|

市場調查報告書

商品編碼

2065611

歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Integrated GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

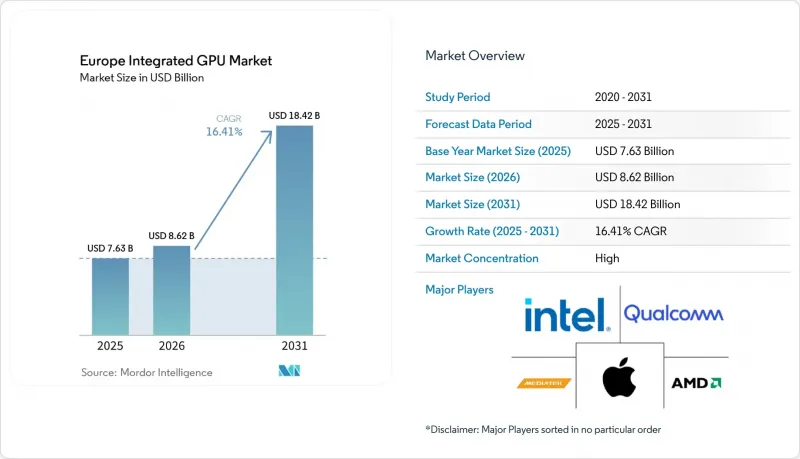

根據 Mordor Intelligence 預測,歐洲整合 GPU 市場規模預計將在 2025 年達到 76.3 億美元,2026 年達到 86.2 億美元,到 2031 年達到 184.2 億美元,2026 年至 2031 年的複合年成長率為 16.41%。

本報告按設備類別(桌上型電腦和筆記型電腦處理器、行動SoC(智慧型手機和平板電腦)、嵌入式和工業SoC以及具有整合式顯示卡的伺服器和資料中心處理器)、效能等級(入門級(50美元以下)、主流級(50-150美元)、高效能級(150-300美元)及其他)和地區進行細分。市場預測以價值(美元)表示。

歐洲整合GPU市場的趨勢與洞察

人工智慧筆記型電腦的日益普及正在重塑對整合顯示卡的需求。

隨著企業尋求能夠在整個更新周期內支援本地人工智慧功能的系統,人工智慧筆記型電腦已成為歐洲整合顯示卡市場的一個獨立購買類別。在2026年國際消費電子展(CES)上,英特爾發布了Panther Lake Core Ultra Series 3處理器,該處理器配備多達12個Xe3 GPU核心和一個50 TOPS的NPU。這一平台清晰地表明,在客戶端運算的討論中,圖形處理和人工智慧如今已同等重要。實際上,NPU和整合式顯示卡(iGPU)現在共同承擔日常商業應用中的混合工作負載,例如影片品質增強、背景分割和文件處理。這提高了筆記型電腦的最低圖形配置要求,而筆記型電腦曾經被視為標準的辦公設備。因此,歐洲整合顯示卡市場不僅受益於銷售量的成長,也受益於需求結構的增強,因為人工智慧筆記型電腦正從利基市場轉向主流企業需求。

Windows 11 更新和 Windows 10 支援的終止將加速 PC 硬體的結構性更新。

Windows 10 於 2025 年 10 月 14 日正式停止支持,這直接導致歐洲眾多無法滿足 Windows 11 最低安全要求(例如 TPM 2.0 和安全啟動)的設備面臨硬體升級壓力。這對歐洲整合顯示卡市場影響巨大,因為與典型的作業系統遷移相比,整合顯示卡的升級主要由硬體主導而非軟體主導,因此其處理器出貨量的成長幅度將更為顯著。許多中小企業推遲了 2024 年的升級計劃,這意味著相當一部分現有設備只能透過完全更換才能完成遷移。此外,消費者越來越傾向選擇支援人工智慧的平台,而不是僅僅滿足最低配置要求的系統,這進一步提升了主流和高效能產品的價值。因此,歐洲整合顯示卡市場的需求激增幅度遠超以往 Windows 系統停止支援事件所預期的水準。

