|

市場調查報告書

商品編碼

2064464

日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Japan GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

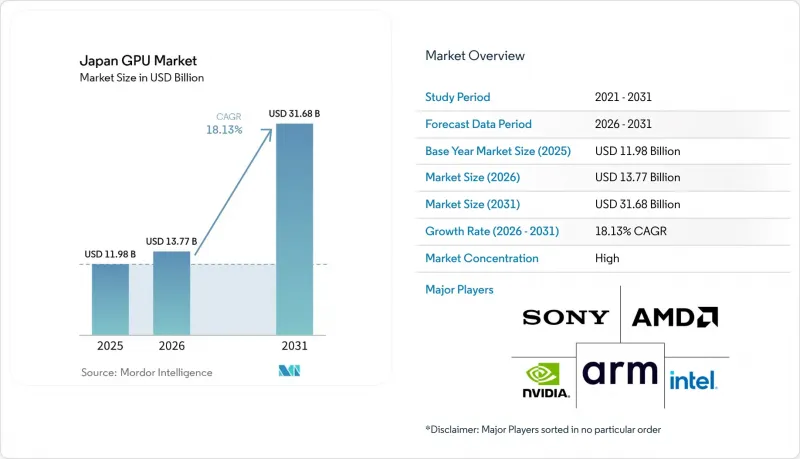

根據 Mordor Intelligence 預測,日本 GPU 市場規模將從 2025 年的 119.8 億美元成長到 2026 年的 137.7 億美元,到 2031 年將達到 316.8 億美元,2026 年至 2031 年的複合年成長率為 18.13%。

本報告按整合類型(整合GPU、獨立GPU)和裝置應用(行動裝置和平板電腦、PC和工作站、伺服器和資料中心加速器、遊戲主機和掌上型遊戲機、汽車/ADAS以及其他嵌入式和邊緣裝置)進行細分。市場預測以美元計價。

日本GPU市場的趨勢與洞察

日本公司人工智慧/機器學習訓練工作量的激增

為了遵守《個人資訊保護法》,銀行、汽車製造商和生命科學公司紛紛將資料中心遷移到配備高階加速器的國內資料中心。 GENIAC計畫的補貼降低了資本支出,使得SAKURA Internet和KDDI等區域性雲端服務供應商能夠在不將敏感資料傳輸到海外的情況下部署配備NVIDIA H200顯示卡的機架。軟銀的1000 GPU叢集和微軟承諾的100億美元基礎設施投資進一步推動了這項需求。光是豐田的「Woven City」模擬中心預計到2025年就將消耗超過500張A100S顯示卡,凸顯了研發工作負載對國內處理能力的依賴程度。

政府補貼用於將國內半導體供應鏈遷回日本

日本經濟產業省已累計1.23兆日圓(約79.7億美元)用於晶圓製造,其中7,320億日圓將投資於台積電熊本廠,9,200億日圓將投資於Rapidus的2nm生產線。台積電計畫於2025年底開始量產其3nm工藝,並為AMD Instinct MI300顯示卡提供基板;Rapidus的目標是在2027年實現其2nm工藝的量產。在日本,晶圓良率的穩定還需要數年時間,但預計到2020年代中期,這一藍圖將降低日本對海外供應的依賴,使國內系統整合商能夠更便捷地獲得供應。

2nm/3nm製程節點產能持續短缺

台積電的CoWoS生產線目前接近滿載運作,Blackwell和Hopper GPU的前置作業時間長達78週。蘋果、英偉達和AMD已經鎖定了2nm流程的訂單,直到2027年,這使得日本無晶圓廠新創公司難以獲得早期訂單。三星的3nm製程良率仍低於85%,導致顧客不願拓展供應鏈。在Rapidus實現量產之前,系統整合商要麼需要延長產品週期,要麼只能重新採用上一代晶片。

