|

市場調查報告書

商品編碼

2066595

泰國可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢與統計數據及成長預測(2026-2031)Thailand Folding Carton Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

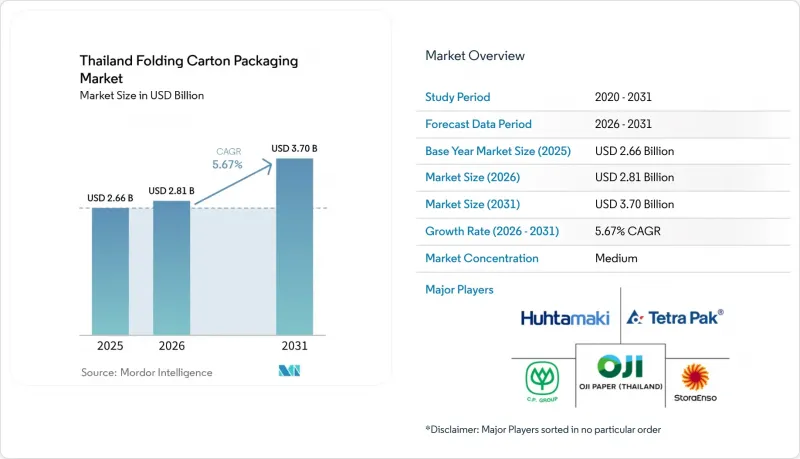

據 Mordor Intelligence 稱,2025 年泰國可折疊瓦楞紙包裝市場價值為 26.6 億美元,預計到 2031 年將從 2026 年的 28.1 億美元成長至 37 億美元,預測期(2026-2031 年)複合年成長率為 5.67%。

本報告按材料類型(固態漂白硫酸紙漿、折疊紙盒用紙板、塗佈未漂白牛皮紙、白線塑合板等)、印刷技術(膠印、柔版印刷、數位印刷等)和終端用戶行業(食品飲料、電子商務和零售包裝、煙草等)進行細分。市場預測以美元計價。

泰國可折疊瓦楞紙板包裝市場的趨勢和洞察。

電子商務交易量強勁成長,並致力於永續性

2023年泰國線上零售額達265億美元,預計到2025年將達到320億美元,這推動了對兼具保護性和品牌展示功能的折疊紙盒的需求。各大平台日益強制要求使用再生材料,以符合企業的ESG(環境、社會和治理)目標,迫使加工商在進口量波動的情況下確保再生纖維的穩定供應。零售商拓展全通路運營,需要標準化的模切線來實現從倉庫到客戶家門口的無縫配送,這推動了多用途瓦楞紙箱的設計。儘管每平方公尺仍存在0.02至0.05美元的成本溢價,但永續性促使人們擴大採用水性塗料作為不含PFAS的替代方案。小包裹數量的成長和環保包裝目標的日益重視,共同支撐著泰國折疊瓦楞紙包裝市場持續保持中等個位數的銷售成長。

轉向使用FMCG品牌下的優質印刷瓦楞紙板

受泰國中等收入家庭數量成長和遊客湧入的推動,品牌商正努力通過採用帶有壓紋、啞光清漆和全像處理等表面處理的瓦楞紙箱來提升其商店形象。產品生命週期縮短和季節性系列產品的出現要求快速換線,這為僅需15分鐘即可完成設定的數位印刷機創造了理想的應用場景。像利樂這樣的技術供應商每年投入約1億歐元(1.18億美元)進行研發,以開發能夠實現優質影像效果並同時降低工廠能耗40%的阻隔塗層。優質化在個人護理、化妝品和特色糖果甜點行業中尤為顯著,因為包裝是影響消費者購買決策的重要因素。

中國進口政策導致再生紙板價格波動

中國2018年禁止進口混合紙的政策對東南亞地區產生了連鎖反應,導致大量品質不穩定的原料湧入泰國造紙廠。受此影響,混合紙價格從2017年的每噸60美元以上暴跌至幾乎為零,之後才有所回升。泰國國內的回收率遠低於已開發國家,使得加工商難以規避成本波動風險。儘管近期區域回收廠產能的提升正在縮小品質差距,但政策變化,例如印尼可能削減配額,這意味著價格風險仍然很高。泰國大型企業已儲備了三個月的紡織品庫存,但流動資金有限的小型企業卻無力負擔價格的急劇上漲,利潤空間受到擠壓,甚至可能被迫停產。

