|

市場調查報告書

商品編碼

2072487

影像處理處理器(GPU):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Graphics Processing Unit (GPU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

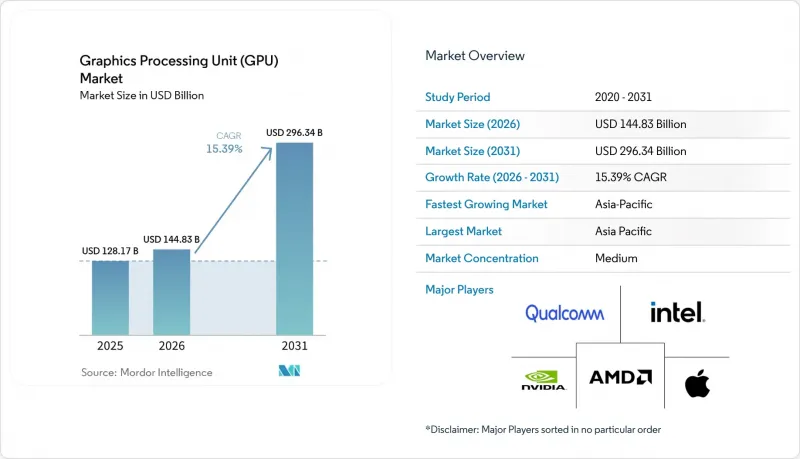

根據 Mordor Intelligence 預測,GPU 市場預計將從 2025 年的 1,281.7 億美元成長到 2026 年的 1,448.3 億美元,到 2031 年達到 2963.4 億美元,2026 年至 2031 年的複合年成長率預計為 15.39%。

本報告按整合類型(整合GPU和獨立GPU)、裝置應用(行動裝置和平板電腦、PC和工作站、伺服器和資料中心加速器、遊戲主機和手持終端機、汽車和ADAS以及其他嵌入式和邊緣裝置)以及地區進行細分。市場預測以美元(USD)為單位。

全球影像處理處理器 (GPU) 市場趨勢與洞察

超大規模人工智慧訓練與推理叢集擴展

GPU市場正受到從週期性模型訓練轉變為「永不運作的AI工廠」的驅動,這種「永不停歇的AI工廠」在整個訓練、訓練後處理和推理階段都保持叢集運作。亞馬遜、Google、Meta和微軟已確認,其總資本支出將從2025年的4,100億美元增至2026年的7,250億美元,其中大部分成長將用於AI基礎設施,而GPU仍是其中一項主要的硬體成本。供應側趨勢也呈現類似的模式,NVIDIA的資料中心營收在2027會計年度第一季達到752億美元,運算營收增至604億美元,網路營收增至148億美元。因此,隨著大規模AI工廠需要高密度互連架構和加速器,GPU市場正在擴張以滿足運算和網路方面的需求。 NVIDIA也表示,超大規模資料中心業者資料中心僅佔其資料中心收入的一半,這表明需求正在擴展到雲端服務商、企業部署和政府主導的專案。這對 GPU 市場具有重大意義,因為它減少了對單一買家群體的依賴,並使當前的需求比超大規模資料中心業者的狹窄週期更具永續性。

企業人工智慧工廠和國家主導的運算採購

隨著國家級運算項目和企業人工智慧工廠開始將GPU叢集視為戰略基礎設施而非僅僅作為一種可選的技術資源,GPU市場湧現新的需求流。中東和歐洲的採購模式形成了與傳統超大規模資料中心業者不同的客戶群,高階GPU的採購範圍也隨之擴大。歐盟人工智慧立法以及受監管行業更嚴格的資料居住要求,也促使更多運算資源留在國內,使得本地加速器採購不僅成為效能考量,也成為合規性問題。這導致價格趨勢發生變化,因為主權買家通常不受超大規模資料中心業者資料中心批量採購配額的限制,以標價或高於標價的價格吸收供應。此外,儘管雲端運算的普及程度有所提高,但頂級加速器的長期排隊等候使得一般企業更難進入GPU市場。因此,在政府和受監管企業要求明確市場未來前景的同時,小規模買家的供應平衡卻變得更加緊張。

