|

市場調查報告書

商品編碼

2063942

亞太地區綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

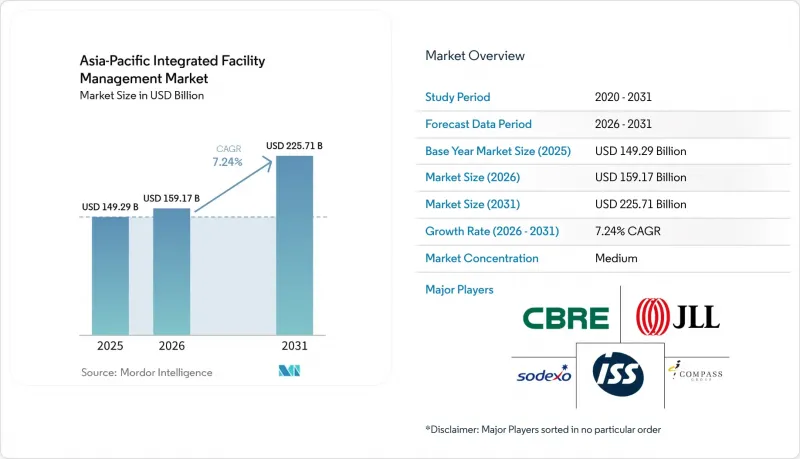

根據 Mordor Intelligence 預測,亞太地區綜合設施管理市場規模預計將從 2025 年的 1,492.9 億美元成長到 2026 年的 1,591.7 億美元,到 2031 年將達到 2,257.1 億美元,2026 年至 2031 年的複合年成長率為 7.24%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和安保、清潔服務、餐飲服務等])、最終用戶(商業、酒店、工業和流程行業等)以及地區進行細分。市場預測以價值(美元)表示。

亞太地區整合性機構管理市場的趨勢與洞察

在設施管理中擴大物聯網和智慧建築技術的應用

在亞太地區的整合性機構管理市場,互聯建築系統正從商業項目中的可選升級方案轉變為日常營運工具。新加坡的綠建築總體規劃高度重視提升建築性能,從而提升了整合監控和服務響應在日常營運中的價值。既有建築《建築管理法》的修訂提高了營運決策中能源性能和設備效率的透明度,鼓勵業主依賴數據豐富的設施管理模型,而非僅依賴人工巡檢。上海2025年綠建築規範進一步加速了這一趨勢,更高的性能標準凸顯了從性能驗證到運營的系統整合的重要性。這加劇了能夠將感測器、資產數據和工單整合到單一工作流程中的供應商與僅提供任務式的服務交付供應商之間的商業性差距。隨著應用範圍的擴大,亞太地區的綜合設施管理市場將更加重視那些能夠將建築資料轉化為快速服務決策、清晰合規記錄和更穩定服務品質的供應商。

對能源效率和綠色建築合規性的需求日益成長

在亞太地區的大部分綜合設施管理市場中,能源效率是採購的必要條件,而非可選項。新加坡針對高能耗大型建築的「強制性節能改造計畫」要求進行能源審計,並需實現可衡量的能耗強度降低,從而使設施管理服務商直接參與到規劃和實施合規工作中。上海目前要求所有新建私人建築至少達到一星級綠建築標準,而政府和大規模公共大樓則必須達到最高的三星標準。香港已將強制性能源審計的範圍擴大到11種類型的建築,並將審計週期縮短至五年,這增加了定期技術審查和後續後續的必要性。由於業主要求提供營運改善和服務交付方面的證明,這些法規有利於那些能夠將維護、性能再檢驗和數位化報告整合到單一合約中的服務商。因此,擁有認證能源管理能力的公司在亞太地區綜合設施管理市場的競標中具有強大的競爭優勢。

亞太地區不同司法管轄區的監管法規各不相同,這增加了合規成本。

由於亞太地區各司法管轄區在建築能源績效、安全、審計週期和報告等方面的法規存在差異,跨境設施管理服務仍面臨挑戰。在新加坡、澳洲、印度和東南亞營運的供應商無法依賴單一的合規指南,導致營運成本增加,標準化進程放緩。一項關於馬來西亞智慧建築部署的研究也表明,缺乏具體的法律法規和政策框架,以及資料共用和所有權問題,都是重大障礙。這些摩擦在區域性合約中尤其突出,因為客戶要求跨地域保持一致,而當地的營運規則要求進行市場客製化。留在單一司法管轄區的當地產業通常可以避免部分此類負擔,即使其業務範圍較窄,成本也可能看起來更低。在標準進一步統一之前,由於合規任務重疊和營運要求不統一,亞太地區綜合設施管理市場將繼續面臨利潤率壓力。

