|

市場調查報告書

商品編碼

2073604

化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

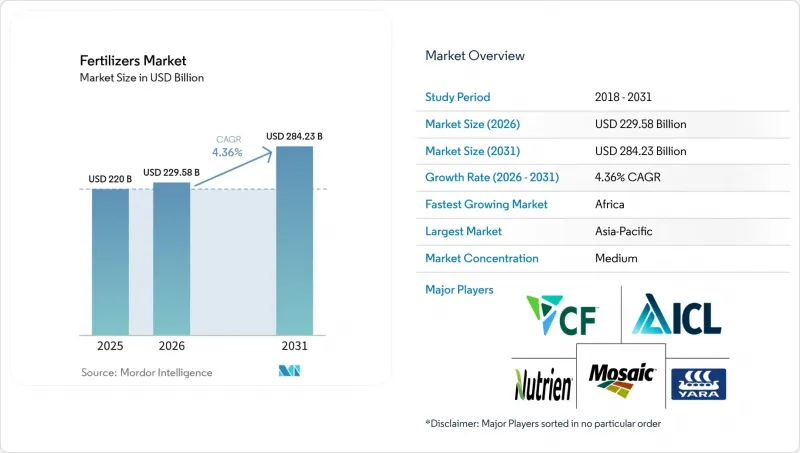

根據 Mordor Intelligence 預測,化肥市場規模將從 2025 年的 2,200 億美元和 2026 年的 2,295.8 億美元成長到 2031 年的 2,842.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.36%。

本報告按類型(複合肥和單質肥)、形態(常規型和特種型)、施用方法(灌溉施肥、葉面噴布、土壤施用)、作物類型(田間作物、園藝作物、草坪和觀賞作物)以及地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以價值(美元)和數量(公噸)表示。

全球化肥市場趨勢及洞察

精密農業計畫導致化肥需求激增

精密農業整合了全球導航衛星系統 (GNSS)、土壤感測器和機器學習演算法,能夠根據作物的實際需求,精準施用。這種定向施肥方式已在美國的玉米試驗種植中降低了每蒲式耳氮肥的用量,從而節省了成本並減少了氧化亞氮 (N₂O)的排放。在農場整合不斷推進、通訊基礎設施完善且配備變數控制器的大型農業機械推廣應用的地區,這項技術的應用正在加速。隨著設備製造商將農業軟體整合到噴霧器和肥料中,種植者對緩釋肥和液態肥的需求日益成長,這些肥料能夠根據田間具體處方箋進行客製化。這種需求驅動效應正穩步提升北美和西歐對特種營養素的需求,類似的趨勢也開始在中國和巴西出現。投資可在兩個種植季內收回的證明,增強了即使是小規模種植者也進行投資的合理性,從而擴大了微區客製化數位農藝和營養組合的潛在市場。

向氣候敏感型營養管理政策轉型

由於化肥生產和農地排放都是農業溫室氣體排放的重要來源,世界各國政府正將養分管理納入其應對氣候變遷的承諾中。歐盟的「從農場到餐桌」策略旨在2030年將化肥使用量減少20%,而印度則在其「國家永續農業使命」下推廣平衡施肥。這些法規推動了對硝化抑制劑、尿素酶抑制劑和聚合物包膜尿素的需求,這些產品能夠減緩養分釋放並減少揮發。中國的相關規定要求在購買化學肥料前進行土壤檢測,加速了從均質施肥到精準施肥的轉變。能夠提供高效產品的生產商正在獲得定價權,而大規模生產的通用型化肥在監管區域則面臨價格下行壓力。從長遠來看,統一的碳計量可以根據排放進一步區分供應商,從而增強低碳氮肥生產路線的戰略價值。

