|

市場調查報告書

商品編碼

1885894

術後恢復蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Post-Surgical Recovery Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

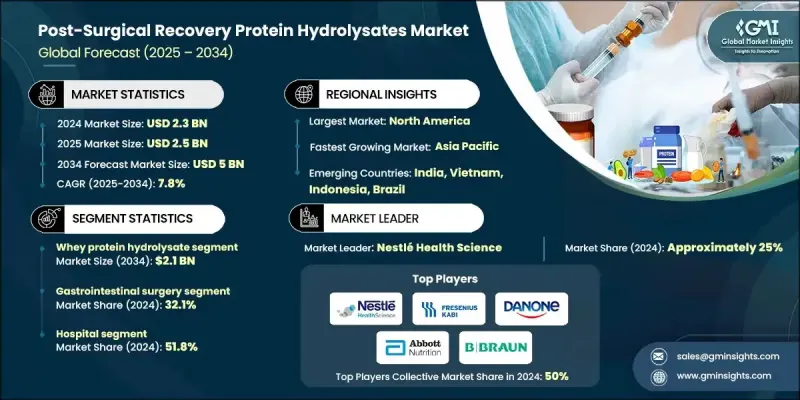

2024 年全球術後恢復蛋白水解物市場價值為 23 億美元,預計到 2034 年將以 7.8% 的複合年成長率成長至 50 億美元。

市場成長受多種因素驅動,包括人口老化、手術量增加以及實證臨床營養實踐的持續發展。蛋白質水解物配方技術的進步提高了消化率、療效和患者依從性,同時隨著新興市場外科營養基礎設施的完善,也擴大了其可及性。由於圍手術期集中使用以及臨床方案和醫院處方集的強大影響力,醫院和醫療機構管道仍然佔據市場主導地位。零售和家庭醫療保健管道貢獻了剩餘的市場收入,為出院後康復階段的患者提供服務。最佳化圍手術期營養的趨勢,以及蛋白質水解物在外科護理路徑中的更廣泛應用,將使該市場在未來十年持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 23億美元 |

| 預測值 | 50億美元 |

| 複合年成長率 | 7.8% |

2024年,乳清蛋白水解物市佔率達到43.8%,預計到2034年將以7.7%的複合年成長率成長。乳清蛋白水解物以其卓越的氨基酸組成(尤其是亮氨酸)而著稱,是刺激肌肉蛋白質合成和促進快速恢復的理想選擇。其快速吸收的特性確保在30-60分鐘內達到血漿氨基酸峰值水平,因此非常適合消化功能受損的術後患者。

2024年,醫院市場佔比51.8%,預計到2034年將以7.7%的複合年成長率成長。醫院仍然是術前和術後蛋白質水解物的主要消費場所。其使用受臨床方案、處方集決策和品質指標的指導,這些指標強調減少併發症和縮短患者住院時間。

2024年,北美術後恢復蛋白水解物市場佔據33.2%的市場佔有率,預計到2034年將以7.7%的複合年成長率成長。該地區的市場主導地位得益於人口老化導致的大量手術、超過60%的主要醫院廣泛採用ERAS方案等臨床營養指南、醫療保險和私人保險對腸內營養的有利報銷政策,以及雅培營養和雀巢健康科學等主要企業強大的分銷網路。

術後恢復蛋白水解物市場的主要參與者包括雅培營養品、雀巢健康科學、費森尤斯卡比、味之素株式會社、百特國際、貝朗醫療、達能紐瓦克健康科學、費森尤斯卡比、味之素株式會社、百特國際、貝朗醫療、達能紐迪希亞、凱特農場、奧爾德薩實驗室、美贊臣營養品、美敦力、明治控股、紐迪希亞先進醫療營養、大冼Vitaflo International。這些公司採取的關鍵策略包括:開發創新蛋白配方以提高吸收率和生物利用度;加強研發投入以提高療效和患者依從性;拓展新興市場,完善外科手術基礎設施;以及加強與醫院和臨床營養部門的合作。各公司致力於建立強大的經銷網路,確保產品進入藥品目錄,並提供量身訂製的圍手術期營養解決方案。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依配方類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計

- 主要進口國

- 主要出口國(註:僅提供重點國家的貿易統計)

