|

市場調查報告書

商品編碼

2065533

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Japan Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

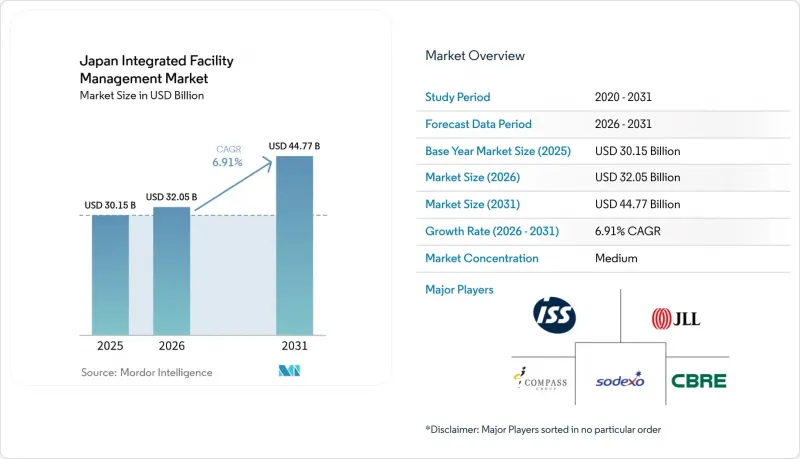

根據 Mordor Intelligence 預測,日本綜合設施管理市場預計將從 2025 年的 301.5 億美元成長到 2026 年的 320.5 億美元,到 2031 年達到 447.7 億美元,2026 年至 2031 年的複合年成長率為 6.91%。

本報告按服務類型(硬性設施管理[資產管理、機電/暖通空調服務等]、軟性設施管理[辦公室支援/安保、清潔服務、餐飲服務等])和最終用戶(商業設施、飯店、公共設施/公共基礎設施、醫療設施等)分類。市場預測以美元計價。

日本綜合設施管理市場趨勢與分析

基礎設施老化推動了對外包的需求。

在日本綜合設施管理 (IFM) 市場,老舊商業建築的出現為長期外包創造了有利條件。這是因為老舊資產需要更協調的維護和更嚴格的維護計劃。抗震加固、機電 (MEP) 設備升級、消防安全措施和衛生管理義務等工作,如果外包給多個缺乏協調的供應商,將難以有效管理,尤其是在大型、有人居住的物業中,服務中斷是不可接受的。因此,資產所有者正在轉向能夠透過單一合約處理多項技術範圍並維護符合法律要求的文件的綜合服務提供者。這種轉變也提高了合約續約率,因為客戶優先考慮透過單一聯絡人明確責任、在整個生命週期內實現透明化以及減少其建築組合的交接次數。實際上,東京、大阪和名古屋的老舊物業正在推動能夠將建築工程管理與定期合規性相結合的服務提供者發揮越來越重要的作用。這意味著日本的綜合設施管理 (IFM) 市場不僅與日常服務密切相關,而且與成熟城市資產的定期維修週期密切相關。

對預測性維護更高精度的需求日益成長

預測性維護正成為日本綜合設施管理市場實現有效成長的驅動力,它幫助服務提供者從定期檢查轉向基於狀態的干預。這在日本尤其重要,因為老舊建築、勞動力短缺以及確保技術可靠性的需求,都導致被動維護故障的成本更高。 2026年4月,NTT DOCOMO和NTT Facilities開始在NTT DOCOMO的七棟建築中檢驗互動式人工智慧系統,該系統利用圖RAG和多智慧體處理技術,使員工能夠以自然語言查詢BIM資料。該模型意義重大,因為它降低了培訓門檻,即使是缺乏專業知識的設施管理負責人也能輕鬆使用,同時改善了日常營運中對資產健康資訊的存取。此外,NTT DATA在2025年報告稱,其位於三鷹東的設施將BIM和FM整合後,在保持完整資產可見性的同時,模型資料量減少了98.8%,從而能夠在標準硬體上實現廣泛的多站點部署。隨著這些工具從試點營運過渡到合約要求,日本的綜合設施管理市場將繼續轉向基於勞動力投入、運作、可預防故障和可衡量的建築成果的定價模式。

