|

市場調查報告書

商品編碼

2073619

中東和非洲化肥市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East and Africa Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

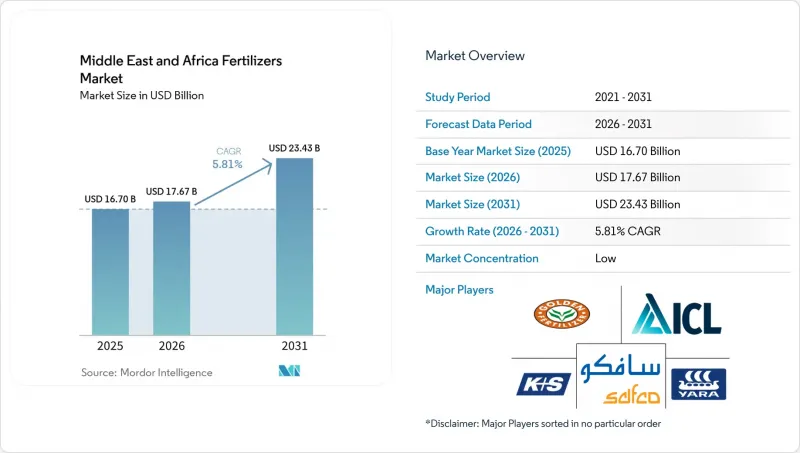

據 Mordor Intelligence 稱,2025 年中東和非洲的化肥市場價值為 167 億美元,預計到 2031 年將達到 234.3 億美元,而 2026 年為 176.7 億美元,預測期(2026-2031 年)的複合年成長率為 5.81%。

本報告按類型(複合肥和單質肥)、形態(常規型和特種型)、施用方法(灌溉施肥、葉面噴布等)、作物(田間作物、園藝作物、土壤)和地區(奈及利亞、沙烏地阿拉伯、南非、土耳其等)分類。市場預測以價值(美元)和數量(公噸)表示。

中東及非洲化肥市場趨勢及洞察

加大力度保障該地區的糧食安全。

中東和非洲各國政府正將化肥自給自足與糧食主權直接掛鉤。 2024年,沙烏地阿拉伯撥款12億美元用於一項進口替代項目,旨在建造一座綜合氨尿素生產廠,以減少其對外國化肥的依賴。奈及利亞總統化肥舉措的目標是利用丹格特集團新增的產能,2027年將化肥進口量減少50%。衣索比亞正與私人投資者合作,利用國內天然氣蘊藏量建造一座價值25億美元的尿素廠,預計年產能300萬噸的生產線將在40個月內投入運作。撒哈拉以南非洲目前約80%的化肥依賴進口,因此,每個新工廠的建設都會向貸款機構和跨國設備供應商發出正面的訊號。這些項目還有助於刺激連接區域供應鏈的配套投資,例如天然氣管道、鐵路支線和散貨碼頭。

擴大政府化肥補貼計劃

世界各國財政部都將補貼視為穩定投入成本、提高農村收入的直接手段。埃及在2024年將其補貼總額提高了35%,使農民購買尿素的價格降至每噸180美元,而國際價格則超過每噸350美元。肯亞的補助計畫惠及120萬小規模農戶,透過行動代金券將基於土壤檢測結果的處方箋與認證零售商聯繫起來,從而降低了高達50%的投入成本。奈及利亞在2024年發放了1,200萬袋補貼的NPK複合肥,並在推廣的同時引入電子錢包支付以遏制挪用行為。沙烏地阿拉伯為椰棗種植者承擔微量元素肥料包75%的農場到貨成本,從而促進了乾旱地區精準養分管理技術的普及。由於需求可預測,混合商可以提前敲定原料合約並規劃存貨周轉。

天然氣價格波動對氨價格的影響

由於能源成本約佔氨生產成本的四分之三,天然氣價格波動直接影響尿素價格。 2022年天然氣價格飆升高峰期,歐盟關閉了高達70%的產能,迫使非洲買家支付更高的運費並延長交貨週期。在肯亞,2020年至2022年間,零售前置作業時間價格上漲了150%,影響了小農戶的主糧作物產量,而這些小規模農戶供應了該國大部分糧食。進口商目前正在實現供應商多元化並利用長期天然氣契約,但每當基準天然氣市場趨緊時,風險仍然很高。

