|

市場調查報告書

商品編碼

2064416

越南綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

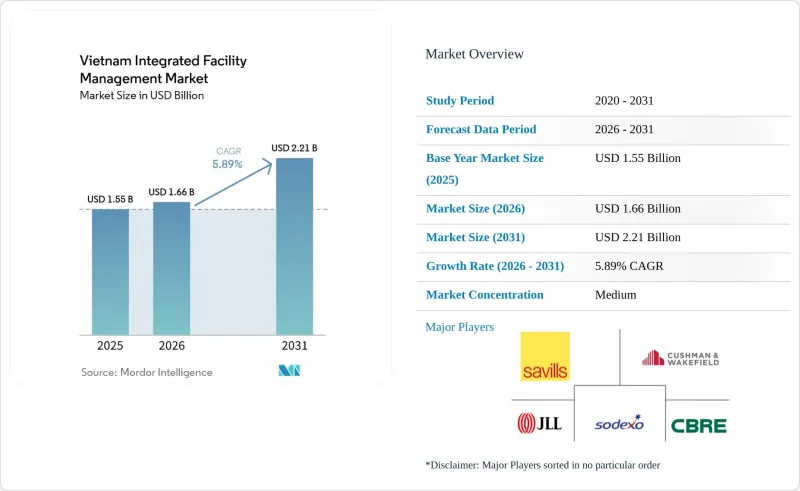

根據 Mordor Intelligence 預測,越南綜合設施管理市場規模預計將在 2025 年達到 15.5 億美元,2026 年達到 16.6 億美元,到 2031 年達到 22.1 億美元,2026 年至 2031 年的複合年成長率為 5.89%。

本報告按服務類型(硬性設施管理[資產管理、機電/暖通空調服務等]、軟性設施管理[辦公室支援/安保、清潔服務、餐飲服務等])和最終用戶行業(商業、旅館、公共設施/公共基礎設施、醫療保健等)進行分類。市場預測以美元計價。

越南綜合設施管理市場趨勢及分析

增加外國直接投資(FDI)和擴大工業園區

越南的綜合設施管理市場正受惠於新建工業園區的供應以及南北兩地高附加價值製造業活動的穩定成長。新建工廠、物流中心和供應商園區不僅擴大了占地面積,還引入了技術系統、安全規程和營運規範,這些都需要單一、負責的服務模式,而非多個各自為政的供應商。這一趨勢在北寧、北江和海防尤為顯著,這些地區的電子、半導體組裝和精密製造企業需要潔淨室管理、不間斷的公用設施供應、協調的維護計劃以及可審計的現場安全措施。南部走廊地區,包括平陽和同奈,也呈現類似的趨勢,工業擴張催生了大量技術密集、綜合設施管理合約。根據第一太平戴維斯越南公司預測,到2025年,預計將有42個新的工業園區計畫獲得批准,新增約8,400公頃可租賃土地。隨著這些工業園區進入進駐階段,越南綜合設施管理市場將形成一個多年期的資產儲備庫。隨著越南吸引更多流程導向生產基地,越南綜合設施管理市場的服務範圍正從被動的現場支援轉向更高階的領域,例如預防性維護、合規管理和持續營運保障。

快速的都市化和商業不動產的成長

越南的綜合設施管理市場持續擴張,部分原因是河內和胡志明市的城市建設不斷增加,導致需要系統化全生命週期管理的建築數量持續成長。根據越南電視台報道,到2024年底,這兩個城市將有超過2870座高層建築竣工,這顯示對常規設施管理服務的需求基礎廣泛且持續成長。這一機遇在相對較新的甲級和高階商業地產中尤其明顯,因為這些資產通常配備集中式建築管理系統、暖通空調分區系統、智慧門禁系統和能源監控工具,需要經過培訓的操作人員,而非單一承包商。綠色認證辦公大樓的開發也加速了這一趨勢,因為業主需要完善的基礎設施來維持認證結果,並滿足租戶對能源、室內空氣品質和服務透明度的期望。雖然這一趨勢在河內西部和胡志明市中心最為顯著,但隨著辦公室、綜合用途和物流項目的設計日益規範化,其影響也正擴展到峴港和海防等城市。類似的城市擴張也推高了飯店、零售和科技業辦公租戶的需求,因為這些公司需要比傳統建築通常需要的更專業的清潔、支援、保全和資產管理方案。