每輛車的ADAS和車載運算能力均有所提高

此外,隨著ADAS感知處理、感測器融合和駕駛座渲染等功能向集中式運算平台轉移,汽車產業的GPU市場正處於長期成長軌道上。 NVIDIA的DRIVE Thor平台旨在為L4級應用提供2000 TOPS的運算能力,這表明汽車設計正朝著更高的單車運算密度方向發展。透過將ADAS和駕駛座工作負載整合到數量更少、功能更強大的處理器上,每個平台的半導體數量增加,從而支援各代車型對GPU的持續需求。這種轉變也有利於擁有檢驗的汽車級軟體和安全功能的供應商,因為設計方案的採用不僅取決於純粹的性能,還取決於法規遵循。與軟體定義汽車和車輛安全相關的法規進一步推動了這一趨勢,因為它們增加了量產車對持續即時推理的需求。在GPU市場,這意味著汽車產業的收入成長速度將低於資料中心的收入成長速度,但每輛車的半導體數量正變得結構性地穩定。

細分市場分析

到2025年,獨立GPU將佔據GPU市場佔有率的63.84%,預計到2031年,該細分市場將以15.78%的複合年成長率成長。這個細分市場的主導地位反映出,在高階領域,專用顯存、高頻寬以及與高要求AI工作負載的兼容性是共用系統資源無法比擬的。 NVIDIA的Blackwell架構顯著提升了封裝記憶體容量,B200的HBM3e顯存容量高達192GB,而H100僅為80GB,這凸顯了即使在單一產品週期內,記憶體需求也在快速成長。 NVIDIA也採用了透過10TB/s NV-HBI連接的雙晶片設計,顯示高階獨立顯示卡設計正在突破單晶片設計的限制,以保持運算密度。在 GPU 市場,離散型產品在訓練和大規模批量推理方面仍然佔據主導地位,因為這些工作負載仍然受到記憶體頻寬和本地加速器容量的限制。

到2026年,整合GPU將取得顯著發展,其在客戶端AI系統和低成本推理環境中的作用將會擴展。 AMD的Ryzen AI 400系列將高達60 TOPS的NPU運算能力與整合的Radeon 800M系列顯示卡結合,而Ryzen AI Halo平台則透過更強大的圖形處理能力和大規模的統一記憶體池進一步擴展了其產品模式。這項進步使得本地推理在專業筆記型電腦、開發系統和工作站級設備中更加實用,這些設備對成本和功耗都有嚴格的要求。然而,由於統一記憶體平台的頻寬HBM的加速器,GPU產業在尖端訓練和高吞吐量推理方面仍依賴獨立顯示卡產品。因此,在圖形處理器(GPU)市場,儘管整合顯示卡產品在邊緣運算領域的重要性持續成長,獨立顯示卡產品仍可能繼續主導效能領域,並佔據大部分利潤。

區域分析

2025年,亞太地區佔全球銷售額的43.16%,預計到2031年,該地區GPU市場將以15.37%的複合年成長率成長。亞太地區的主導地位源自於其作為記憶體、封裝和系統製造等關鍵供應鏈樞紐的地位,以及其龐大的終端用戶需求。中國仍是GPU市場的核心,國內廠商在加強在地採購政策的推動下加速了商業化進程。 Biren和Iluvatar CoreX在2025年均實現了三位數的銷售成長,反映出在出口環境日益嚴峻的情況下,中國市場對本土供應商的需求不斷增強。韓國依然至關重要,三星和SK海力士提供的HBM堆疊支撐著尖端加速器的性能。同時,日本透過採用超大規模資料中心和工業數位雙胞胎擴大了其需求。

