|

市場調查報告書

商品編碼

2064372

新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Singapore Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

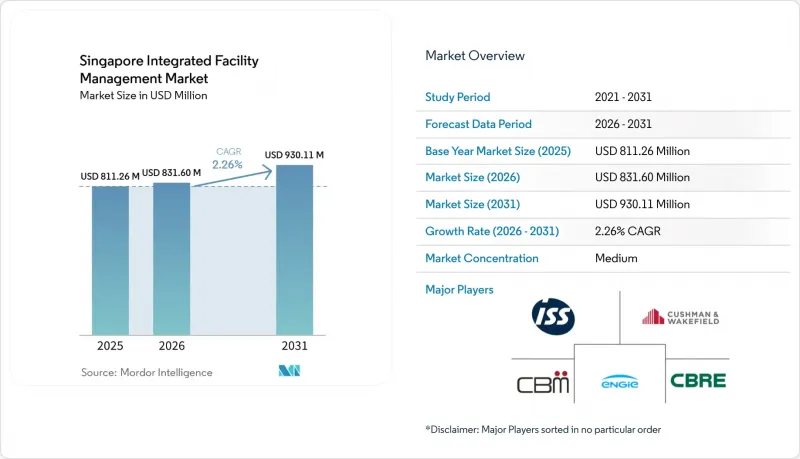

根據 Mordor Intelligence 預測,新加坡綜合設施管理市場規模預計將從 2025 年的 8.1126 億美元和 2026 年的 8.316 億美元成長到 2031 年的 9.3011 億美元,2026 年至 2031 年的複合年成長率為 2.26%。

本報告依服務類型(硬體管理[資產管理、機電/暖通空調服務等]、軟體設備管理[辦公室支援/保全、清潔服務、餐飲服務等])及最終用戶(商業、飯店、醫療保健、工業/流程產業等)分類。市場預測以美元計價。

新加坡綜合設施管理市場趨勢與洞察

政府加大力度推廣智慧綠建築

新加坡的綜合設施管理市場正受惠於政府為提升現有建築能源效率所採取的直接措施。新加坡建築業的二氧化碳排放量佔全國總排放的20%以上,因此,能源效率仍然是一項重要的政策重點,這也支撐了對能夠提供可衡量成果的技術服務供應商的長期需求。 《2025年建築規例(現有建築環境永續性措施)(修訂)規則》於2025年9月30日生效,該規則設定了辦公大樓、零售場所和醫院的能源消耗強度閾值:辦公大樓200千瓦時/平方公尺/年,零售場所495千瓦時/平方公尺/年,醫院360千瓦時/平方公尺/平方公尺/年,醫院360千瓦時/平方公尺/平方公尺/年,醫院360千瓦時/平方公尺/平方公尺/年,醫院360千瓦時/平方公尺/平方公尺/年,醫院360千瓦時/平方公尺/平方公尺/年,醫院360千瓦時。超過這些閾值的建築物必須聘請合格的能源審計師,提交能源效率改進計劃,並在三年內實現10%的節能目標。這擴大了設施管理合約的技術範圍,並促進了持續的專業合作。此外,「現有建築綠色標誌獎勵計畫2.0」透過津貼高達50%的維修成本,降低了維修工程的經濟門檻,使業主更容易簽訂與績效掛鉤的設施管理(FM)合約。在新加坡,2026年5月,61%的建築將達到綠色標準,而2030年實現80%的目標仍有差距,這顯示新加坡綜合設施管理(IFM)市場對維修相關服務的短期需求必將旺盛。

預防性維護和健康、安全與環境法規的強制性要求

新加坡的綜合設施管理(IFM)市場也受惠於嚴格的法規環境,這使得預防性維護難以延後。建築業主必須管理一系列相互交織的義務,包括職場安全和消防安全認證、電梯維護、電扶梯維護以及空調系統維護等,因此,能夠以單一運營模式協調這些服務的綜合供應商越來越受歡迎。新加坡建設局(BCA)的FM01商業領袖框架縮小了公共部門維護合約的合格候選人範圍,M1級申請人必須擁有200萬新元(150萬美元)的實繳資本,以及至少相當於4000萬新元(3000萬美元)的檢驗的IFM項目經驗。這種篩選機制有助於新加坡綜合設施管理市場中大規模認證營運商的獲利管理,尤其是在客戶優先考慮可靠性而非最低競標的情況下。政府的競標要求也支持這一趨勢,因為無法達到認證安全標準的營運商不太可能獲得高價值的預防性維護工作。實際上,這使得合規維護計劃成為成熟公司永續的收入來源,這些公司能夠無縫管理多個監管機構、技術營運和報告義務。