細分市場分析

到2025年,由於其良好的印刷性和成本優勢,白面紙板將佔據泰國折疊瓦楞紙包裝市場45.15%的佔有率。品牌商青睞其光滑的表面,便於高解析度影像印刷。隨著零售商承諾在2030年實現30%的再生材料含量,折疊紙盒的年複合成長率(CAGR)正以6.51%的速度成長。折疊紙盒具有優異的剛度重量比,可以製作更薄的紙板,從而降低跨境運輸至柬埔寨、寮國、緬甸和越南(CLMV)的運費8-10%。固態實心紙板在化妝品行業中仍佔有一席之地,其亮度指標有助於提升產品在商店的視覺衝擊力,但其高昂的成本限制了其大規模應用。另一方面,塗佈未漂白牛皮紙板則受到電子產品出口商的青睞,因為他們優先考慮重型零件的抗穿刺性能。

採用沉澱氧化鋁(AlOx)的阻隔塗層材料提升了可折疊瓦楞紙板的功能極限,實現了對堅果、巧克力、粉狀飲料和其他產品的安全包裝,有效防止成分滲漏。 SRF有限公司的第三台BOBST金屬化設備計劃於2025年9月在羅勇府安裝,屆時將提升該地區用於層壓結構的高阻隔薄膜的產量。這種材料轉變凸顯了泰國可折疊瓦楞包裝市場的新格局:目前塑合板產量佔比更高,而可折疊瓦楞紙板則擁有強大的品牌形象。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務交易量強勁成長,並致力於永續性

- 快速消費品品牌轉向使用高級印刷紙盒

- 政府擬定生產者責任延伸法案草案,旨在提振對再生材料的需求

- 數位式高產能瓦楞紙板印刷機的商業化部署

- 快速將膠印產能從中國轉移到泰國

- 食材自煮包和調理食品的訂閱量激增。

- 市場限制因素

- 中國進口政策導致再生紙板價格波動

- 工業電費飆升

- 中小企業加工設施分散,限制了品管。

- 不含 PFAS 塗料的合規成本

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊紙板

- 塗層未漂白牛皮紙

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 微影術印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品/工業物品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Siam Toppan Packaging Co., Ltd.

- SCG Packaging Public Company Limited

- Thai Containers Group Co., Ltd.

- Thung Hua Sinn Company Limited

- Continental Packaging(Thailand)Co., Ltd.

- Oji Paper(Thailand)Ltd.

- ASA Group Co., Ltd.

- Sarnti Packing Co., Ltd.

- Thai Card-Board Company Limited

- S&D Industries Company Limited

- JK Cartons Group Co., Ltd.

- Huhtamaki(Thailand)Ltd.

- Tetra Pak(Thailand)Ltd.

- Ratchapruek Packaging Co., Ltd.

- Print Master Co., Ltd.

- SC Packaging Asia Co., Ltd.

- Stora Enso(Thailand)Co., Ltd.

- Charoen Pokphand Packaging Co., Ltd.

- Great Wall Enterprise(Thailand)Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the thailand folding carton packaging market was valued at USD 2.66 billion in 2025 and estimated to grow from USD 2.81 billion in 2026 to reach USD 3.7 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031).

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, E-Commerce and Retail-Ready Packaging, Tobacco, and More). The Market Forecasts are Provided in Terms of Value (USD).

Thailand Folding Carton Packaging Market Trends and Insights

Robust E-Commerce Volume Growth and Sustainability Commitments

Thai online retail sales reached USD 26.5 billion in 2023 and are projected to reach USD 32 billion by 2025, driving demand for protective yet brand-forward folding cartons. Large platforms increasingly mandate recycled content to align with corporate ESG goals, compelling converters to secure stable recycled fiber supplies despite volatile import flows. Retailers expanding their omnichannel operations require standardized die lines that can move seamlessly from warehouse to doorstep, pushing multipurpose carton designs. Sustainability pledges are driving the adoption of water-based coatings as PFAS-free alternatives, despite the persistence of cost premiums of USD 0.02-0.05 per m2. Together, rising parcel counts and green-packaging targets underpin consistent mid-single-digit volume growth for the Thailand folding carton packaging market.

FMCG Brand Shift Toward Premium Printed Cartons

Thailand's middle-income households and tourist influx encourage brand owners to upgrade shelf presence with embossed, matte-varnish, and holographic carton finishes. Shorter product lifecycles and seasonal collections require nimble changeovers, a sweet spot for digital presses capable of 15-minute makereadies. R&D spending by technology vendors such as Tetra Pak, about EUR 100 million (USD 118 million) per year, is channeling barrier coatings that enable the reduction of plant energy use by 40% while supporting premium graphics. Premiumization is most visible in personal-care, cosmetics, and specialty confectionery, where packaging is a primary purchase trigger.