細分市場分析

預計到2025年,獨立GPU將佔日本GPU市場67.59%的銷售額,凸顯其在大規模AI訓練領域的統治地位。隨著NVIDIA Blackwell平台(擁有2080億個電晶體和10TB/s的NVLink傳輸能力)的逐步普及,超大規模資料中心業者資料中心紛紛在機架中部署可升級的擴展卡,獨立GPU的統治地位將進一步鞏固。 AMD的MI350X為推理處理提供了一種經濟高效的選擇,有助於雲端服務領域的挑戰者分散對供應商的依賴。同時,整合GPU在超薄筆記型電腦和汽車等對散熱要求較高的環境中仍然佔據主導地位。瑞薩電子的R-Car Gen 5預計在2027年後推動整合GPU在高級駕駛輔助功能方面取得突破。然而,這仍然不足以彌補資料中心工作負載所需的效能差距。

雖然獨立顯示卡仍然是預算有限的工作站和電競咖啡館實現 400Hz影格速率的首選,但行動裝置和平板電腦的設計則依賴整合 SoC 圖形處理器來平衡電池續航時間。蘋果的 M4 和高通的驍龍 X Elite 晶片組目前的吞吐量已可與入門級獨立顯卡相媲美,這表明低功耗領域整合度已臻於極致。由於記憶體頻寬的限制,整合架構無法在高階市場取代專用加速器。因此,預計到 2031 年,獨立顯示卡仍將是日本 GPU 市場的主要收入來源。

其他福利

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 日本公司人工智慧/機器學習訓練工作量的激增

- 政府補貼用於將國內半導體供應鏈遷回日本

- 高影格速率PC遊戲咖啡館的蓬勃發展是由電子競技推動的。

- 人工智慧驅動的行動應用迅速普及

- 整合基於GPU的視覺功能的汽車SoC晶片正在擴展,以用於ADAS(高級駕駛輔助系統)。

- 日本製造業身臨其境型3D設計工具的發展

- 市場限制因素

- 2nm/3nm製程節點產能持續短缺

- 能源效率法規限制了資料中心的電力預算。

- 日圓匯率波動導致進口GPU的平均售價上漲。

- 高階人工智慧加速器的出口限制

- 產業價值/價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按類型整合

- 整合顯示卡(iGPU)

- 獨立GPU(dGPU)

- 裝置應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Sony Group Corporation

- Nintendo Co., Ltd.

- Fujitsu Limited

- NEC Corporation

- Arm Ltd.

- Qualcomm Incorporated

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Micro-Star International Co., Ltd.(MSI)

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- ZOTAC Technology Limited

- Acer Incorporated

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Imagination Technologies Limited

- Renesas Electronics Corporation

- Broadcom Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan gPU market size is expected to increase from USD 11.98 billion in 2025 to USD 13.77 billion in 2026 and reach USD 31.68 billion by 2031, growing at a CAGR of 18.13% over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

Japan GPU Market Trends and Insights

Surging AI/ML Training Workloads Across Japanese Enterprises

Compliance with the Act on the Protection of Personal Information is steering banks, automakers, and life-science firms toward sovereign datacenters equipped with high-end accelerators. Subsidies under the GENIAC program cut capital outlays, letting regional cloud providers such as SAKURA Internet and KDDI deploy racks of NVIDIA H200 cards without offshoring sensitive data. SoftBank's 1,000-GPU cluster and Microsoft's USD 10 billion infrastructure pledge further anchor demand. Toyota's Woven City simulation hub alone consumed more than 500 A100S in 2025, underscoring how R&D workloads now hinge on domestic capacity.

Government Subsidies for Domestic Semiconductor Supply Chain Re-Shoring

The Ministry of Economy, Trade and Industry has earmarked JPY 1.23 trillion (USD 7.97 billion) for wafer fabs, channeling JPY 732 billion into TSMC's Kumamoto site and JPY 920 billion into Rapidus' 2-nm line. TSMC began 3-nm output in late 2025, shipping substrates for AMD Instinct MI300 cards, while Rapidus targets 2-nm production by 2027. JP. Although yields will take years to mature, the roadmap promises mid-decade relief from overseas dependency, positioning local integrators to capture supply closer to home.