有機農業面積擴大

隨著有機耕作面積的擴大,合成氮肥的需求顯著下降,而對有機肥料、生物肥料和堆肥的需求則增加。隨著消費者對有機產品的偏好日益成長,經認證的農地面積也不斷擴大,這些農地禁止使用合成肥料。歐盟的《有機農業行動計畫(2021-2030)》是「從農場到餐桌」策略的關鍵組成部分,旨在2030年實現至少25%的農地採用有機耕作的目標。目前,已有188個國家進行有機農業,截至2024年,超過9,600萬公頃的農地由至少450萬農民進行有機管理。每增加一公頃有機耕作面積,化學肥料的潛在市場規模就會縮小,這構成了一種結構性阻力,僅靠技術手段無法克服。雖然有機農場的每公頃產量往往較低,但其溢價支持了耕地面積的增加,並抑制了高所得地區的長期需求。

細分市場分析

按類型分類,單養分肥料仍是最大的細分市場,預計到2025年將佔全球肥料市場佔有率的63.0%。此主導地位源自於作物生產系統對氮、磷、鉀三種養分單獨施用的持續依賴。在這一細分市場中,氮肥的銷售量最大,尿素、無水氨和硝酸銨等產品在全部區域的需求強勁。根據國際肥料協會(IFA)預測,2024年全球尿素產量將達2.01億噸,比2023年成長3%。在中國,隨著新增產能的運作,預計2026年尿素產量將達7,650萬噸。儘管採購成本不斷上漲,磷酸二銨、磷酸一銨、磷酸一磷和磷酸三磷等磷肥在作物生長中仍扮演著至關重要的角色。以氯化鉀為代表的鉀肥需求持續穩定,這得益於產能的不斷擴大。此外,該領域還包括次要營養元素和微量元素,其中鋅在微量元素中佔比最大,而硼在集約化種植系統中應用日益廣泛。

複合肥料預計將成為成長最快的肥料類型,其複合年成長率預計將超過整體市場成長率,2026年至2031年的複合年成長率將達到5.8%。這類肥料透過將多種營養元素結合在單一配方中,促進作物養分平衡,同時簡化施用流程並減少所需勞動力。複合肥料的應用正在不斷擴大,尤其是在園藝、人工林和其他高價值作物系統中,因為在這些地區,養分利用效率對產量至關重要。在歐洲,為了實現減少養分浪費的目標和永續性目標,人們正在推廣使用高濃度複合肥,以提高養分利用效率並降低施用量。此外,精密農業技術、可變施肥系統和土壤特異性養分管理方法的日益普及也推動了對平衡肥料產品的需求。隨著種植者致力於最大限度地提高產量和肥料利用率,複合肥料正逐漸成為單一養分肥料的首選替代品,並有望在整個預測期內保持穩定成長。

傳統肥料仍是最大的肥料形式,預計到2025年將佔肥料市場規模的88.5%。然而,在監管嚴格的地區,生產商正逐步轉向更有效率的肥料形式,以在不犧牲產量的前提下實現環境目標。這些產品通常是未包衣的顆粒或微粒肥料,使用撒播機施用或在犁地時混入土壤。養分有效性取決於土壤濕度、溫度和微生物活性等因素。由於其生產成本低且與現有農業機械相容性高,傳統肥料在對價格敏感的市場(例如穀物、油籽和甘蔗)中仍然被廣泛使用。另一方面,由於施用量的監管限制以及對養分徑流的環境擔憂,傳統肥料正面臨日益嚴峻的挑戰。因此,即使在對成本敏感的領域,也正在逐步轉向更有效率的替代肥料。

預計2026年至2031年間,特種肥料的複合年成長率將達6.3%。這一成長主要得益於緩效、緩效、液態和水溶性配方肥料的廣泛應用,這些肥料能夠提高養分利用效率並減少人工投入。聚合物或硫包膜的緩釋肥料可根據土壤溫度和濕度釋放養分,使養分供應與作物需求相匹配,與傳統肥料相比,可減少20%至40%的養分淋失。含有脲醛和異丁烯二脲等化學物質的緩效肥料能夠長期釋放養分,且經濟高效,因此適用於草坪和觀賞植物。液態肥料在北美和歐洲市場呈現顯著成長,並已被整合到大型農場的現有噴灑系統中,用於葉面噴布和啟動施肥,以確保養分均勻分佈並被植物快速吸收。

