|

市場調查報告書

商品編碼

2065507

菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Philippines Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

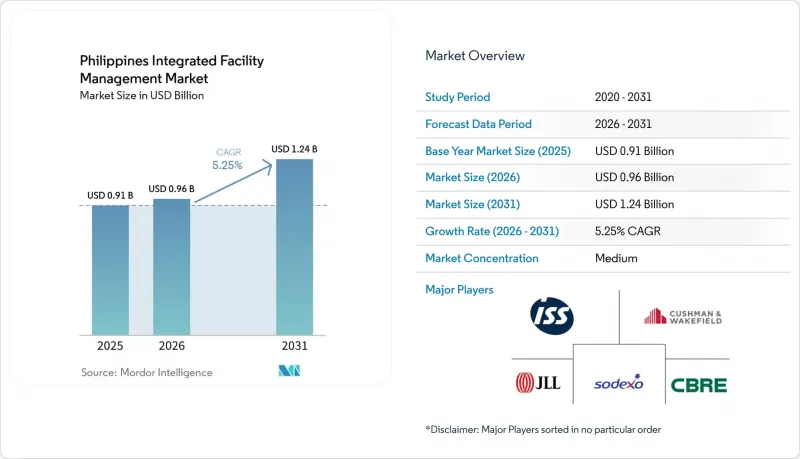

預計到 2025 年,菲律賓綜合設施管理市場規模將達到 9.1 億美元,到 2026 年將達到 9.6 億美元,到 2031 年將達到 12.4 億美元,2026 年至 2031 年的複合年成長率為 5.25%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和保全、清潔服務、餐飲服務等])和最終用戶(商業設施、旅館、公共機構和公共基礎設施等)進行分類。市場預測以美元計價。

菲律賓整合性機構管理市場趨勢及洞察

擴大基礎設施建設和擴建管道

菲律賓政府大力推動基礎建設,推動了菲律賓整合性機構管理市場的發展。這是因為新建的鐵路、碼頭和公共產業設施即使在完工後仍會產生持續的服務需求。截至2026年1月,官民合作關係(PPP)專案儲備顯著增加,專案範圍涵蓋了更廣泛的資產,這些資產將隨著時間的推移逐步過渡到營運和維護階段。 2026年5月,政府進一步宣布了總額達3.16兆菲律賓披索(約546億美元)的252個專案計畫。其中,鐵路開發案佔比最大。這一點意義重大,因為特許經營者通常傾向於專注於提供運輸服務和營運資產,而不是在每個地點建立大規模的內部設施管理團隊。能夠將技術維護、資產管理、清潔和保全等服務整合起來的供應商,在這些設施投入運作後,將更有利於贏得大宗訂單。因此,隨著目前在建項目過渡到更廣泛的運作中公共資產,預計 2027 年至 2030 年間採購活動將進一步活性化。

商業辦公室業務流程外包 (BPO) 和外包的發展趨勢

菲律賓綜合設施管理市場持續受益於辦公大樓領域的外包模式,尤其是大規模租戶更傾向於在多層辦公大樓和園區辦公室獲得可預測的服務標準。受IT和BPM產業需求以及全球服務中心快速擴張的推動,預計到2025年,馬尼拉大都會區的辦公大樓交易面積將達到84.7萬平方公尺。隨著營運商在巴科洛德等城市和其他成熟服務地點增加服務能力,業務拓展至區域範圍,合約範圍已從宿霧和達沃擴展到其他地區。這意義重大,因為BPO的需求不再局限於基本的辦公室支援。醫療資訊管理、人工智慧營運和軟體開發環境需要更精準的溫度控制、更可靠的電力供應和更乾淨的室內空氣。這些變化提高了現有辦公室和新租賃辦公室的設施管理(FM)標準,從而凸顯了採用綜合服務合約而非單一服務供應商的優勢。由於北美仍是IT-BPM投資的主要來源,因此市場需求仍面臨美國政策風險。因此,供應商們正擴大檢驗他們的收入計劃,以應對客戶成長速度放緩的情況。

技術純熟勞工短缺和工資上漲

菲律賓綜合設施管理市場持續面臨勞動力短缺的困境,尤其是持證機電(機械、電氣和管道)工程師和高級技術主管嚴重短缺。在主要商業區,這一問題尤其突出,專業職位可能長期空缺,而經驗豐富的工程人員要求的薪資遠高於市場標準。海外需求加劇了這一短缺,因為海灣地區的雇主為類似的工程和施工管理職位提供的薪資遠高於菲律賓。這種人才流失減少了能夠處理技術要求高的專案(例如醫院、工業廠房和資料中心)的經驗豐富的專業人員的供應。這也限制了國內供應商從軟性服務轉向更複雜的硬體維修業務的速度。同時,薪資上漲的壓力正在降低固定價格合約的利潤率,因此,儘管一些公共部門買家持續反對,供應商仍在推動引入年度價格調整條款。