高昂的人事費用將限制未來的競爭。

人事費用上漲仍然是日本綜合設施管理市場短期內最明顯的阻礙因素,因為在清潔、保全、檢查和建築營運等領域,人員配備仍然至關重要。許多合約都是基於傳統的人員配置模式設計的,成本轉嫁的柔軟性有限,難以抵銷薪資上漲的壓力。這種壓力在公共部門營運中更為突出,因為公共部門的採購結構往往限制了成本上漲在合約價格中的體現程度。這削弱了提供先進服務的經濟效益,因為如果執行成本的增加沒有得到補償,供應商可能會猶豫是否在合約中部署高技能團隊或數位化支援系統。此外,自動化正在加速向機器人清潔、遠端監控和人工智慧安保的轉變,因為它已成為應對結構性勞動力短缺的一種手段,而不僅僅是提高效率。隨著這種差距的擴大,擁有雄厚財力和技術資源的大型營運商在日本綜合設施管理(IFM)市場中,在保持盈利能力方面將比那些僅僅跟隨成本波動的供應商擁有更大的優勢。

細分市場分析

截至2025年,軟性設施管理(soft FM)佔據了日本綜合設施管理(IFM)市場54.4%的佔有率,而硬體維修)預計到2031年將以7.7%的複合年成長率成長。硬體維修管理的快速擴張源於客戶日益重視由單一負責的供應商協調建築健康、生命週期規劃和工程密集型任務。需求最高的領域是那些需要比基本定期檢查更先進的技術營運模式的領域,例如老舊資產、維修需求和性能主導維護。 NTT Data在三鷹東工廠的研究表明,將BIM與FM整合可以在保持資產完全可見性的同時,將模型資料量減少98.8%。這使得在大規模資產組合中更廣泛地部署硬體維修服務成為可能,而不會對系統造成過重的負擔。 NTT Facilities和NTT Docomo也在試行使用互動式人工智慧來存取建築資訊。這減少了在日常設施管理營運中使用BIM資料的工作量,並提高了工程師提供的服務品質。

軟性設施管理涵蓋清潔、餐飲、廢棄物處理、前台支援及相關日常服務,在日本綜合設施管理(IFM)市場中仍佔據相當大的佔有率,因為這些服務與建築物的日常運作息息相關。即使租戶預算趨於緊張,這些服務也難以長期推遲,因為它們直接影響衛生、住戶體驗和基本合規性。此外,軟性服務通常是客戶在擴展到更專業的技術範圍之前首先整合的服務,因此該領域也非常適合簽訂綜合合約。這為希望與客戶建立長期合作關係並在現場長期駐留,最終簽訂大規模管理服務合約的供應商提供了一個切實可行的切入點。從這個意義上講,即使硬性設施管理(硬體維修)在服務組合中成長更為迅速,軟性設施管理在日本綜合設施管理行業中仍然扮演著至關重要的角色。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基礎設施日益老化,推動了對外包的需求。

- 預測性維護的需求預測準確性

- 政府能源政策和企業設施管理服務需求,旨在改善綜合服務

- 本地技術/管理服務正在快速成長。

- 由於資料中心的擴張,設施管理(FM)專業化應運而生。

- 由於日本人口老化,對醫療和社會福利機構的需求增加。

- 市場限制因素

- 高昂的人事費用將限制未來的競爭。

- 嚴格的建築規範導致合規成本增加。

- 細分領域設施管理人員短缺

- 過時的績效指標阻礙了行政營運(CAFM)

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 按服務類型

- 硬體設施管理

- 資產管理

- 機電/暖通空調服務

- 消防系統和安全措施

- 其他硬體維修服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟調頻服務

- 硬體設施管理

- 最終用戶

- 商業的

- 飯店業

- 公共設施和公共基礎設施

- 醫療保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Compass Group PLC

- ISS A/S

- Sodexo SA

- Mitsui Fudosan Facilities Co., Ltd.

- Tokyu Community Corp.

- Mitsubishi Estate Facilities Co., Ltd.