來自人工智慧加速器和高階行動SoC在先進節點市場的競爭正在限制供應。

歐洲整合GPU市場仰賴先進晶圓代工廠的產能。這是因為高階筆記型電腦和智慧型手機需要採用最先進的製程工藝,才能在低功耗限制下實現高性能圖形處理。由於人工智慧加速器和高階行動處理器都在爭奪相同的3nm-4nm製程產能,這造成了結構性的供應問題。對於AMD、聯發科和高通等廠商而言,這個問題尤其關鍵,因為這些公司實際上是在晶圓投入方面與自身高利潤產品線競爭。因此,下一代產品的發布可能會延遲,價格可能會飆升,面向歐洲OEM客戶的大規模生產供應可能會受到限制。因此,儘管終端用戶需求強勁,但歐洲整合GPU市場短期內仍將面臨嚴重的成長放緩。

細分市場分析

2025年,行動SoC佔據了歐洲整合GPU市場49.45%的佔有率,成為該地區銷售量構成中最大的設備類別。這一主導地位反映了高階智慧型手機在歐洲的高滲透率,以及中高階和旗艦級Android設備持續向更強大的整合式顯示卡轉型,這些顯示卡具備硬體射線追蹤、快速媒體引擎和強大的裝置端AI支援。三星Exynos 1680和聯發科天璣9500系列表明,歐洲整合GPU產業的行動領域正在超越單純依靠銷售成長,轉向透過先進製程節點提升圖形效能。 2025年至2026年,桌上型電腦和筆記型電腦處理器仍將維持第二大市場佔有率,這主要得益於Windows 11更新周期帶來的企業筆記型電腦和桌上型電腦持續的更換需求。

預計到2031年,整合顯示卡的伺服器和資料中心處理器將以16.97%的複合年成長率成長,成為歐洲整合GPU市場規模展望中成長最快的設備類別。歐洲雲端服務供應商和企業資料中心越來越傾向於選擇無需專用加速器即可處理運算、視訊轉碼、輕量級推理和視覺化的整合處理器。英特爾計畫於2026年上半年發布的「Xeon 6+ Clearwater Forest」預覽版,展示了先進節點整合顯示卡功能正以驚人的速度引入伺服器級平台,從而推動了這一轉變。嵌入式和工業SoC雖然尺寸較小,但隨著邊緣AI在德國、法國和義大利的工廠和工業設備中不斷擴展,其戰略重要性日益凸顯。恩智浦半導體的i.MX 93W以及瑞薩電子對Irida Labs的收購表明,歐洲整合GPU產業也在向嵌入式平台轉型,圖形、AI、連接性和軟體差異化在客戶決策中變得越來越重要。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 停止對 Windows 11 Refresh 和 Windows 10 的支持

- 人工智慧筆記型電腦的普及率不斷提高

- 輕薄設備對低功耗圖形的需求

- 向高階智慧型手機SoC中更高效能的圖形處理能力和先進的製程節點過渡。

- 歐盟關於生態設計和能源標籤檢視的法規正在鼓勵低能耗設計。

- 工業邊緣人工智慧的日益普及正在推動對嵌入式SoC的需求。

- 市場限制因素

- AI加速器與高階行動SoC之間的先進節點競爭

- 記憶體和儲存成本的不斷上漲給我們的升級預算帶來了壓力。

- 互聯嵌入式平台遵守《網路彈性法案》的負擔。

- 高階內容創作和遊戲工作負載持續推動獨立顯示卡的需求。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過裝置

- 桌上型電腦和筆記型電腦處理器

- 行動SoC(智慧型手機和平板電腦)

- 嵌入式和工業級SoC

- 伺服器和資料中心處理器,整合顯示卡

- 按績效水準

- 入門級(50美元以下)

- 主流(50-150美元)

- 性能範圍(150-300美元)

- 高性能(超過 300 美元)

- 國家

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Intel Corporation

- Advanced Micro Devices, Inc.

