緩釋配方的需求,因為傳統的顆粒肥料無法實現精準施肥。消費者願意為溫室種植的農產品支付更高的價格,凸顯了先進養分管理系統的經濟可行性。

與傳統NPK肥料相比,初始成本較高

在亞太地區的大多數市場,緩釋肥料的價格仍然比普通尿素高出1.8倍,這對種植稻米和小麥的面積小規模農戶來說構成了更大的障礙。雖然補貼在一定程度上抵消了這一差價,但前期投入成本仍然很高,許多生產者都在等待附近田地的示範項目確認其季節性收益後再採用緩釋肥料。在中國,精準施肥所需的設備,例如滴灌和噴灌系統,成本可能超過每英畝1400美元(相當於每公頃93.30美元)。農業融資管道有限以及規避風險的耕作方式進一步限制了小規模農戶採用緩釋肥料,因為他們無力承擔高昂的初始投資,儘管緩釋肥料具有潛在的長期收益。

細分市場分析

到2025年,聚合物包膜產品將在亞太緩釋肥料市場佔據71.2%的最大市場。這反映了該技術的成熟及其在不同農業系統中的有效性。中國和日本等國家強大的生產能力,以及其在養分利用效率和養分控釋方面的顯著優勢,正在推動此類產品的普及應用。包膜配方的不斷改進提升了產品在各種氣候條件下的性能,進一步鞏固了其在該領域的主導地位。

預計到2031年,聚合物包膜和硫包膜產品將成為成長最快的包膜類型,年複合成長率(CAGR)將達到8.9%。這一成長主要得益於市場對經濟高效、緩釋解決方案的需求不斷成長,以及包膜技術的進步提高了養分輸送的穩定性。同時,聚合物包膜性肥料因其能夠提高作物產量、減少養分流失並有助於該地區主要作物的精準養分管理,仍具有吸引力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 大田作物

- 園藝作物

- 平均施肥量

- 主要營養素

- 田間作物

- 園藝作物

- 主要營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 政府加大對環保肥料的補貼力道。

- 保護性耕作面積快速擴大

- 高價值作物精準施肥轉型

- 引入含酶塗層可減少釋放量的波動。

- 島國引入強制性營養物徑流上限

- 利用棕櫚仁油製成的生物基聚氨酯塗料的出現。

- 市場限制因素

- 與傳統NPK肥料相比,初始成本較高,且成本較高。

- 大城市以外地區的零售商教育程度不足。

- 特種塗料用聚合物的供應風險

- 區域性禁止使用微塑膠塗層顆粒

第5章 市場規模與成長預測

- 按塗層類型

- 聚合物塗層

- 聚合物硫塗層

- 其他

- 按作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 國家

- 澳洲

- 孟加拉

- 中國

- 印度

- 印尼

- 日本

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太國家

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介。

- ICL Group Ltd

- Grupa Azoty SA(Compo Expert)

- New Mountain Capital(Florikan)

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Kingenta Ecological Engineering Group Co., Ltd.

- Compo Expert GmbH

- Haifa Chemicals Ltd.

- Nutrien Ltd.

- Yara International ASA

- Koch Agronomic Services, LLC

- SQM SA

- Shandong Hualu-Hengsheng Chemical Co., Ltd.

- Hubei Xinyangfeng Fertilizer Co., Ltd.

- Shandong Luxi Fertilizer Co., Ltd.

- Florikan-ESA, LLC.

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the asia-Pacific controlled-release fertilizer market size reached USD 1.12 billion in 2025, is estimated to reach USD 1.21 billion in 2026, and is projected to rise to USD 1.74 billion by 2031, expanding at a 7.60% CAGR during 2026 to 2031.

This report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, and Others), by Crop Type (Field Crops, Horticultural Crops, and Turf & Ornamental), and by Country (Australia, Bangladesh, China, India, Indonesia, Japan, Pakistan, Philippines, Thailand, Vietnam, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Asia-Pacific Controlled-Release Fertilizer Market Trends and Insights

Surge in Government Subsidies for Eco-Efficient Fertilizers

Targeted fiscal support is reshaping fertilizer economics across much of the Asia-Pacific. India's nutrient-based subsidy scheme now covers controlled-release formulations, lowering farmer switching costs by up to 40% and driving significant sales volume in Uttar Pradesh, Punjab, and Tamil Nadu. China deploys a mix of direct input subsidies and reduced value-added tax on eco-efficient fertilizers, providing twin price and liquidity advantages for growers. Agricultural banks in Indonesia and Vietnam are adding preferential credit lines that specifically earmark funds for controlled-release purchases, signaling sustained public-sector commitment. As a result, manufacturers are expanding capacity closer to demand centers to satisfy subsidy-driven orders, while distributors intensify extension services to capture emerging rural demand.