區域分析

亞太地區是最大的區域市場,預計到2025年將佔化肥市場佔有率的52.3%,其中中國和印度將引領市場。中國國內尿素產能將在2024年超過8,045萬噸,確保穩定的供應。然而,老舊的燃煤電廠可能面臨更嚴格的排放法規,甚至可能導致停產;而配備碳捕集技術的沿海燃氣電廠則可能帶來商機。根據印度農業部報告顯示,2023-2024年度印度化肥年消費總量約6,010萬噸,其中5,030萬噸為國內生產,1,770萬噸為進口。在東南亞,棕櫚油、稻米和橡膠人工林是推動化學肥料需求的主要因素。此外,印尼煉油廠正在稻田進行大規模緩釋肥混合試驗,以滿足永續性認證的要求。

預計到2031年,非洲將呈現最高的成長率,年複合成長率將達到6.2%。撒哈拉以南非洲的化肥需求受農業現代化、人口成長以及各國政府為實現糧食自給自足所做的努力的影響。該地區的化肥施用量遠低於全球平均水平,這意味著如果基礎設施改善和價格挑戰得到解決,該地區化肥需求仍有巨大的成長空間。作為該地區最大的經濟體,奈及利亞和南非正致力於提高國內化肥生產能力,以減少對進口的依賴並穩定價格。此外,衣索比亞、肯亞和坦尚尼亞正在進口散裝尿素和磷酸二銨(DAP),並擴大其混合設施,以生產符合當地作物(如咖啡、茶葉和玉米)需求的、具有特定氮磷鉀比例的化肥。在中東,沙烏地阿拉伯、阿拉伯聯合大公國和土耳其等國正透過將國內生產能力與進口相結合來滿足化肥需求,因為乾旱的氣候和有限的耕地限制了農業成長。由於其戰略位置,土耳其已成為橫跨歐洲、亞洲和非洲的化肥貿易物流樞紐。

在歐洲,面對嚴格的營養法規和飆升的能源成本,傳統化肥的出貨量正在減少,而特種化肥的利潤率卻在增加。東歐市場,特別是烏克蘭和俄羅斯,仍然是尿素、硝酸銨和鉀肥的主要出口國。然而,地緣政治不穩定和出口限制擾亂了貿易流動,導致部分出口轉向亞洲和非洲。在英國,脫歐後的農業政策將重點轉向環境友善土地管理,補貼也從生產支持轉向生態系統服務。這種轉變進一步抑制了對傳統化學肥料的需求,同時也為有機肥料和生物促效劑產品創造了新的機會。法國和西班牙的農作物種植者正在投資精準噴霧器,以在不降低糧食產量的情況下滿足氮肥限量要求,這推動了對含抑制劑包膜產品的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 主要營養素

- 田間作物

- 園藝作物

- 次要營養元素

- 田間作物

- 園藝作物

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 精密農業計畫導致化肥需求激增

- 向注重氣候的養分管理政策轉型

- 特殊配方和緩釋配方的快速普及

- 擴大低成本天然氣生產的產能

- 綠色氨生產的排碳權獎勵

- 人工智慧驅動的可變速率擴散平台

- 市場限制因素

- 原物料價格波動

- 歐洲對氮肥使用的限制

- 擴大有機農業用地面積

- 乾旱地區施肥和灌溉用水短缺

第5章 市場規模與成長預測

- 按類型

- 複雜類型

- 直的

- 微量營養素

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 氮基

- 硝酸銨

- 無水氨

- 尿素

- 其他

- 磷酸鹽基

- 磷酸二銨(DAP)