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依來源分類,2021-2034年

- 主要趨勢

- 乳清蛋白水解物

- 酪蛋白水解物

- 膠原蛋白水解物

- 禽肉蛋白質水解物

- 植物性蛋白質水解物

第6章:市場估算與預測:依劑型分類,2021-2034年

- 主要趨勢

- 標準胜肽基製劑

- 免疫營養配方

- 高蛋白/低碳水化合物配方

- 富含麩醯胺酸的配方

- MCT增強配方

- 傷口癒合專用配方

第7章:市場估計與預測:依手術類型分類,2021-2034年

- 主要趨勢

- 胃腸外科

- 大腸直腸手術

- 減重手術

- 肝膽外科手術

- 胰臟手術

- 上消化道手術

- 腫瘤外科

- 頭頸癌手術

- 食道癌和胃癌手術

- 婦科腫瘤手術

- 膀胱癌手術

- 大腸直腸癌手術

- 骨科手術

- 關節置換手術(膝關節、髖關節)

- 脊椎外科手術

- 創傷重建手術

- 心臟外科手術

- 冠狀動脈繞道手術(CABG)

- 瓣膜置換手術

- 心臟移植手術

- 創傷與燒傷

- 鈍性或穿透性創傷

- 多重創傷

- 部分皮層燒傷

- 全層燒傷

- 高體表面積燒傷

- 普通外科和混合外科

- 疝氣修補術

- 闌尾切除術

- 膽囊切除術

- 剖腹探查術

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院

- 家庭醫療保健

- 長期照護機構

- 門診手術中心

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Abbott Nutrition

- Ajinomoto Co.

- B. Braun Melsungen

- Baxter International

- Cambrooke Therapeutics

- Danone Nutricia

- Fresenius Kabi

- Kate Farms

- Laboratorios Ordesa

- Mead Johnson Nutrition

- Medline Industries

- Meiji Holdings

- Nestle Health Science

- Nutricia Advanced Medical Nutrition

- Otsuka Pharmaceutical

- Real Food Blends

- Solace Nutrition

- Targeted Medical Pharma

- Victus

- Vitaflo International

- Others

The Global Post-Surgical Recovery Protein Hydrolysates Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 5 billion by 2034.

The market growth is driven by multiple factors, including demographic aging, rising surgical volumes, and evolving evidence-based clinical nutrition practices. Technological advancements in protein hydrolysate formulations are improving digestibility, efficacy, and patient compliance, while expanding accessibility in emerging markets with developing surgical nutrition infrastructure. Hospitals and institutional channels continue to dominate the market due to concentrated usage during the perioperative period and strong influence from clinical protocols and hospital formularies. Retail and home healthcare channels contribute the remaining market revenue, serving patients in post-discharge recovery phases. The trend toward optimized perioperative nutrition, combined with broader adoption of protein hydrolysates in surgical care pathways, positions this market for sustained expansion over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $5 Billion |

| CAGR | 7.8% |

The whey protein hydrolysate segment held a 43.8% share in 2024 and is expected to grow at a CAGR of 7.7% through 2034. Recognized for its superior amino acid profile, particularly leucine, whey hydrolysate is ideal for stimulating muscle protein synthesis and supporting rapid recovery. Its quick absorption ensures peak plasma amino acid levels within 30-60 minutes, making it highly suitable for post-surgical patients with compromised digestion.

The hospital segment accounted for a 51.8% share in 2024 and is projected to grow at a CAGR of 7.7% through 2034. Hospitals remain the primary consumption point for protein hydrolysates during the preoperative and postoperative periods. Usage is guided by clinical protocols, formulary decisions, and quality metrics that emphasize reducing complications and shortening patient stays.

North America Post-Surgical Recovery Protein Hydrolysates Market held 33.2% share in 2024, with a projected CAGR of 7.7% through 2034. The region's dominance is supported by a high volume of surgeries among an aging population, widespread adoption of clinical nutrition guidelines such as ERAS protocols in over 60% of major hospitals, favorable reimbursement policies for enteral nutrition through Medicare and private insurance, and strong distribution networks from major players like Abbott Nutrition and Nestle Health Science.