合格的設施管理(FM)人員短缺限制了服務的擴充性。

勞動力仍是限制新加坡綜合設施管理(IFM)市場快速擴張的最明顯結構性因素。預計到2025年12月,新加坡的就業與失業比率將達到1.58,24.3%的雇主表示存在技能缺口,這增加了工作量並影響了服務品質。設施管理產業面臨的壓力更為嚴峻,因為人事費用佔營運成本的40-50%,許多硬體維修合約需要持有認證的技術人員、機械工程師和能源審計師,這些人員難以取代。本地技術人員的老化以及年輕人進入科技領域的速度緩慢加劇了這個問題,而引進外籍勞工的限制也使得大規模人員招募變得困難。這些因素共同限制了新業務能夠吸收的規模,即使存在市場需求,因為合約的履行不僅取決於銷售能力,還取決於能否獲得合格的人員。雖然新加坡建設局學院的專業培訓計畫有助於中期人才儲備,但並不能完全解決新加坡綜合設施管理市場面臨的短期人才短缺問題。

細分市場分析

在新加坡綜合設施管理 (IFM) 市場中,硬設施管理 (FM) 是成長最快的服務領域,預計該領域的市場規模將從 2026 年到 2031 年以 2.88% 的複合年成長率 (CAGR) 成長。這一成長率與將於 2025 年 9 月生效的「能源強度指數 (MEI)」計劃密切相關。該計劃將能源績效從一項可選的升級目標轉變為占地面積超過 5,000平方公尺的大型建築的一項有時效性的合規要求。如果建築物的能源強度超過指定的閾值,業主必須聘請合格的專業人員並記錄糾正措施。這將使硬體維修管理服務提供者在審計、機械設備最佳化、系統調整和後續報告方面發揮持續作用。自 KONE 在新加坡實施智慧連網電梯服務以來,兩年內,透過預測性維護將故障偵測率提高了 70%,並將現場服務呼叫量減少了 40%。這表明技術運營商正從定期檢查轉向持續監測契約,以提高每項資產的收益。此外,新加坡的綜合設施管理 (IFM) 產業也受惠於當地的營運環境。全年高濕度和長時間的運作使得暖通空調 (HVAC) 基礎設施的建設難以推遲,否則將影響舒適度、效率和建築合規性。

軟性設施管理(Soft FM)將繼續保持其最大的市場佔有率,預計到2025年將佔據新加坡綜合設施管理(IFM)市場61.75%的佔有率。這一主導地位反映了其業務的廣泛性,涵蓋清潔、保全、園林綠化、蟲害控制、禮賓服務以及幾乎所有資產類別相關的現場服務。在新加坡的綜合設施管理產業,該服務集團深深紮根於商業建築、公共空間、物流設施以及需要持續日常執行且衛生管理至關重要的場所。然而,成本結構正在改變。清潔和保全產業的工資法規迫使營運商不僅要透過增加員工人數來維持獲利,還要透過Softbank Corporation、流程再造和基於結果的定價來提高獲利能力。 OCS新加坡與軟銀機器人公司於2024年11月達成的合作以及《2025年環境服務產業轉型路線圖》均指向這一方向,顯示生產力、自動化和勞動效率將塑造軟性設施管理下一階段的競爭格局。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加強政府舉措,推廣智慧環保建築。

- 基於建築規範的預防性維護強制性標準

- 企業ESG目標正在推動設施營運外包。

- 引進5G物聯網進行預測性維護

- 綜合度假村和混合用途大型企劃的擴張

- 公共部門向基於結果的設施管理合約過渡

- 市場限制因素

- 高科技建築系統熟練技術人員短缺

- 人事費用上升正在給利潤率帶來壓力。

- 基於雲端的FM平台的資料安全問題

- 疫情後商業不動產需求的波動

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬體設備管理

- 資產管理

- 機電/暖通空調服務

- 消防系統和安全

- 其他硬體設備管理服務

- 軟體設備管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟體和設備管理服務

- 硬體設備管理

- 按最終用戶行業分類

- 商業

- 飯店業

- 設施和公共基礎設施

- 醫療保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- C&W Services

- ISS A/S

- CBM Pte Ltd

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- ENGIE Services Singapore Pte Ltd.

