|

市場調查報告書

商品編碼

2064400

北美GPU市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)North America GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

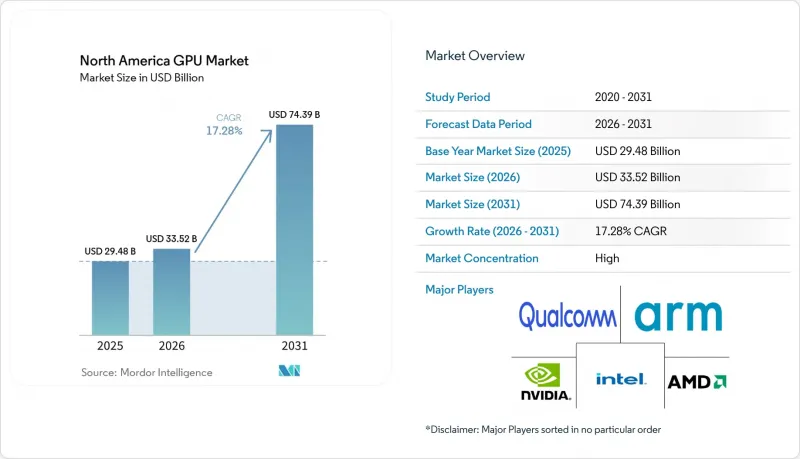

根據 Mordor Intelligence 預測,北美 GPU 市場規模將從 2025 年的 294.8 億美元和 2026 年的 335.2 億美元成長到 2031 年的 743.9 億美元,2026 年至 2031 年的複合年成長率為 17.28%。

本報告按整合類型(整合GPU、獨立GPU)、裝置應用(行動裝置/平板電腦、PC/工作站、伺服器/資料中心加速器、家用/掌上型遊戲機、汽車/DAS、其他)和國家(美國、加拿大、墨西哥)進行細分。市場預測以美元(USD)為單位。

北美GPU市場趨勢與分析

人工智慧主導資料中心GPU採購量激增

隨著人工智慧模式規模的擴大,超大規模資料中心業者正將原本長達數年的硬體升級週期縮短至18個月。 xAI在孟菲斯運作了名為「Colossus」的資料中心,該資料中心由55.5萬塊NVIDIA H100 GPU組成,耗電量達150兆瓦,每個機架的液冷迴路成本高達1.2萬美元。 IREN在德克薩斯州訂購的15萬塊GPU利用了每千瓦時0.018美元的電力成本,與沿海地區相比,營運成本降低了70%。亞馬遜將其100萬塊GPU的採購拆分為NVIDIA H200和AMD MI325X兩種組件,以分散供應風險並爭取批量折扣。雖然此類大宗交易推高了平均售價,但季度出貨量仍然波動較大,因為單一項目的延誤可能導致兩位數的需求下降。這種集中化正在推動北美GPU市場收入的快速成長,但也增加了預測的風險。

高清雲端遊戲服務的普及

雲端平台正從共用虛擬化轉向專用加速器,以維持 4K 120fps 的串流播放。 NVIDIA 基於 RTX 5080 節點的 GeForce NOW Ultimate 計劃在推出八週內就實現了 15 分鐘的等待時間,這促使其在奧勒岡州斥資 4 億美元進行擴張。微軟的 Xbox 雲端遊戲預計到 2025 年將在該地區擁有 280 萬用戶,但其每個用戶所需的 GPU 數量比競爭對手多 40%,這引發了人們對單位經濟效益的擔憂。由於每個用戶消耗的資金量不成比例,營運商在用戶模式穩定之前暫緩擴大規模。儘管如此,每月 24.99 美元的親民定價使得每塊 GPU 的收入頗具吸引力,從而維持了北美 GPU 市場的穩定需求。

先進HBM和GDDR7記憶體供應鏈中的漏洞

目前瓶頸不在於光刻技術,而是高頻寬記憶體。 SK海力士的HBM4良率低於60%,每月僅能生產12,000片晶圓,僅相當於NVIDIA H200加速器需求的一半左右。三星在2025年第三季發生的污染事件導致AMD MI325X的HBM3E認證延後了三個月。美光的市佔率太小,不足以緩解供不應求。 GDDR7的初始售價為每GB 18美元,給附加板的利潤率帶來了壓力。由於HBM市場由三家供應商主導,任何供應中斷都會波及北美GPU市場,阻礙出貨量成長。