Major players operating in the Post-Surgical Recovery Protein Hydrolysates Market include Abbott Nutrition, Nestle Health Science, Fresenius Kabi, Ajinomoto Co., Baxter International, B. Braun Melsungen, Danone Nutricia, Kate Farms, Laboratorios Ordesa, Mead Johnson Nutrition, Medline Industries, Meiji Holdings, Nutricia Advanced Medical Nutrition, Otsuka Pharmaceutical, Real Food Blends, Solace Nutrition, Targeted Medical Pharma, Victus, Cambrooke Therapeutics, and Vitaflo International. Key strategies adopted by companies in the Post-Surgical Recovery Protein Hydrolysates Market include developing innovative protein formulations that enhance absorption and bioavailability, investing in R&D to improve efficacy and patient compliance, expanding into emerging markets with growing surgical infrastructure, and strengthening partnerships with hospitals and clinical nutrition departments. Firms focus on building robust distribution networks, securing formulary placements, and offering tailored perioperative nutrition solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Formulation type

- 2.2.4 Surgery type

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By formulation type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries ( Note: the trade statistics will be provided for key countries only)

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2021 - 2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Whey Protein Hydrolysate

- 5.3 Casein Hydrolysate

- 5.4 Collagen Hydrolysate

- 5.5 Poultry Protein Hydrolysate

- 5.6 Plant-Based Protein Hydrolysates

Chapter 6 Market Estimates and Forecast, By Formulation Type, 2021 - 2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Standard Peptide-Based Formulations

- 6.3 Immunonutrition Formulations

- 6.4 High Protein/Low Carbohydrate Formulations

- 6.5 Glutamine-Enriched Formulations

- 6.6 MCT-Enhanced Formulations

- 6.7 Wound Healing Specific Formulations

Chapter 7 Market Estimates and Forecast, By Surgery Type, 2021 - 2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Gastrointestinal Surgery

- 7.2.1 Colorectal Surgery

- 7.2.2 Bariatric Surgery

- 7.2.3 Hepatobiliary Surgery

- 7.2.4 Pancreatic Surgery

- 7.2.5 Upper GI Surgery

- 7.3 Oncologic Surgery

- 7.3.1 Head and Neck Cancer Surgery

- 7.3.2 Esophageal and Gastric Cancer Surgery

- 7.3.3 Gynecologic Oncology Surgery

- 7.3.4 Bladder Cancer Surgery

- 7.3.5 Colorectal Cancer Surgery

- 7.4 Orthopedic Surgery

- 7.4.1 Joint Replacement Surgery (Knee, Hip)

- 7.4.2 Spinal Surgery

- 7.4.3 Trauma Reconstruction Surgery

- 7.5 Cardiac Surgery

- 7.5.1 Coronary Artery Bypass Grafting (CABG)

- 7.5.2 Valve Replacement Surgery

- 7.5.3 Heart Transplant Surgery

- 7.6 Trauma & Burns

- 7.6.1 Blunt or Penetrating Trauma

- 7.6.2 Polytrauma

- 7.6.3 Partial Thickness Burns

- 7.6.4 Full Thickness Burns

- 7.6.5 High TBSA Burns

- 7.7 General & Mixed Surgery

- 7.7.1 Hernia Repair

- 7.7.2 Appendectomy

- 7.7.3 Cholecystectomy

- 7.7.4 Exploratory Laparotomy

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Home Healthcare

- 8.4 Long-Term Care Facilities

- 8.5 Ambulatory Surgical Centers

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Abbott Nutrition

- 10.2 Ajinomoto Co.

- 10.3 B. Braun Melsungen

- 10.4 Baxter International

- 10.5 Cambrooke Therapeutics

- 10.6 Danone Nutricia

- 10.7 Fresenius Kabi

- 10.8 Kate Farms

- 10.9 Laboratorios Ordesa

- 10.10 Mead Johnson Nutrition

- 10.11 Medline Industries

- 10.12 Meiji Holdings

- 10.13 Nestle Health Science

- 10.14 Nutricia Advanced Medical Nutrition

- 10.15 Otsuka Pharmaceutical

- 10.16 Real Food Blends

- 10.17 Solace Nutrition

- 10.18 Targeted Medical Pharma

- 10.19 Victus

- 10.20 Vitaflo International

- 10.21 Others

有機蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)單細胞蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)精準發酵法製備蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)老年營養蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)下一代蛋白質水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034)

有機蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)單細胞蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)精準發酵法製備蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)老年營養蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)下一代蛋白質水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034) 蛋白質水解物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、形態、製程、應用、地區和競爭格局分類,2020-2030年預測非基因改造蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)食品廢棄物衍生蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)噴霧乾燥蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)發酵蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

蛋白質水解物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、形態、製程、應用、地區和競爭格局分類,2020-2030年預測非基因改造蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)食品廢棄物衍生蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)噴霧乾燥蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)發酵蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)