細分市場分析

截至2025年,軟性綜合設施管理(FM)在菲律賓綜合設施管理(IFM)市場中佔據68.41%的佔有率。同時,硬體維修)預計到2031年將以6.07%的複合年成長率成長。這一收入結構反映了菲律賓IFM行業的基本客群,其中辦公租戶、酒店和主導設施仍然佔據活躍合約的大部分。清潔、辦公室支援和保全服務由於其頻繁的需求和在商業設施中的廣泛應用,仍然是核心收入來源。與更容易受經濟波動影響的專案型工作相比,這些服務為供應商提供了更多的持續合約和穩定的現金流。餐飲服務仍集中在工業廠房、醫院和大規模業務流程外包(BPO)園區,這些場所的現場供餐有助於保障員工福祉和營運連續性。

由於新型資產類別對機電、暖通空調、消防安全和計畫性維護的技術要求不斷提高,硬體維修)的成長正在加速。資料中心、鐵路系統和醫院設施的建設提升了工程技術在菲律賓綜合設施管理(IFM)市場的重要性,促使買家轉向預防性維護和資產管理模式。在硬體維修管理領域,資產管理和機電/暖通空調服務是收入最集中的領域,因為工業、交通和醫療設施的停機時間會直接影響營運。消防安全和生命安全服務的收入佔比仍然較小,但由於所有公共和私人建築都必須遵守相關規定,因此其需求基礎穩定。其他硬體維修服務,包括土木工程維護和外觀工程,隨著建築環境的擴張而不斷發展,但與技術建築系統服務相比,其差異化程度仍然較低。菲律賓建築承包商協會(PCAB)的「四A」級認證以及品質、環境和安全方面的正式認證對大規模公共產業和政府客戶仍然至關重要,這使得高階服務類別的選擇更加嚴格。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 更好的基礎設施建設和管道擴建

- 商業辦公室業務流程外包 (BPO) 和外包的發展趨勢

- 醫療設施的擴建和現代化

- 引進利用智慧建築和物聯網的設施管理

- 強制性ESG與綠建築認證

- 擴展超大規模資料中心的容量

- 市場限制因素

- 技術純熟勞工短缺和工資上漲

- 電網能源成本波動

- 供應商分佈廣泛,價格競爭激烈。

- 根據《能源效率和節能法》進行的審計所帶來的合規負擔

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全措施

- 其他硬設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬設施管理

- 按最終用戶行業分類

- 商業

- 飯店業

- 機構和公共基礎設施

- 衛生保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 策略趨勢

- 市佔率分析

- 公司簡介

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- ISS A/S

- Sodexo SA

- Atalian Global Services Philippines Inc.

- Servicio Filipino Inc.

- Meralco Industrial Engineering Services Corporation

- SGS Philippines, Inc.

- Santos Knight Frank, Inc.

- Century Properties Management, Inc.

- G4S Secure Solutions(Philippines), Inc.

- KMC Solutions Holdings, Inc.

- Mansion Maintenance Company, Inc.

- Kontrac Facilities Management Services, Inc.

- Hydron Corporation

- WeCare Facility Management Services, Inc.

- Artelia Group

- CPMGI

- Kabraso Multi-Purpose Cooperative

第7章 市場機會與未來展望

According to Mordor Intelligence, the philippines integrated facility management market size is projected to be USD 0.91 billion in 2025, USD 0.96 billion in 2026, and reach USD 1.24 billion by 2031, growing at a CAGR of 5.25% from 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Integrated Facility Management Market Trends and Insights

Build Better More Infrastructure Pipeline Expansion

The Philippines integrated facility management market is drawing support from the government's broader infrastructure build-out because new rail, terminal, and utility assets create recurring service demand after construction ends. The PPP pipeline expanded materially by January 2026, and the project base now covers a larger set of assets that move into operating and maintenance phases over time. In May 2026, the administration also unveiled a PHP 3.16 trillion (USD 54.6 billion) project pipeline, across 252 projects, with railway development taking the largest value share in that list. That matters because concessionaires usually focus on transport delivery and asset operation rather than building large in-house FM teams across every location. Providers that can combine technical maintenance, asset management, cleaning, and security are better positioned to win bundled work as these facilities come online. Procurement activity is therefore likely to deepen between 2027 and 2030, when today's construction pipeline converts into a broader installed base of operating public assets.

Outsourcing Trend Among BPO and Commercial Offices

The Philippines integrated facility management market continues to benefit from the outsourcing practices of the office sector, especially where large occupiers prefer predictable service standards across multi-floor or campus-style sites. Metro Manila office transactions reached 847,000 sqm in 2025, and that recovery was supported by IT-BPM demand and faster expansion from Global Capability Centers. Provincial expansion also widened the contract map beyond Cebu and Davao, as operators added capacity in cities such as Bacolod and across other established delivery locations. This matters because BPO requirements are no longer limited to basic occupancy support, since healthcare information management, AI operations, and software development environments require better thermal control, more dependable power support, and cleaner indoor air. Those changes raise the FM specification of both existing and newly leased sites, which strengthens the case for integrated service contracts instead of separate single-service vendors. The demand base still carries some exposure to U.S. policy risk because North America remains the main origin of IT-BPM investment, so providers are increasingly testing revenue plans against slower client expansion scenarios.

