|

市場調查報告書

商品編碼

2065493

東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Southeast Asia GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

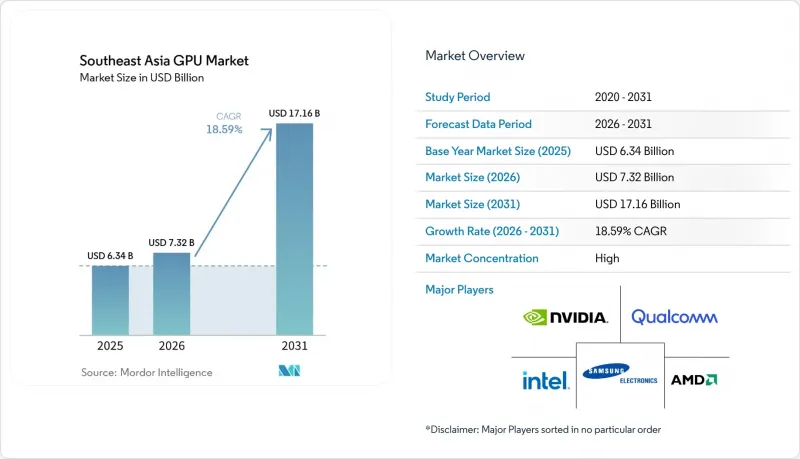

據 Mordor Intelligence 稱,東南亞 GPU 市場預計將從 2026 年的 73.2 億美元成長到 2031 年的 171.6 億美元,2026 年至 2031 年的複合年成長率為 18.59%。

本報告按整合類型(整合GPU、獨立GPU)和裝置應用(行動裝置/平板電腦、PC/工作站、伺服器/資料中心加速器、遊戲機/掌上型電腦、汽車/ADAS以及其他嵌入式/邊緣裝置)進行分類。市場預測以美元計價。

東南亞GPU市場趨勢與洞察

資料中心對高效能運算的需求日益成長

為了滿足資料駐留要求並降低生成式人工智慧推理的延遲,超大規模資料中心業者正開始將計算叢集在地化。微軟 Azure 將於 2025 年在馬來西亞和印尼部署 ND GB200-v6 實例,同年,Google雲端也在曼谷推出了配備 H100 GPU 的 A3 節點。楊忠禮電力國際已在柔佛州啟動一座 500 兆瓦人工智慧園區的建設,預計將於 2027 年完工。區域託管服務提供者也在對其設施維修,以引入液冷系統。這些發展正推動東南亞從以新加坡為中心的「輻射點」轉型為一流的推理中心。

雲端遊戲和線上電子競技的快速發展

光纖到府 (FTTH) 的普及和 5G 網路在全國範圍內的覆蓋,使得訂閱制雲端遊戲服務能夠實現低於 20 毫秒的遊戲響應速度。 Radian Arc 與 Singtel-Razer 合作的試點計畫在 2024 年至 2025 年間從試用階段過渡到商業服務,這表明每月低於 10 美元的定價對於業務規模至關重要。隨著電子競技被列入 2025 年東南亞運動會的正式比賽項目,公共部門對配備 GPU 的訓練中心的投資也隨之增加,導致泰國和菲律賓的工作站級顯示卡短期銷量激增。

全球GPU供應鏈中斷與晶片短缺

2025年全年,HBM3E顯存持續短缺,迫使NVIDIA和AMD限制旗艦級加速器的供應,僅向簽訂多年合約的超大規模資料中心業者公司供貨。向區域雲端服務供應商的交付時間超過六個月,台積電CoWoS封裝產能利用率超過90%。美國出口限制將2025年至2027年向印尼出口的資料中心GPU數量上限設定為5萬顆,迫使企業優先考慮推理而非訓練。

細分市場分析

到2025年,獨立GPU將佔據東南亞GPU市場67.85%的佔有率。圍繞NVIDIA H200和AMD MI325X加速器建構的資料中心叢集進一步鞏固了這一地位。隨著超大規模資料中心超大規模資料中心業者簽署多年供貨契約,預計到2031年,東南亞獨立GPU市場將以19.11%的複合年成長率成長。楊忠禮電力國際計畫僅在其位於柔佛州的500兆瓦工廠就安裝數萬張GPU卡,而沃爾沃等汽車OEM廠商正在整合雙驅動AGX Orin顯示卡,每輛車可提供254 TOPS的運算能力。

整合顯示卡雖然目前規模仍然較小,但在智慧型手機和人工智慧PC出貨量的推動下,正經歷著快速成長。聯發科驍龍9500系列顯示卡整合了具備硬體射線追蹤功能的Immortalis-G925核心,正縮小與入門級獨立顯示卡的效能差距。高通驍龍8 Gen 3和聯發科驍龍8500在熱門手機遊戲中均能保持60幀的流暢運行,這表明整合晶片現在也能處理以往只有擴充卡才能勝任的工作負載。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 雲端遊戲和線上電子競技的快速發展

- 資料中心對高效能運算的需求日益成長

- 東南亞行動遊戲生態系統的發展

- AAA級PC和主機遊戲對圖形效能的要求越來越高。

- 政府對國內半導體封裝和測試的激勵措施

- 拓展人工智慧驅動的社群電商內容創作

- 市場限制因素

- 全球GPU供應鏈中斷與半導體短缺

- 平均售價上漲限制了入門車型的普及。

- 新興國家資料中心對能源成本的敏感性

- 主要市場對加密貨幣挖礦的監管

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按類型整合

- 整合顯示卡(iGPU)

- 獨立GPU(dGPU)

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- ARM Holdings plc

- Imagination Technologies Limited

- Apple Inc.