分散且無組織的服務提供者的現狀

越南的綜合設施管理(IFM)市場受制於其高度分散的服務體系,該體系仍涵蓋清潔公司、保全公司、維修供應商和小規模本地支援服務提供者。越南電視台指出,與新業務數量迅速成長,但這種擴張並未轉化為標準化服務品質或更廣泛的多服務能力的相應提升。這種情況使得租戶難以整合供應商,因為許多國內業者能夠有效管理一兩項服務,但只有少數業者能夠提供配備充足人員、完善的文件和保險的全面IFM服務。中型物業最容易受到此問題的影響,它們通常依賴非正式或有限的分包協議,這使得綜合服務提供者難以僅憑價格優勢就取代它們。由於缺乏全國統一的強制性設施管理品質標準,不合格的業者得以繼續競標,從而限制了越南綜合設施管理市場的平均合約價值。這種情況也減緩了越南中小企業(SME)的轉型。這些中小企業往往仍然不相信綜合合約能夠提供足夠的價值,從而證明放棄低成本、單一服務採購的合理性。

細分市場分析

到2025年,軟性設施管理(FM)將佔越南綜合設施管理(IFM)市場佔有率的55.7%,反映出清潔、餐飲、蟲害控制、禮賓和支援服務在商業、飯店、工業和住宅設施中的廣泛應用。這一細分市場規模龐大,是因為飯店、醫院、食品加工廠和人流量大的辦公大樓等勞動密集型環境需要穩定的人員配備和服務流程,從而保證了合約價值的穩定性。此外,在越南的IFM產業,軟性FM的重要性日益凸顯,因為即使沒有高度複雜的技術系統,衛生管理、租戶支援和前台營運也至關重要。在此背景下,捆綁式FM正在蓬勃發展,因為租戶更傾向於簽訂一份包含設施支援、資產管理和合規報告的單一契約,而不是從多個供應商獲得零散的服務。 Lotus V4的普及也為此提供了助力。獲得認證的物業需要更有系統的績效記錄和標準化的建築管理,這比分散的外包模式更適合協調的服務模式。

預計2026年至2031年間,硬體維修)將以6.4%的複合年成長率成長,成為越南綜合設施管理(IFM)市場中成長最快的服務領域。其主要原因是新投入運作的資產,特別是工廠、已建成的工業園區、高階辦公大樓和數據連接設施的技術特性。這些設施僅靠日常維修人員無法充分維護。半導體組裝、電子產品製造商和電動汽車零件製造商需要計劃性維護、精密工程支援、消防安全系統認證以及機電設備的持續運作,以保障生產品質並降低停機風險。 KCN Vietnam指出,在海防、同奈和北寧等地區,獲得LEED金級認證的現成工廠數量不斷增加,這正在推動向常駐現場工程團隊和數位化輔助維護營運的轉變。在越南的IFM產業,這意味著硬體維修正在從單純的支援職能轉變為先進製造業和機構投資者房地產相關合約中的核心價值創造因素。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 技術分析

- 監理情勢

- 市場促進因素

- 外國直接投資流入增加和工業園區擴張

- 快速的都市化和商業不動產的成長

- 由於成本最佳化壓力,非核心的設施管理 (FM) 業務擴大被外包。

- 數位轉型和智慧建築技術的引入

- 加強ESG合規要求,推廣綠建築認證

- 飯店、零售和科技辦公室產業對專業設施管理的需求日益成長。

- 市場限制因素

- 設施管理服務供應商的市場結構極為分散且無序。

- 合格且技能嫻熟的設施管理專家短缺

- 對整合式設施管理技術平台進行大量初始資本投資

- 國內中小企業對綜合設施管理價值提案的認知較低。

- 波特五力分析

第5章:預測市場規模與成長率

- 按服務類型

- 硬體設施管理

- 資產管理

- 機電/暖通空調服務

- 消防系統和安全

- 其他硬體設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬體設施管理

- 按最終用戶行業分類

- 商業

- 飯店業

- 公共設施和公共基礎設施

- 醫療保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Savills Vietnam Ltd.

- ISS A/S

- Sodexo SA

- G4S Plc

- Cushman AND Wakefield plc

- Knight Frank LLP

- Colliers International Group Inc.

- FPT Facility Management JSC

- VinService JSC

- BVFM Facility Management Co. Ltd.