Skilled-Labor Shortage and Wage Inflation

The Philippines integrated facility management market still faces a labour bottleneck, and the most acute shortage exists in licensed MEP engineers and senior technical supervisors. The problem is more severe in major business districts, where specialist roles can remain open for extended periods and experienced engineering staff command significant pay premiums over standard market benchmarks. Overseas demand worsens the shortage because Gulf employers continue to offer materially higher pay for comparable engineering and construction management roles. That outflow reduces the pool of experienced professionals available for technically demanding contracts in hospitals, industrial plants, and data centers. It also limits how quickly domestic providers can move beyond soft services into more complex hard FM scopes. At the same time, wage pressure weakens margins on fixed-price contracts, which is why providers are pushing for annual escalation clauses, even though some public-sector buyers remain resistant.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare Facility Build-outs and Modernization

- Smart-Building and IoT-Enabled FM Adoption

- Energy-Cost Volatility in the Grid

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft integrated facility management (FM) held 68.41% of the Philippines integrated facility management (IFM) market share in 2025, while Hard FM is projected to expand at a 6.07% CAGR through 2031. That revenue mix reflected the buyer base of the Philippines IFM industry, where office occupiers, hospitality sites, and retail-led facilities still account for a large share of active contracts. Cleaning, office support, and security remained the core revenue generators because they are required at high frequency and across a wide installed base of commercial premises. These services also offered providers repeat contract volumes and steadier cash flow than highly cyclical project-linked work. Catering remained more concentrated in industrial plants, hospitals, and very large BPO campuses where on-site food provision supports workforce welfare and operating continuity.

Hard FM is growing faster because new asset classes carry higher technical obligations in MEP, HVAC, fire safety, and planned maintenance. Data centers, railway systems, and hospital facilities are increasing the engineering intensity of the Philippines IFM market and pushing buyers toward preventive maintenance and asset management models. Within the hard FM stack, asset management and MEP and HVAC services hold the strongest revenue concentration because downtime in industrial, transport, and healthcare sites has direct operating consequences. Fire and life-safety services remain smaller in revenue terms, but they maintain a reliable demand floor because compliance is mandatory across public and private buildings. Other hard FM scopes, including civil maintenance and facade work, are expanding with the built environment, but they remain less differentiated than technical building systems work. PCAB Quadruple A classification and formal quality, environmental, and safety credentials continue to matter for large utility and government accounts, which keeps the top end of the service category more selective.

List of Companies Covered in this Report:

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- ISS A/S

- Sodexo S.A.

- Atalian Global Services Philippines Inc.

- Servicio Filipino Inc.

- Meralco Industrial Engineering Services Corporation

- SGS Philippines, Inc.

- Santos Knight Frank, Inc.

- Century Properties Management, Inc.

- G4S Secure Solutions (Philippines), Inc.

- KMC Solutions Holdings, Inc.

- Mansion Maintenance Company, Inc.

- Kontrac Facilities Management Services, Inc.

- Hydron Corporation

- WeCare Facility Management Services, Inc.

- Artelia Group

- CPMGI

- Kabraso Multi-Purpose Cooperative

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Build Better More Infrastructure Pipeline Expansion

- 4.2.2 Outsourcing Trend Among BPO and Commercial Offices

- 4.2.3 Healthcare Facility Build-outs and Modernization

- 4.2.4 Smart-Building and IoT-Enabled FM Adoption

- 4.2.5 Mandatory ESG and Green-Building Certifications

- 4.2.6 Hyperscale Data-Center Capacity Growth

- 4.3 Market Restraints

- 4.3.1 Skilled-Labor Shortage and Wage Inflation

- 4.3.2 Energy-Cost Volatility in the Grid

- 4.3.3 Fragmented Supplier Base and Price Competition

- 4.3.4 Compliance Burden from Energy Efficiency and Conservation Act Audits

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 CBRE Group, Inc.

- 6.3.2 Jones Lang LaSalle Incorporated

- 6.3.3 Cushman & Wakefield plc

- 6.3.4 ISS A/S

- 6.3.5 Sodexo S.A.

- 6.3.6 Atalian Global Services Philippines Inc.

- 6.3.7 Servicio Filipino Inc.

- 6.3.8 Meralco Industrial Engineering Services Corporation

- 6.3.9 SGS Philippines, Inc.

- 6.3.10 Santos Knight Frank, Inc.

- 6.3.11 Century Properties Management, Inc.

- 6.3.12 G4S Secure Solutions (Philippines), Inc.

- 6.3.13 KMC Solutions Holdings, Inc.

- 6.3.14 Mansion Maintenance Company, Inc.

- 6.3.15 Kontrac Facilities Management Services, Inc.

- 6.3.16 Hydron Corporation

- 6.3.17 WeCare Facility Management Services, Inc.

- 6.3.18 Artelia Group

- 6.3.19 CPMGI

- 6.3.20 Kabraso Multi-Purpose Cooperative

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)