|

市場調查報告書

商品編碼

2064403

歐洲GPU市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Europe GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

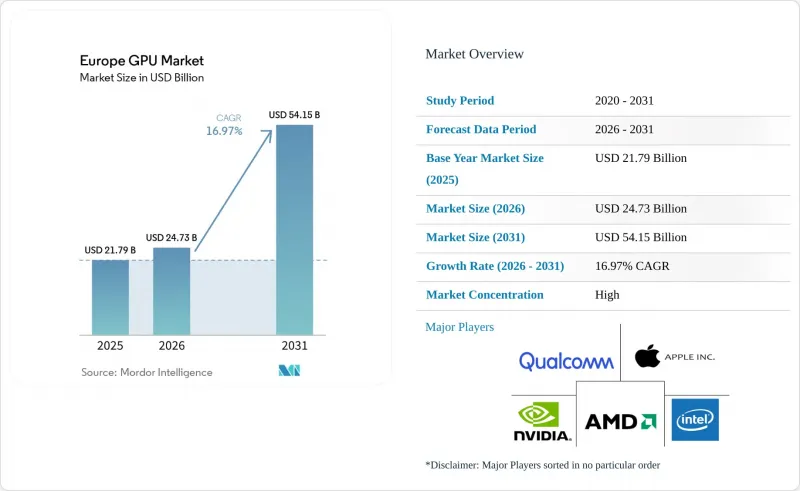

根據 Mordor Intelligence 預測,歐洲 GPU 市場規模預計將在 2025 年達到 217.9 億美元,2026 年達到 247.3 億美元,到 2031 年達到 541.5 億美元,2026 年至 2031 年的複合年成長率為 16.97%。

本報告按整合類型(整合GPU、獨立GPU)、裝置應用(行動裝置/平板電腦、PC/工作站、伺服器/資料中心加速器、遊戲機/掌上遊戲機、汽車/ADAS、其他)和國家(德國、英國、法國、其他)進行細分。市場預測以美元(USD)計價。

歐洲GPU市場趨勢與分析

加速歐洲資料中心採用人工智慧和機器學習工作負載

英國高達 423 億美元的大規模投資,加上法國的數吉瓦級項目,正在為區域伺服器機架增加數萬台 NVIDIA Blackwell 和 AMD Instinct 加速器。 OpenAI 的 Stargate UK 計畫、微軟的超級電腦建設,以及 Mistral AI 和 Sesterce 在法國的部署,都顯示公共和私人投資如何與資料主權要求相契合。營運商傾向於選擇水冷 GPU叢集,以滿足電源使用效率 (PUE)基準值並降低因電費上漲而產生的營運成本。這些大規模採購加速了原本預計在 2020 年代末期才會出現的需求,導致短期出貨量預測上調。總而言之,這些發展有望推動歐洲 GPU 市場走上正軌,到 2028 年,資料中心加速器將佔據區域收入的相當大一部分。

歐盟晶片法的獎勵正在促進歐洲GPU製造領域的投資。

這項耗資430億歐元(約464億美元)的「歐洲晶片法」包含前所未有的設施津貼、稅額扣抵以及用於試點生產線的資金,旨在重振歐洲大陸的半導體產能。雖然目前只有兩個5奈米以下製程的專案獲得批准,但相關的封裝和異構整合生產線正在德累斯頓、格勒諾布爾和諾瓦拉等地建設中。 Silicon Box在義大利投資32億歐元(約35億美元)建設的先進封裝工廠以及意法半導體在法國擴建的晶圓廠,都展現了獨立GPU廠商賴以進行晶片組裝的配套基礎設施建設的強勁勢頭。像SiPearl這樣的無晶圓廠新創公司正在利用這些資源,將歐洲製造的CPU與進口加速器結合,從而加強區域供應鏈並降低一些地緣政治風險。儘管大規模生產仍需數年時間,但這項政策架構已開始影響計畫在2028年至2031年間部署的超大規模資料中心業者的籌資策略。

先進節點地緣政治緊張局勢導致供應鏈中斷

目前,大多數尖端GPU晶圓都由台灣晶圓廠供應,這些晶圓廠依賴氦氣、高數值孔徑EUV光刻機以及集中在少數幾家分包商手中的先進封裝技術。由於沿岸地區的衝突導致氦氣短缺,阻礙了3nm晶圓在2024年下半年的投產,延長了NVIDIA Blackwell和AMD MI300X向歐洲整合商的交付前置作業時間。高頻寬記憶體的短缺進一步限制了板級記憶體的供應,迫使系統供應商在現貨市場支付30%至50%的溢價。由於歐洲晶圓廠在2028年之前沒有大規模生產5nm或更小製程晶圓的預期,超大規模資料中心業者正在建立儲備庫存,但如果再次發生地緣政治事件擾亂台灣晶圓廠,專案仍有可能延遲數月。