- Atalian Global Services

- Knight Frank Pte Ltd.

- Keppel Infrastructure Holdings Pte Ltd.

- SMM Pte Ltd

- Colliers International Group Inc.

- Sodexo SA

- DTZ Facilities & Engineering(S)Limited

- Certis Group

- AETOS Holdings Pte Ltd.

- Surbana Jurong Pte Ltd.

- UEMS Solutions Pte Ltd.

- Mapletree Facilities Services Pte Ltd.

- OCS Group International Ltd.

- BMS Engineering and Trading Pte Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the singapore integrated facility management market size is projected to expand from USD 811.26 million in 2025 and USD 831.60 million in 2026 to USD 930.11 million by 2031, registering a CAGR of 2.26% between 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Healthcare, Industrial and Process Sector, and More). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Integrated Facility Management Market Trends and Insights

Growing Government Push for Smart Green Buildings

The Singapore integrated facility management market is benefiting from the government's direct push to improve the energy performance of existing buildings. Singapore's building sector accounted for more than 20% of national carbon emissions, which keeps energy efficiency high on the policy agenda and supports long-term demand for technical service providers that can deliver measurable outcomes. The Building Control (Environmental Sustainability Measures for Existing Buildings) (Amendment) Regulations 2025 took effect on September 30, 2025, and imposed Energy Use Intensity thresholds of 200 kWh/m2/year for offices, 495 kWh/m2/year for retail, and 360 kWh/m2/year for hospitals. Buildings that exceed those thresholds must appoint a qualified energy auditor, submit an Energy Efficiency Improvement Plan, and deliver a 10% reduction within 3 years, which expands the technical scope of FM contracts and supports recurring specialist work. The Green Mark Incentive Scheme for Existing Buildings 2.0 also lowers the financial barrier for retrofit activity by co-funding up to 50% of retrofit capital expenditure, which makes performance-linked FM contracts easier for owners to adopt. Singapore had greened 61% of its building stock by May 2026, and the remaining gap to the 80% target by 2030 leaves a clear near-term pipeline for retrofit-linked service mandates in the Singapore integrated facility management (IFM) market.

Mandatory Preventive Maintenance Requirements and HSE Regulations

The Singapore IFM market also benefits from a stringent regulatory environment that makes preventive maintenance difficult to defer. Building owners must manage overlapping obligations covering workplace safety, fire safety certification, lift servicing, escalator servicing, and cooling system maintenance, which increases the appeal of a single integrated provider that can coordinate those routines under one operating model. The BCA FM01 work head framework narrows the eligible pool for public sector maintenance contracts because M1-grade applicants must hold SGD 2 million (USD 1.5 million) in paid-up capital and at least SGD 40 million (USD 30 million) in a verified IFM project track record. That screening effect supports margin discipline for larger accredited operators in the Singapore integrated facility management market, especially where clients value reliability over lowest-cost bidding. Government tender requirements also reinforce that pattern because operators that cannot meet recognized safety standards are less likely to qualify for high-value preventive maintenance work. In practice, this turns compliance calendars into a recurring revenue base for established firms that can handle multiple regulators, technical trades, and reporting obligations without disruption.

Shortage Of Qualified FM Workforce Limiting Service Scalability

Labor remains the clearest structural limit on how fast the Singapore integrated facility management (IFM) market can scale. Singapore's labour market recorded a vacancy-to-unemployed ratio of 1.58 in December 2025, and 24.3% of employers reported skills gaps that increased workloads and affected service quality. In facility management, the pressure is sharper because labour accounts for 40% to 50% of operating costs, and many hard FM contracts require certified technicians, mechanical engineers, and energy auditors who are not easy to replace. The aging domestic technical workforce and weaker entry of younger workers into trade roles are adding to the problem, while foreign worker limits make large-scale staffing responses difficult. That combination restrains how much new business providers can absorb, even when demand is present, because contract mobilization depends on qualified people rather than only sales capacity. BCA Academy's specialist training programs support the medium-term pipeline, but they do not fully relieve the near-term staffing constraint facing the Singapore integrated facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Corporate ESG Push Driving Outsourcing of Facility Services