細分市場分析

2025年,單一成分肥料在中東和非洲肥料市場佔據57.9%的市場。政府扶持政策往往補貼基礎氮磷鉀肥,使得單一成分肥料成為小規模農戶的首選。尿素在糧食生產系統中氮肥銷售中佔據主導地位,而磷酸二銨(DAP)和磷酸一銨(MAP)仍然是磷酸鹽類肥料的主要產品。中東和非洲單一成分肥料市場的規模得益於標準化的分銷和倉儲系統,該系統適合大宗運輸。

複合肥料預計將成為成長最快的細分市場,2026年至2031年的複合年成長率將達到7.2%。它們在園藝、灌溉經濟作物和需要精確養分比例的出口型農場中發揮著至關重要的作用。摩洛哥在SP2M計畫下擴大產能,將提高整個北非地區的複合肥料產量,提供結合大量元素和微量元素的田間專用配方。在南非等強制進行土壤檢測的地區,以及貸款機構要求提供農業化學品處方箋作為貸款條件的地區,複合肥料的應用最為廣泛。

到2025年,傳統顆粒肥料將在中東和非洲的肥料市場佔據83.5%的佔有率。其廣泛的應用、穩健的供應鏈以及與現有設備的兼容性支撐了其市場主導地位。為了保持成本競爭力,生產商正在投資節能維修,例如提高埃及阿布基爾地區的天然氣利用效率。

特種肥料、緩效肥料、水溶性肥料和葉面噴布液態肥佔據著一個規模雖小但成長迅速的細分市場,預計2026年至2031年將以9.3%的複合年成長率成長。海灣國家溫室滴灌面積的擴大以及土耳其園藝業水耕技術的普及,正在推動全水溶性產品的需求。緩釋包衣技術對勞動力資源有限的偏遠地區種植者極具吸引力,因為它可以減少施肥頻率,並最大限度地減少沙質土壤中的養分流失。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 主要營養素

- 田間作物

- 園藝作物

- 次要營養元素

- 田間作物

- 園藝作物

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 地方社區糧食安全措施增加

- 擴大政府化肥補貼計劃

- 擴大特種肥料和緩釋肥料的使用

- 加大對現代灌溉系統的投資

- 在油籽作物輪作中過渡到添加硫的混合飼料。

- 淡化水使用量的增加推動了對微量營養素的需求。

- 市場限制因素

- 氨價波動與天然氣價格相關

- 紅海主要港口仍存在物流瓶頸。

- 監管機構反對進口磷酸鹽中的鎘含量

- 農民對在高價值作物中使用生技藥品的偏好日益成長

第5章 市場規模與成長預測

- 類型

- 複雜類型

- 直的

- 微量營養素

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 氮基

- 硝酸銨

- 尿素

- 其他

- 磷酸鹽基

- 磷酸二銨(DAP)

- 磷酸一銨(MAP)

- 瞬態過磷酸鈣(SSP)

- 三重過磷酸鈣(TSP)

- 其他

- 鉀基

- 氯化鉀(MoP)

- 硫酸鉀(SoP)

- 其他

- 次要大量營養元素

- 鈣

- 鎂

- 硫

- 微量營養素

- 形式

- 傳統的

- 專業

- 控釋肥料(CRF)

- 液體肥料

- 緩效性肥料(SRF)

- 水溶性

- 使用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 地區

- 奈及利亞

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲國家

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- Yara International ASA

- SABIC Agri-Nutrients Company(Saudi Basic Industries Corporation)

- OCP Group

- Ma'aden Phosphate Company(Saudi Arabian Mining Company-Ma'aden)

- Qatar Fertiliser Company QAFCO(Industries Qatar)

- ICL Group Ltd

- K+S Aktiengesellschaft

- EuroChem Group AG

- PhosAgro PJSC

- Fertiglobe PLC(OCI NV)

- Omnia Fertilizer(Pty)Ltd(Omnia Holdings Ltd)

- Dangote Fertilizer Ltd(Dangote Industries Ltd)

- Indorama Eleme Fertilizer and Chemicals Ltd(Indorama Corporation)

- Haifa Group

- Jordan Phosphate Mines Company PLC

- Golden Fertilizer Company Limited

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the middle east and Africa fertilizers market size was valued at USD 16.70 billion in 2025 and estimated to grow from USD 17.67 billion in 2026 to reach USD 23.43 billion by 2031, at a CAGR of 5.81% during the forecast period (2026-2031).

