|

市場調查報告書

商品編碼

2065755

印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

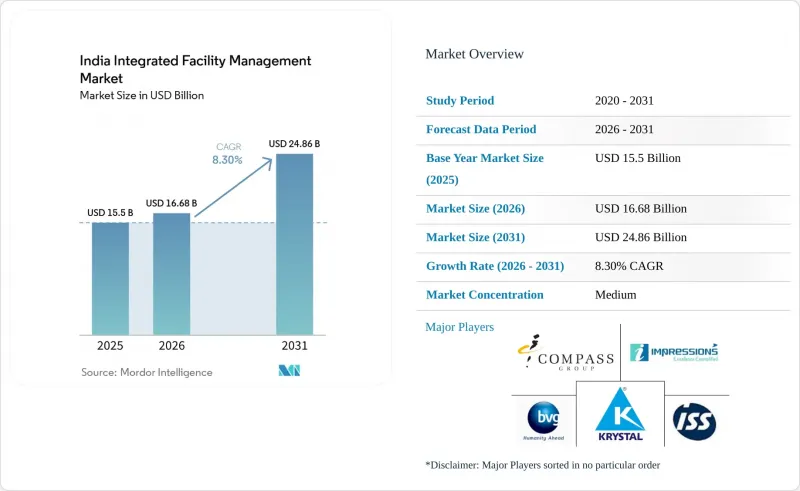

根據 Mordor Intelligence 預測,印度綜合設施管理市場規模預計將在 2025 年達到 155 億美元,2026 年達到 166.8 億美元,到 2031 年達到 248.6 億美元,2026 年至 2031 年的複合年成長率為 8.30%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和保全、清潔服務、餐飲服務等])和最終用戶(商業設施、飯店、公共機構和公共基礎設施、醫療設施等)進行分類。市場預測以美元計價。

印度整合性機構管理市場的趨勢與洞察

擴建甲級辦公室及綜合用途園區

預計2025年印度甲級辦公室市場將創下歷史新高,八大主要城市的淨吸收面積將達到6,140萬平方英尺,較去年同期成長25%。這直接反映了需要持續營運支援的專業管理物業的擴張。此外,預計到2026年,印度將佔亞太地區新增甲級辦公室供應量(6,130萬平方英尺)的40%,將確保印度綜合設施管理市場擁有蓬勃發展的新交易管道。供應構成與品質構成同樣重要。預計2026年新增供應量的80%將獲得綠色認證,將提高能源管理、用水監測、室內空氣品質控制和可審計報告等方面的服務標準。此外,在將辦公室、零售、旅館和食品服務等功能整合於單一管理環境下的綜合用途園區中,業主擴大指定單一的責任業者負責多個服務領域的營運。規模、技術要求和業主偏好等因素繼續有利於在硬體維修具備均衡專業知識的綜合服務提供商,從而推動印度綜合設施管理市場向更全面的IFM合約轉變。

將供應商納入綜合性和結果導向合約

印度的綜合設施管理市場正從依賴人員配置的合約模式轉向以服務等級協議 (SLA) 為導向的商業模式,這種模式衡量的是運轉率、能源效率、衛生品質和使用者體驗,而不僅僅是人力配置。在五個或更多服務類別中使用單一 IFM 合作夥伴的公司報告稱,供應商管理成本平均降低了 18%,這為採購團隊提供了直接成本節約和管理效率提升的基礎,從而促進了整合。這種轉變也提升了硬體維修管理的策略價值,因為暖通空調 (HVAC)運轉率、電氣系統可靠性和電力利用效率等技術指標在競標階段比許多軟性服務交付成果更容易檢驗和管理。機構投資者在印度辦公物業組合中的持股比例正在擴大,超過 3.8 億平方英尺的 A 級辦公空間具有 REIT 潛力。這些業主傾向於在其多元化的投資組合中應用統一的標準,而不是為每個地區設立單獨的營運結構。隨著這種模式的標準化,缺乏全國覆蓋範圍、數據系統和深厚合規能力的小規模公司,即使在區域層面保持價格競爭力,也可能在印度的綜合設施管理市場失去市場佔有率。