- Huawei Technologies Co., Ltd.

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

- Acer Incorporated

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- EVGA Corporation

- Zotac Technology Limited

- Colorful Technology Company Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the southeast asia gPU market size is expected to increase from USD 7.32 billion in 2026 to USD 17.16 billion by 2031, growing at a CAGR of 18.59% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs), and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

Southeast Asia GPU Market Trends and Insights

Rising Demand for High-Performance Computing in Data Centers

Hyperscalers have started localizing compute clusters to satisfy data-residency mandates and reduce latency for generative AI inference. Microsoft Azure rolled out ND GB200-v6 instances in Malaysia and Indonesia in 2025, while Google Cloud launched a Bangkok region with A3 nodes powered by H100 GPUs the same year. YTL Power International broke ground on a 500 MW AI campus in Johor, scheduled for 2027 completion, and regional colocation providers are retrofitting halls with liquid cooling. These moves establish Southeast Asia as a first-tier inference hub rather than a spoke served out of Singapore.

Rapid Adoption of Cloud Gaming and Online Esports

Fiber-to-the-home penetration and nationwide 5G coverage have enabled sub-20 ms gameplay for subscription-based cloud gaming services. Radian Arc and Singtel-Razer pilots moved from trial to commercial launch during 2024-2025, with monthly pricing under USD 10 proving critical for scale. Esports' inclusion as a medal event in the Southeast Asian Games 2025 triggered public-sector investment in GPU-equipped training centers, spurring near-term purchases of workstation-class cards across Thailand and the Philippines.

Global GPU Supply Chain Disruptions and Chip Shortages

HBM3E memory remained constrained through 2025, compelling NVIDIA and AMD to ration flagship accelerators to hyperscalers on multi-year contracts. Lead times for regional cloud providers stretched beyond six months, and CoWoS packaging capacity at TSMC exceeded 90% utilization. U.S. export controls imposed a 50,000-unit ceiling on datacenter GPUs shipped to Indonesia for 2025-2027, forcing enterprises to emphasize inference over training.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of AI-Powered Content Creation for Social Commerce

- Growth of Mobile Gaming Ecosystem in Southeast Asia

- Rising Average Selling Prices Limiting Entry-Level Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete units controlled 67.85% of the Southeast Asia GPU market in 2025, a position amplified by datacenter clusters built around NVIDIA H200 and AMD MI325X accelerators. The Southeast Asia GPU market size for discrete units is on track to expand at a 19.11% CAGR through 2031 as hyperscalers lock in multi-year supply agreements. YTL Power International's 500 MW Johor facility alone plans to host tens of thousands of cards, while automotive OEMs such as Volvo integrate dual Drive AGX Orin boards that deliver 254 TOPS per vehicle.

Smaller but rising, integrated GPUs ride smartphone and AI PC shipments. MediaTek's 9500s embeds an Immortalis-G925 core with hardware ray tracing, trimming the gap with entry-level discrete boards. Qualcomm's Snapdragon 8 Gen 3 and MediaTek's 8500 sustain 60 fps on popular mobile titles, underscoring that integrated silicon now handles workloads once reserved for add-in cards.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- ARM Holdings plc

- Imagination Technologies Limited

- Apple Inc.

- Huawei Technologies Co., Ltd.

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

- Acer Incorporated

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- EVGA Corporation

- Zotac Technology Limited

- Colorful Technology Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud Gaming and Online Esports

- 4.2.2 Rising Demand for High-Performance Computing in Data Centers

- 4.2.3 Growth of Mobile Gaming Ecosystem in Southeast Asia

- 4.2.4 Increasing Graphics Requirements for AAA PC and Console Titles

- 4.2.5 Government Incentives for Local Semiconductor Packaging and Testing

- 4.2.6 Expansion of AI-Powered Content Creation for Social Commerce

- 4.3 Market Restraints

- 4.3.1 Global GPU Supply Chain Disruptions and Chip Shortages

- 4.3.2 Rising Average Selling Prices Limiting Entry-Level Adoption

- 4.3.3 Energy Cost Sensitivity of Emerging Country Data Centers

- 4.3.4 Regulatory Scrutiny on Cryptocurrency Mining in Key Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Threat of New Entrants

- 4.8.3 Threat of Substitutes

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Bargaining Power of Buyers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 MediaTek Inc.

- 6.4.7 ARM Holdings plc

- 6.4.8 Imagination Technologies Limited

- 6.4.9 Apple Inc.

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Lenovo Group Limited

- 6.4.12 ASUSTeK Computer Inc.

- 6.4.13 Micro-Star International Co., Ltd.

- 6.4.14 Gigabyte Technology Co., Ltd.

- 6.4.15 Acer Incorporated

- 6.4.16 Dell Technologies Inc.

- 6.4.17 Hewlett Packard Enterprise Company

- 6.4.18 EVGA Corporation

- 6.4.19 Zotac Technology Limited

- 6.4.20 Colorful Technology Company Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析 超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)