|

市場調查報告書

商品編碼

2066481

可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Folding Carton Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

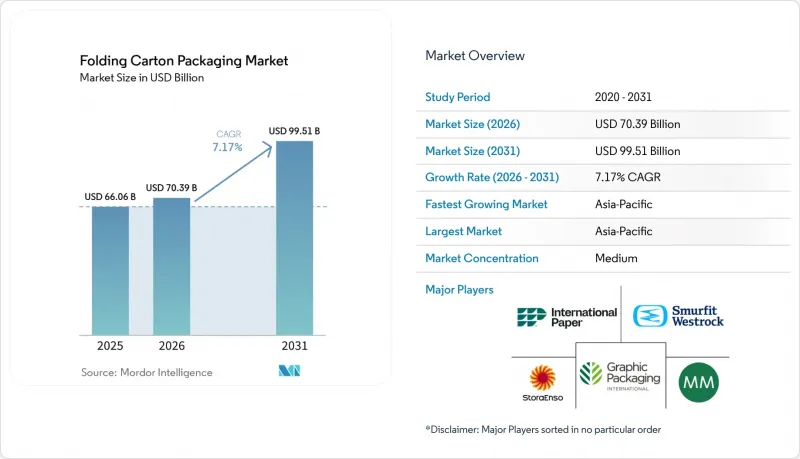

根據 Mordor Intelligence 預測,可折疊瓦楞紙包裝市場預計將從 2025 年的 660.6 億美元成長到 2026 年的 703.9 億美元,到 2031 年達到 995.1 億美元,2026 年至 2031 年的複合年成長率預計為 7.17%。

本報告按材料類型(固態漂白硫酸漿、折疊紙板、塗佈未漂白牛皮紙等)、印刷技術(膠印、凹版印刷等)、終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)以及地區進行細分。市場預測以價值(美元)表示。

全球可折疊瓦楞紙板包裝市場趨勢及洞察

食品和飲料加工產業的擴張

食品飲料加工產業仍是折疊瓦楞紙包裝市場最大的需求來源。東南亞、印度和撒哈拉以南非洲地區產能的提升,不僅取代了現有需求,也推動了折疊瓦楞紙包裝的新需求。此外,市場需求正轉向阻隔塗層和無菌包裝形式,這意味著折疊瓦楞紙包裝市場對高附加價值基材(而非僅限於標準漂白紙板)的需求將進一步成長。 Smurfit WestRock plc 公佈的 2025 會計年度淨銷售額為 311.8 億美元,食品飲料加工行業的加工量持續支撐著該公司在紙包裝領域的規模。這進一步印證了該產業在瓦楞紙需求中的核心地位。新興市場的加工商目前仍主要採購具備基本阻隔性能的中檔產品,而歐洲和北美的品牌商則指定使用經認證的可回收優質產品,以滿足永續性相關的採購法規。

電子商務包裝需求不斷成長

電子商務物流正在改變整個可折疊瓦楞紙包裝市場的包裝需求,這一趨勢在輕質履約流程的需求。零售包裝正成為許多線上和全通路供應鏈的標準配置,這對能夠小批量處理多種SKU的加工商而言極具優勢。品牌對小批量生產中更多設計變化的需求也在重塑可折疊瓦楞紙包裝市場,削弱了高複雜性與大規模生產之間的傳統關聯。 Graphic Packaging International LLC於2025年12月推出了其「Boardio」多包裝生產機,以紙板取代了塑膠多罐環支架。這與品牌所有者對可回收且易於分銷管道使用的包裝形式的需求直接契合。即使傳統印刷品質保持競爭力,缺乏數位印刷能力和小批量生產經濟效益的加工商也面臨在可折疊瓦楞紙包裝市場失去市場佔有率的風險。

紙板價格波動

原料成本波動仍然是可折疊瓦楞紙板包裝市場面臨的最緊迫的商業風險。根據美國包裝公司(Packing Corporation of America)預測,北美箱板紙價格預計將在2026年4月上漲50美元/噸,並預計在2026年年中進一步上漲50至70美元/噸,這將持續擠壓加工商的利潤空間。合約價格通常落後於現貨市場原物料價格波動一到兩個季度,這給尚未實施供應鏈管理或後向整合的加工商造成了利潤缺口。儘管美國NBSK紙漿價格在2025年第三季下降了7.6%,至790至860美元/噸,但成品紙板價格的上漲意味著紙漿價格下跌帶來的收益不足以完全恢復下游利潤空間。 Mayr-Melnhof Karton AG報告稱,其「面向未來」計劃在2025會計年度實現了7,000萬歐元(約7,910萬美元)的成本節約。這表明,儘管效率提升計畫可以緩解成本衝擊,但對於地域分散的加工商而言,複製這些節約成果卻十分困難。因此,大規模企業在可折疊瓦楞紙包裝市場仍佔據主導地位,尤其是在原物料價格波動較大的市場中。

