|

市場調查報告書

商品編碼

2064542

印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)India GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

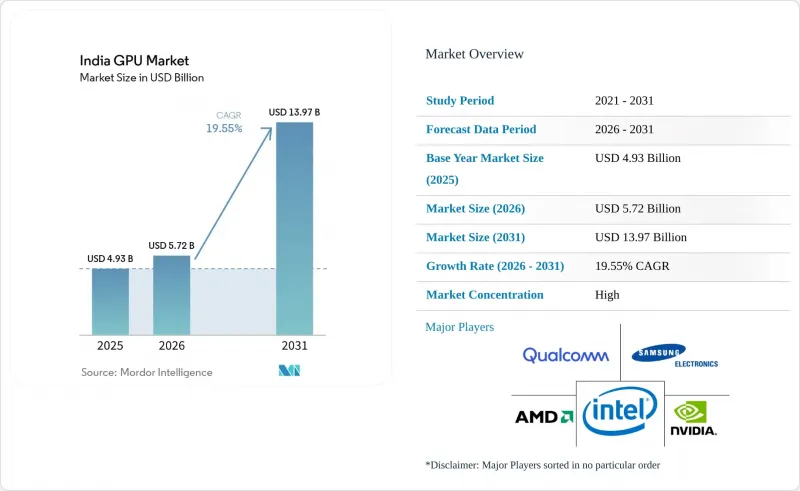

據 Mordor Intelligence 稱,印度 GPU(圖形處理器)市場預計將從 2025 年的 49.3 億美元成長到 2026 年的 57.2 億美元,到 2031 年達到 139.7 億美元,2026 年至 2031 年的複合年成長率為 19.5%。

本報告按整合類型(整合GPU、獨立GPU)和裝置應用(行動裝置/平板電腦、PC/工作站、伺服器/資料中心加速器、遊戲機/掌上遊戲機、汽車/ADAS以及其他嵌入式裝置/邊緣裝置)進行分類。市場預測以美元(USD)計價。

印度GPU市場的趨勢與洞察

雲端服務供應商正在加大對印度超大規模資料中心的投資。

超大規模營運商如今正將印度定位為戰略運算區域,而不僅僅是成本套利中心。微軟的多區域部署採用了NVIDIA H100和即將推出的Blackwell GPU,而Google則在擴展其TPU和GPU加速的基礎設施,以支援企業級AI工作負載。本土供應商Yotta Infrastructure已部署超過32,000塊H100,並可升級至Blackwell Ultra,顯示印度正在從通用雲端轉向推理最佳化叢集。 「印度人工智慧計畫」(IndiaAI Mission)正在撥款34,000塊國產GPU,以減少對海外雲端的依賴。這些發展共同推動了印度GPU市場持續兩位數的成長。

在邊緣設備上採用人工智慧工作負載

邊緣推理技術已從概念驗證(PoC) 階段邁向零售分析、工業視覺和公共安全等領域的全面部署。高通驍龍 8 Elite Gen 5 的圖形性能提升了 23%,使旗艦智慧型手機能夠實現設備內 AI 生成。同時,聯發科天璣 9500 將射線追蹤硬體引入中高階設備。在二線智慧城市專案中,邊緣 GPU 節點正被用於滿足低於 50 毫秒的延遲要求。印度國家支付公司 (NPCI) 正在使用 GPU 加速模型每月審查 120 億筆支付交易,這證明了在全國範圍內進行關鍵任務型邊緣推理的可行性。

高級節點中的慢性導入依賴

由於印度缺乏28奈米以下的製造程序,不得不進口採用4奈米或更小前置作業時間製造的資料中心GPU。 GPU約佔人工智慧伺服器組件成本的90%,而海外代工廠的供應分配則是限制其發展的一大瓶頸。除了交貨週期長之外,本地封裝高頻寬記憶體的能力有限,也加劇了印度易受地緣政治衝擊的影響。