細分市場分析

2025年,獨立顯示卡將佔據歐洲GPU市場65.38%的佔有率,隨著超大規模資料中心業者大量訂購NVIDIA Blackwell和AMD Instinct加速器,這一差距也將持續擴大。預計到2031年,歐洲獨立GPU市場將以17.74%的複合年成長率成長,這主要得益於「主權運算」需求,該需求優先考慮能夠進行多千兆次浮點運算級訓練的本地硬體。整合到NVLink機架中的Blackwell B200和B300顯示卡使營運商能夠將模型訓練週期從數週縮短至數天,從而直接縮短大型歐洲語言模型的上市時間。 AMD的Instinct MI300X配備192GB HBM3顯存,頻寬5.2TB/s,可有效解決廣播公司和國防機構面臨的記憶體受限推理挑戰。整合式顯示卡在客戶端 PC 和掌上型遊戲機中仍然很重要,但隨著運算密集型工作負載超過熱設計功率的限制,預計其在歐洲 GPU 市場的佔有率將會下降。

儘管英特爾的 Meteor Lake系統晶片在筆記型電腦中應用廣泛,但其架構性能仍落後於目前配備 600W 級水冷散熱系統的獨立顯示卡。價格趨勢也對獨立顯示卡有利。儘管消費級顯示卡的價格預計將上漲 10-15%,但資料中心級顯示卡的供應優先順序和利潤率仍保持穩定。這種轉變正將獨立顯示卡從傳統的圖形周邊設備提升為歐洲數位主權策略的基石。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 歐洲GPU市場

- 市場促進因素

- 加速歐洲資料中心採用人工智慧和機器學習工作負載

- 歐盟晶片法為本地GPU製造投資提供了獎勵。

- 雲端遊戲和訂閱平台的興起

- 計算電動車對資訊娛樂和ADAS的需求

- 媒體產業向 4K/8K 內容製作工作流程轉型

- 透過開放原始碼GPU驅動程式和生態系統降低企業整體擁有成本

- 市場限制因素

- 先進節點地緣政治緊張局勢導致供應鏈中斷

- 歐洲能源成本上漲對GPU總擁有成本(TCO)的影響

- GPU功耗標準的監管

- 歐洲先進半導體設計領域技術人才短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按整合類型

- 整合顯示卡(iGPU)

- 獨立GPU(dGPU)

- 裝置應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機/掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式邊緣設備

- 按地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 歐洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Arm Holdings plc

- Imagination Technologies Limited

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Apple Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Acer Inc.

- Dell Technologies Inc.

- Lenovo Group Limited

- Huawei Technologies Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe gPU market size is projected to be USD 21.79 billion in 2025, USD 24.73 billion in 2026, and reach USD 54.15 billion by 2031, growing at a CAGR of 16.97% from 2026 to 2031.

This report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and More), and Country (Germany, United Kingdom, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe GPU Market Trends and Insights

Accelerated Adoption of AI And ML Workloads in European Datacenters

Large-scale commitments totaling USD 42.3 billion from the United Kingdom, together with multi-gigawatt projects in France, are adding tens of thousands of NVIDIA Blackwell and AMD Instinct accelerators to regional server racks. OpenAI's Stargate UK, Microsoft's supercomputer build-out, and France-based deployments by Mistral AI and Sesterce illustrate how public and private investments align with data-sovereignty mandates. Operators favor liquid-cooled GPU clusters to meet power-usage-effectiveness thresholds and curb operating expenses driven by high electricity tariffs. The scale of these purchases is pulling forward demand that once sat in the second half of the decade, thereby raising near-term shipment forecasts. Collectively, these rollouts anchor the European GPU market on a trajectory in which datacenter accelerators account for a majority of regional revenue before 2028.

