|

市場調查報告書

商品編碼

2065532

義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Italy Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

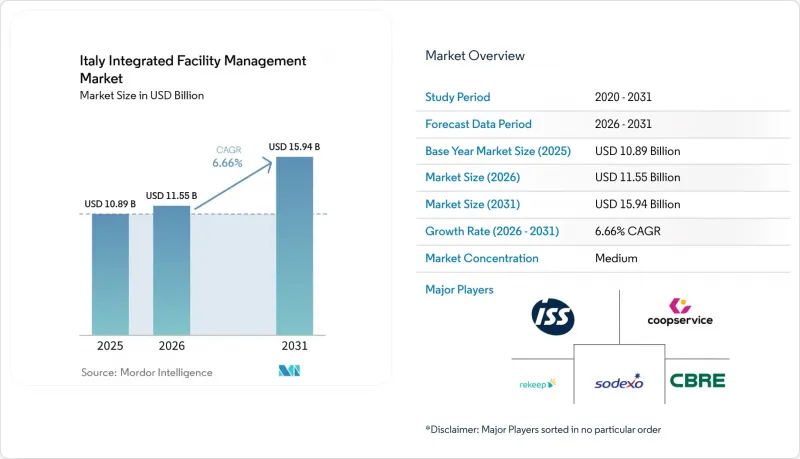

根據 Mordor Intelligence 預測,義大利綜合設施管理市場規模將從 2025 年的 108.9 億美元和 2026 年的 115.5 億美元成長到 2031 年的 159.4 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.66%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和保全、清潔服務、餐飲服務等])和最終用戶(商業設施、飯店、公共機構和公共基礎設施、醫療設施等)進行分類。市場預測以美元計價。

義大利整合性機構管理市場的趨勢與洞察

從單一服務外包轉型為綜合設施管理策略

義大利整合性機構管理市場正經歷結構性轉型。截至2025年1月,綜合合約僅佔設施管理總收入的26%,這意味著傳統單一服務支出的大片領域將成為整合的目標。這一點意義重大,因為分散的合約會導致供應商過多、營運環節過多,並且在買家要求對複雜的房地產投資組合進行可衡量的服務評估時,缺乏有效的課責。米蘭理工大學的研究也支持這一趨勢,研究表明,與綜合模式相比,分散的多供應商設施管理模式的總擁有成本(TCO)可能更高。這為財務部門和營運經理推廣服務捆綁提供了更有力的理由。這種轉變不再只是為了降低成本,因為公共和私人買家越來越需要由單一供應商在單一商業性框架下管理的績效儀表板、資產可視性、服務順序和可審計的報告。這正在改變義大利綜合設施管理市場的競標格局。能夠整合軟體服務、技術服務、數位化工具和檢驗方法的供應商,在贏得以往被拆分成多個採購項目的合約方面更具優勢。從長遠來看,這將帶來更長的合約期限、更高的客戶留存率,並進一步拉大規模業者與那些仍局限於狹窄服務領域的公司之間的差距。

加強能源效率法規與ESG要求的銜接

能源效率法規正成為義大利綜合大樓管理市場需求的直接來源。這是因為相關法規已從自願改進轉向公共建築和非住宅建築的強制性措施。 2023/1791 號指令要求公共實體在 2021 年的基礎上,每年降低其最終能源消耗 1.9%,並對所有公共實體設定 3% 的年度維修目標,這些公共實體管理的公共建築占地面積估計達 2.09 億平方米。義大利的 CAM 法規於 2024 年 8 月生效,並在此基礎總合增加了更多要求。這些要求包括強制實現 B 級或更高級別的自動化、整合建築能源管理系統 (BEMS)、基於 BIM 的合約管理,以及在初始合約中檢驗的年度初級能源消耗至少降低 10%。這意味著技術能力不再被視為可選的附加服務,而是納入了競標要求。義大利國家能源與環境署 (ENEA) 發布的《2025 年建築能源認證報告》進一步凸顯了這個問題的迫切性。義大利56%的公共住宅建築仍被評級F級或G級能源效率等級,顯示該國建築存量仍面臨巨大的維修壓力。實際上,這使得硬體維修商能夠確保公共資產服務流程更加清晰、永續,同時也增強了將設施管理與可衡量的能源績效掛鉤的績效合約的合法性。正因如此,義大利的綜合設施管理市場正逐漸轉向以產能為主導,因為採購現在更加重視已驗證的能源效率、系統整合和合規管理,而非單一服務的低價。