細分市場分析

截至2025年,固體漂白硫酸漿(SBS)將佔可折疊瓦楞紙包裝市場39.13%的佔有率,預計2026年至2031年將以7.76%的複合年成長率成長。這種高於市場平均的規模和成長率在可折疊瓦楞紙包裝市場中實屬罕見,因為這種關鍵材料仍然是對規格要求最高的等級之一。 SBS在食品接觸和製藥應用領域繼續保持主導地位,在這些領域,白度、印刷品質和認證仍然至關重要。其光滑的表面可實現高解析度圖形印刷,而其完善的合規性有助於跨國品牌所有者在不同市場實現紙箱規格的標準化。

可折疊瓦楞紙板在可折疊瓦楞包裝市場中佔據第二大市場佔有率,並持續保持重要地位,尤其是在歐洲的煙草和高階化妝品行業。 2025年3月,Metsä Board宣布,與白紙塑合板相比,在食品包裝中使用可折疊瓦楞紙板可減少60%以上的碳足跡。這正在影響著那些有氣候目標的品牌對材料的選擇。 「塗層未漂白牛皮紙」因其優異的剛度重量比和自然的外觀,在快餐和零售包裝中發揮著重要作用。 「白紙塑合板」仍然用於對價格敏感的瓦楞紙產品,例如穀物和清潔劑,但在塗層降低其可回收性的領域,其市場佔有率正在逐漸下降。

區域分析

預計到2025年,亞太地區將佔據可折疊瓦楞紙包裝市場42.89%的佔有率,並在2031年之前以8.03%的複合年成長率成長。中國佔亞太地區需求的49%,這得益於食品加工的現代化、現代零售業的發展以及以零售業態為普遍需求的電子商務系統的普及。印度是該地區可折疊瓦楞紙包裝市場的第二大成長引擎,都市化、包裝食品的普及以及國內日常消費品(FMCG)市場的擴張都支撐了強勁的需求。此外,印度的需求也正從進口基礎材料轉向更多本地採購的中檔SBS和FBB材料,反映出國內包裝產能的提升。 2026 年 3 月,索諾科產品公司在泰國開設了一家紙罐製造廠,年產能為 2 億個,顯示跨國製造商正在投資,以期獲得該地區強勁的需求前景。

北美仍是可折疊瓦楞紙包裝市場第二大區域,但目前正面臨需求放緩和供應調整。 Graphic Packaging International LLC於2026年4月宣佈在全球裁員500多人。這並不意味著瓦楞紙板的重要性結構性下降,而是顯示由於產能過剩和短期需求疲軟而進行的業務調整。該地區的製藥和醫療保健產業繼續為高價值的SBS瓦楞紙箱創造穩定的需求,有助於產品結構的穩定。國際紙業公司於2026年1月完成了對DS Smith的收購,交易金額為72億美元。這正在重塑北美和歐洲紙包裝規模與紙板供應之間的關係。在南美,該地區受益於一次性塑膠法規的訂定以及對當地食品加工業投資的增加,其中巴西憑藉其強大的紙漿基礎和Cravin的規模優勢繼續發揮核心作用。

歐洲在可折疊瓦楞紙包裝市場中佔據著舉足輕重的地位,德國、法國和英國仍然是瓦楞紙板需求和加工能力的核心樞紐。將於2026年8月12日生效的(EU) 2025/40號法規,透過其關於可回收性和PFAS的規定,加強了整個歐洲快速消費品供應鏈對紙漿基瓦楞紙板的長期需求基礎。斯道拉恩索公司(Stora Enso Oyj)運作其Owl生產線,併計劃到2027年實現每年75萬噸近乎碳中和的可折疊紙板產能,以滿足塑膠向紙板替代帶來的新需求。中東地區雖然絕對規模仍然較小,但隨著阿拉伯聯合大公國和沙烏地阿拉伯零售業的正常化以及更廣泛的經濟多元化,食品加工專案正在推動新的紙盒需求。非洲仍面臨依賴進口、基礎設施不足和電力供應不穩定等限制因素,但該地區快速消費品市場的擴張繼續為可折疊紙盒包裝市場創造更多機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 食品飲料加工部門的擴張