細分市場分析

到2025年,獨立顯示卡將佔據印度GPU市場66.18%的佔有率。伺服器、遊戲PC和專業工作站正在轉向使用專用晶片,這些晶片能夠提供更高的記憶體頻寬和更專業的張量運算能力。大規模部署,例如Yotta公司擁有超過32000個單元的H100叢集,充分展現了企業對頂級加速器的巨大需求。在顯示卡廠商的協助下,遊戲發燒友正從GTX 1060等級的硬體升級到RTX 50系列顯示卡,這些廠商提供的預超頻和延長保固服務也功不可沒。在專業領域,CAD和媒體製作軟體正在使用經過驅動認證的Quadro和Radeon Pro系列顯示卡,這推高了顯示卡的平均售價。

整合式顯示卡(佔剩餘的33.82%)是主流筆記型電腦和智慧型手機出貨量的主要驅動力,這些裝置的散熱設計和組件成本上限都非常嚴格。英特爾Iris Xe和AMD Radeon 700M顯示卡能夠滿足日常辦公室和輕量級創新工作負載的需求。在智慧型手機領域,高通Adreno和聯發科Immortalis核心現在負責裝置上的漫反射建模和NPU輔助攝影。在印度GPU市場,整合晶片的市場規模預計將繼續絕對成長,但由於資料中心需求不斷成長,營收佔有率正逐漸向獨立顯示卡轉移。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在邊緣設備上採用人工智慧工作負載

- 印度遊戲生態系統的快速擴張

- 政府半導體製造生產關聯激勵計劃

- 銀行、金融服務和保險 (BFSI) 行業對高效能運算的需求日益成長。

- 數據主導汽車高階駕駛輔助系統(ADAS)的普及

- 雲端服務供應商正在加大對印度超大規模資料中心的投資。

- 市場限制因素

- 高級節點中的慢性導入依賴

- 電力成本波動會影響資料中心的總擁有成本 (TCO)。

- 國內GPU設計人才庫缺乏智慧財產權

- 由於全球供應鏈中斷導致供不應求

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 按整合類型

- 整合顯示卡(iGPU)

- 獨立GPU(dGPU)

- 裝置應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機/掌上遊戲機

- 汽車/ADAS

- 其他嵌入式設備和邊緣設備

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Advanced Micro Devices Inc.

- Intel Corporation

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- Imagination Technologies Ltd.

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Gigabyte Technology Co. Ltd.

- Colorful Technology Co. Ltd.

- Zotac Technology Ltd.

- Palit Microsystems Ltd.

- Sapphire Technology Ltd.

- InnoVision Multimedia Ltd.

- Ineda Systems Pvt. Ltd.

- Saankhya Labs Pvt. Ltd.

- ARM Ltd.

- Xilinx India Technology Services Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india gPU market size is expected to increase from USD 4.93 billion in 2025 to USD 5.72 billion in 2026 and reach USD 13.97 billion by 2031, growing at a CAGR of 19.55% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, and Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded, and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

India GPU Market Trends and Insights

Growing Cloud Service Provider Investments in Indian Hyperscale DCs

Hyperscale operators now treat India as a strategic compute region rather than a cost-arbitrage outpost. Microsoft's multi-region rollout features NVIDIA H100 and forthcoming Blackwell GPUs, while Google is expanding TPU- and GPU-accelerated infrastructure for enterprise AI workloads. Domestic provider Yotta Infrastructure is deploying more than 32,000 H100 units with an upgrade path to Blackwell Ultra, signaling a pivot from general-purpose cloud to inference-optimized clusters. The IndiaAI Mission sets aside public funding for 34,000 sovereign GPUs, reducing reliance on foreign clouds. Collectively, these moves underpin sustained double-digit growth for the India GPU market.

Proliferation of AI Workloads in Edge Devices

Edge inference has graduated from proof-of-concept to volume rollout across retail analytics, industrial vision, and public safety. Qualcomm's Snapdragon 8 Elite Gen 5 delivers a 23% graphics uplift, enabling on-device generative AI for flagship smartphones, while MediaTek's Dimensity 9500s brings ray-tracing hardware to mid-premium tiers. Tier-2 smart-city projects leverage edge GPU nodes to meet sub-50 ms latency budgets. The National Payments Corporation of India uses GPU-accelerated models to screen 12 billion monthly payment transactions, demonstrating mission-critical edge inference at a national scale.