北美保持了其作為全球第二大GPU市場的地位,擁有全球最大的超大規模採購商,並在全球人工智慧叢集部署中擁有強大的購買力。亞馬遜、Google、Meta和微軟計畫在2026年共投入7,250億美元的資本支出,這些支出趨勢確保了美國持續維持加速器採購中心的地位。從政策角度來看,北美也對全球市場產生了影響,因為美國的出口管制架構直接影響先進GPU供應商可以服務哪些海外市場。加拿大推出的國家主權運算舉措拓寬了該地區的需求結構,使其不再局限於私人超大規模企業,這印證了公共部門採購在未來將變得更加重要的觀點。因此,與其他地區相比,北美對GPU市場的供需兩端都產生了更大的影響。

隨著合規性、數位主權以及受監管產業對人工智慧的採用,歐洲GPU市場發展迅速,推動了本地運算投資進入更系統化的階段。中東和非洲的重要性日益凸顯,海灣國家政府主導的計畫已開始大規模訂購高階叢集,其規模遠遠超過僅憑人口規模所能預期的水平。南美洲仍處於發展初期,巴西是金融服務業資料中心託管成長和人工智慧需求的重要樞紐。在歐洲、中東和非洲以及南美洲,GPU市場的擴張更源自於策略需求和政策調整,而非純粹的消費者需求,因此呈現出比以往週期更加多元化的區域成長模式。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 規模化超大規模人工智慧訓練與推理集群

- 企業人工智慧工廠和主權運算採購

- PC 與行動裝置的邊緣 AI 升級週期

- 每輛車的ADAS和車載運算能力均有所提高

- 基於晶片組的GPU藍圖旨在提高良率和產品擴展性

- GPU即服務:擴大超超大規模資料中心業者以外使用者的存取權限

- 市場限制因素

- 出口限制和關稅波動

- GPU 和記憶體的平均售價 (ASP) 飆升,正在減緩它們在主流市場的普及速度。

- 過度依賴 HBM 和 CoWoS 分配到 AI 機架

- 高密度GPU園區電網連接延遲

- 產業價值鏈分析

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型整合

- 整合顯示卡(iGPU)

- 獨立GPU(dGPU)

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車和高級駕駛輔助系統

- 其他嵌入式和邊緣設備

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Arm Holdings plc

- Apple Inc.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- Imagination Technologies Group Limited

- Huawei Technologies Co., Ltd.

- Moore Threads Intelligent Technology(Beijing)Co., Ltd.

- Biren Technology Co., Ltd.

- VeriSilicon Co., Ltd.

- Zhaoxin Semiconductor Co., Ltd.

- VIA Technologies, Inc.

- UNISOC Technologies Co., Ltd.

- Renesas Electronics Corporation

- Rockchip Electronics Co., Ltd.

- Loongson Technology Corporation Limited

- Bolt Graphics, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the GPU market size is expected to increase from USD 128.17 billion in 2025 to USD 144.83 billion in 2026 and reach USD 296.34 billion by 2031, growing at a CAGR of 15.39% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, and Discrete GPUs), Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and Other Embedded and Edge Devices), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

Global Graphics Processing Unit (GPU) Market Trends and Insights

Hyperscale AI Training and Inference Cluster Expansion

The GPU market is being pushed higher by a shift from periodic model training to always-on AI factory operations that keep clusters busy across training, post-training, and inference. Amazon, Google, Meta, and Microsoft confirmed a combined 2026 capital expenditure of USD 725 billion, up from USD 410 billion in 2025, and most of that increase was directed toward AI infrastructure, where GPUs remain the main hardware cost item. Supply-side results pointed to the same pattern as NVIDIA's data center revenue reached USD 75.2 billion in Q1 FY2027, while compute revenue reached USD 60.4 billion, and networking revenue rose to USD 14.8 billion. The GPU market is therefore expanding to meet both compute and networking demand, as larger AI factories require dense interconnect fabrics and accelerators. NVIDIA also said hyperscalers accounted for only half of its data center revenue, indicating that demand had broadened to cloud specialists, enterprise deployments, and sovereign programs. This matters for the GPU market because it reduces dependence on a single buyer group and makes current demand more durable than a narrow hyperscaler cycle.