非正規供應商之間的主導競爭

來自非正規供應商的價格主導仍然是印度綜合設施管理市場最明顯的結構性阻礙。小規模供應商透過規避儲備基金、員工國家保險和最低工資義務,將價格定得比正規公司低15%到20%。這種壓力在清潔、家事和保全產業尤為突出,因為人事費用是這些產業的主要成本因素,而且採購者在採購時往往難以客觀評估服務品質。這個問題並不會隨著合約的簽訂而結束,因為此時顯現的價格差異會影響合約續約談判,從而給正規公司帶來新的壓力,迫使其在符合規定的服務交付模式下接受更低的價格。雖然印度勞動法的整合未來可能會改善競爭平衡,但各邦的執行情況仍不一致,法規效果也因地區而異。儘管如此,大型企業買家正逐漸從追求最低價格轉向考慮總擁有成本(TCO),這應該會逐步改善印度綜合設施管理市場的品質平衡。

細分市場分析

預計到2031年,硬設施管理(FM)將以9.47%的複合年成長率成長,超過整體市場成長率,成為印度綜合設施管理(IFM)市場服務領域最強勁的成長引擎。這項加速成長與A級資產技術密度的提高和資料中心的擴張密切相關,預計國內資料中心容量將從2025年底的約1.7吉瓦增至2030年的4吉瓦以上。這項擴張推動了對機電工程(MEP)服務、暖通空調(HVAC)管理、電力供應可靠性、備用電源支援和全天候技術人員編制配備的需求成長,而這些服務難以由一般服務提供者輕鬆滿足。隨著房地產投資信託基金(REIT)主導的投資組合和海灣合作理事會(GCC)園區從例行維護週期轉向生命週期規劃、更換管理和與資本支出(Capex)掛鉤的管理,資產管理服務的角色也在不斷擴大。

到2025年,軟性設施管理(Soft FM)將佔印度綜合設施管理(IFM)市場規模的67.19%,反映出印度商業、旅館、醫療和公共設施在清潔、餐飲、辦公室支援和保全方面需要龐大的勞動力。由於軟性設施管理直接影響日常入住體驗,且大規模租戶難以在其多地點物業組合中全面整合,因此該領域仍然是許多服務提供者的收入支柱。然而,綜合合約中的服務組成正在逐步改變。這是因為硬性服務每平方英尺的附加價值更高,且比勞動密集型軟性服務更容易根據服務等級協定(SLA)進行衡量。清潔服務正受益於機械化和機器人地面管理系統,而辦公室支援和保全功能則透過人工智慧監控和智慧訪客管理變得更加智慧化。這使得印度的綜合設施管理產業即使在競爭激烈的價格環境下也能維持服務品質。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴建甲級辦公室及綜合用途園區

- 供應商向綜合性、結果導向合約轉型

- 智慧建築和預測性維護的廣泛應用

- 永續性主導的能源、水和廢棄物最佳化需求。

- 將全球容量中心擴展到一級樞紐以外

- 資料中心和關鍵任務基礎設施的開發

- 市場限制因素

- 非正規供應商之間的價格競爭

- 技術工人外流和工資上漲

- 由於應收帳款回收延遲,導致營運資金短缺。

- 關鍵資產中公共產業的可靠性以及面臨水資源壓力的風險

- 產業價值鏈分析

- 技術分析

- 監理情勢

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全措施

- 其他硬設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬設施管理

- 最終用戶

- 商業

- 飯店業

- 機構和公共基礎設施

- 衛生保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BVG India Limited

- SIS Limited

- Sodexo India Services Private Limited

- Updater Services Limited

- Bluspring Enterprises Limited

- ISS Facility Services India Private Limited

- Krystal Integrated Services Limited

- CBRE South Asia Private Limited

- Jones Lang LaSalle Property Consultants(India)Private Limited

- Cushman & Wakefield India Private Limited

- Compass Group India(Compass Group PLC)