- Newtecons FM Co. Ltd.

- PMC Building Services and Trading Co. Ltd.

- NoVa Facility Management Co., Ltd.

- A2Z Facility Services Co. Ltd.

- Aplitek Services Co. Ltd.

- Vinhomes Property and Facility Management

- Anabuki Clean Service Vietnam Co. Ltd.

- REE Corporation(Facility Services Division)

- Detech Facility Management Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the vietnam integrated facility management market size is projected to be USD 1.55 billion in 2025, USD 1.66 billion in 2026, and reach USD 2.21 billion by 2031, growing at a CAGR of 5.89% from 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Integrated Facility Management Market Trends and Insights

Rising FDI And Industrial Park Expansion

The Vietnam integrated facility management market is gaining direct support from new industrial park supply and from the steady rise in higher-value manufacturing activity across both the north and the south. New factories, logistics hubs, and supplier campuses not only add floor area but also introduce technical systems, safety procedures, and operating protocols that require a single accountable service model rather than multiple disconnected vendors. This is especially visible in Bac Ninh, Bac Giang, and Hai Phong, where electronics, semiconductor assembly, and precision manufacturing tenants need cleanroom control, uninterrupted utilities, calibrated maintenance schedules, and auditable site security practices. The same pattern is visible in southern corridors such as Binh Duong and Dong Nai, where industrial expansion is creating a pipeline of bundled, technically intensive FM contracts. Savills Vietnam reported 42 newly approved industrial park projects in 2025, adding close to 8,400 hectares of leasable land, which supports a multi-year asset pipeline for the Vietnam integrated facility management market as those parks move toward occupancy. As Vietnam attracts more process-critical production, the service scope within the Vietnam integrated facility management market shifts upward from reactive site support toward preventive engineering, compliance management, and continuous operations assurance.

Rapid Urbanization and Commercial Real Estate Growth

Vietnam integrated facility management market is also expanding because urban construction in Hanoi and Ho Chi Minh City continues to add a large stock of buildings that need organized lifecycle management. Vietnam Television reported that the two cities had more than 2,870 completed high-rise buildings by late 2024, which shows that the demand base for recurring FM services is broad and still expanding. The opportunity is strongest in newer Grade A and upper-tier commercial properties because those assets usually include centralized building management systems, HVAC zoning, smart access controls, and energy monitoring tools that require trained operators rather than single-line contractors. Green-certified office development is reinforcing that pattern because owners need maintenance regimes that preserve certification outcomes and support tenant expectations around energy, indoor air quality, and service transparency. West Hanoi and central Ho Chi Minh City are showing this movement most clearly, but the spillover is reaching Da Nang and Hai Phong as office, mixed-use, and logistics projects become more institutional in design. The same urban expansion is also lifting demand from hospitality, retail, and technology office occupiers, which need more specialized cleaning, support, security, and asset-care programs than older buildings typically required.

Fragmented And Unorganized Provider Landscape

The Vietnam integrated facility management market is still held back by a service base that remains highly fragmented across cleaning firms, security companies, maintenance vendors, and small local support providers. Vietnam Television noted that the number of new FM-related businesses has been rising quickly, but this expansion has not created a comparable rise in standardized delivery quality or broad multi-service capability. That makes vendor consolidation harder for occupiers because many domestic operators can manage one or two service lines effectively, but only a limited number can absorb a full IFM mandate with the right staffing depth, documentation discipline, and insurance coverage. Mid-market properties are the most exposed to this issue because they often rely on informal or narrowly scoped subcontracting arrangements that are difficult for integrated providers to displace on price alone. The absence of a compulsory national quality framework for FM keeps underqualified players in the bidding pool and caps average contract value across the Vietnam integrated facility management market. This same landscape also slows the conversion of domestic SMEs, which often remain unconvinced that integrated contracts offer enough value to justify a shift away from low-cost single-service procurement.

