|

市場調查報告書

商品編碼

2063930

北美綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

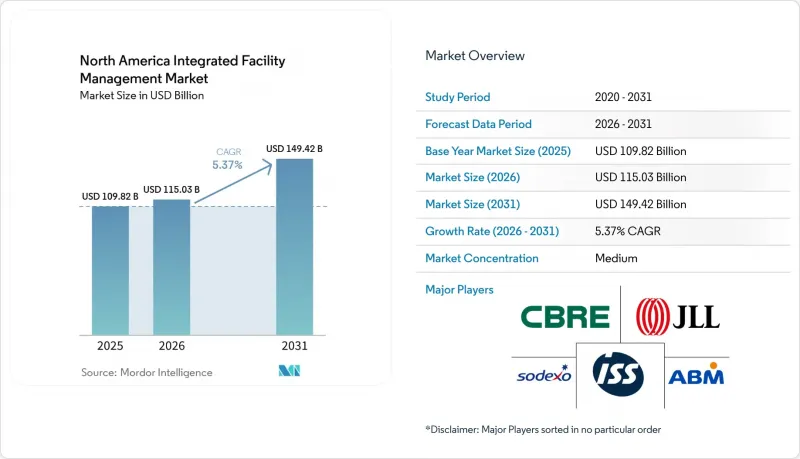

根據 Mordor Intelligence 預測,北美綜合設施管理 (FM) 市場規模預計將從 2025 年的 1098.2 億美元和 2026 年的 1150.3 億美元成長到 2031 年的 1494.2 億美元,2026 年至 2031 年的複合年成長率為 5.4%。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和安保、清潔服務、餐飲服務等])、最終用戶(商業、醫療保健、工業和流程行業及其他)以及地區進行細分。市場預測以價值(美元)為單位。

北美綜合設施管理市場趨勢與洞察

最佳化營運成本的需求日益成長

北美綜合設施管理 (IFM) 市場的發展動力更源自於成本控制需求,而非短期通膨擔憂。仲量聯行 (JLL) 的一項調查發現,81% 的設施管理領導者計劃減少供應商數量、整合契約,並將數據主導的標竿管理作為主要的成本削減工具。這使得綜合服務提供者比單一服務供應商更具優勢。 ABM 報告稱,2025 會計年度新訂單創歷史新高,達到 19 億美元,年增 12%,並將這一業績歸功於客戶對單一聯絡人責任制和可衡量的營運成本降低的需求。這意味著 IFM 的價值日益凸顯,它不僅被視為一種外包服務,更被視為降低整體擁有成本的手段。對於擁有龐大且分散資產組合的組織而言,這種轉變尤其重要,因為合約整合擴大了單一 IFM 服務提供者可提供的服務範圍。

擴大非核心服務的外包

北美綜合設施管理市場也受益整體技術和工作場所支援職能外包的擴張。外包趨勢已從清潔和餐飲擴展到建築自動化、能源管理以及機電(機械、電氣和管道)維護,推高了平均合約價值。 ABM表示,其內部人員配置模式使其能夠保留高達90%的員工作為直接僱員而非分包商,這一特點吸引了採購負責人,因為它降低了不同地點服務品質的差異。江森自控在2026年報告中指出,其95%的員工每週至少在辦公室工作三天。這意味著租戶現在需要更穩定的現場服務和更高的服務密度,而許多內部團隊無法大規模提供這種服務。這正在擴大外包設施管理基本客群,並鼓勵更多組織簽訂先前因內部原因而推遲的綜合合約。

熟練技術人員及設施管理人員短缺

北美綜合設施管理市場持續面臨結構性勞動力短缺,限制了服務提供者的擴張速度。根據REMI Network引用IFMA的數據,2025年第三季度,北美設施管理人員的平均招募週期達到3.6個月。仲量聯行(JLL)的一項調查也顯示,45%的設施管理領導者認為技術工人短缺是一個主要問題,農村和高生活成本地區的壓力尤其嚴重。在醫療設施管理(HFM)領域,《HFM雜誌》報道稱,招募暖通空調(HVAC)技術人員的難度高達94%,顯示在技術先進的環境中,人才短缺問題十分嚴峻。這不僅僅是招募問題。 IFMA估計,到2026年,隨著北美綜合設施管理市場合約複雜性的增加以及專業知識流失風險的上升,現有設施管理人員中將有40%退休。

