|

市場調查報告書

商品編碼

2063764

美國折疊式紙盒:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)United States Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

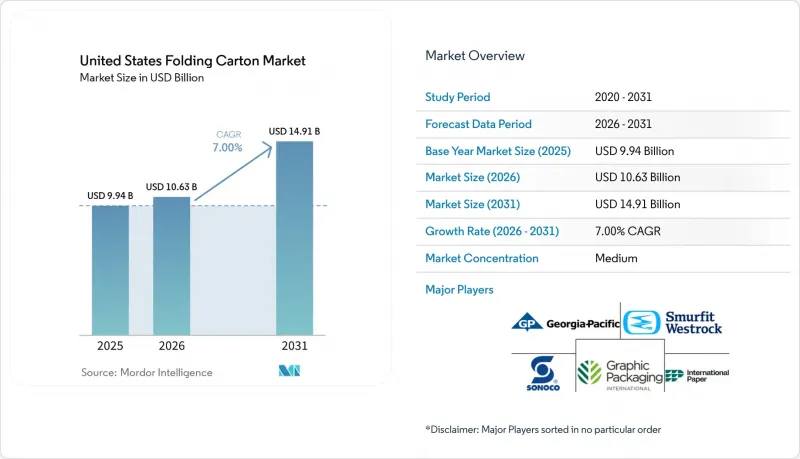

據 Mordor Intelligence 稱,2025 年美國折疊式紙盒市值為 99.4 億美元,預計到 2031 年將達到 149.1 億美元,而 2026 年為 106.3 億美元,預測期(2026-2031 年)的複合年成長率為 7%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙板、塗佈未漂白牛皮紙等)、印刷技術(膠印、柔版印刷、數位印刷、凹版印刷等)和終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)進行細分。市場預測以美元計價。

美國折疊式紙盒市場趨勢與洞察

電子商務的快速發展帶動了對輕型保護包裝的需求。

紙盒和紙箱佔所有電商包裝的40%,因此加工商需要設計尺寸合適的包裝結構,以承受商店展示和配送網路的雙重考驗。在北美,自動化系統透過減少多餘空間,使平均包裝重量降低了43%,運輸過程中的破損率降低了24%。這推動了對具有ISTA認證邊緣和加固角線的折疊式紙盒的需求。如今,數位印刷機可以列印連結到會員網站的可變QR碼,滿足了50%掃描2D碼的消費者的需求,零售商也計劃在2027年前全面推廣2D條碼。自動化、可追溯性和全通路適用的美觀性相結合,正推動美國折疊式紙盒市場從通用型紙盒轉向客製化規格紙盒。

對永續和可回收包裝解決方案的需求日益成長

已有七個州頒布了生產者延伸責任制(EPR)法,要求生產者承擔收集和回收的成本。明尼蘇達州規定,到2032年,所有包裝材料必須可回收、可重複使用、可再填充或可堆肥,並且到2031年,至少90%的系統成本必須由政府資金籌措。華盛頓州的計畫將在2032年前逐步實現90%的成本報銷,並從2029年開始撥款500萬美元用於再利用基礎建設。這些法律徵收的環境友善費用有利於回收率檢驗的再生纖維紙盒,迫使品牌所有者從使用原生漂白紙板轉向使用含有更多消費後再生纖維的可折疊紙板。奧勒岡州在2026年就費用透明度問題提出了憲法挑戰,導致對生產者成本轉嫁策略的審查增加。然而,從長遠來看,可回收的塗佈紙和較薄的紙板仍然是更受歡迎的選擇。因此,永續基材的選擇現在與財務和合規性密切相關,再生紙板在美國折疊式紙盒市場正經歷持續的順風。

再生紙和原生紙漿價格波動

2025年11月,再生紙板(OCC)均價為每噸44美元,年減41%,但由於造紙企業為應對春季停產而囤積庫存,2026年1月價格反彈至每噸1美元。優質再生紙漿生產者物價指數從2025年11月的77.411飆升至2025年10月的87.545,隨後在2026年2月回落至82.723。這凸顯了月度成本波動對合約預算的扭曲。中國一項強制揭露濕紙漿和乾紙漿進口量的政策轉變,正在減弱對出口的溢出效應,並加劇國內價格的不確定性。折疊紙盒加工商通常會滯後3-6個月才調整價格以適應客戶需求,因此,再生紙板(OCC)和原生紙漿價格在周期中期的每一次飆升都會對其利潤率造成壓力。這些持續的價格波動使美國折疊紙盒產業的策略採購變得複雜,並阻礙了長期價格承諾的達成。