Ongoing 2 nm/3 nm Process Node Capacity Shortages

TSMC's CoWoS lines now run at near-full load, stretching lead times for Blackwell and Hopper GPUs to as long as 78 weeks. Apple, NVIDIA, and AMD have already block-booked 2-nm slots through 2027, denying Japanese fabless start-ups early access. Samsung's 3-nm yields remain under 85%, deterring customers from diversifying supply. Until Rapidus ramps, integrators must elongate product cycles or revert to prior-generation silicon.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Automotive SoCs Integrating GPU-Based Vision for ADAS

- Rapid Uptake of Generative-AI-Enabled Mobile Apps

- Energy-Efficiency Regulations Limiting Datacenter Power Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs captured 67.59% of 2025 revenue, highlighting their primacy in large-scale AI training within the Japan GPU market share. Ongoing migration to NVIDIA's Blackwell platform, with 208 billion transistors and 10 TB/s NVLink, cements this lead as hyperscalers fill racks with upgradeable add-in boards. AMD's MI350X provides a cost-advantaged option for inference, helping cloud challengers diversify vendor exposure. Meanwhile, integrated GPUs prevail in thermally constrained environments such as ultraportable notebooks and automobiles. Renesas R-Car Gen 5 will propel integrated units into higher tiers of driver-assistance from 2027, albeit without threatening the performance gulf that datacenter workloads demand.

Budget-sensitive workstations and esports cafes still prefer discrete cards to hit 400-Hz frame rates, while mobile and tablet designs rely on SoC-embedded graphics to balance battery life. Apple's M4 and Qualcomm's Snapdragon X Elite chipsets now match entry-level discrete throughput, signaling eventual convergence in low-power segments. Nevertheless, memory bandwidth ceilings keep integrated architectures from replacing dedicated accelerators at the top end. Therefore, discrete units will remain the principal revenue engine for the Japan GPU market size through 2031.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Sony Group Corporation

- Nintendo Co., Ltd.

- Fujitsu Limited

- NEC Corporation

- Arm Ltd.

- Qualcomm Incorporated

- ASUSTeK Computer Inc.

- Giga-Byte Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- ZOTAC Technology Limited

- Acer Incorporated

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Imagination Technologies Limited

- Renesas Electronics Corporation

- Broadcom Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI/ML Training Workloads Across Japanese Enterprises

- 4.2.2 Government Subsidies for Domestic Semiconductor Supply Chain Re-Shoring

- 4.2.3 Esports-Led Boom in High-Frame-Rate PC Gaming Cafes

- 4.2.4 Rapid Uptake of Generative-AI-Enabled Mobile Apps

- 4.2.5 Expansion of Automotive SoCs Integrating GPU-Based Vision for ADAS

- 4.2.6 Growth of Immersive 3D Design Tools in Japan's Manufacturing Sector

- 4.3 Market Restraints

- 4.3.1 Ongoing 2 nm/3 nm Process Node Capacity Shortages

- 4.3.2 Energy-Efficiency Regulations Limiting Datacenter Power Budgets

- 4.3.3 Yen Volatility Raising Imported GPU ASPs

- 4.3.4 Export-Control Restrictions on High-End AI Accelerators

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Existing Competitors

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Sony Group Corporation

- 6.4.5 Nintendo Co., Ltd.

- 6.4.6 Fujitsu Limited

- 6.4.7 NEC Corporation

- 6.4.8 Arm Ltd.

- 6.4.9 Qualcomm Incorporated

- 6.4.10 ASUSTeK Computer Inc.

- 6.4.11 Giga-Byte Technology Co., Ltd.

- 6.4.12 Micro-Star International Co., Ltd. (MSI)

- 6.4.13 Dell Technologies Inc.

- 6.4.14 Hewlett Packard Enterprise Company

- 6.4.15 Lenovo Group Limited

- 6.4.16 ZOTAC Technology Limited

- 6.4.17 Acer Incorporated

- 6.4.18 Apple Inc.

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 Imagination Technologies Limited

- 6.4.21 Renesas Electronics Corporation

- 6.4.22 Broadcom Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析 東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)