Enterprise AI Factory and Sovereign Compute Procurement

The GPU market gained another demand stream as national compute programs and enterprise AI factories began treating GPU clusters as strategic infrastructure rather than optional technology capacity. Procurement in the Middle East and Europe added a separate customer layer that sat outside the traditional hyperscaler channel, widening the geographic spread of high-end GPU buying. The EU AI Act and tighter data residency rules in regulated sectors also pushed more compute to remain within national borders, making local accelerator procurement a compliance issue as well as a performance decision. This shifted pricing behavior because sovereign buyers often operated outside hyperscaler volume frameworks and absorbed supply at or above list pricing. The GPU market also became harder for mainstream enterprises to access because allocation queues for top-end accelerators stayed long even as cloud access expanded. As a result, sovereign and regulated enterprises demand that the market's forward visibility be strengthened while also tightening the supply balance for smaller buyers.

Rising ADAS and In-Cabin Compute Content Per Vehicle

The GPU market also has a longer-cycle growth path in vehicles as ADAS perception, sensor fusion, and cockpit rendering move onto centralized compute platforms. NVIDIA's DRIVE Thor platform was positioned at 2,000 TOPS for Level 4 applications, which showed how automotive designs are moving toward much higher compute density per vehicle. Consolidating ADAS and cockpit workloads onto fewer, more capable processors raises semiconductor content per platform and supports sustained GPU demand across model generations. The same shift also favors suppliers with validated automotive-grade software and safety capabilities, because design wins depend on compliance as much as raw performance. Regulations tied to software-defined vehicles and vehicle safety are reinforcing that direction by increasing the need for continuous real-time inference in production fleets. In the GPU market, that means automotive revenue grows more slowly than datacenter revenue, but content growth per vehicle is becoming structurally stronger.

Other drivers and restraints analyzed in the detailed report include:

- Edge AI Upgrade Cycle in PCs and Mobile Devices

- Export Controls and Tariff Volatility

- Elevated GPU and Memory ASPs Slowing Mainstream Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs held 63.84% of the GPU market share in 2025, and this segment is projected to expand at a 15.78% CAGR through 2031. The segment's lead reflected the fit between dedicated memory, high bandwidth, and intensive AI workloads that shared system resources cannot match at the top end. NVIDIA's Blackwell generation raised on-package memory sharply, with the B200 carrying 192 GB of HBM3e versus 80 GB on the H100, underscoring how quickly memory requirements have risen within a single product cycle. NVIDIA also used a dual-die design connected via NV-HBI at 10 TB/s, demonstrating how high-end discrete designs are moving beyond monolithic limits to sustain compute density. The GPU market continued to favor discrete products in training and large-batch inference because those workloads remain constrained by memory bandwidth and local accelerator capacity.

Integrated GPUs improved materially in 2026, which widened their role in client AI systems and lower-cost inference setups. AMD's Ryzen AI 400 Series combined up to 60 TOPS of NPU compute with integrated Radeon 800M Series graphics, and the Ryzen AI Halo platform extended that model with stronger graphics capability and large unified memory pools. That progress made local inference more practical for professional notebooks, developer systems, and workstation-class devices that need lower cost and tighter power envelopes. Even so, the GPU industry still relies on discrete products for frontier training and high-throughput inference because unified memory platforms do not yet match the bandwidth of HBM-based accelerators. The graphics processing unit (GPU) market is therefore likely to continue to see integrated products gain relevance at the edge while discrete products hold the performance frontier and most of the profit pool.

Complete Report Scope:

- By Integration Type

- Integrated GPUs (iGPU)

- Discrete GPUs (dGPU)

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive and ADAS

- Other Embedded and Edge Devices

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Rest of Asia-Pacific

- South America

- Middle East and Africa

- North America

Geography Analysis

Asia-Pacific held 43.16% of global revenue in 2025, and the regional GPU market is projected to expand at a 15.37% CAGR through 2031. The region led because it combined major end demand with critical supply chain positions in memory, packaging, and system manufacturing. China remained central to the GPU market as domestic vendors accelerated commercialization under a stronger local procurement push. Biren and Iluvatar CoreX both reported triple-digit revenue growth in 2025, reflecting the growing support of Chinese demand for local suppliers amid a tighter export environment. South Korea remained vital because Samsung and SK Hynix supply the HBM stacks that underpin leading-edge accelerator performance, while Japan added demand through hyperscale data centers and industrial digital twin adoption.