- Sumitomo Mitsui Construction Facilities Co., Ltd.

- NTT Facilities, Inc.

- Secom Co., Ltd.

- Daikin Facilities Co., Ltd.

- Kajima Tatemono Sogo Kanri Co., Ltd.

- Obayashi Facilities Co., Ltd.

- Tokyu Livable, Inc.

- AEON Delight Co., Ltd.

- Hakuyo Facilities Management Co., Ltd.

- Nihon Housing Co., Ltd.

- Meiwa Facilities Co., Ltd.

- Shinryo Corporation

- Daiwa House Group Facilities Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan integrated facility management market size is expected to increase from USD 30.15 billion in 2025 to USD 32.05 billion in 2026 and reach USD 44.77 billion by 2031, growing at a CAGR of 6.91% over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

Japan Integrated Facility Management Market Trends and Insights

Rising Aging Infrastructure Driving Outsourcing Demand

Aging commercial buildings are creating a long-duration outsourcing base for the Japan integrated facility management market because older assets need more coordinated upkeep and stricter maintenance planning. Seismic reinforcement, MEP upgrades, fire safety work, and sanitation obligations are harder to manage when handled by disconnected vendors, especially in large, occupied properties that cannot tolerate service disruptions. Asset owners are therefore moving toward integrated providers that can handle multiple technical scopes within a single contract and maintain documentation aligned with statutory requirements. This shift also improves contract stickiness because clients place value on single-point accountability, lifecycle visibility, and fewer operational handoffs across the building portfolio. In practice, the aging stock in Tokyo, Osaka, and Nagoya is supporting a wider role for providers that can combine building engineering oversight with scheduled compliance execution. That keeps the Japan integrated facility management (IFM) market tied not only to routine services but also to recurring upgrade cycles across mature urban assets.

Growing Demand for Predictive Maintenance Accuracy

Predictive maintenance is becoming a practical growth lever in the Japan integrated facility management market because it helps providers shift from scheduled inspections to condition-based intervention. This matters more in Japan because aging building systems, labour scarcity, and the need for technical reliability raise the cost of reactive maintenance failure. NTT Docomo and NTT Facilities began field validation in April 2026 of a conversational AI system that uses Graph RAG and multi-agent processing to let staff query BIM data in natural language across seven NTT Docomo buildings. The model is important because it lowers the training barrier for non-specialist FM personnel while improving access to asset health information in daily operations. NTT Data also reported in 2025 that BIM-FM integration at its Mitaka East facility reduced model data size by 98.8% while preserving full asset visibility, supporting broader multi-site deployment on standard hardware. As these tools move from pilot use to contract expectations, the Japan IFM market will keep moving toward pricing based on uptime, prevented failures, and measurable building outcomes rather than labour input alone.

High Labor Costs Limiting Future Competitiveness

Labor cost inflation remains the clearest near-term restraint on the Japan integrated facility management market because staffing is still essential across cleaning, security, inspections, and building operations. Wage pressure is difficult to offset when many contracts were designed around traditional labour deployment and low pass-through flexibility. The pressure is more visible in public-sector work, where procurement structures often limit how much cost inflation can be reflected in contract pricing. That weakens the economics of advanced service delivery because providers may hesitate to place higher-skilled teams or digital support layers into contracts that do not compensate for rising execution costs. It also accelerates the push toward robotic cleaning, remote monitoring, and AI-assisted security because automation becomes a hedge against structurally tight labour supply rather than a simple efficiency upgrade. As that divide widens, scale operators with funding and technology will be better placed than cost-reactive providers to defend margins in the Japan integrated facility management (IFM) market.

