|

市場調查報告書

商品編碼

2064462

德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Germany GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

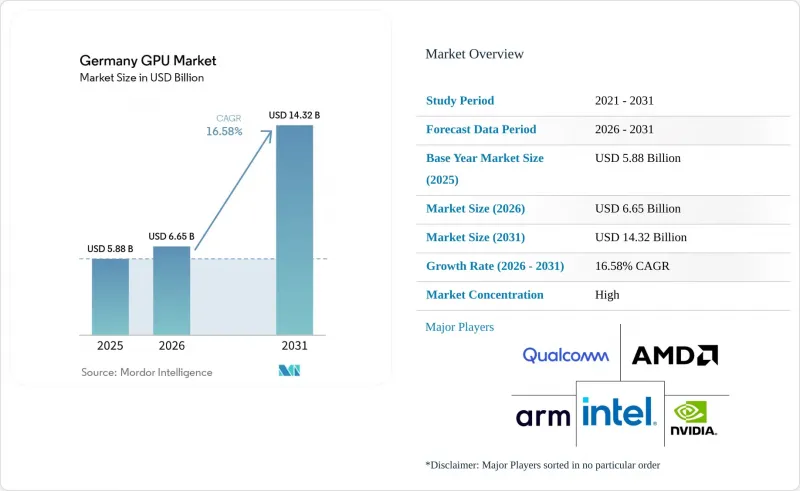

根據 Mordor Intelligence 預測,德國 GPU 市場規模將從 2025 年的 58.8 億美元成長到 2026 年的 66.5 億美元,到 2031 年達到 143.2 億美元,2026 年至 2031 年的複合年成長率預計為 16.58%。

本報告按整合類型(整合GPU、獨立GPU)和裝置應用(行動裝置和平板電腦、PC和工作站、伺服器和資料中心加速器、遊戲主機和掌上型遊戲機、汽車/ADAS以及其他嵌入式和邊緣裝置)進行細分。市場預測以美元計價。

德國GPU市場的趨勢與洞察

人工智慧和高效能運算工作負載的快速成長

為了遵守歐盟人工智慧法規並避免來自歐盟以外的資料請求,德國企業正優先部署本地GPU叢集。德國電信位於慕尼黑的工業人工智慧雲端將於2026年2月投入運作,該雲端部署了1萬塊NVIDIA Blackwell GPU,領先包括西門子和安永在內的主要租戶售出了超過三分之一的容量。施瓦茨集團已撥款110億歐元(約126.5億美元)用於國家人工智慧基礎建設,而來自IPCEI微電子計畫的政府補貼已使資本成本降低了20%至30%。高斯超級運算中心內的研究中心目前正在同步升級到最新的NVIDIA和AMD加速器,凸顯了高頻寬記憶體設計在氣候建模、藥物研發和材料科學領域的重要性。

電子競技的擴張正在推動高階遊戲GPU的成長。

德國將電子競技認定為正式體育項目,確保了場館和訓練設施的公共資金投入,並使GPU密集型基礎設施的建設制度化。超過4500萬活躍玩家推動支援240Hz輸出和即時定序的獨立顯示卡的持續更換。 G2 esports、柏林國際遊戲和SK Gaming等職業戰隊經營配備NVIDIA GeForce RTX 5080和AMD Radeon RX 9070 XT顯示卡的訓練中心,實現了低於10毫秒的延遲。直播主播擴大使用雙GPU配置來編碼4K60影片,同時保持144幀/秒或更高的影格速率,這進一步鞏固了高階獨立顯卡市場。

半導體供應鏈中斷

台積電的CoWoS先進封裝生產線已全部排滿,導致GPU前置作業時間延長至12個月以上,並推遲了原定於2026年初在德國的部署。 HBM3e模組的供不應求推高了現貨價格,迫使各公司調整與超大規模資料中心業者、汽車專案和國家人工智慧叢集之間的配額。儘管歐盟晶片立法承諾投資430億歐元用於國內晶圓廠建設,但新工廠預計要到2027年或更晚才能投入運作,這意味著供應短缺在可預見的未來可能仍將持續。

細分市場分析

到2025年,獨立GPU將佔據德國GPU市場65.73%的佔有率,並繼續在大規模語言模型(LLM)訓練叢集中保持領先地位。德國電信在慕尼黑部署1萬塊GPU,以及施瓦茨集團在多個地點擴展GPU部署,都為滿足歐盟資料主權法規的要求,推動了德國獨立加速器市場的蓬勃發展。同時,整合GPU在功耗受限的汽車駕駛座以及高通、AMD和英特爾等廠商推出的配備Copilot+技術的筆記型電腦中,市佔率正穩定成長,這些產品的SoC晶片單晶片運算能力可達80 TOPS。

遊戲和內容創作工作負載正在推動對獨立顯示卡的需求,因為發燒友們更重視更大的幀緩衝區和經過認證的驅動程式。然而,在持續高負載下,整合式顯示卡會因過熱而降頻,從而降低實際吞吐量。雖然整合式顯示卡在能耗有限的場景下表現出色,但獨立顯示卡在長達數小時的速率定序序列和擁有70億參數模型的AI推理中仍然保持著效能優勢。

其他福利

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧和高效能運算工作負載的快速成長

- 電子競技的擴張正在推動高階遊戲GPU的成長。

- 汽車製造商採用ADAS視覺化技術

- 航太和國防領域的模擬工作負載

- 可再生能源的數位雙胞胎模擬

- 德國對半導體智慧財產權(IP)研發的稅收優惠

- 市場限制因素

- 半導體供應鏈中斷

- 獨立顯示卡平均售價上漲

- 資料中心硬體能源效率上限

- GPU軟體最佳化領域人才短缺

- 產業價值/價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型整合

- 整合顯示卡(iGPU)

- 獨立GPU(dGPU)

- 裝置應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Arm Ltd.