細分市場分析

在北美綜合設施管理市場中,硬設施管理是成長最快的服務類型,預計到2031年將以6.7%的複合年成長率成長。資產管理、機電工程服務、消防系統和安全等領域的需求不斷成長,這主要得益於資料中心、半導體製造廠和醫療設施等行業的持續投資,因為這些行業的運作直接轉化為營運價值。根據世邦魏理仕(CBRE)的報告,到2025年,北美資料中心的淨吸收面積將達到創紀錄的2497.6萬平方英尺,主要市場的空置率將降至1.4%。這為技術密集型服務合約的長期發展提供了支撐。此外,江森自控的一項調查發現,52%計劃在2026年部署人工智慧的設施管理人員將預測性維護列為人工智慧投資的首要任務,這進一步鞏固了擁有工程和資料處理能力的硬體維修服務提供者的地位。

預計到2025年,軟性設施管理(Soft FM)將佔北美綜合設施管理市場佔有率的62.3%,並繼續成為商業、公共和酒店物業最大的收入來源。雖然清潔服務、辦公室支援、保全和餐飲服務仍然佔據北美綜合設施管理行業軟性設施管理需求的大部分,但清潔服務仍然是對價格最敏感的領域。根據江森自控的報告,到2026年,75%的組織將使用工作場所管理技術進行空間管理和規劃,這將推動軟性設施管理服務交付更加貼近入住率分析和即時人員配置決策。這種轉變將使軟性設施管理合約更加數據驅動,也更容易獲得認可,因為服務提供者可以將服務成果與利用率趨勢和用戶體驗聯繫起來。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 最佳化營運成本的需求日益成長

- 非核心服務外包增加

- 智慧建築技術的快速普及

- 嚴格的能源效率和永續性法規

- 關稅上漲導致的供應鏈重組將有利於本地綜合設施管理(IFM)供應商。

- 資料中心走廊的擴張推動了對全天候專業設施管理 (FM) 合約的需求。

- 市場限制因素

- 熟練技術人員及設施管理人員短缺

- 整合數位平台:初始成本高

- 客戶對獨家供貨合約中供應商鎖定問題的擔憂

- 各州在許可和合規標準方面存在差異

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 硬體設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全

- 其他硬體設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他軟性設施管理服務

- 硬體設施管理

- 最終用戶

- 商業

- 飯店業

- 公共機構及公共基礎設施

- 醫療保健

- 工業和流程部門

- 其他

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated

- Sodexo SA

- ISS A/S

- ABM Industries Incorporated

- Cushman and Wakefield plc

- Compass Group PLC

- Aramark

- GDI Integrated Facility Services Inc.

- EMCOR Group Inc.

- BGIS

- Johnson Controls International plc

- Colliers International Group Inc.

- Apleona GmbH

- Mitie Group plc

- Serco Group plc

- Allied Universal

- Atalian Servest

- Honeywell International Inc.

- C&W Services

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america integrated facility management market size is projected to expand from USD 109.82 billion in 2025 and USD 115.03 billion in 2026 to USD 149.42 billion by 2031, registering a CAGR of 5.4% between 2026 to 2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), End User (Commercial, Healthcare, Industrial and Process Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Integrated Facility Management Market Trends and Insights

Growing Demand for Operational Cost Optimization

The North America integrated facility management market is being pushed by cost control more than by short-term inflation concerns. JLL found that 81% of FM leaders planned to consolidate contracts with fewer suppliers and use data-led benchmarking as their main cost-reduction tools, which directly favors integrated providers over single-service vendors. ABM reported record new sales bookings of USD 1.9 billion in fiscal 2025, up 12% year over year, and linked that performance to client demand for single-source accountability and measurable operating savings. This means IFM is increasingly being assessed as a way to reduce total occupancy cost, not only as an outsourced service package. That shift is especially relevant for organizations with large and dispersed portfolios because each contract consolidation expands the service scope that one IFM provider can hold.

Increased Outsourcing of Non-Core Services

The North America integrated facility management market is also benefiting from broader outsourcing across technical and workplace support functions. The outsourcing trend now extends beyond janitorial and catering into building automation, energy management, and MEP maintenance, which raises the average value of each contract. ABM said its self-performing workforce model can keep as much as 90% of staff directly employed rather than subcontracted, and that feature is gaining procurement appeal because it reduces service variability across locations. Johnson Controls reported in 2026 that 95% of employees were in the office at least 3 days per week, which means occupiers now need more consistent onsite response and service density than many in-house teams can deliver at scale. This is widening the buyer base for outsourced FM and pulling more organizations into integrated contracts that they had previously delayed for internal reasons.