- 磷酸一銨(MAP)

- 瞬態過磷酸鈣(SSP)

- 三重過磷酸鈣(TSP)

- 其他

- 鉀基

- 氯化鉀(MoP)

- 硫酸鉀(SoP)

- 其他

- 次要營養元素

- 鈣

- 鎂

- 硫

- 微量營養素

- 按形式

- 傳統的

- 特種

- 控釋肥料(CRF)

- 液體肥料

- 緩效性肥料(SRF)

- 水溶性

- 透過應用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 按作物類型

- 大田作物

- 園藝作物

- 草坪和觀賞植物

- 按地區

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 其他北美國家

- 歐洲

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 其他歐洲國家

- 亞太地區

- 澳洲

- 孟加拉

- 中國

- 印度

- 印尼

- 日本

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太國家

- 南美洲

- 阿根廷

- 巴西

- 其他南美國家

- 中東

- 土耳其

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 奈及利亞

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nutrien Ltd.

- Uralkali PJSC(Uralchem Group)

- The Mosaic Company

- K+S Aktiengesellschaft

- ICL Group Ltd.

- EuroChem Group AG

- CF Industries Holdings, Inc.

- OCP SA

- PhosAgro PJSC

- Coromandel International Limited

- Indian Farmers Fertiliser Cooperative Limited(IFFCO)

- Haifa Chemicals Ltd.

- Yara International ASA

- Koch Fertilizer, LLC

- Grupa Azoty SA(Compo Expert)

- BHP Group Limited

- Qinghai Salt Lake Industry Co., Ltd.

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the fertilizers market size is projected to expand from USD 220.00 billion in 2025 and USD 229.58 billion in 2026 to USD 284.23 billion by 2031, registering a CAGR of 4.36% between 2026 and 2031.

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Fertilizers Market Trends and Insights

Surge in Fertilizer Demand from Precision-Agriculture Projects

Precision agriculture integrates global navigation satellite systems, soil sensors, and machine-learning algorithms to apply nutrients only where and when crops need them. This targeted approach reduces nitrogen use per bushel in United States corn trials, saving money and cutting nitrous oxide emissions. Adoption accelerates where farm consolidation and reliable connectivity support large machinery fleets fitted with variable-rate controllers. As equipment manufacturers embed agronomic software in sprayers and spreaders, growers seek controlled-release and liquid fertilizers that match site-specific prescriptions. The resulting pull effect spurs a steady rise in specialty nutrient demand across North America and Western Europe, with early signs of replication in China and Brazil. Evidence of payback within two seasons strengthens the investment case for smaller producers, widening the total addressable market for digital agronomy and nutrient combinations tailored to micro-zones.

Transition to Climate-Smart Nutrient-Management Policies

Governments embed nutrient stewardship in climate commitments because both fertilizer production and field emissions contribute significantly to agricultural greenhouse gas emissions. The European Union Farm to Fork Strategy targets a 20% cut in fertilizer use by 2030, while India promotes balanced fertilization under the National Mission for Sustainable Agriculture. Such mandates elevate demand for nitrification inhibitors, urease inhibitors, and polymer-coated urea that slow nutrient release and curb volatilization. China's guidelines require soil testing before fertilizer purchase, accelerating the shift from blanket doses to precision prescriptions. Producers capable of supplying enhanced-efficiency products gain pricing power, whereas commodity-grade volume faces downward pressure in regulated regions. Over the long term, harmonized carbon accounting may further differentiate suppliers on embedded emissions, reinforcing the strategic value of low-carbon nitrogen routes.