細分市場分析

2025年,軟性設施管理(Soft FM)佔區域收入的61.72%,而硬體維修)預計到2031年將以7.74%的複合年成長率成長。軟性設施管理服務仍佔較大佔有率,因為清潔、保全、辦公室支援和餐飲等服務屬於勞動密集型,且在商業、公共和政府設施中普遍外包。然而,隨著更嚴格的能源法規和日益複雜的設施,技術維護在綜合合約中的價值不斷提升,這種平衡正在改變。硬體維修管理直接受益於擁有集中式機電(MEP)設施的資產數量不斷成長,例如資料中心和生命科學園區,在這些設施中,運轉率和合規性與日常服務交付同等重要。因此,亞太地區的綜合設施管理市場正從基礎服務執行轉向以工程專業知識作為定價因素的合約模式。

硬體維修的機會也正在改變收入模式,因為預測性維護和遠端監控為曾經以例行檢查和故障維修為主的業務增添了持續的數位化元素。新加坡的定期暖通空調審核要求和香港更廣泛的審核範圍,都增加了對能夠解讀設備數據並將其轉化為糾正措施的供應商的需求。三星電子在韓國的Factual Seongsu大樓展示了整合式建築控制系統如何幫助降低能耗並提高智慧建築的可靠性,凸顯了技術嫻熟的操作人員的重要性。在整合設施管理產業,擁有現場工程師、能源專業知識和建築系統可視性的供應商,比純粹的軟體服務供應商更有優勢,能夠搶佔亞太地區整合設施管理市場快速成長的細分領域。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太地區二線城市商業不動產快速成長

- 對能源效率和綠色建築合規性的需求日益成長

- 跨國公司非核心設施管理職能外包趨勢

- 擴大物聯網和智慧建築技術在設施管理的應用。

- 政府強制性的淨零碳排放要求正在加快維修後性能驗證進程。

- 老化的建築存量正在推動預測性維護即服務模式的普及。

- 市場限制因素

- 亞太地區各司法管轄區的監管碎片化正在增加合規成本。

- 由於對成本敏感,中小企業對綜合設施管理(IFM)的採用率較低。

- 疫情後混合型硬體和軟體設施管理(FM)職位的熟練工人短缺

- 互聯建築系統引發的網路安全漏洞

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全

- 其他硬設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬設施管理

- 最終用戶

- 商業

- 飯店業

- 公共和機構基礎設施

- 衛生保健

- 工業和流程部門

- 其他終端用戶產業

- 按地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 紐西蘭

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sodexo SA

- CBRE Group, Inc.

- ISS A/S

- Compass Group PLC

- Jones Lang LaSalle Incorporated

- Colliers International Group Inc.

- Cushman & Wakefield plc

- Ventia Services Group

- OCS Group Limited

- Aeon Delight Co. Ltd.

- Serco Group plc

- Aramark Corporation

- Quess Corp Limited

- Aden Services

- Atalian Global Services

- Sinar Jernih Sdn Bhd

- UEMS Solutions Pte Ltd.

- NIPPON KANZAI Co., Ltd.

- Keppel Land Limited(Keppel Infrastructure Services)

- SIS Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific integrated facility management market size is expected to grow from USD 149.29 billion in 2025 to USD 159.17 billion in 2026 and is forecast to reach USD 225.71 billion by 2031 at 7.24% CAGR over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Hospitality, Industrial and Process Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Integrated Facility Management Market Trends and Insights

Increasing Adoption of IoT and Smart Building Technologies in Facility Management

Connected building systems are moving from optional upgrades to routine operating tools in commercial portfolios across the APAC integrated facility management market. Singapore's Green Building Masterplan places strong emphasis on better building performance, which raises the value of integrated monitoring and service response in daily operations. The Building Control Act changes for existing buildings also make energy performance and plant efficiency more visible in operating decisions, which pushes owners to rely on data-rich FM models rather than manual rounds alone. Shanghai's 2025 green building rules add further momentum because higher baseline performance standards increase the importance of system integration from commissioning through operations. This is widening the commercial gap between providers that can connect sensors, asset data, and work orders in one workflow and providers that only offer task-based delivery. As adoption broadens, the Asia-Pacific integrated facility management market is likely to reward operators that can turn building data into faster service decisions, clearer compliance records, and more stable service quality.

Rising Demand For Energy Efficiency and Green Buildings Compliance

Energy efficiency has become a procurement requirement rather than a discretionary upgrade in much of the Asia-Pacific integrated facility management market. Singapore's Mandatory Energy Improvement regime for large energy-intensive buildings requires audits and measurable reductions in energy use intensity, which brings FM providers directly into compliance planning and execution. Shanghai now requires all new civilian buildings to meet at least a one-star green standard, while government and large public buildings must reach the highest three-star level. Hong Kong has broadened mandatory energy audits to 11 building types and shortened the audit cycle to 5 years, which raises the need for recurring technical review and follow-through. These rules favor providers that can combine maintenance, retro-commissioning, and digital reporting in one contract because owners need proof of operational improvement and not only service coverage. The result is a stronger bidding position for companies with certified energy management capabilities across the APAC integrated facility management market.