- Imagination Technologies Ltd.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Micro-Star International Co., Ltd.(MSI)

- Zotac Technology Limited

- Sapphire Technology Limited

- Tenstorrent, Inc.

- PowerColor(TUL Corporation)

- ASRock Inc.

- InnoVision Multimedia Ltd.(Inno3D)

- Matrox Electronic Systems Ltd.

- Huawei Technologies Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany gPU market size is expected to increase from USD 5.88 billion in 2025 to USD 6.65 billion in 2026 and reach USD 14.32 billion by 2031, growing at a CAGR of 16.58% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

Germany GPU Market Trends and Insights

Rapid Growth of AI and HPC Workloads

German enterprises are prioritizing on-premises GPU clusters to comply with the EU AI Act and avoid extraterritorial data requests. Deutsche Telekom's Industrial AI Cloud in Munich, operational since February 2026 with 10,000 NVIDIA Blackwell GPUs, has pre-sold more than one-third of its capacity to anchor tenants that include Siemens and EY. The Schwarz Group earmarked EUR 11 billion (USD 12.65 billion) for sovereign AI infrastructure, while national subsidies under the IPCEI Microelectronics program lower capital costs by 20-30%. Research centers inside the Gauss Center for Supercomputing are concurrently upgrading to the latest NVIDIA and AMD accelerators, underscoring how high-bandwidth-memory designs are now indispensable for climate modeling, drug discovery, and materials science.

Esports Expansion Driving High-End Gaming GPUs

Germany's recognition of esports as an official sport has unlocked public funding for arenas and training facilities, institutionalizing GPU-intensive infrastructure. More than 45 million active gamers drive steady refresh cycles for discrete graphics cards capable of 240 Hz output and real-time ray tracing. Professional teams, G2 Esports, Berlin International Gaming, and SK Gaming, run training centers equipped with NVIDIA GeForce RTX 5080 and AMD Radeon RX 9070 XT boards that deliver sub-10-millisecond latency. Streaming creators often use dual-GPU setups for 4K60 encoding while maintaining 144-plus frame rates, reinforcing the market for high-end add-in-boards.

Semiconductor Supply-Chain Disruptions

TSMC's fully booked CoWoS advanced-packaging lines extend GPU lead times beyond 12 months, delaying German deployments slated for early 2026. Shortfalls in HBM3e modules raise spot prices and compel enterprises to ration allocations among hyperscaler contracts, automotive projects, and sovereign AI clusters. Although the EU Chips Act commits EUR 43 billion to onshore fabs, new facilities will not come online before 2027, leaving near-term supply tight.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Adoption for ADAS Visualization

- Aerospace and Defence Simulation Workloads

- Escalating Average Selling Prices of dGPUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs held 65.73% of the Germany GPU market share in 2025 and remain the workhorse for large-language-model training clusters. The Germany GPU market size for discrete accelerators benefits from Deutsche Telekom's 10,000-GPU Munich installation and the Schwarz Group's multi-site build-out, each designed to meet EU data-sovereignty rules. Integrated GPUs are nonetheless gaining ground in power-constrained automotive cockpits and Copilot+ laptops that rely on Qualcomm, AMD, and Intel SoCs delivering up to 80 TOPS on die.

Gaming and content-creation workloads reinforce discrete demand, as enthusiasts prioritize larger frame buffers and certified drivers. Conversely, sustained loads expose thermal throttling in integrated solutions, trimming real-world throughput. Integrated devices shine where energy budgets are fixed, yet for multi-hour ray-traced sequences or AI inference on 7-billion-parameter models, discrete cards still carry the performance edge.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Arm Ltd.

- Imagination Technologies Ltd.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- Zotac Technology Limited

- Sapphire Technology Limited

- Tenstorrent, Inc.

- PowerColor (TUL Corporation)

- ASRock Inc.

- InnoVision Multimedia Ltd. (Inno3D)

- Matrox Electronic Systems Ltd.

- Huawei Technologies Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth of AI and HPC Workloads

- 4.2.2 Esports Expansion Driving High-End Gaming GPUs

- 4.2.3 Automotive OEM Adoption for ADAS Visualization

- 4.2.4 Aerospace and Defence Simulation Workloads

- 4.2.5 Renewable-Energy Digital-Twin Simulations

- 4.2.6 German R&D Tax Incentives for Semiconductor IP

- 4.3 Market Restraints

- 4.3.1 Semiconductor Supply-Chain Disruptions

- 4.3.2 Escalating Average Selling Prices of dGPUs

- 4.3.3 Energy-Efficiency Caps on Datacentre Hardware

- 4.3.4 Talent Shortage in GPU Software Optimisation

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacentre Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Arm Ltd.

- 6.4.6 Imagination Technologies Ltd.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 Apple Inc.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Giga-Byte Technology Co., Ltd.

- 6.4.11 Micro-Star International Co., Ltd. (MSI)

- 6.4.12 Zotac Technology Limited

- 6.4.13 Sapphire Technology Limited

- 6.4.14 Tenstorrent, Inc.

- 6.4.15 PowerColor (TUL Corporation)

- 6.4.16 ASRock Inc.

- 6.4.17 InnoVision Multimedia Ltd. (Inno3D)

- 6.4.18 Matrox Electronic Systems Ltd.

- 6.4.19 Huawei Technologies Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析 東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)