Growing Organic Farming Acreage

The expansion of organic farming acreage is substantially decreasing the demand for synthetic nitrogen-based fertilizers while increasing the demand for organic fertilizers, biofertilizers, and compost. As consumer preference for organic produce rises, certified farmland grows and prohibits synthetic nutrient inputs. The European Union Organic Action Plan (2021-2030) serves as a fundamental component of the Farm to Fork Strategy, aiming to achieve a target of at least 25% of agricultural land under organic farming by 2030. Organic agriculture is practiced in 188 countries, with over 96 million hectares of agricultural land managed organically by at least 4.5 million farmers as of 2024. Each converted hectare removes volume from the addressable market for chemical fertilizers, constituting a structural headwind that technology cannot offset. Although organic farms often yield less per hectare, their premium pricing sustains the acreage trend and dampens long-term demand in high-income regions.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Specialty and Slow-Release Formulations

- Artificial Intelligence Enabled Variable-Rate Application Platforms

- Scarcity of Water for Fertigation in Arid Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers remained the largest segment by type and accounted for 63.0% of the global fertilizers market share in 2025. This dominance is attributed to the continued reliance of crop production systems on separate applications of nitrogen, phosphorus, and potassium nutrients. Within this segment, nitrogen fertilizers accounted for the largest volume, with products such as urea, anhydrous ammonia, and ammonium nitrate driving demand across major agricultural regions. According to the International Fertilizer Association, global urea production reached 201 million metric tons in 2024, up 3% compared to 2023. China's urea output is projected to reach 76.5 million metric tons by 2026 as new production capacities become operational. Phosphatic fertilizers, including diammonium phosphate, monoammonium phosphate, single superphosphate, and triple superphosphate, remained critical for crop establishment despite higher procurement costs. Potassic fertilizers, led by muriate of potash, continued to experience stable demand, supported by expanding production capacities. Additionally, the segment encompasses secondary nutrients and micronutrients, with zinc holding the largest share among micronutrients, and boron witnessing increased adoption in intensively cultivated farming systems.

Complex fertilizers are anticipated to be the fastest-growing segment by type, with a projected CAGR of 5.8% from 2026 to 2031, surpassing the overall market growth rate. These fertilizers combine multiple nutrients into a single formulation, promoting balanced crop nutrition while simplifying application processes and reducing labor requirements. Adoption is particularly increasing in horticultural, plantation, and other high-value crop systems where nutrient efficiency is crucial for productivity. In Europe, nutrient reduction targets and sustainability initiatives are driving the use of nutrient-dense formulations that enhance nutrient-use efficiency while lowering application volumes. Furthermore, the growing adoption of precision agriculture technologies, variable-rate application systems, and soil-specific nutrient management practices is bolstering demand for balanced fertilizer products. As growers focus on maximizing yields and improving fertilizer efficiency, complex fertilizers are emerging as a preferred alternative to standalone nutrient products, supporting consistent growth throughout the forecast period.

Conventional fertilizers are the largest form and account for 88.5% of the fertilizers market size in 2025, yet growers in regulated regions are gradually shifting to enhanced-efficiency forms that meet environmental targets without sacrificing yield. These products, generally uncoated granules or prills, are applied using broadcast spreaders or incorporated into the soil during tillage. Nutrient availability depends on factors such as soil moisture, temperature, and microbial activity. Their low production cost and compatibility with existing farming equipment support their continued prevalence in price-sensitive markets, including cereals, oilseeds, and sugarcane. Conventional products are increasingly challenged by regulatory restrictions on application rates and by environmental concerns about nutrient runoff. This has led to a gradual shift toward enhanced-efficiency alternatives, even in cost-sensitive segments.

Specialty fertilizers are projected to grow at a CAGR of 6.3% during the period 2026-2031. This growth is driven by the adoption of controlled-release, slow-release, liquid, and water-soluble formulations, which enhance nutrient-use efficiency and reduce labor requirements. Controlled-release fertilizers, coated with polymers or sulfur, release nutrients based on soil temperature and moisture, aligning nutrient availability with crop demand and reducing leaching losses by 20% to 40% compared to conventional fertilizers. Slow-release fertilizers, formulated with chemicals such as urea-formaldehyde or isobutylidene diurea, provide a cost-effective option with extended nutrient release, making them suitable for turfgrass and ornamental applications. Liquid fertilizers are witnessing significant growth in North America and Europe, where large farms incorporate them into existing sprayer systems for foliar or starter applications, ensuring uniform coverage and rapid nutrient uptake by plants.