- QUALCOMM Incorporated

- Apple Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- Arm Limited

- Imagination Technologies Limited

- NXP Semiconductors NV

- STMicroelectronics NV

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- NVIDIA Corporation

- Broadcom Inc.

- UNISOC(Shanghai)Technologies Co., Ltd.

- Rockchip Electronics Co., Ltd.

- Amlogic Co., Ltd.

- Allwinner Technology Co., Ltd.

- Google LLC

- Socionext Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe integrated GPU market size is projected to be USD 7.63 billion in 2025, USD 8.62 billion in 2026, and reach USD 18.42 billion by 2031, growing at a CAGR of 16.41% from 2026 to 2031.

This report is Segmented by Device Category (Desktop and Laptop Processors, Mobile SoCs (Smartphones and Tablets), Embedded and Industrial SoCs, and Server and Data Center Processors With Integrated Graphics), Performance Tier (Entry-Level (Less Than USD 50), Mainstream (USD 50-USD 150), Performance (USD 150-USD 300), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Integrated GPU Market Trends and Insights

Rising AI-Capable Notebook Penetration Reshapes Integrated GPU Demand Mix

AI-capable notebooks have become a defined buying category across the Europe integrated GPU market as enterprises look for systems that can support local AI features over a full replacement cycle. Intel launched Panther Lake Core Ultra Series 3 at CES 2026 with up to 12 Xe3 GPU cores and a 50 TOPS NPU, making the platform a clear signal that graphics and AI now sit together in the same client computing conversation. The practical change is that the NPU and iGPU now share mixed workloads such as video enhancement, background segmentation, and document processing in everyday business use. That raises the graphics specification floor even in notebooks that were once treated as standard office machines. The Europe integrated GPU market is therefore benefiting not only from more units, but also from a stronger mix as AI-ready notebooks move from a niche class into mainstream enterprise demand.

Windows 11 Refresh and Windows 10 Retirement Drive Structural PC Hardware Replacement

Windows 10 reached its official end of support on October 14, 2025, and that created direct hardware replacement pressure across European device fleets that did not meet Windows 11 security minimums such as TPM 2.0 and Secure Boot. This matters for the Europe integrated GPU market because the refresh is hardware-led rather than software-led, which lifts processor shipments more strongly than a normal operating system transition. Many small and medium enterprises delayed upgrades through 2024, so a meaningful share of installed devices could not move forward without full replacement. Buyers are also tending to choose AI-capable platforms instead of minimum-spec compliant systems, and that supports stronger value across the Mainstream and Performance tiers. The Europe integrated GPU market is therefore seeing a larger uplift than earlier Windows sunsets would have suggested.

Advanced-Node Supply Competition From AI Accelerators and Premium Mobile SoCs Constrains Supply

The Europe integrated GPU market depends on advanced foundry capacity because premium notebooks and smartphones now need leading-edge nodes to deliver higher graphics capability within lower power limits. This creates a structural supply problem because AI accelerators and premium mobile processors are chasing the same 3nm-4nm class capacity. The issue is important for vendors such as AMD, MediaTek, and Qualcomm because they are effectively competing against their own higher-margin product lines for wafer starts. That can delay next-generation launches, raise pricing, or limit supply at the volume tier for European OEM customers. The Europe integrated GPU market therefore faces a real near-term brake even when end-user demand remains healthy.

Other drivers and restraints analyzed in the detailed report include:

- Premium Smartphone SoC Migration to Richer Graphics and Advanced Nodes Expands Mobile iGPU Value

- Demand for Power-Efficient Graphics in Thin-and-Light Devices Elevates Advanced-Node iGPU Design Spend

- High-End Creator and Gaming Workloads Sustain Discrete GPU Demand at the Top End

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile SoCs held 49.45% of the Europe integrated GPU market share in 2025, making them the largest device category across the region's revenue mix. Their lead reflects Europe's dense premium smartphone base and the ongoing move of upper-mid and flagship Android devices toward richer integrated graphics blocks with hardware ray tracing, faster media engines, and stronger on-device AI support. Samsung's Exynos 1680 and MediaTek's Dimensity 9500 family show how the mobile layer of the Europe integrated GPU industry is moving toward higher graphics value at advanced nodes rather than relying only on unit growth. Desktop and Laptop Processors remained the second-largest category because the Windows 11 refresh cycle sustained replacement demand across enterprise notebooks and desktops in 2025 and into 2026.