市場分散且對價格敏感,阻礙了競爭。

義大利綜合設施管理市場面臨的主要限制因素之一是,該行業的大部分企業仍然依賴分散的區域間競爭,價格仍然是首要的選擇標準。這削弱了企業投資更先進技術的商業價值。在這種環境下,許多公司無需建構大規模綜合營運所需的數位化平台、認證體系和先進工程能力,就能贏得小規模合約。米蘭理工大學的一項研究表明,系統碎片化是義大利設施管理(FM)實踐中資訊通訊技術(ICT)應用面臨的最常見障礙之一。這意味著,即使技術本身已經可用,組織結構的複雜性仍然會阻礙轉型。這直接影響服務質量,因為過度受初始價格驅動的合約幾乎沒有為建築能源管理系統(BEMS)、智慧電錶、認證能源管理和持續數據檢驗的實施留出空間。雖然公共部門負責人已開始透過在某些競標結構中更加重視技術品質來應對這一問題,但這種轉變在全國範圍內仍然不均衡,尚未完全取代價格主導的採購行為。在這種平衡發生更廣泛的轉變之前,義大利的綜合設施管理市場可能會繼續呈現「兩極化」的趨勢,即高度發展的頂層市場和以成本主導的中階。

細分市場分析

截至2025年,軟性設施管理(FM)佔義大利綜合設施管理(IFM)市場佔有率的53.7%,而硬體維修預計到2031年將以7.4%的複合年成長率成長。軟性設施管理仍然佔據較大佔有率,因為它仍然是公共部門、醫療保健和企業租戶外包的常見起點。在這些部門,清潔、衛生、接待、搬運服務和日常支援服務通常是最早外包的專案。硬體維修的快速成長源於義大利的能源法規、合規義務以及建築老化問題,這些因素正在將技術維護從一項延遲的資本決策轉變為一項持續的營運必需品。公共建築每年3%的維修目標以及公共機構普遍存在的節能要求正在推動這一轉變,使學校、醫院和其他國有設施對技術服務的需求更加明確。在硬體維修中,資產管理和機電(機械、電氣和管道)服務仍然佔據核心地位,因為它們與運轉率、能源效率和法規遵循密切相關。然而,隨著互聯建築基礎設施的日益普及,防火防災系統和安防系統的重要性也日益凸顯。

硬性硬體維修)也是義大利綜合設施管理(IFM)市場的重要組成部分,預計在預測期內,該領域將受益於產能主導型採購。由於醫療保健和公共部門的採購方在合約規範和服務審核中持續保持高衛生標準,因此對清潔和管理服務的需求仍然穩定。隨著門禁控制、監控和技術系統擴大在單一營運模式下進行管理,保全服務也呈現成長勢頭,從而減少了交接環節,並提高了設施績效的課責。這正在改變義大利IFM產業的服務包結構,因為軟性設施管理(Soft FM)供應商需要更強大的數位化連接和報告工具,才能保護其合約範圍免受更多IFM競爭對手的衝擊。 Consip FM4正在推動這項變革,它將客服中心支援、資產帳簿、管治工具和即時監控整合到合約執行流程中,而非作為可選附加功能。米蘭理工大學的學術研究也支持這一方向,該研究表明,將物聯網數據與建築管理系統整合可以提高設施管理效率。然而,現實情況是,許多組織在建立內部系統方面仍然面臨挑戰,而非技術本身。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從單一服務外包轉型為綜合設施管理策略

- 加強能源效率法規與ESG要求的銜接

- 智慧建築物連網平台的廣泛應用

- 疫情後對衛生和公共衛生服務的需求

- 公共基礎設施私有化與PNRR相關投資

- 公共部門對非核心職能外包的需求日益成長。

- 市場限制因素

- 市場分散且對價格敏感,阻礙了競爭。

- IFM平台的高市場准入成本與生命週期成本

- 限制柔軟性的數位轉型能力

- 勞動力短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全措施

- 其他硬體維修服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟調頻服務

- 硬設施管理

- 最終用戶

- 商業

- 飯店業

- 機構和公共基礎設施

- 衛生保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Rekeep SpA

- Coopservice Societa Cooperativa per Azioni

- ISS Facility Services Srl

- Sodexo SA

- CBRE Group, Inc.