Complete Report Scope:

- By Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Ammonium Nitrate

- Anhydrous Ammonia

- Urea

- Others

- Phosphatic

- Di-ammonium Phosphate (DAP)

- Mono Ammonium Phosphate (MAP)

- Single Super Phosphate (SSP)

- Triple Superphosphate (TSP)

- Others

- Potassic

- Muriate of Potash (MoP)

- Sulphate of Potash (SoP)

- Others

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- By Form

- Conventional

- Specialty

- Controlled-Release Fertilizer (CRF)

- Liquid Fertilizer

- Slow-Release Fertilizer (SRF)

- Water Soluble

- By Application Mode

- Fertigation

- Foliar

- Soil

- By Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- By Geography

- North America

- Canada

- Mexico

- United States

- Rest of North America

- Europe

- France

- Germany

- Italy

- Netherlands

- Russia

- Spain

- Ukraine

- United Kingdom

- Rest of Europe

- Asia-Pacific

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

- South America

- Argentina

- Brazil

- Rest of South America

- Middle East

- Turkey

- Saudi Arabia

- Rest of Middle East

- Africa

- Nigeria

- South Africa

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific is the largest geography segment, accounting for 52.3% of the fertilizers market share in 2025, led by China and India. China's domestic urea production capacity exceeded 80.45 million metric tons in 2024, ensuring a stable supply. However, older coal-based facilities may face stricter emissions regulations, potentially leading to idled operations and creating opportunities for coastal gas-based plants equipped with carbon capture technology. In India, the Ministry of Agriculture reported that total annual fertilizer consumption for 2023-24 was approximately 60.1 million metric tons. Of this, 50.3 million metric tons were produced domestically, while 17.7 million metric tons were imported. In Southeast Asia, demand is driven by palm oil, rice, and rubber plantations. Additionally, Indonesian refiners are testing controlled-release fertilizer blends in large rice paddies to meet sustainability certification requirements.

Africa is projected to record the fastest compound annual growth rate (CAGR) of 6.2% through 2031. Fertilizer demand in Sub-Saharan Africa is shaped by agricultural modernization, population growth, and government efforts to achieve food self-sufficiency. Fertilizer application rates in the region are considerably lower than global averages, indicating significant growth potential as infrastructure improves and affordability challenges are addressed. Nigeria and South Africa, the region's largest economies, are focusing on increasing domestic production capacities to reduce reliance on imports and stabilize prices. Additionally, Ethiopia, Kenya, and Tanzania are expanding blending facilities that import bulk urea and diammonium phosphate (DAP) to create customized NPK ratios tailored to local crops such as coffee, tea, and maize. In the Middle East, countries like Saudi Arabia, the United Arab Emirates, and Turkey combine domestic production capabilities with imports to meet fertilizer demand, as arid climates and limited arable land restrict agricultural growth. Turkey's strategic location positions it as a logistics hub for fertilizer trade across Europe, Asia, and Africa.

Europe confronts stringent nutrient caps and elevated energy costs that curb straight-fertilizer volumes but boost specialty margins. Eastern European markets, particularly Ukraine and Russia, remain key exporters of urea, ammonium nitrate, and potash. However, geopolitical instability and export restrictions have disrupted trade flows, redirecting volumes toward Asia and Africa. In the United Kingdom, post-Brexit agricultural policy focuses on environmental land management, with subsidies transitioning from production support to ecosystem services. This shift has placed additional pressure on conventional fertilizer demand while creating opportunities for organic and biostimulant products. Crop producers in France and Spain invest in precision-spreaders to comply with nitrogen limits without depressing grain output, reinforcing demand for inhibitor-coated products.