Rapid Expansion of Protected Cultivation Acreage

Protected cultivation systems are growing rapidly across the Asia-Pacific region, driven by urbanization and the demand for year-round high-value crop production. Australia's greenhouse sector has grown by 15% annually since 2024, with controlled environment agriculture requiring precise nutrient management that favors controlled-release fertilizers over conventional types. The growth is significant in hydroponic and aeroponic systems, where nutrient solution management reduces total fertilizer consumption by up to 60% through automated dosing and recycling systems. Thailand's GAP 9001-2021 standards for hydroponic vegetable production require regular water quality monitoring and chemical residue testing, creating a regulatory need for controlled-release technologies that reduce leaching and environmental contamination . This expansion of protected cultivation increases the demand for specialized controlled-release formulations for soilless media, as traditional granular fertilizers cannot provide precise nutrient timing. Consumers' willingness to pay higher prices for greenhouse-grown produce supports the economic viability of advanced nutrient management systems.

High Upfront Cost Versus Conventional NPK

Controlled-release fertilizers still carry a 1.8 times price premium over standard urea in most Asia-Pacific markets, a hurdle magnified for smallholders who dominate rice and wheat acreage. While subsidies offset part of the gap, out-of-pocket expenses remain high, and many growers defer adoption until clear seasonal paybacks are validated through neighbor demonstration plots. In China, the cost of equipment, such as drip or sprinkler systems essential for precise application, can surpass USD 1,400 per mu (equivalent to USD 93.3 per ha). Limited access to agricultural credit and risk-averse farming practices further constrain adoption among smallholders who cannot afford the higher initial investment despite potential long-term benefits.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Precision-Fertigation in High-Value Crops

- Introduction of Enzyme-Embedded Coatings Lowers Release Variability

- Limited Retailer Education Outside Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer-coated products held the largest Asia-Pacific controlled-release fertilizer market share at 71.2% in 2025, reflecting the technology's maturity and effectiveness across diverse agricultural systems. Their widespread adoption is driven by robust manufacturing capabilities in countries like China and Japan, coupled with demonstrated benefits in nutrient-use efficiency and controlled nutrient release. Ongoing advancements in coating formulations continue to enhance performance under diverse climatic conditions, further solidifying the segment's leading position.

Polymer sulfur-coated products are anticipated to be the fastest-growing coating type, with a projected CAGR of 8.9% through 2031. This growth is attributed to rising demand for cost-effective controlled-release solutions and advancements in coating technologies that improve nutrient delivery consistency. Concurrently, polymer-coated fertilizers maintain their appeal due to their ability to enhance crop productivity, minimize nutrient losses, and facilitate precision nutrient management across key crops in the region.

Complete Report Scope:

- Coating Type

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

- Country

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- ICL Group Ltd

- Grupa Azoty S.A. (Compo Expert)

- New Mountain Capital (Florikan)

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Kingenta Ecological Engineering Group Co., Ltd.

- Compo Expert GmbH

- Haifa Chemicals Ltd.

- Nutrien Ltd.

- Yara International ASA

- Koch Agronomic Services, LLC

- SQM S.A.

- Shandong Hualu-Hengsheng Chemical Co., Ltd.

- Hubei Xinyangfeng Fertilizer Co., Ltd.

- Shandong Luxi Fertilizer Co., Ltd.

- Florikan-E.S.A., LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Surge in government subsidies for eco-efficient fertilizers

- 4.6.2 Rapid expansion of protected cultivation acreage

- 4.6.3 Shift toward precision-fertigation in high-value crops

- 4.6.4 Introduction of enzyme-embedded coatings lowers release variability

- 4.6.5 Mandatory nutrient-runoff caps adopted by island economies

- 4.6.6 Emergence of bio-based polyurethane coatings from palm-kernel oil

- 4.7 Market Restraints

- 4.7.1 High upfront cost versus conventional NPK

- 4.7.2 Limited retailer education outside Tier-1 cities

- 4.7.3 Supply risk of specialty coating polymers

- 4.7.4 Regional bans on micro-plastic coated granules

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 Bangladesh

- 5.3.3 China

- 5.3.4 India

- 5.3.5 Indonesia

- 5.3.6 Japan

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 ICL Group Ltd

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 New Mountain Capital (Florikan)

- 6.4.4 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Compo Expert GmbH

- 6.4.7 Haifa Chemicals Ltd.

- 6.4.8 Nutrien Ltd.

- 6.4.9 Yara International ASA

- 6.4.10 Koch Agronomic Services, LLC

- 6.4.11 SQM S.A.

- 6.4.12 Shandong Hualu-Hengsheng Chemical Co., Ltd.

- 6.4.13 Hubei Xinyangfeng Fertilizer Co., Ltd.

- 6.4.14 Shandong Luxi Fertilizer Co., Ltd.

- 6.4.15 Florikan-E.S.A., LLC.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)