- 電子商務包裝需求不斷成長

- 對永續包裝解決方案的需求日益成長

- 擴大數位印刷在小批量瓦楞紙箱中的應用。

- 政府對塑膠包裝徵收消費稅,正在推動包裝轉向紙板包裝。

- 雲端廚房和食材自煮包新創公司的快速發展,帶動了對少量瓦楞紙箱的需求成長。

- 市場限制因素

- 紙板價格波動

- 來自軟性包裝替代品的競爭

- 由於國內紙漿產量不足,對進口的依賴性增加。

- 電力供應中斷導致轉換器生產成本上升。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊紙板

- 塗層未漂白牛皮紙

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 微影術印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品/工業物品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit WestRock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc.

- American Carton Company

- Packaging Corporation of America

- Edelmann GmbH

- CCL Industries Inc.

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray, LP

- Klabin SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the folding carton packaging market size is expected to increase from USD 66.06 billion in 2025 to USD 70.39 billion in 2026 and reach USD 99.51 billion by 2031, growing at a CAGR of 7.17% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic Printing, Gravure Printing, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Folding Carton Packaging Market Trends and Insights

Expansion of the Food and Beverage Processing Sector

The food and beverage processing sector remains the largest demand anchor for the folding carton packaging market. Capacity additions across Southeast Asia, India, and sub-Saharan Africa are driving fresh carton procurement demand rather than simply replacing existing volumes. Demand is also moving toward barrier-coated and aseptic formats, which means the folding carton packaging market is seeing a stronger pull toward higher-value substrates rather than just standard bleached board. Smurfit WestRock plc reported FY2025 net sales of USD 31.18 billion, with food and beverage conversion volumes continuing to support its scale in paper-based packaging, which reinforces the sector's central role in carton demand. Emerging-market processors are still buying more mid-tier grades with basic barrier properties, while European and North American brand owners are specifying certified recyclable premium grades to meet sustainability-related procurement rules.

Growth of E-commerce Packaging Demand

E-commerce logistics are changing packaging requirements across the folding carton packaging market, especially for lightweight cartons that still need enough strength for automated fulfillment handling. Retail-ready packaging is becoming a standard specification in many online and omnichannel supply chains, and this favors converters that can manage multiple SKUs with short production runs. The folding carton packaging market is also being reshaped by the fact that brands now want more design variants in smaller batches, which weakens the old link between high complexity and high volume. Graphic Packaging International LLC launched the Boardio multipack machine in December 2025 to replace plastic multi-can ring holders with paperboard alternatives, a move that aligned directly with brand-owner demand for recyclable and channel-ready formats. Converters that lack digital print capability or short-run economics are at risk of losing share in the folding carton packaging market even when their conventional print quality remains competitive.

Volatility In Paperboard Prices

Input cost volatility remains the most immediate operating risk for the folding carton packaging market. Packaging Corporation of America said North American containerboard prices rose by USD 50 per ton in April 2026, with another announced increase of USD 50-70 per ton for mid-2026, which continued to pressure converting margins. Contract pricing often lags spot input changes by one or two quarters, creating an earnings gap for converters without supply protection or backward integration. Even though NBSK pulp prices in the United States eased by 7.6% to USD 790-860 per metric ton in Q3 2025, rising finished board prices meant that the relief at pulp level did not fully restore downstream margins. Mayr-Melnhof Karton AG reported that its Fit-for-Future program delivered EUR 70 million in savings in FY2025, equivalent to USD 79.1 million, showing that efficiency programs can soften cost shocks but are harder to replicate for fragmented regional converters. As a result, the folding carton packaging market still favors large-scale operators when raw material prices become volatile.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Sustainable Packaging Solutions

- Increased Adoption of Digital Printing for Short-run Cartons

- Competition From Flexible Packaging Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid Bleached Sulfate accounted for 39.13% of the folding carton packaging market in 2025 and is projected to grow at a 7.76% CAGR from 2026 to 2031. That combination of scale and above-market growth is unusual in the folding carton packaging market because the leading material also remains one of the most specification-sensitive grades. SBS continues to lead in food-contact and pharmaceutical applications because brightness, print quality, and certification remain essential in those categories. Its surface smoothness supports high-resolution graphics, while its established compliance profile helps multinational brand owners standardize carton specifications across markets.