- Compass Group PLC

- Apleona GmbH

- Dussmann Stiftung & Co. KGaA

- Euro & Promos Facility Management SpA

- PFE SpA

- GSA Gruppo Servizi Associati SpA

- Servizi Italia SpA

- Atalian Global Services Italia SpA

- Engie Italia SpA

- Johnson Controls International plc

- Savills plc

- Siram Veolia SpA

- Elmet Srl

- NAZCA Facility Management Srl

- Olly Services Srl

第7章 市場機會與未來展望

According to Mordor Intelligence, the italy integrated facility management market size is projected to expand from USD 10.89 billion in 2025 and USD 11.55 billion in 2026 to USD 15.94 billion by 2031, registering a CAGR of 6.66% between 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

Italy Integrated Facility Management Market Trends and Insights

Strategic Shift from Single Service Outsourcing to Integrated FM

The Italy integrated facility management market is moving through a structural conversion phase because integrated contracts still accounted for only 26% of total FM revenue in January 2025 and that leaves a broad base of legacy single-service spending open to consolidation. This matters because fragmented contracting creates too many vendors, too many operating interfaces, and too little accountability when buyers need measurable service results across complex estates. Research from Politecnico di Milano supports that direction, showing that fragmented multi-vendor FM models can carry a higher total cost of ownership than integrated structures, which gives both finance teams and operating leaders a stronger case for service bundling. The shift is no longer limited to basic cost reduction, because public and private buyers increasingly want one provider to manage performance dashboards, asset visibility, service sequencing, and audit-ready reporting under one commercial framework. That is changing the shape of bidding in the Italy integrated facility management market, since providers that can combine soft services, technical services, digital tools, and verification methods are better placed to capture contracts that previously sat across separate procurement lots. Over time, this should lift contract duration, improve retention, and widen the gap between scale operators and firms that remain tied to narrowly defined service lines.

Increasing Energy Efficiency Regulations with ESG Mandates

Energy efficiency rules are becoming a direct source of demand in the Italy integrated facility management market, because regulation has moved from voluntary improvement toward mandatory action in both public and non-residential buildings. Directive 2023/1791 requires a 1.9% annual reduction in final energy consumption for public entities against a 2021 baseline, and it extends the 3% annual renovation target across public entities that together cover an estimated 209 million m2 of public building surface. Italy's August 2024 CAM rules add another layer, because they require class B or higher automation, BEMS integration, BIM-based contract management, and at least 10% verified annual primary energy savings in first contracts, which means technical competence is now built into tender compliance rather than treated as an optional service add-on. ENEA's 2025 building energy certification reporting adds urgency, since 56% of Italian public residential buildings were still rated in energy class F or G, showing the depth of the retrofit burden that remains in the national building stock. In practice, this gives Hard FM providers a clearer and more durable work pipeline across public assets, while also strengthening the case for outcome-based contracts that link facility management with measured energy results. It also explains why the Italy integrated facility management market is becoming more capability-led, because procurement now rewards proof of savings, system integration, and compliance management more than low standalone service pricing.

Fragmented And Price-Sensitive Market Dampening Competition

A major constraint on the Italy integrated facility management market is that a large share of the sector still operates through fragmented regional competition, where price remains the first screening tool and that weakens the business case for deeper capability investment. In that environment, many firms can still win smaller contracts without building the digital platforms, certification systems, and engineering depth that are needed for larger integrated mandates. Politecnico di Milano research also shows that fragmentation of systems is one of the most common barriers to ICT adoption in Italian FM settings, which means organizational complexity continues to slow change even when the technology itself is available. This has a direct effect on service quality, because contracts shaped too heavily by upfront price leave less room for BEMS installation, smart metering, certified energy management, and ongoing data verification. Public buyers are starting to respond by placing more weight on technical quality in some tender structures, yet that shift is still uneven across the country and has not fully displaced price-led buying behaviour. Until that balance changes more widely, the Italy integrated facility management market will keep showing a two-speed pattern, with a sophisticated top tier and a cost-driven middle layer.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Smart Building IoT Platforms