North America remained the second-largest center of the GPU market because it houses the largest hyperscale buyers and the primary purchasing authority for global AI cluster deployments. Amazon, Google, Meta, and Microsoft together planned USD 725 billion in 2026 capital expenditure, and that spending profile kept the United States at the center of accelerator procurement. North America also shaped the global market through policy, since the US export control framework directly affected which overseas markets advanced GPU vendors could serve. Canada's addition of sovereign compute initiatives widened the region's demand profile beyond private hyperscalers and supported the view that public sector procurement would matter more over time. The region, therefore, influenced both the demand and the supply sides of the GPU market more than any other geography.

Europe's GPU market advanced as compliance, digital sovereignty, and regulated-sector AI adoption pushed local compute investment into a more structured phase. The Middle East and Africa became more important because Gulf sovereign programs started ordering high-end clusters at a scale that exceeded what population size alone would suggest. South America remained earlier in its development cycle, with Brazil serving as the primary base for colocation growth and AI demand in financial services. Across Europe, the Middle East and Africa, and South America, the GPU market expanded more through strategic need and policy alignment than through pure consumer demand, making regional growth patterns more diverse than in earlier cycles.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Arm Holdings plc

- Apple Inc.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- Imagination Technologies Group Limited

- Huawei Technologies Co., Ltd.

- Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- Biren Technology Co., Ltd.

- VeriSilicon Co., Ltd.

- Zhaoxin Semiconductor Co., Ltd.

- VIA Technologies, Inc.

- UNISOC Technologies Co., Ltd.

- Renesas Electronics Corporation

- Rockchip Electronics Co., Ltd.

- Loongson Technology Corporation Limited

- Bolt Graphics, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Hyperscale AI Training and Inference Cluster Expansion

- 4.3.2 Enterprise AI Factory and Sovereign Compute Procurement

- 4.3.3 Edge AI Upgrade Cycle in PCs and Mobile Devices

- 4.3.4 Rising ADAS and In-Cabin Compute Content per Vehicle

- 4.3.5 Chiplet-Based GPU Road Maps Improving Yield and Product Scaling

- 4.3.6 GPU-as-a-Service Broadening Access Beyond Hyperscalers

- 4.4 Market Restraints

- 4.4.1 Export Controls and Tariff Volatility

- 4.4.2 Elevated GPU and Memory ASPs Slowing Mainstream Adoption

- 4.4.3 HBM and CoWoS Allocation Bias Toward AI Racks

- 4.4.4 Grid Interconnection Delays for High-Density GPU Campuses

- 4.5 Industry Value Chain Analysis

- 4.6 Supply-Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive and ADAS

- 5.2.6 Other Embedded and Edge Devices

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 South Korea

- 5.3.3.4 India

- 5.3.3.5 Southeast Asia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Incorporated

- 6.4.5 Arm Holdings plc

- 6.4.6 Apple Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 MediaTek Inc.

- 6.4.9 Imagination Technologies Group Limited

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- 6.4.12 Biren Technology Co., Ltd.

- 6.4.13 VeriSilicon Co., Ltd.

- 6.4.14 Zhaoxin Semiconductor Co., Ltd.

- 6.4.15 VIA Technologies, Inc.

- 6.4.16 UNISOC Technologies Co., Ltd.

- 6.4.17 Renesas Electronics Corporation

- 6.4.18 Rockchip Electronics Co., Ltd.

- 6.4.19 Loongson Technology Corporation Limited

- 6.4.20 Bolt Graphics, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

整合顯示卡:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

整合顯示卡:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)