- Colliers International(India)Property Services Private Limited

- Knight Frank(India)Private Limited

- Tenon Facility Management India Private Limited

- Dusters Total Solutions Services Private Limited

- Property Solutions(India)Private Limited

- OCS India

- SMS Integrated Facility Services Private Limited

- Impressions Services Private Limited

- ServiceMax Facility Management Private Limited

- Supreme Facility Management Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the india integrated facility management market size is projected to be USD 15.5 billion in 2025, USD 16.68 billion in 2026, and reach USD 24.86 billion by 2031, growing at a CAGR of 8.30% from 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Integrated Facility Management Market Trends and Insights

Expansion Of Grade A Offices and Mixed-use Campuses

India's Grade A office market delivered its strongest year on record in 2025, with net absorption of 61.4 million sq ft across the top 8 cities, up 25% year over year, thereby directly expanding the professionally managed estate that requires continuous operating support. India is also expected to account for 40% of Asia-Pacific's 61.3 million sq ft of new Grade A office supply in 2026, which keeps the onboarding pipeline active for the India integrated facility management market. The quality mix matters as much as the quantity mix, because 80% of the new 2026 supply is expected to be green-certified, and that raises the service threshold for energy management, water monitoring, indoor air quality control, and audit-ready reporting. Mixed-use campuses are also bringing office, retail, hospitality, and food service functions into a single managed environment, which makes owners more likely to appoint one accountable operator across multiple service lines. This combination of scale, technical requirements, and ownership preference continues to favour integrated providers with balanced Hard FM and Soft FM depth, which supports the move toward fuller IFM contracts within the India integrated facility management market.

Vendor Consolidation into Integrated and Outcome-based Contracts

The India integrated facility management market is moving away from headcount-driven contracts and toward SLA-linked commercial models that measure uptime, energy efficiency, hygiene quality, and user experience rather than just labour deployment. Enterprises that use a single IFM partner across 5 or more service categories have reported an average 18% reduction in vendor management overhead, which gives procurement teams a direct cost and control argument for consolidation. This shift also lifts the strategic value of Hard FM, because technical metrics such as HVAC uptime, electrical reliability, and power usage performance are easier to verify and govern than many soft-service outputs at the bid stage. Institutional ownership is expanding across India's office stock, with more than 380 million sq ft of Grade A space carrying REIT potential, and these owners prefer consistent standards across distributed portfolios rather than separate local operating arrangements. As this model becomes standard, smaller firms without national reach, data systems, and compliance depth are likely to lose share in the India integrated facility management market even when they remain locally competitive on price.

Price-led Competition from Unorganized Vendors

Price-led competition from unorganized vendors remains the clearest structural brake on the India integrated facility management market, with smaller operators undercutting organized firms by 15% to 20% by bypassing Provident Fund, Employees' State Insurance, and minimum wage obligations. The pressure is strongest in cleaning, housekeeping, and security, where labour is the main cost input and output quality is often harder for buyers to benchmark objectively during procurement. The problem does not end at contract award, because the visible price gap then shapes renewal discussions and creates fresh pressure on organized firms to accept lower rates on compliant delivery models. India's labour code consolidation could improve the competitive balance over time, but state-level implementation remains uneven, and that keeps enforcement outcomes inconsistent across locations. Even so, large enterprise buyers are slowly shifting from lowest-bid decisions toward total-cost-of-ownership reviews, which should gradually improve the quality mix in the India integrated facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Wider Adoption of Smart Buildings and Predictive Maintenance

- Sustainability-led Demand for Energy, Water and Waste Optimization

- Skilled Workforce Attrition and Wage Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard facility management (FM) is forecast to expand at a 9.47% CAGR through 2031, which places it ahead of the overall growth rate and makes it the strongest service-side growth engine in the India integrated facility management (IFM) market. This acceleration is closely tied to higher technical density in Grade A assets and to data center expansion, with national capacity projected to rise from nearly 1.7 GW at the end of 2025 to more than 4 GW by FY30. That buildout increases demand for MEP services, HVAC management, electrical reliability, power backup support, and 24/7 technical staffing that general service operators cannot easily scale. Asset management services are also gaining a larger role as REIT-led portfolios and GCC campuses shift from periodic maintenance cycles toward lifecycle planning, replacement tracking, and capex-linked stewardship.