- Post-Pandemic Demand for Hygiene and Sanitation Services

- Digital Transformation Capabilities Limiting Flexibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management (FM) held 53.7% of the Italy integrated facility management (IFM) market share in 2025, while Hard FM is forecast to grow at a 7.4% CAGR through 2031. Soft FM stayed larger because it remains the usual starting point for outsourcing in public administration, healthcare, and corporate occupier settings, where cleaning, hygiene, reception, porterage, and routine support services are often the first scopes to move outside the organization. Hard FM is rising faster because energy rules, compliance obligations, and the age profile of Italian buildings are turning technical maintenance into a continuous operating need rather than a delayed capital decision. The 3% annual public-building renovation target and the broader energy reduction requirements across public entities support that shift by giving technical services a clearer demand base across schools, hospitals, and other state-owned estates. Within Hard FM, asset management and MEP services remain central because they sit closest to uptime, energy efficiency, and statutory compliance, while fire safety and security systems are gaining relevance as connected building infrastructure becomes more common.

Hard FM is also part of the Italy IFM market size that stands to benefit most from capability-led procurement during the forecast period. Cleaning and janitorial services still carry steady demand, because healthcare and institutional buyers continue to keep hygiene standards high inside contract specifications and service audits. Security services are also gaining ground as access control, surveillance, and technical systems are more often managed inside one operating model, which reduces handoffs and improves accountability for site performance. This is changing how the Italy IFM industry packages service bundles, because Soft FM operators now need stronger digital coordination and reporting tools if they want to protect contract scope against broader IFM rivals. Consip FM4 has reinforced that shift by making call-center support, asset registries, governance tools, and real-time monitoring part of contract execution rather than optional overlays. Academic work from Politecnico di Milano also supports the direction of travel, showing that IoT data linked to building management systems can improve FM efficiency, even if many organizations still struggle more with internal readiness than with the technology itself.

List of Companies Covered in this Report:

- Rekeep SpA

- Coopservice Societa Cooperativa per Azioni

- ISS Facility Services S.r.l.

- Sodexo S.A.

- CBRE Group, Inc.

- Compass Group PLC

- Apleona GmbH

- Dussmann Stiftung & Co. KGaA

- Euro & Promos Facility Management S.p.A.

- PFE S.p.A.

- GSA Gruppo Servizi Associati S.p.A.

- Servizi Italia S.p.A.

- Atalian Global Services Italia S.p.A.

- Engie Italia S.p.A.

- Johnson Controls International plc

- Savills plc

- Siram Veolia S.p.A.

- Elmet S.r.l.

- NAZCA Facility Management S.r.l.

- Olly Services S.r.l.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strategic Shift from Single Service Outsourcing to Integrated FM

- 4.2.2 Increasing Energy Efficiency Regulations with ESG Mandates

- 4.2.3 Growing Adoption of Smart Building IoT Platforms

- 4.2.4 Post-Pandemic Demand for Hygiene and Sanitation Services

- 4.2.5 Public Infrastructure Privatization and PNRR-Linked Investment

- 4.2.6 Rising Demand for Outsourced Non-Core Services in the Public Sector

- 4.3 Market Restraints

- 4.3.1 Fragmented and Price-Sensitive Market Dampening Competition

- 4.3.2 High Market Entry and Lifecycle Expenses for IFM Platforms

- 4.3.3 Digital Transformation Capabilities Limiting Flexibility

- 4.3.4 Insufficient Labor Coverage

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Rekeep SpA

- 6.4.2 Coopservice Societa Cooperativa per Azioni

- 6.4.3 ISS Facility Services S.r.l.

- 6.4.4 Sodexo S.A.

- 6.4.5 CBRE Group, Inc.

- 6.4.6 Compass Group PLC

- 6.4.7 Apleona GmbH

- 6.4.8 Dussmann Stiftung & Co. KGaA

- 6.4.9 Euro & Promos Facility Management S.p.A.

- 6.4.10 PFE S.p.A.

- 6.4.11 GSA Gruppo Servizi Associati S.p.A.

- 6.4.12 Servizi Italia S.p.A.

- 6.4.13 Atalian Global Services Italia S.p.A.

- 6.4.14 Engie Italia S.p.A.

- 6.4.15 Johnson Controls International plc

- 6.4.16 Savills plc

- 6.4.17 Siram Veolia S.p.A.

- 6.4.18 Elmet S.r.l.

- 6.4.19 NAZCA Facility Management S.r.l.

- 6.4.20 Olly Services S.r.l.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)