Fragmented Regulatory Codes Across Asia-Pacific Jurisdictions Increasing Compliance Costs

Cross-border FM delivery remains difficult because APAC jurisdictions apply different rules for building energy performance, safety, audit cycles, and reporting. A provider serving Singapore, Australia, India, and Southeast Asia cannot rely on one compliance playbook, which raises overhead and slows standardization. Research on smart building adoption in Malaysia also identified the absence of specific legislation and policy frameworks as a major barrier, alongside data-sharing and ownership issues. These frictions matter most in regional contracts where clients want consistency across sites but local operating rules force market-by-market customization. Local operators that stay within one jurisdiction often avoid part of this burden, which can make them look cheaper even when their scope is narrower. Until standards align further, the APAC IFM market will continue to face margin pressure from duplicated compliance work and uneven operating requirements.

Other drivers and restraints analyzed in the detailed report include:

- Government Net-Zero Carbon Mandates Accelerating Retro-Commissioning Contracts

- Rapid Commercial Real Estate Growth in Tier 2 Asia-Pacific Cities

- Cybersecurity Vulnerabilities Arising From Connected Building Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft FM accounted for 61.72% of regional revenue in 2025, while Hard FM is set to expand at a 7.74% CAGR through 2031. Soft facility management services remained the larger pool because cleaning, security, office support, and catering are labor-intensive and widely outsourced across commercial, institutional, and public facilities. Even so, the balance is shifting because energy codes and equipment complexity are increasing the value of technical maintenance inside integrated contracts. Hard FM benefits directly from the growing stock of MEP-heavy assets, including data centers and life-sciences campuses, where uptime and compliance matter as much as routine service coverage. This is pushing the Asia-Pacific integrated facility management market toward contracts where engineering depth carries more pricing power than basic task execution.

The hard FM opportunity is also changing the revenue model because predictive maintenance and remote monitoring add recurring digital layers to what used to be scheduled or break-fix work. Singapore's periodic air-conditioning plant audit requirement and Hong Kong's broader audit scope both strengthen demand for providers that can interpret plant data and translate it into corrective action. Samsung Electronics' Factorial Seongsu building in South Korea showed how integrated building controls can support lower energy use and stronger smart building credentials, which reinforces the case for technically capable operators. In the integrated facility management industry, providers that combine field technicians, energy expertise, and building systems visibility are better positioned than pure soft-service vendors to capture the faster-growing side of the APAC integrated facility management market.

List of Companies Covered in this Report:

- Sodexo SA

- CBRE Group, Inc.

- ISS A/S

- Compass Group PLC

- Jones Lang LaSalle Incorporated

- Colliers International Group Inc.

- Cushman & Wakefield plc

- Ventia Services Group

- OCS Group Limited

- Aeon Delight Co. Ltd.

- Serco Group plc

- Aramark Corporation

- Quess Corp Limited

- Aden Services

- Atalian Global Services

- Sinar Jernih Sdn Bhd

- UEMS Solutions Pte Ltd.

- NIPPON KANZAI Co., Ltd.

- Keppel Land Limited (Keppel Infrastructure Services)

- SIS Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Commercial Real Estate Growth in Tier 2 Asian-Pacific Cities

- 4.2.2 Rising Demand for Energy Efficiency and Green Buildings Compliance

- 4.2.3 Outsourcing Trend Among Multinational Corporations for Non-Core FM Functions

- 4.2.4 Increasing Adoption of IoT and Smart Building Technologies in Facility Management

- 4.2.5 Government Net-Zero Carbon Mandates Accelerating Retro-Commissioning Contracts

- 4.2.6 Aging Building Stock Pushing Predictive Maintenance-as-a-Service Models

- 4.3 Market Restraints

- 4.3.1 Fragmented Regulatory Codes Across Asia-Pacific Jurisdictions Increasing Compliance Costs

- 4.3.2 Low Penetration of IFM in Small and Medium Enterprises Due to Cost Sensitivity

- 4.3.3 Skilled Labor Shortages in Hybrid Hard-Soft FM Roles Post-Pandemic

- 4.3.4 Cybersecurity Vulnerabilities Arising From Connected Building Systems

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

- 5.3 By Geography

- 5.3.1 China

- 5.3.2 Japan

- 5.3.3 India

- 5.3.4 South Korea

- 5.3.5 Australia

- 5.3.6 New Zealand

- 5.3.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sodexo SA

- 6.4.2 CBRE Group, Inc.

- 6.4.3 ISS A/S

- 6.4.4 Compass Group PLC

- 6.4.5 Jones Lang LaSalle Incorporated

- 6.4.6 Colliers International Group Inc.

- 6.4.7 Cushman & Wakefield plc

- 6.4.8 Ventia Services Group

- 6.4.9 OCS Group Limited

- 6.4.10 Aeon Delight Co. Ltd.

- 6.4.11 Serco Group plc

- 6.4.12 Aramark Corporation

- 6.4.13 Quess Corp Limited

- 6.4.14 Aden Services

- 6.4.15 Atalian Global Services

- 6.4.16 Sinar Jernih Sdn Bhd

- 6.4.17 UEMS Solutions Pte Ltd.

- 6.4.18 NIPPON KANZAI Co., Ltd.

- 6.4.19 Keppel Land Limited (Keppel Infrastructure Services)

- 6.4.20 SIS Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)