Server and Data Center Processors with Integrated Graphics are projected to expand at a CAGR of 16.97% through 2031, which makes them the fastest-growing device category in the Europe integrated GPU market size outlook. European cloud operators and enterprise data centers are increasingly looking at unified processors that can handle compute, video transcoding, lightweight inference, and visualization without a dedicated add-in accelerator in every use case. Intel's preview of Xeon 6+ Clearwater Forest, expected in the first half of 2026, illustrates how advanced-node integrated graphics capability is moving into server-grade platforms at a speed that supports this shift. Embedded and Industrial SoCs are smaller in absolute value, but they are gaining strategic importance as edge AI expands in factories and industrial equipment across Germany, France, and Italy. NXP's i.MX 93W and Renesas' acquisition of Irida Labs show that the Europe integrated GPU industry is also shifting toward embedded platforms where graphics, AI, connectivity, and software differentiation now matter together in customer decisions.

List of Companies Covered in this Report:

- Intel Corporation

- Advanced Micro Devices, Inc.

- QUALCOMM Incorporated

- Apple Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- Arm Limited

- Imagination Technologies Limited

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- NVIDIA Corporation

- Broadcom Inc.

- UNISOC (Shanghai) Technologies Co., Ltd.

- Rockchip Electronics Co., Ltd.

- Amlogic Co., Ltd.

- Allwinner Technology Co., Ltd.

- Google LLC

- Socionext Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Windows 11 Refresh and Windows 10 Retirement

- 4.2.2 Rising AI-Capable Notebook Penetration

- 4.2.3 Demand for Power-Efficient Graphics in Thin-and-Light Devices

- 4.2.4 Premium Smartphone SoC Migration to Richer Graphics and Advanced Nodes

- 4.2.5 EU Ecodesign and Energy Labeling Pressure Favoring Lower-Power Designs

- 4.2.6 Industrial Edge AI Rollouts Expanding Embedded SoC Demand

- 4.3 Market Restraints

- 4.3.1 Advanced-Node Supply Competition From AI Accelerators and Premium Mobile SoCs

- 4.3.2 Memory and Storage Cost Inflation Limiting Replacement Budgets

- 4.3.3 Cyber Resilience Act Compliance Burden for Connected Embedded Platforms

- 4.3.4 High-End Creator and Gaming Workloads Still Pulling Demand Toward Discrete GPUs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Category

- 5.1.1 Desktop and Laptop Processors

- 5.1.2 Mobile SoCs (Smartphones and Tablets)

- 5.1.3 Embedded and Industrial SoCs

- 5.1.4 Server and Data Center Processors with Integrated Graphics

- 5.2 By Performance Tier

- 5.2.1 Entry-Level (Less than USD 50)

- 5.2.2 Mainstream (USD 50 - USD 150)

- 5.2.3 Performance (USD 150 - USD 300)

- 5.2.4 High-Performance (Greater than USD 300)

- 5.3 By Country

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 QUALCOMM Incorporated

- 6.4.4 Apple Inc.

- 6.4.5 MediaTek Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Arm Limited

- 6.4.8 Imagination Technologies Limited

- 6.4.9 NXP Semiconductors N.V.

- 6.4.10 STMicroelectronics N.V.

- 6.4.11 Texas Instruments Incorporated

- 6.4.12 Renesas Electronics Corporation

- 6.4.13 NVIDIA Corporation

- 6.4.14 Broadcom Inc.

- 6.4.15 UNISOC (Shanghai) Technologies Co., Ltd.

- 6.4.16 Rockchip Electronics Co., Ltd.

- 6.4.17 Amlogic Co., Ltd.

- 6.4.18 Allwinner Technology Co., Ltd.

- 6.4.19 Google LLC

- 6.4.20 Socionext Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析 東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)