Recycled Paperboard Price Volatility Linked to China's Import Policy

China's 2018 ban on mixed-paper imports cascaded into Southeast Asia, flooding Thai mills with inconsistent feedstock and sending mixed-paper prices from above USD 60 per ton in 2017 to near zero before rebounding. Converters struggle to hedge cost swings because domestic collection rates lag developed-market norms. Recent capacity additions in regional recycling plants are narrowing quality gaps, yet policy pivots, such as potential quota reductions in Indonesia, keep price risk elevated. Larger Thai players stock three-month fiber inventories, but SMEs operating on thin working capital cannot absorb sudden spikes, compressing margins and occasionally prompting production halts.

Other drivers and restraints analyzed in the detailed report include:

- Government EPR Draft Law Catalyzing Recycled-Content Demand

- Commercial Rollout of Digital Short-Run Carton Presses

- Soaring Industrial Electricity Tariffs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White-lined chipboard accounted for 45.15% of the Thailand folding carton packaging market in 2025, due to its printability and cost advantage. Brands favor its smooth surface for high-resolution imagery, but folding boxboard is growing at a 6.51% CAGR as retailers pledge to reach 30% recycled content by 2030. Folding boxboard's stiffness-to-weight ratio enables down-gauging, which reduces freight costs by 8-10% for cross-border shipments to the CLMV (Cambodia, Laos, Myanmar, Vietnam). Solid bleached board maintains a niche use in cosmetics, where brightness metrics serve shelf-impact goals; however, its higher cost limits mass adoption. Coated unbleached kraftboard appeals to electronics exporters who value puncture resistance for heavy components.

Barrier-coated grades integrating vapor-deposited aluminum oxide (AlOx) raise the functional ceiling for folding boxboard, enabling migration-safe packaging for nuts, chocolate, and powdered drinks. SRF Limited's third BOBST metallizer installation, scheduled for September 2025 in Rayong, will increase the regional output of high-barrier films that feed laminate structures. These material shifts underscore an emerging hierarchy where chipboard dominates volume but folding boxboard captures reputational mindshare in the Thailand folding carton packaging market.

List of Companies Covered in this Report:

- Siam Toppan Packaging Co., Ltd.

- SCG Packaging Public Company Limited

- Thai Containers Group Co., Ltd.

- Thung Hua Sinn Company Limited

- Continental Packaging (Thailand) Co., Ltd.

- Oji Paper (Thailand) Ltd.

- ASA Group Co., Ltd.

- Sarnti Packing Co., Ltd.

- Thai Card-Board Company Limited

- S&D Industries Company Limited

- J.K. Cartons Group Co., Ltd.

- Huhtamaki (Thailand) Ltd.

- Tetra Pak (Thailand) Ltd.

- Ratchapruek Packaging Co., Ltd.

- Print Master Co., Ltd.

- SC Packaging Asia Co., Ltd.

- Stora Enso (Thailand) Co., Ltd.

- Charoen Pokphand Packaging Co., Ltd.

- Great Wall Enterprise (Thailand) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust E-Commerce Volume Growth and Sustainability Commitments

- 4.2.2 FMCG Brand Shift Toward Premium Printed Cartons

- 4.2.3 Government EPR Draft Law Catalyzing Recycled-Content Demand

- 4.2.4 Commercial Rollout of Digital Short-Run Carton Presses

- 4.2.5 High-Speed Offset Capacity Relocations from China to Thailand

- 4.2.6 Meal-Kit and Ready-Meal Subscriptions Surge

- 4.3 Market Restraints

- 4.3.1 Recycled Paperboard Price Volatility Linked to China's Import Policy

- 4.3.2 Soaring Industrial Electricity Tariffs

- 4.3.3 Fragmented SME Converting Base Limiting Quality Control

- 4.3.4 PFAS-Free Coating Compliance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Siam Toppan Packaging Co., Ltd.

- 6.4.2 SCG Packaging Public Company Limited

- 6.4.3 Thai Containers Group Co., Ltd.

- 6.4.4 Thung Hua Sinn Company Limited

- 6.4.5 Continental Packaging (Thailand) Co., Ltd.

- 6.4.6 Oji Paper (Thailand) Ltd.

- 6.4.7 ASA Group Co., Ltd.

- 6.4.8 Sarnti Packing Co., Ltd.

- 6.4.9 Thai Card-Board Company Limited

- 6.4.10 S&D Industries Company Limited

- 6.4.11 J.K. Cartons Group Co., Ltd.

- 6.4.12 Huhtamaki (Thailand) Ltd.

- 6.4.13 Tetra Pak (Thailand) Ltd.

- 6.4.14 Ratchapruek Packaging Co., Ltd.

- 6.4.15 Print Master Co., Ltd.

- 6.4.16 SC Packaging Asia Co., Ltd.

- 6.4.17 Stora Enso (Thailand) Co., Ltd.

- 6.4.18 Charoen Pokphand Packaging Co., Ltd.

- 6.4.19 Great Wall Enterprise (Thailand) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)