EU Chips Act Incentives Boosting Local GPU Manufacturing Investments

The EUR 43 billion (USD 46.4 billion) European Chips Act offers first-of-a-kind facility grants, tax credits, and pilot-line funding to revive continental semiconductor capacity. Although only two sub-5 nm projects have cleared approval, related packaging and heterogeneous-integration lines in Dresden, Grenoble, and Novara are underway. Silicon Box's EUR 3.2 billion (USD 3.5 billion) advanced-packaging plant in Italy and STMicroelectronics' wafer-fab expansions in France signal momentum on supporting infrastructure that discrete GPU vendors rely on for chiplet assembly. Fabless startups such as SiPearl tap these resources to pair European CPUs with imported accelerators, reinforcing a local supply chain that modestly buffers geopolitical risk. While volume output remains years away, the policy framework has already influenced sourcing strategies for hyperscalers planning 2028-2031 deployments.

Supply Chain Disruptions from Geopolitical Tensions on Advanced Nodes

The majority of leading-edge GPU wafers originate from Taiwanese fabs that rely on helium, high-NA EUV scanners, and advanced packaging capacity concentrated at a handful of subcontractors. Helium shortages tied to Gulf-region conflicts curtailed 3 nm wafer starts in late 2024, extending lead times for NVIDIA Blackwell and AMD MI300X shipments to European integrators. Scarcity of high-bandwidth memory further constrains board-level availability, forcing system vendors to pay 30%-50% premiums on the spot market. With no European fab expected to ship sub-5 nm volume before 2028, hyperscalers maintain contingency buffers yet still risk multi-month project delays should another geopolitical event disrupt Taiwanese foundries.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Cloud Gaming and Subscription Platforms

- Electric Vehicle Infotainment and ADAS Compute Demand

- Escalating Energy Costs in Europe Impacting GPU TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete devices captured 65.38% of Europe GPU market share in 2025 and continue to widen the gap as hyperscalers place bulk orders for NVIDIA Blackwell and AMD Instinct accelerators. Europe GPU market size for discrete units is projected to expand at a 17.74% CAGR to 2031, supported by sovereign-compute mandates that prioritize on-premises hardware capable of multi-petaflop training. Blackwell B200 and B300 cards, paired in NVLink racks, let operators shrink model training cycles from weeks to days, directly boosting time-to-market for European large language models. AMD's Instinct MI300X, with 192 GB of HBM3 at 5.2 TB/s, answers memory-bound inference challenges faced by broadcasters and defense agencies. Integrated GPUs remain critical in client PCs and handheld consoles, yet their share of the European GPU market size is projected to decline as compute-intensive workloads outpace their thermal budgets.

Intel's Meteor Lake system-on-chips, though prevalent in laptops, cannot match the architectural headroom of discrete boards that now ship with 600 W-class liquid-cooling loops. Pricing dynamics also favor discrete parts; despite a 10%-15% list-price increase announced for consumer cards, datacenter SKUs enjoy steady allocation priority and premium margins. This shift elevates discrete designs from a traditional graphics accessory to a cornerstone of Europe's digital-sovereignty strategy.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Arm Holdings plc

- Imagination Technologies Limited

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Apple Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Acer Inc.

- Dell Technologies Inc.

- Lenovo Group Limited

- Huawei Technologies Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Europe GPU Market

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of AI and ML Workloads in European Datacenters

- 4.2.2 EU Chips Act Incentives Boosting Local GPU Manufacturing Investments

- 4.2.3 Rise of Cloud Gaming and Subscription Platforms

- 4.2.4 Electric Vehicle Infotainment and ADAS Compute Demand

- 4.2.5 Migration to 4K/8K Content Creation Workflows Across Media Sector

- 4.2.6 Open-source GPU Drivers and Ecosystems Lowering TCO for Enterprises

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions from Geopolitical Tensions on Advanced Nodes

- 4.3.2 Escalating Energy Costs in Europe Impacting GPU TCO

- 4.3.3 Regulatory Scrutiny over GPU Power Consumption Standards

- 4.3.4 Talent Shortage in Advanced Semiconductor Design in Europe

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products or Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

- 5.3 By Geography

- 5.3.1 Europe

- 5.3.1.1 Germany

- 5.3.1.2 United Kingdom

- 5.3.1.3 France

- 5.3.1.4 Italy

- 5.3.1.5 Rest of Europe

- 5.3.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Arm Holdings plc

- 6.4.5 Imagination Technologies Limited

- 6.4.6 Qualcomm Technologies Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 Apple Inc.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Micro-Star International Co. Ltd.

- 6.4.11 Sapphire Technology Limited

- 6.4.12 Palit Microsystems Ltd.

- 6.4.13 Acer Inc.

- 6.4.14 Dell Technologies Inc.

- 6.4.15 Lenovo Group Limited

- 6.4.16 Huawei Technologies Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析 東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)