- AI And IoT Integration for Predictive Maintenance

- Data Privacy and Cybersecurity Risks in Smart Building Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard Facility Management (FM) is the fastest-growing service line in the Singapore integrated facility management (IFM) market, with the Singapore IFM market size for this segment set to rise at a 2.88% CAGR from 2026 to 2031. That pace is tied to the September 2025 MEI regime, which turns energy performance from a discretionary upgrade topic into a timed compliance requirement for large buildings above 5,000 m2 gross floor area. Once buildings cross prescribed energy intensity thresholds, owners must engage qualified specialists and document improvement actions, which gives hard FM providers a recurring role in audits, mechanical optimization, system tuning, and follow-up reporting. KONE's connected elevator services in Singapore, which improved proactive fault identification by 70% and reduced callouts by 40% in the first 2 years of deployment, show how technical operators are moving from scheduled visits toward continuous monitoring contracts that increase revenue per asset. The Singapore integrated facility management industry also benefits from local operating conditions because high humidity and long annual cooling hours make HVAC upkeep difficult to defer without affecting comfort, efficiency, and building compliance.

Soft FM remained the volume leader and held 61.75% of the Singapore IFM market share in 2025. Its lead reflects the breadth of work covered across cleaning, security, landscaping, pest control, concierge, and related site services that appear in almost every asset class. In the Singapore integrated facility management industry, this service group remains deeply embedded in commercial buildings, public spaces, logistics facilities, and hygiene-sensitive environments that require steady execution every day. The cost profile is changing, however, because wage regulation in cleaning and security is pushing operators to defend margins through robotics, process redesign, and outcome-based pricing rather than through higher labour deployment alone. OCS Singapore's November 2024 arrangement with SoftBank Robotics and the Environmental Services Industry Transformation Map 2025 both point in that direction, with productivity, automation, and labour efficiency shaping the next phase of competition in soft FM.

List of Companies Covered in this Report:

- C&W Services

- ISS A/S

- CBM Pte Ltd

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- ENGIE Services Singapore Pte Ltd.

- Atalian Global Services

- Knight Frank Pte Ltd.

- Keppel Infrastructure Holdings Pte Ltd.

- SMM Pte Ltd

- Colliers International Group Inc.

- Sodexo SA

- DTZ Facilities & Engineering (S) Limited

- Certis Group

- AETOS Holdings Pte Ltd.

- Surbana Jurong Pte Ltd.

- UEMS Solutions Pte Ltd.

- Mapletree Facilities Services Pte Ltd.

- OCS Group International Ltd.

- BMS Engineering and Trading Pte Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Government Push for Smart, Green Buildings

- 4.2.2 Mandatory Preventive Maintenance Norms Under BCA Regulations

- 4.2.3 Corporate ESG Targets Driving Outsourcing of Facility Operations

- 4.2.4 5G-Enabled IoT Adoption for Predictive Maintenance

- 4.2.5 Expansion of Integrated Resorts and Mixed-Use Mega Projects

- 4.2.6 Shift Toward Outcome-Based FM Contracts in Public Sector

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Technicians for High-Tech Building Systems

- 4.3.2 Squeezed Margins Due to Rising Manpower Costs

- 4.3.3 Data-Security Concerns in Cloud-Based FM Platforms

- 4.3.4 Volatility in Commercial Real-Estate Demand Post-Pandemic

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 C&W Services

- 6.4.2 ISS A/S

- 6.4.3 CBM Pte Ltd

- 6.4.4 CBRE Group, Inc.

- 6.4.5 Jones Lang LaSalle Incorporated

- 6.4.6 ENGIE Services Singapore Pte Ltd.

- 6.4.7 Atalian Global Services

- 6.4.8 Knight Frank Pte Ltd.

- 6.4.9 Keppel Infrastructure Holdings Pte Ltd.

- 6.4.10 SMM Pte Ltd

- 6.4.11 Colliers International Group Inc.

- 6.4.12 Sodexo SA

- 6.4.13 DTZ Facilities & Engineering (S) Limited

- 6.4.14 Certis Group

- 6.4.15 AETOS Holdings Pte Ltd.

- 6.4.16 Surbana Jurong Pte Ltd.

- 6.4.17 UEMS Solutions Pte Ltd.

- 6.4.18 Mapletree Facilities Services Pte Ltd.

- 6.4.19 OCS Group International Ltd.

- 6.4.20 BMS Engineering and Trading Pte Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)