- Nutrien Ltd.

- Uralkali PJSC (Uralchem Group)

- The Mosaic Company

- K+S Aktiengesellschaft

- ICL Group Ltd.

- EuroChem Group AG

- CF Industries Holdings, Inc.

- OCP S.A.

- PhosAgro PJSC

- Coromandel International Limited

- Indian Farmers Fertiliser Cooperative Limited (IFFCO)

- Haifa Chemicals Ltd.

- Yara International ASA

- Koch Fertilizer, LLC

- Grupa Azoty S.A. (Compo Expert)

- BHP Group Limited

- Qinghai Salt Lake Industry Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Surge in fertilizer demand from precision-agriculture projects

- 4.6.2 Transition to climate-smart nutrient-management policies

- 4.6.3 Rapid adoption of specialty and slow-release formulations

- 4.6.4 Capacity expansions in low-cost natural-gas regions

- 4.6.5 Carbon-credit incentives for green ammonia production

- 4.6.6 Artificial intelligence enabled variable-rate application platforms

- 4.7 Market Restraints

- 4.7.1 Volatile feedstock prices

- 4.7.2 Regulatory caps on nitrogen usage in Europe

- 4.7.3 Growing organic farming acreage

- 4.7.4 Scarcity of water for fertigation in arid regions

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Anhydrous Ammonia

- 5.1.2.2.3 Urea

- 5.1.2.2.4 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 Di-ammonium Phosphate (DAP)

- 5.1.2.3.2 Mono Ammonium Phosphate (MAP)

- 5.1.2.3.3 Single Super Phosphate (SSP)

- 5.1.2.3.4 Triple Superphosphate (TSP)

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 Muriate of Potash (MoP)

- 5.1.2.4.2 Sulphate of Potash (SoP)

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 By Form

- 5.2.1 Conventional

- 5.2.2 Specialty

- 5.2.2.1 Controlled-Release Fertilizer (CRF)

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 Slow-Release Fertilizer (SRF)

- 5.2.2.4 Water Soluble

- 5.3 By Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 By Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 Mexico

- 5.5.1.3 United States

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 France

- 5.5.2.2 Germany

- 5.5.2.3 Italy

- 5.5.2.4 Netherlands

- 5.5.2.5 Russia

- 5.5.2.6 Spain

- 5.5.2.7 Ukraine

- 5.5.2.8 United Kingdom

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 Australia

- 5.5.3.2 Bangladesh

- 5.5.3.3 China

- 5.5.3.4 India

- 5.5.3.5 Indonesia

- 5.5.3.6 Japan

- 5.5.3.7 Pakistan

- 5.5.3.8 Philippines

- 5.5.3.9 Thailand

- 5.5.3.10 Vietnam

- 5.5.3.11 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Argentina

- 5.5.4.2 Brazil

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 Nigeria

- 5.5.6.2 South Africa

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Nutrien Ltd.

- 6.4.2 Uralkali PJSC (Uralchem Group)

- 6.4.3 The Mosaic Company

- 6.4.4 K+S Aktiengesellschaft

- 6.4.5 ICL Group Ltd.

- 6.4.6 EuroChem Group AG

- 6.4.7 CF Industries Holdings, Inc.

- 6.4.8 OCP S.A.

- 6.4.9 PhosAgro PJSC

- 6.4.10 Coromandel International Limited

- 6.4.11 Indian Farmers Fertiliser Cooperative Limited (IFFCO)

- 6.4.12 Haifa Chemicals Ltd.

- 6.4.13 Yara International ASA

- 6.4.14 Koch Fertilizer, LLC

- 6.4.15 Grupa Azoty S.A. (Compo Expert)

- 6.4.16 BHP Group Limited

- 6.4.17 Qinghai Salt Lake Industry Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)