Shortage of Skilled Technicians and FM Workforce

The North America integrated facility management market continues to face a structural labor constraint that limits how quickly providers can scale. IFMA data cited by REMI Network showed that the average time to fill a facility management role in North America reached 3.6 months in Q3 2025. JLL also found that 45% of FM leaders viewed skilled trade labor shortages as a primary concern, with the pressure strongest in rural locations and high cost-of-living areas. In healthcare FM, HFM Magazine reported a 94% fill difficulty rate for HVAC trades, which shows how severe the shortage has become in technically sensitive environments. The problem is larger than recruitment alone because IFMA estimates that 40% of existing facilities managers will retire by 2026, which raises the risk of knowledge loss at the same time that contract complexity is rising in the NA integrated facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Smart Building Technologies

- Stringent Energy Efficiency and Sustainability Regulations

- High Upfront Costs of Integrated Digital Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard facility management is the fastest-growing service type in the North America integrated facility management market and is forecast to expand at a 6.7% CAGR through 2031. Demand is rising across asset management, MEP services, and fire systems and safety as investment continues in data centers, semiconductor fabs, and healthcare campuses where uptime has direct operating value. CBRE reported record net absorption of 2,497.6 MW in North American data centers during 2025, while vacancy in primary markets fell to 1.4%, which supports a long pipeline of technically intensive service contracts. Johnson Controls also found that predictive maintenance was the top AI investment priority for 52% of facility managers planning new AI deployments in 2026, which strengthens the position of Hard FM providers with engineering and data capability.

Soft facility management held 62.3% of the North America integrated facility management market share in 2025 and remains the largest revenue base across commercial, institutional, and hospitality properties. In the North America integrated facility management industry, cleaning services, office support and security, and catering services still account for most Soft FM demand, although cleaning remains the most price-sensitive part of the mix. Johnson Controls reported that 75% of organizations used workplace management technology for space management and planning in 2026, which is pushing soft service delivery closer to occupancy analytics and real-time staffing decisions. That shift is making Soft FM contracts more data-aware and more defensible when providers can connect service output with utilization trends and user experience.

List of Companies Covered in this Report:

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated

- Sodexo S.A.

- ISS A/S

- ABM Industries Incorporated

- Cushman and Wakefield plc

- Compass Group PLC

- Aramark

- GDI Integrated Facility Services Inc.

- EMCOR Group Inc.

- BGIS

- Johnson Controls International plc

- Colliers International Group Inc.

- Apleona GmbH

- Mitie Group plc

- Serco Group plc

- Allied Universal

- Atalian Servest

- Honeywell International Inc.

- C&W Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Operational Cost Optimization

- 4.2.2 Increased Outsourcing of Non-Core Services

- 4.2.3 Rapid Adoption of Smart Building Technologies

- 4.2.4 Stringent Energy Efficiency and Sustainability Regulations

- 4.2.5 Rising Tariff-Induced Supply Chain Reconfigurations Favoring Local IFM Providers

- 4.2.6 Expansion of Data Center Corridors Driving Specialized 24/7 FM Contracts

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Technicians and FM Workforce

- 4.3.2 High Upfront Costs of Integrated Digital Platforms

- 4.3.3 Client Concerns Around Vendor Lock-In in Single-Source Contracts

- 4.3.4 State-Level Variability in Licensing and Compliance Standards

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-User Industries

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 Jones Lang LaSalle Incorporated

- 6.4.3 Sodexo S.A.

- 6.4.4 ISS A/S

- 6.4.5 ABM Industries Incorporated

- 6.4.6 Cushman and Wakefield plc

- 6.4.7 Compass Group PLC

- 6.4.8 Aramark

- 6.4.9 GDI Integrated Facility Services Inc.

- 6.4.10 EMCOR Group Inc.

- 6.4.11 BGIS

- 6.4.12 Johnson Controls International plc

- 6.4.13 Colliers International Group Inc.

- 6.4.14 Apleona GmbH

- 6.4.15 Mitie Group plc

- 6.4.16 Serco Group plc

- 6.4.17 Allied Universal

- 6.4.18 Atalian Servest

- 6.4.19 Honeywell International Inc.

- 6.4.20 C&W Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)