Other drivers and restraints analyzed in the detailed report include:

- Government Energy and Corporate FM Service Needs Are Improving Integrated Services

- Local Technology and Managed Services Are Growing Rapidly

- Stringent Building Codes Increasing Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management (FM) held 54.4% of the Japan integrated facility management market share in 2025, while Hard FM is projected to grow at a 7.7% CAGR through 2031. Hard FM is expanding faster because clients are giving more weight to building integrity, lifecycle planning, and the coordination of engineering-heavy scopes under one accountable provider. Demand is strongest where aging assets, retrofit requirements, and performance-led maintenance need a deeper technical operating model than basic scheduled servicing. NTT Data's work at the Mitaka East facility showed that BIM-FM integration can preserve full asset visibility while cutting model data size by 98.8%, which supports broader hard service deployment across large portfolios without a heavy system burden. NTT Facilities and NTT Docomo are also testing conversational AI for building information access, which can reduce the friction of using BIM data in day-to-day FM work and improve the quality of technician responses.

Soft Facility Management remains the foundational volume layer of the Japan IFM market because cleaning, catering, waste management, front-of-house support, and related recurring services are tied to daily building continuity. Even when occupiers tighten budgets, these functions are difficult to defer for long because they directly affect hygiene, occupant experience, and baseline compliance. The segment also fits integrated contracts well because soft services are often the first bundle clients consolidate before they expand into more technical scopes. That creates a practical entry route for providers that want to deepen account coverage over time and turn recurring site presence into larger managed service relationships. In that sense, Soft FM continues to anchor the Japan integrated facility management industry even as Hard FM becomes the faster-growing part of the service mix.

List of Companies Covered in this Report:

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Compass Group PLC

- ISS A/S

- Sodexo S.A.

- Mitsui Fudosan Facilities Co., Ltd.

- Tokyu Community Corp.

- Mitsubishi Estate Facilities Co., Ltd.

- Sumitomo Mitsui Construction Facilities Co., Ltd.

- NTT Facilities, Inc.

- Secom Co., Ltd.

- Daikin Facilities Co., Ltd.

- Kajima Tatemono Sogo Kanri Co., Ltd.

- Obayashi Facilities Co., Ltd.

- Tokyu Livable, Inc.

- AEON Delight Co., Ltd.

- Hakuyo Facilities Management Co., Ltd.

- Nihon Housing Co., Ltd.

- Meiwa Facilities Co., Ltd.

- Shinryo Corporation

- Daiwa House Group Facilities Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Aging Infrastructure, Citing Outsourcing Demand

- 4.2.2 Accuracy of Demand of the Predictive Maintenance

- 4.2.3 Government Energy/Corporate FM Service Needs for Improving Integrated Services

- 4.2.4 Local Technology/Managed Services Growing Rapidly

- 4.2.5 Expansion of Data Centers Resulting in FM Specialization

- 4.2.6 Rising Healthcare and Institutional Facility Requirements Amid Japan's Aging Demographics

- 4.3 Market Restraints

- 4.3.1 High Labor Costs Limiting Future Competitiveness

- 4.3.2 Stringent Building Codes Increasing Compliance Costs

- 4.3.3 Shortage of FM Talent for Niche Services

- 4.3.4 Outdated Performance Metrics Hindering Administration (CAFM)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group, Inc.

- 6.4.2 Jones Lang LaSalle Incorporated

- 6.4.3 Compass Group PLC

- 6.4.4 ISS A/S

- 6.4.5 Sodexo S.A.

- 6.4.6 Mitsui Fudosan Facilities Co., Ltd.

- 6.4.7 Tokyu Community Corp.

- 6.4.8 Mitsubishi Estate Facilities Co., Ltd.

- 6.4.9 Sumitomo Mitsui Construction Facilities Co., Ltd.

- 6.4.10 NTT Facilities, Inc.

- 6.4.11 Secom Co., Ltd.

- 6.4.12 Daikin Facilities Co., Ltd.

- 6.4.13 Kajima Tatemono Sogo Kanri Co., Ltd.

- 6.4.14 Obayashi Facilities Co., Ltd.

- 6.4.15 Tokyu Livable, Inc.

- 6.4.16 AEON Delight Co., Ltd.

- 6.4.17 Hakuyo Facilities Management Co., Ltd.

- 6.4.18 Nihon Housing Co., Ltd.

- 6.4.19 Meiwa Facilities Co., Ltd.

- 6.4.20 Shinryo Corporation

- 6.4.21 Daiwa House Group Facilities Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)