細分市場分析

預計到2025年,獨立加速器將佔據北美GPU市場63.48%的佔有率,並將在2031年之前以17.77%的複合年成長率成長,凸顯其在超大規模計算中的核心地位。 NVIDIA的Blackwell GB200 NVL72機架式封裝整合了72個GPU和36個Grace CPU,可提供1.4 exaflops的FP4運算效能。這種配置雖然減少了叢集的面積,但也提高了平均售價。 AMD的MI325X將於2025年12月開始出貨,配備192GB HBM3E顯存,面向頻寬超過5TB/s的記憶體受限推理任務。預計到2025年,英特爾的Ponte Vecchio將佔據美國國家實驗室高效能運算(HPC)部署的22%,這表明開放標準互連可以與專有CUDA叢集共存。

在資料中心之外,獨立顯示卡正在推動遊戲和專業視覺化領域的革命。英特爾的 Battlemage B580 售價 249 美元,在上市 90 天內便佔據了 300 美元以下台式機市場的佔有率,這表明對價格敏感的遊戲玩家對價格具有很高的接受度。有傳言稱,NVIDIA 的 RTX 5090 擁有 24,576 個 CUDA 核心和 28GB GDDR7 顯存,其運算效能比 RTX 4090 提升了 40%,進一步拉大了與整合顯示卡的差距。蘋果的 M 系列整合顯示卡現在支援硬體射線追蹤,但散熱限制了其性能,使其僅適用於 75W 以下的工作負載,高階渲染和模擬任務仍然需要獨立顯示卡來完成。因此,儘管整合 NPU 可以處理一些較輕的生成式 AI 任務,但獨立顯示卡仍然是北美 GPU 市場的主要收入來源。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧主導資料中心GPU採購量激增

- 高清雲端遊戲服務的普及

- 人工智慧驅動的個人電腦在企業中的快速普及。

- 汽車高階駕駛輔助系統(ADAS)運算需求的擴展

- Chiplet 3D堆疊式GPU架構的進展

- 政府推出措施支持國內半導體產能

- 市場限制因素

- 先進HBM和GDDR7記憶體供應鏈中的漏洞

- 高階GPU的熱設計功耗限制正在提高。

- 加強中美之間的技術出口限制

- 電子競技的波動性和消費者更換週期

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 按整合類型

- 整合顯示卡(iGPU)

- 獨立GPU(dGPU)

- 裝置應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 家用遊戲機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式邊緣設備

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Arm Holdings plc

- Apple Inc.

- Samsung Electronics Co Ltd.

- Imagination Technologies Ltd.

- ASUSTeK Computer Inc.

- Micro-Star International Co Ltd(MSI)

- Gigabyte Technology Co Ltd

- Zotac Technology Ltd

- Sapphire Technology Ltd

- PowerColor Technology Inc.

- Xilinx Inc.(AMD Adaptive Computing)

- Tenstorrent Inc.

- Graphcore Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america gPU market size is projected to expand from USD 29.48 billion in 2025 and USD 33.52 billion in 2026 to reach USD 74.39 billion by 2031, registering a CAGR of 17.28% between 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and More), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America GPU Market Trends and Insights

Surging AI-Driven Datacenter GPU Procurement

Hyperscalers are compressing multi-year hardware refresh cycles to 18 months as AI model sizes grow. xAI commissioned the Colossus complex in Memphis, comprising 555,000 NVIDIA H100 GPUs that draw 150 MW and require USD 12,000 in liquid-cooling loops per rack. IREN's order for 150,000 GPUs in Texas leverages USD 0.018 kWh power, cutting operating costs by 70% relative to coastal sites. Amazon split a one-million-unit purchase between NVIDIA H200 and AMD MI325X parts to dilute supply risk and extract volume discounts. Such megablock deals raise average selling prices but make quarterly shipments volatile, as a single project delay can wipe out double-digit demand. This concentration gives the North America GPU market rapid topline growth alongside elevated forecasting risk.

Proliferation of High-Fidelity Cloud Gaming Services

Cloud platforms are shifting from shared virtualization to dedicated accelerators that sustain 4K 120 fps streams. NVIDIA's GeForce NOW Ultimate tier, built on RTX 5080 nodes, hit 15-minute queues within eight weeks, prompting a USD 400 million Oregon expansion. Microsoft's Xbox Cloud Gaming added 2.8 million regional subscribers in 2025, yet it needs 40% more GPUs per user than its rival, raising concerns about unit economics. Because each subscriber consumes disproportionate capital, operators restrain scaling until utilization models stabilize. Even so, enthusiast pricing at USD 24.99 per month keeps revenue per GPU attractive enough to sustain steady North America GPU market demand.