細分市場分析

到2025年,固體漂白硫酸漿(SBS)將在美國折疊式紙盒市場佔據38.21%的市場佔有率。這主要得益於食品、飲料和藥品等產品對油墨附著力和食品接觸面認證的高要求。折疊紙板預計將以8.19%的複合年成長率成長,優於整體市場表現,這得益於生產者延伸責任制(EPR)收費系統,該機制鼓勵使用再生材料,以及價格為每噸44美元的大量再生紙(OCC)。塗佈未漂白牛皮紙滿足了對耐油性和天然紋理有要求的細分市場需求,而白面塑合板則在非食品二級包裝領域具有成本競爭力。到了2025年,隨著Graphic Packaging位於韋科的工廠產能擴張抵消明尼蘇達州和德克薩斯州工廠的關閉,再生紙板的淨產能將略有成長。明尼蘇達州的 EPR 生態調節法規鼓勵減輕重量,這促使各大品牌轉向更薄的折疊板,進一步加速了從原生漂白基材轉向其他基材的轉變。

能夠獲得高品質再生材料的加工商維持著穩健的價格。這是因為,由於與再生材料含量掛鉤的生產者延伸責任制(EPR)費用,再生材料與原生材料之間的成本差異正在縮小。美國包裝公司(Packaging Corporation of America)收購了Greif的回收工廠,使其再生材料比例從20%提高到30%,這凸顯了該公司向成本效益更高的基礎材料策略轉型。纖維配方的這些調整表明,美國折疊紙盒市場將繼續朝著再生纖維方向發展,尤其是在監管嚴格的沿海州,因為費用結構直接影響總交付成本。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 市場促進因素

- 電子商務的快速發展帶動了對輕質防護包裝材料的需求。

- 對永續和可回收包裝解決方案的需求日益成長

- 食品飲料行業的優質化趨勢正在推動對高品質印刷的需求。

- 食材自煮包和已調理食品宅配服務的快速成長

- 各州層級的生產者延伸責任法正在加速紙盒包裝的普及。

- 藥品低溫運輸運輸中對專用折疊式紙箱的需求日益成長。

- 市場限制因素

- 再生紙和原生紙漿價格波動

- 擴大軟包裝產能將蠶食折疊式紙盒的市場佔有率。

- 駕駛人正在擾亂供應鏈並延長前置作業時間。

- 熟練的印刷機操作人員短缺阻礙了生產成長。

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- Graphic Packaging Holding Company

- International Paper Company

- Sonoco Products Company

- Georgia-Pacific LLC

- Pratt Industries Inc.

- Atlantic Packaging Corp.

- Mayr-Melnhof Karton AG

- AR Packaging Group AB

- Clearwater Paper Corporation

- Hood Container Corporation

- PaperWorks Industries Inc.

- Bell Incorporated

- L Industrial Packaging

- JohnsByrne Company

- Curtis Packaging Corporation

- All Packaging Company

- American Carton Company

- Diamond Packaging

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states folding carton market size was valued at USD 9.94 billion in 2025 and is estimated to grow from USD 10.63 billion in 2026 to reach USD 14.91 billion by 2031, at a CAGR of 7% during the forecast period (2026-2031).

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Folding Carton Market Trends and Insights

E-Commerce Boom Driving Demand for Lightweight Protective Packaging

Boxes and cartons account for 40% of all e-commerce packaging formats, compelling converters to engineer right-sized structures that survive both shelf display and parcel networks. Automated systems that trim void space have cut average package weight by 43% in North America and lowered shipping damage by 24%, pushing demand toward folding cartons with ISTA-validated edges and reinforced corner scores. Digital presses now add variable QR codes that link to loyalty sites, meeting the 50% of consumers who scan codes and the retailers who plan universal 2D barcode acceptance by 2027. This convergence of automation, traceability, and omnichannel aesthetics is steering the United States folding cartons market away from commodity grades toward engineered formats.

Increasing Demand for Sustainable and Recyclable Packaging Solutions

Seven states enacted EPR statutes requiring producers to finance collection and recycling, with Minnesota mandating that all packaging be recyclable, reusable, refillable, or compostable by 2032 and to fund at least 90% of system costs by 2031. Washington's program phases in 90% reimbursement by 2032 and earmarks USD 5 million for reuse infrastructure starting in 2029. These laws impose eco-modulated fees that privilege recycled-fiber cartons with verifiable recovery rates, driving brand owners to swap virgin bleached board for folding boxboard containing higher post-consumer fiber. Oregon's 2026 constitutional challenge over fee transparency has heightened producer scrutiny of cost pass-through strategies, yet the long-term trajectory still favors recyclable-coated barriers and lightweight calipers. As a result, sustainable substrate selection is now intertwined with finance and compliance, giving recycled paperboard a lasting tailwind in the United States folding cartons market.