Chronic Import Dependence for Advanced Nodes

India lacks sub-28 nm fabrication, so datacenter GPUs manufactured on 4 nm and below must be imported. GPUs represent roughly 90% of AI server bills of materials, making supply allocation decisions by overseas foundries a critical bottleneck. Long lead times, coupled with limited local high-bandwidth memory packaging, amplify vulnerability to geopolitical shocks.

Other drivers and restraints analyzed in the detailed report include:

- Government PLI Schemes for Semiconductor Manufacturing

- Rapid Expansion of India's Gaming Ecosystem

- Global Supply Chain Disruptions Causing Allocation Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs accounted for 66.18% of the India GPU market share in 2025. Servers, gaming PCs, and professional workstations have gravitated to dedicated silicon that provides higher memory bandwidth and specialized tensor math. Large-scale installations, such as Yotta's 32,000-plus H100 cluster, illustrate enterprise appetite for top-bin accelerators. Enthusiast gamers are migrating from GTX 1060-class hardware to RTX 50-series cards, aided by board partners that bundle factory overclocks and extended warranties. On the professional side, CAD and media-creation suites exploit driver-certified Quadro and Radeon Pro lines, supporting higher average selling prices.

Integrated GPUs, holding the remaining 33.82%, dominate unit shipments in mainstream laptops and smartphones, where thermals and bill-of-materials ceilings are stringent. Intel Iris Xe and AMD Radeon 700M graphics meet everyday productivity and light creative workloads. In smartphones, Qualcomm Adreno and MediaTek Immortalis cores now handle on-device diffusion models and NPU-assisted photography. The India GPU market size for integrated silicon will continue to climb in absolute terms, although its slice of revenue tilts toward discrete devices because of rising datacenter volumes.

List of Companies Covered in this Report:

- Advanced Micro Devices Inc.

- Intel Corporation

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- Imagination Technologies Ltd.

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Gigabyte Technology Co. Ltd.

- Colorful Technology Co. Ltd.

- Zotac Technology Ltd.

- Palit Microsystems Ltd.

- Sapphire Technology Ltd.

- InnoVision Multimedia Ltd.

- Ineda Systems Pvt. Ltd.

- Saankhya Labs Pvt. Ltd.

- ARM Ltd.

- Xilinx India Technology Services Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of AI Workloads in Edge Devices

- 4.2.2 Rapid Expansion of India's Gaming Ecosystem

- 4.2.3 Government PLI Schemes for Semiconductor Manufacturing

- 4.2.4 Rising Demand for High-Performance Computing in BFSI

- 4.2.5 Data-Driven Automotive ADAS Adoption

- 4.2.6 Growing Cloud Service Provider Investments in Indian Hyperscale DCs

- 4.3 Market Restraints

- 4.3.1 Chronic Import Dependence for Advanced Nodes

- 4.3.2 Electricity Cost Volatility Impacting Datacenter TCO

- 4.3.3 Limited Domestic IP for GPU Design Talent Pool

- 4.3.4 Global Supply Chain Disruptions Causing Allocation Shortages

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Advanced Micro Devices Inc.

- 6.4.2 Intel Corporation

- 6.4.3 NVIDIA Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Imagination Technologies Ltd.

- 6.4.6 Samsung Electronics Co. Ltd.

- 6.4.7 MediaTek Inc.

- 6.4.8 Apple Inc.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Micro-Star International Co. Ltd.

- 6.4.11 Gigabyte Technology Co. Ltd.

- 6.4.12 Colorful Technology Co. Ltd.

- 6.4.13 Zotac Technology Ltd.

- 6.4.14 Palit Microsystems Ltd.

- 6.4.15 Sapphire Technology Ltd.

- 6.4.16 InnoVision Multimedia Ltd.

- 6.4.17 Ineda Systems Pvt. Ltd.

- 6.4.18 Saankhya Labs Pvt. Ltd.

- 6.4.19 ARM Ltd.

- 6.4.20 Xilinx India Technology Services Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析 東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)