Supply-Chain Fragility for Advanced HBM and GDDR7 Memory

High-bandwidth memory is now the bottleneck, not lithography. SK Hynix's HBM4 yields stay below 60%, allowing only 12,000 wafer starts a month, roughly half of NVIDIA's demand for H200 accelerators. Samsung's contamination event in Q3 2025 delayed HBM3E qualification for AMD MI325X by three months. Micron's share is too small to ease shortages. GDDR7 debuted at USD 18 per GB, squeezing add-in-board margins. With three suppliers controlling the HBM market, any hiccup reverberates through the North America GPU market and curtails shipment growth.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Generative-AI PCs in Enterprise Fleets

- Expanding Automotive ADAS Compute Requirements

- Escalating Thermal-Design Power Limits in High-End GPUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete accelerators captured 63.48% of the North America GPU market share in 2025 and are projected to expand at a 17.77% CAGR through 2031, underscoring their central role in hyperscale build-outs. NVIDIA's Blackwell GB200 NVL72 rack package bundles 72 GPUs and 36 Grace CPUs to deliver 1.4 exaflops of FP4 compute, a configuration that compresses cluster footprints while boosting average selling prices. AMD's MI325X, shipping since December 2025 with 192 GB of HBM3E, targets memory-bound inference tasks in which bandwidth above 5 TB s-1 becomes decisive. Intel's Ponte Vecchio seized 22% of U.S. national-lab high-performance-computing deployments during 2025, proving that an open-standard interconnect can coexist with proprietary CUDA clusters.

Beyond data centers, discrete GPUs power gaming and professional-visualization refreshes. Intel's Battlemage B580, priced at USD 249, captured a share of sub-USD 300 desktop units within 90 days, demonstrating price elasticity among cost-sensitive gamers. Rumors place NVIDIA's RTX 5090 at 24,576 CUDA cores and 28 GB of GDDR7, a 40% compute leap over the RTX 4090, widening the gap with integrated solutions. Apple's M-series iGPUs now offer hardware ray tracing, but thermal constraints limit their performance to workloads below 75 W, leaving high-end rendering and simulation to discrete GPUs. As a result, the discrete tier remains the revenue locomotive for the North America GPU market, even as integrated NPUs shoulder light generative AI tasks.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Arm Holdings plc

- Apple Inc.

- Samsung Electronics Co Ltd.

- Imagination Technologies Ltd.

- ASUSTeK Computer Inc.

- Micro-Star International Co Ltd (MSI)

- Gigabyte Technology Co Ltd

- Zotac Technology Ltd

- Sapphire Technology Ltd

- PowerColor Technology Inc.

- Xilinx Inc. (AMD Adaptive Computing)

- Tenstorrent Inc.

- Graphcore Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI-Driven Datacenter GPU Procurement

- 4.2.2 Proliferation of High-Fidelity Cloud Gaming Services

- 4.2.3 Rapid Adoption of Generative-AI PCs in Enterprise Fleets

- 4.2.4 Expanding Automotive ADAS Compute Requirements

- 4.2.5 Advancements in Chiplet and 3D-Stacked GPU Architectures

- 4.2.6 Government Incentives for Domestic Semiconductor Capacity

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Fragility for Advanced HBM and GDDR7 Memory

- 4.3.2 Escalating Thermal-Design Power Limits in High-End GPUs

- 4.3.3 Intensifying US-China Tech Export Controls

- 4.3.4 Volatility in Esports and Consumer Upgrade Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Arm Holdings plc

- 6.4.6 Apple Inc.

- 6.4.7 Samsung Electronics Co Ltd.

- 6.4.8 Imagination Technologies Ltd.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Micro-Star International Co Ltd (MSI)

- 6.4.11 Gigabyte Technology Co Ltd

- 6.4.12 Zotac Technology Ltd

- 6.4.13 Sapphire Technology Ltd

- 6.4.14 PowerColor Technology Inc.

- 6.4.15 Xilinx Inc. (AMD Adaptive Computing)

- 6.4.16 Tenstorrent Inc.

- 6.4.17 Graphcore Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

整合顯示卡:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

整合顯示卡:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)影像處理處理器(GPU):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)影像處理處理器(GPU):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)