Volatility in Recovered Paper and Virgin Pulp Prices

Old corrugated containers (OCC) averaged USD 44 per ton in November 2025, sinking 41% from the prior year before rebounding USD 1 per ton in January 2026 as mills pre-bought for spring downtime. The Producer Price Index for high-grade recyclable pulp whipsawed from 77.411 in November 2025 to 87.545 in October 2025 and back to 82.723 by February 2026, underscoring monthly cost swings that distort contract budgeting. Chinese policy shifts requiring disclosure of wet versus dry recycled pulp imports cut export pull-through, intensifying domestic price uncertainty. Because folding carton converters typically adjust customer pricing with a 3- to 6-month lag, margin compression surfaces whenever OCC or virgin pulp spikes mid-cycle. Persistent volatility complicates strategic sourcing and discourages long-term price commitments in the United States folding carton industry.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization in Food and Beverage Boosting High-Quality Printing

- State-Level Extended Producer Responsibility Legislation Accelerating Carton Adoption

- Capacity Expansion of Flexible Packaging Displacing Folding Cartons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The United States folding carton market size for solid bleached sulfate captured 38.21% market share in 2025, underpinned by food, beverage, and pharmaceutical SKUs that require flawless ink laydown and certified food-contact surfaces. Folding boxboard is projected to outpace the overall market at an 8.19% CAGR, buoyed by EPR fee schedules that reward recycled content and by plentiful OCC priced at USD 44 per ton. Coated unbleached kraft serves grease-resistant, natural-aesthetic niches, while white line chipboard competes on cost for non-food secondary packs. Net recycled board capacity rose modestly in 2025 as Graphic Packaging's Waco mill ramp offset closures in Minnesota and Texas. Minnesota's EPR eco-modulation rules that favor weight reduction are pushing brands toward lighter caliper folding boxboard, reinforcing momentum away from virgin bleached substrates.

Converters that secure high-quality recycled furnish enjoy price resilience, because EPR fees linked to recycled content narrow the cost gap versus virgin grades. Packaging Corporation of America's acquisition of Greif's recycled mills raised its recycled mix from 20% to 30%, highlighting a strategic pivot toward fee-friendly substrates. These fiber-mix adjustments suggest that the United States folding cartons market will continue tilting toward recycled fiber, especially in regulated coastal states where fee structures directly impact total delivered cost.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Graphic Packaging Holding Company

- International Paper Company

- Sonoco Products Company

- Georgia-Pacific LLC

- Pratt Industries Inc.

- Atlantic Packaging Corp.

- Mayr-Melnhof Karton AG

- AR Packaging Group AB

- Clearwater Paper Corporation

- Hood Container Corporation

- PaperWorks Industries Inc.

- Bell Incorporated

- L Industrial Packaging

- JohnsByrne Company

- Curtis Packaging Corporation

- All Packaging Company

- American Carton Company

- Diamond Packaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 E-commerce Boom Driving Demand for Lightweight Protective Packaging

- 4.7.2 Increasing Demand for Sustainable and Recyclable Packaging Solutions

- 4.7.3 Premiumization in Food and Beverage Boosting High-Quality Printing

- 4.7.4 Rapid Growth of Meal Kit and Ready-to-Eat Delivery Services

- 4.7.5 State-Level Extended Producer Responsibility Legislation Accelerating Carton Adoption

- 4.7.6 Rise of Pharmaceutical Cold-Chain Shipments Requiring Specialized Folding Cartons

- 4.8 Market Restraints

- 4.8.1 Volatility in Recovered Paper and Virgin Pulp Prices

- 4.8.2 Capacity Expansion of Flexible Packaging Displacing Folding Cartons

- 4.8.3 Supply Chain Disruptions from Trucker Shortages Increasing Lead Times

- 4.8.4 Labor Shortage in Skilled Press Operators Restricting Output Growth

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Graphic Packaging Holding Company

- 6.4.3 International Paper Company

- 6.4.4 Sonoco Products Company

- 6.4.5 Georgia-Pacific LLC

- 6.4.6 Pratt Industries Inc.

- 6.4.7 Atlantic Packaging Corp.

- 6.4.8 Mayr-Melnhof Karton AG

- 6.4.9 AR Packaging Group AB

- 6.4.10 Clearwater Paper Corporation

- 6.4.11 Hood Container Corporation

- 6.4.12 PaperWorks Industries Inc.

- 6.4.13 Bell Incorporated

- 6.4.14 L Industrial Packaging

- 6.4.15 JohnsByrne Company

- 6.4.16 Curtis Packaging Corporation

- 6.4.17 All Packaging Company

- 6.4.18 American Carton Company

- 6.4.19 Diamond Packaging

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)泰國可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢與統計數據及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)泰國可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢與統計數據及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)