Soft FM held 67.19% share of the India IFM market size in 2025, which reflects the large labour base needed for cleaning, catering, office support, and security across India's commercial, hospitality, healthcare, and institutional estate. The segment remains the revenue anchor for many providers because it touches daily occupancy experience and is difficult for large occupiers to internalize across multi-site portfolios. Even so, the service mix inside integrated contracts is gradually shifting, because hard services carry higher value per square foot and support more measurable SLA outcomes than many labour-heavy soft lines. Cleaning is benefiting from mechanization and robotic floor care, while office support and security functions are being upgraded through AI-assisted surveillance and intelligent visitor management, which helps the India IFM industry defend service quality in a price-sensitive environment.

List of Companies Covered in this Report:

- BVG India Limited

- SIS Limited

- Sodexo India Services Private Limited

- Updater Services Limited

- Bluspring Enterprises Limited

- ISS Facility Services India Private Limited

- Krystal Integrated Services Limited

- CBRE South Asia Private Limited

- Jones Lang LaSalle Property Consultants (India) Private Limited

- Cushman & Wakefield India Private Limited

- Compass Group India (Compass Group PLC)

- Colliers International (India) Property Services Private Limited

- Knight Frank (India) Private Limited

- Tenon Facility Management India Private Limited

- Dusters Total Solutions Services Private Limited

- Property Solutions (India) Private Limited

- OCS India

- SMS Integrated Facility Services Private Limited

- Impressions Services Private Limited

- ServiceMax Facility Management Private Limited

- Supreme Facility Management Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Grade A Offices and Mixed-use Campuses

- 4.2.2 Vendor Consolidation Into Integrated and Outcome-based Contracts

- 4.2.3 Wider Adoption of Smart Buildings and Predictive Maintenance

- 4.2.4 Sustainability-led Demand for Energy, Water and Waste Optimization

- 4.2.5 Global Capability Centre Expansion Beyond Tier-1 Hubs

- 4.2.6 Data Centre and Mission-critical Infrastructure Buildout

- 4.3 Market Restraints

- 4.3.1 Price-led Competition From Unorganized Vendors

- 4.3.2 Skilled Workforce Attrition and Wage Inflation

- 4.3.3 Working-capital Stress From Delayed Receivables

- 4.3.4 Utility Reliability and Water-stress Exposure in Critical Assets

- 4.4 Industry Value Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BVG India Limited

- 6.4.2 SIS Limited

- 6.4.3 Sodexo India Services Private Limited

- 6.4.4 Updater Services Limited

- 6.4.5 Bluspring Enterprises Limited

- 6.4.6 ISS Facility Services India Private Limited

- 6.4.7 Krystal Integrated Services Limited

- 6.4.8 CBRE South Asia Private Limited

- 6.4.9 Jones Lang LaSalle Property Consultants (India) Private Limited

- 6.4.10 Cushman & Wakefield India Private Limited

- 6.4.11 Compass Group India (Compass Group PLC)

- 6.4.12 Colliers International (India) Property Services Private Limited

- 6.4.13 Knight Frank (India) Private Limited

- 6.4.14 Tenon Facility Management India Private Limited

- 6.4.15 Dusters Total Solutions Services Private Limited

- 6.4.16 Property Solutions (India) Private Limited

- 6.4.17 OCS India

- 6.4.18 SMS Integrated Facility Services Private Limited

- 6.4.19 Impressions Services Private Limited

- 6.4.20 ServiceMax Facility Management Private Limited

- 6.4.21 Supreme Facility Management Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)