Other drivers and restraints analyzed in the detailed report include:

- Cost Optimization Through Outsourcing Non-Core FM Activities

- Digital Transformation and Smart Building Technology Adoption

- Shortage Of Qualified and Skilled FM Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft facility management (FM) held 55.7% of Vietnam integrated facility management (IFM) market share in 2025, reflecting the wide use of cleaning, catering, pest control, concierge, and support services across commercial, hospitality, industrial, and residential properties. This segment remains large because labor-intensive environments, including hotels, hospitals, food processing units, and high-traffic office towers, require consistent headcount deployment and service routines that translate into steady contract value. The Vietnam IFM industry also gives Soft FM added weight because hygiene, occupancy support, and front-of-house services remain essential even when technical systems are less advanced. Bundled FM is gaining ground inside this mix, as occupiers prefer one contract that combines site support, asset care, and compliance reporting rather than a patchwork of separate vendors. LOTUS V4 adds another push because certified properties now need more structured performance records and standardized building operations, which fit better with coordinated service models than with fragmented outsourcing.

Hard FM is projected to grow at a 6.4% CAGR from 2026 to 2031, making it the fastest-growing service type in the Vietnam IFM market. The main reason is the technical profile of new assets entering operation, especially factories, ready-built industrial space, premium offices, and data-linked facilities that cannot rely on periodic repair crews alone. Semiconductor assemblers, electronics manufacturers, and EV component producers need planned maintenance, calibrated engineering support, fire system certification, and continuous MEP uptime to protect production quality and avoid shutdown risk. KCN Vietnam highlighted the rise of LEED Gold ready-built factories in locations such as Hai Phong, Dong Nai, and Bac Ninh, which reinforces the movement toward permanent on-site engineering teams and digitally supported maintenance routines. Within the Vietnam IFM industry, this means Hard FM is moving from a support function to a core value driver for contracts tied to advanced manufacturing and institutional-grade real estate.

List of Companies Covered in this Report:

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Savills Vietnam Ltd.

- ISS A/S

- Sodexo SA

- G4S Plc

- Cushman AND Wakefield plc

- Knight Frank LLP

- Colliers International Group Inc.

- FPT Facility Management JSC

- VinService JSC

- BVFM Facility Management Co. Ltd.

- Newtecons FM Co. Ltd.

- PMC Building Services and Trading Co. Ltd.

- NoVa Facility Management Co., Ltd.

- A2Z Facility Services Co. Ltd.

- Aplitek Services Co. Ltd.

- Vinhomes Property and Facility Management

- Anabuki Clean Service Vietnam Co. Ltd.

- REE Corporation (Facility Services Division)

- Detech Facility Management Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Industry Value-Chain Analysis

- 4.4 Technology Analysis

- 4.5 Regulatory Landscape

- 4.6 Market Drivers

- 4.6.1 Rising FDI Inflows and Industrial Park Expansion

- 4.6.2 Rapid Urbanization and Commercial Real Estate Growth

- 4.6.3 Cost Optimization Pressure Driving Outsourcing of Non-Core FM Activities

- 4.6.4 Digital Transformation and Smart Building Technology Adoption

- 4.6.5 Growing ESG Compliance Requirements and Green Building Certification Adoption

- 4.6.6 Expanding Hospitality, Retail, and Technology Office Sectors Requiring Specialized FM

- 4.7 Market Restraints

- 4.7.1 Highly Fragmented and Unorganized FM Service Provider Landscape

- 4.7.2 Shortage of Qualified and Skilled FM Professionals

- 4.7.3 High Upfront Capital Investment Requirements for Integrated FM Technology Platforms

- 4.7.4 Low Awareness of Integrated FM Value Proposition Among Domestic SMEs

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group, Inc.

- 6.4.2 Jones Lang LaSalle Incorporated

- 6.4.3 Savills Vietnam Ltd.

- 6.4.4 ISS A/S

- 6.4.5 Sodexo SA

- 6.4.6 G4S Plc

- 6.4.7 Cushman AND Wakefield plc

- 6.4.8 Knight Frank LLP

- 6.4.9 Colliers International Group Inc.

- 6.4.10 FPT Facility Management JSC

- 6.4.11 VinService JSC

- 6.4.12 BVFM Facility Management Co. Ltd.

- 6.4.13 Newtecons FM Co. Ltd.

- 6.4.14 PMC Building Services and Trading Co. Ltd.

- 6.4.15 NoVa Facility Management Co., Ltd.

- 6.4.16 A2Z Facility Services Co. Ltd.

- 6.4.17 Aplitek Services Co. Ltd.

- 6.4.18 Vinhomes Property and Facility Management

- 6.4.19 Anabuki Clean Service Vietnam Co. Ltd.

- 6.4.20 REE Corporation (Facility Services Division)

- 6.4.21 Detech Facility Management Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)