This report is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and More), by Crop Type (Field Crops, Horticultural Crops, and Soil), and by Geography (Nigeria, Saudi Arabia, South Africa, Turkey, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Middle East and Africa Fertilizers Market Trends and Insights

Rising Regional Food Security Initiatives

Middle East and African governments are tying fertilizer self-sufficiency directly to food sovereignty. Saudi Arabia earmarked USD 1.2 billion for import-substitution projects in 2024, targeting integrated ammonia and urea complexes that reduce external dependence. Nigeria's Presidential Fertilizer Initiative set a goal to trim fertilizer imports by 50% by 2027, leveraging new capacity at Dangote facilities. Ethiopia partnered with a private investor to build a USD 2.5 billion urea plant that will tap domestic gas reserves, bringing 3 million metric tons annual line online within 40 months. Sub-Saharan Africa currently imports roughly 80% of its fertilizer, so each new plant sends a positive signal to lenders and multinational equipment suppliers. These projects also catalyze ancillary investments in gas pipelines, rail spurs, and bulk terminals that knit the regional supply chain together.

Expansion of Government Fertilizer Subsidy Programs

National treasuries view subsidies as a fast-acting lever to stabilize input costs and rural incomes. Egypt raised its subsidy pool by 35% in 2024, cutting farmer urea prices to USD 180 per metric ton against international quotes above USD 350 per metric ton. Kenya's program reached 1.2 million smallholders, slashing input costs by up to 50% through mobile vouchers that link soil-test prescriptions to verified dealer outlets. Nigeria distributed 12 million bags of subsidized NPK blends in 2024 and combined the roll-out with e-wallet payments that curb leakages. Saudi Arabia covers 75% of the landed cost of micronutrient packages for date-palm growers, prompting a surge in precision nutrition adoption on arid plots. Predictable offtake allows blenders to lock in feedstock contracts and plan inventory turns in advance.

Volatile Natural Gas Linked Ammonia Prices

Energy represents roughly three-quarters of ammonia production cost, so swings in gas prices ripple straight into urea quotations. The European Union shuttered up to 70% of its capacity at the height of the 2022 gas spike, forcing African buyers to absorb freight premiums and longer lead times. Kenya experienced retail fertilizer prices that climbed 150% between 2020 and 2022, denting staple-crop yields among the smallholders who supply most domestic food. Importers now diversify suppliers and use longer-tenor gas contracts, yet risk remains elevated whenever benchmark gas trade tightens.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Specialty and Slow-Release Fertilizers

- Rising Investments in Modern Irrigation Systems

- Persistent Logistical Bottlenecks at Key Red Sea Ports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight formulations accounted for 57.9% of the Middle East and Africa fertilizers market share in 2025. Government programs tend to subsidize basic NPK components, making single-nutrient grades the default choice among smallholders. Urea leads nitrogen sales for cereal production systems, whereas DAP and MAP remain the principal phosphatic products. The Middle East and Africa fertilizers market size for straight grades benefits from standardized distribution and storage systems that favor bulk handling.

Complex fertilizers are projected to be the fastest-growing segment, with a CAGR of 7.2% through 2026 to 2031. They play a crucial role in horticulture, irrigated cash crops, and export-oriented farms that demand precise nutrient ratios. Morocco's capacity expansion under the SP2M plan will lift blended output across North Africa, offering site-specific formulations that pair macronutrients with micronutrient packages. Uptake is strongest where soil-testing mandates exist, such as in South Africa, or where lenders tie credit to agronomic prescriptions.

Conventional granules captured 83.5% share of the Middle East and Africa fertilizers market in 2025. Broad familiarity, robust supply chains, and equipment compatibility underpin their dominance. Producers are investing in energy-saving revamps, such as Egypt's Abu Qir natural gas efficiency upgrade, to keep cost curves competitive.

Specialty fertilizers, grades of controlled-release fertilizers, water-soluble fertilizers, and foliar liquids occupy a small yet fast-rising niche, projected to grow at a CAGR of 9.3% during 2026-2031. Drip-irrigated acreage expansion in Gulf greenhouses and the spread of hydroponics in Turkish horticulture fuel demand for fully soluble products. Slow-release coatings appeal to remote growers with limited labor, reducing application frequency and nutrient loss in sandy soils.