Folding Boxboard held the second-largest material position in the folding carton packaging market and remained especially important in European tobacco and premium cosmetics applications. Metsa Board stated in March 2025 that folding boxboard can cut the carbon footprint by more than 60% compared with white-lined chipboard in food packaging, which is influencing material selection among brands with climate targets. Coated Unbleached Kraft played a strong role in fast-food and retail-ready packaging due to its stiffness-to-weight ratio and natural look. White Line Chipboard stayed present in price-sensitive cartons such as cereals and detergents, but it is gradually losing ground where coatings reduce recyclability classification.

Geography Analysis

Asia-Pacific accounted for 42.89% of the folding carton packaging market share in 2025 and is forecast to grow at a 8.03% CAGR through 2031. China accounted for 49% of Asia-Pacific demand, supported by food processing modernization, the growth of modern retail, and an e-commerce system that has made retail-ready formats a common requirement. India is the second-largest regional growth engine for the folding carton packaging market, as urbanization, packaged food penetration, and domestic FMCG expansion are all supporting durable demand. Demand in India is also shifting from imported substrates toward more locally supplied mid-grade SBS and FBB grades, reflecting improving domestic packaging capabilities. Sonoco Products Company opened a paper can manufacturing plant in Thailand in March 2026, with a capacity of 200 million units per year, indicating that multinational producers are directing investment toward the region's stronger demand outlook.

North America remained the second-largest region in the folding carton packaging market, but it is currently experiencing softer demand and supply rationalization. Graphic Packaging International LLC announced a global workforce reduction of more than 500 positions in April 2026, signaling an operating adjustment tied to overcapacity and weaker near-term demand rather than a structural decline in carton relevance. The region's pharmaceutical and healthcare base still provides consistent demand for higher-value SBS cartons and helps stabilize the mix. International Paper Company completed its USD 7.2 billion acquisition of DS Smith plc in January 2026, which is reshaping paper-based packaging scale and board supply relationships across North America and Europe. South America is benefiting from restrictions on single-use plastics and from rising investment in local food processing, while Brazil continues to anchor the region through its strong fiber base and the scale position of Klabin S.A.

Europe retained a structurally important position in the folding carton packaging market because Germany, France, and the United Kingdom remain core centers for carton demand and converting capacity. Regulation (EU) 2025/40 comes into force from August 12, 2026, and its recyclability and PFAS provisions are strengthening the long-term case for fiber-based cartons across European FMCG supply chains. Stora Enso Oyj inaugurated its Oulu line in August 2025 with a target of 750,000 tonnes per year of near carbon-neutral folding boxboard capacity by 2027, positioning it to capture substitution demand linked to plastic-to-paperboard conversion. The Middle East is still smaller in absolute terms, but retail formalization in the UAE and Saudi Arabia and food processing projects linked to broader economic diversification are supporting new carton demand. Africa remains constrained by import dependence, infrastructure gaps, and unstable power supply, though regional FMCG expansion is still creating incremental opportunities for the folding carton packaging market.

- Smurfit WestRock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc.

- American Carton Company

- Packaging Corporation of America

- Edelmann GmbH

- CCL Industries Inc.

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray, L.P.

- Klabin S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Food and Beverage Processing Sector

- 4.2.2 Growth of E-commerce Packaging Demand

- 4.2.3 Rising Demand for Sustainable Packaging Solutions

- 4.2.4 Increased Adoption of Digital Printing for Short-Run Cartons

- 4.2.5 Government Excise Tax on Plastic Packaging Spurring Shift Toward Paperboard

- 4.2.6 Rapid Growth of Cloud Kitchen and Meal-Kit Start-ups Requiring Small-Batch Cartons

- 4.3 Market Restraints

- 4.3.1 Volatility in Paperboard Prices

- 4.3.2 Competition From Flexible Packaging Alternatives

- 4.3.3 Limited Domestic Pulp Production Increasing Import Dependence

- 4.3.4 Power Supply Interruptions Elevating Production Costs for Converters

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Graphic Packaging International LLC

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 International Paper Company

- 6.4.5 Stora Enso Oyj

- 6.4.6 Georgia-Pacific LLC

- 6.4.7 Mondi plc

- 6.4.8 Huhtamaki Oyj

- 6.4.9 Seaboard Folding Box Co. Inc.

- 6.4.10 American Carton Company

- 6.4.11 Packaging Corporation of America

- 6.4.12 Edelmann GmbH

- 6.4.13 CCL Industries Inc.

- 6.4.14 Rengo Co., Ltd.

- 6.4.15 Sonoco Products Company

- 6.4.16 Autajon Group

- 6.4.17 Southern Champion Tray, L.P.

- 6.4.18 Klabin S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)