Complete Report Scope:

- Type

- Complex

- Straight

- Micronutrients

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Nitrogenous

- Ammonium Nitrate

- Urea

- Others

- Phosphatic

- Diammonium Phosphate (DAP)

- Monoammonium Phosphate (MAP)

- Single Super Phosphate (SSP)

- Triple Super Phosphate (TSP)

- Others

- Potassic

- Muriate of Potash (MoP)

- Sulfate of Potash (SoP)

- Others

- Secondary Macronutrients

- Calcium

- Magnesium

- Sulfur

- Micronutrients

- Form

- Conventional

- Specialty

- Controlled Release Fertilizer (CRF)

- Liquid Fertilizer

- Slow Release Fertilizer (SRF)

- Water Soluble

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- Geography

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

List of Companies Covered in this Report:

- Yara International ASA

- SABIC Agri-Nutrients Company (Saudi Basic Industries Corporation)

- OCP Group

- Ma'aden Phosphate Company (Saudi Arabian Mining Company - Ma'aden)

- Qatar Fertiliser Company QAFCO (Industries Qatar)

- ICL Group Ltd

- K+S Aktiengesellschaft

- EuroChem Group AG

- PhosAgro PJSC

- Fertiglobe PLC (OCI N.V.)

- Omnia Fertilizer (Pty) Ltd (Omnia Holdings Ltd)

- Dangote Fertilizer Ltd (Dangote Industries Ltd)

- Indorama Eleme Fertilizer and Chemicals Ltd (Indorama Corporation)

- Haifa Group

- Jordan Phosphate Mines Company PLC

- Golden Fertilizer Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Rising regional food security initiatives

- 4.6.2 Expansion of government fertilizer subsidy programs

- 4.6.3 Increasing adoption of specialty and slow-release fertilizers

- 4.6.4 Rising investments in modern irrigation systems

- 4.6.5 Shift toward sulfur-enriched blends for oil-seed crop rotations

- 4.6.6 Growing use of desalinated water driving demand for micronutrients

- 4.7 Market Restraints

- 4.7.1 Volatile natural gas linked ammonia prices

- 4.7.2 Persistent logistical bottlenecks at key Red Sea ports

- 4.7.3 Regulatory pushback on cadmium levels in imported phosphates

- 4.7.4 Rising farmer preference for biologicals in high-value crops

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Urea

- 5.1.2.2.3 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 Diammonium Phosphate (DAP)

- 5.1.2.3.2 Monoammonium Phosphate (MAP)

- 5.1.2.3.3 Single Super Phosphate (SSP)

- 5.1.2.3.4 Triple Super Phosphate (TSP)

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 Muriate of Potash (MoP)

- 5.1.2.4.2 Sulfate of Potash (SoP)

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Specialty

- 5.2.2.1 Controlled Release Fertilizer (CRF)

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 Slow Release Fertilizer (SRF)

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental

- 5.5 Geography

- 5.5.1 Nigeria

- 5.5.2 Saudi Arabia

- 5.5.3 South Africa

- 5.5.4 Turkey

- 5.5.5 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 SABIC Agri-Nutrients Company (Saudi Basic Industries Corporation)

- 6.4.3 OCP Group

- 6.4.4 Ma'aden Phosphate Company (Saudi Arabian Mining Company - Ma'aden)

- 6.4.5 Qatar Fertiliser Company QAFCO (Industries Qatar)

- 6.4.6 ICL Group Ltd

- 6.4.7 K+S Aktiengesellschaft

- 6.4.8 EuroChem Group AG

- 6.4.9 PhosAgro PJSC

- 6.4.10 Fertiglobe PLC (OCI N.V.)

- 6.4.11 Omnia Fertilizer (Pty) Ltd (Omnia Holdings Ltd)

- 6.4.12 Dangote Fertilizer Ltd (Dangote Industries Ltd)

- 6.4.13 Indorama Eleme Fertilizer and Chemicals Ltd (Indorama Corporation)

- 6.4.14 Haifa Group

- 6.4.15 Jordan Phosphate Mines Company PLC

- 6.4.16 Golden Fertilizer Company Limited

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

印度緩釋肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區緩釋肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料肥料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)中國化肥市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)德國化肥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)化肥:市佔率分析、產業趨勢與統計、成長預測(2026-2031)南美洲化肥市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2034年化肥市場預測-按產品類型、形態、作物種類、施用方法、技術、通路和地區分類的全球分析綠色肥料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)