|

市場調查報告書

商品編碼

2073617

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East and Africa Micronutrient Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

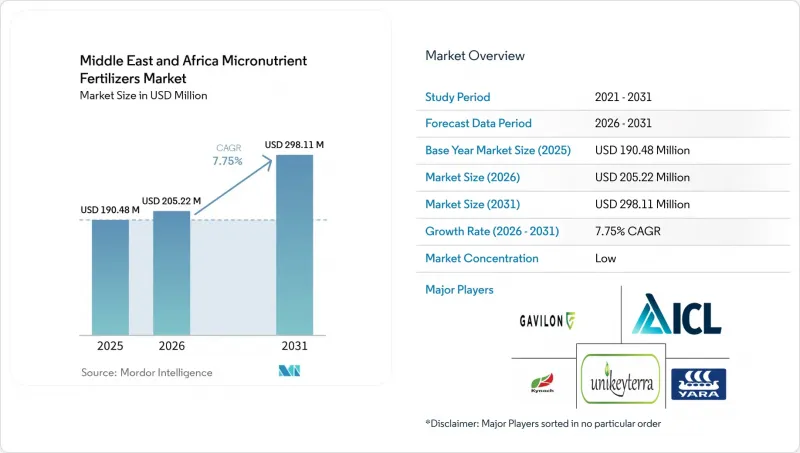

據 Mordor Intelligence 稱,中東和非洲微量元素肥料的市場規模預計將從 2025 年的 1.9048 億美元成長到 2026 年的 2.0522 億美元。

此外,預計到 2031 年,該產業的價值將達到 2.9811 億美元,並且預計從 2026 年到 2031 年的複合年成長率將達到 7.75%。

本報告按產品(硼、銅、鐵、錳、鉬、鋅等)、應用方法(施肥/灌溉、葉面噴布等)、作物類型(田間作物、園藝作物等)和地區(奈及利亞、沙烏地阿拉伯、南非、土耳其等)進行細分。市場預測以價值(美元)和數量(公噸)表示。

中東和非洲微量元素肥料市場的趨勢和洞察

氣候變遷導致土壤微量元素耗竭

在中東和非洲,隨著氣溫升高和沙塵暴頻繁侵蝕肥沃的土壤層,鋅、硼、鐵和錳等元素的流失速度正在加速。根據土耳其國家土壤健康計畫預測,到2024年,65%的農地將出現鋅和硼缺乏,比過去十年惡化了23%。阿卜杜拉國王科技大學(KAUST)的實驗表明,土壤溫度持續高於45 度C可使鈣質土壤中鋅的生物有效性降低高達40%。這種養分流失會導致作物減產15%至30%,迫使生產者採用螯合肥料,即使在鹼性、低水分條件下也能維持溶解性。鑑於區域暖化和土壤侵蝕持續加劇,微量元素的補充將在2030年後繼續對農場盈利發揮核心作用。衛星影像證實,貧瘠土地的擴張與已記錄的微量元素缺乏區域高度吻合。

可控制環境農業中心的發展

海灣國家正以前所未有的規模投資垂直農場、水耕叢集和氣候控制溫室,以提高糧食自給率。沙烏地阿拉伯的NEOM計畫將1萬公頃土地用於室內系統,該系統採用全自動施肥和灌溉,能夠以亞毫升級的精度施用液態螯合劑。阿拉伯聯合大公國的國家糧食安全戰略也正在投資20億美元建造類似設施。這些設施擁有高密度的植物和快速的作物生長週期,使得每公頃的微量營養素消耗量比露天種植高出3到5倍。供應商正在積極應對,開發超高純度液體以防止循環管道中沉澱,並實施低溫運輸儲存系統以防止熱劣化。隨著海灣合作理事會(GCC)成員國的生產商擴大面向高階國內零售和出口市場的生產規模,預計鄰近市場(如阿曼和巴林)對技術驅動型微量營養素解決方案的需求將進一步成長。此外,這些大型計畫也為新的農業技術新創公司奠定了基礎,這些公司將營養分析軟體與施肥和灌溉硬體結合,擴大了特種螯合劑的潛在基本客群。

外匯波動會影響進口成本。

外匯的快速波動推高了螯合肥料的到岸成本,因為這些肥料的原料以歐元和美元計價。 2024年奈及利亞奈拉貶值68%,迫使經銷商將歐洲產品的商店價格提高高達60%。土耳其里拉的波動迫使供應商縮短信用期限,削弱了依賴季節性資金籌措的小規模農戶的購買力。避險費用使產品價格再增加8%至12%,而港口壅塞和由此產生的滯留費進一步推高了成本。雖然一些公司正在就包裝和物流的該地貨幣貨幣合約進行談判,但螯合配體本身的價格仍然與外匯匯率掛鉤,從而固定了剩餘風險。這種波動迫使進口商持有緩衝庫存,佔用了原本可用於市場開發的營運資金。

細分市場分析

預計到2025年,鋅將佔據中東和非洲微量元素肥料市場34.4%的佔有率,這主要歸功於其能夠糾正普遍存在的土壤缺鋅問題,並支持區域糧食強化計畫。此細分市場的主導地位源自於雙重需求:一是彌合產量差距,二是提高主糧的營養價值。

預計到2031年,鉬的需求量將以8.8%的複合年成長率快速成長,成為成長最快的元素。這主要得益於豆類作物種植面積的擴大和固氮計畫的推進,鉬的使用量正在加速成長。鐵錳混合物繼續用於溫室種植的番茄和辣椒,因為這些微量元素的均衡含量對其色澤和保存期限至關重要。銅因其營養價值和病害防治作用,在摩洛哥橄欖種植中需求量大。硼在土耳其和地中海地區蔬菜的果實品管中也繼續發揮重要作用。供應商正在銷售多微量元素包衣,將這些元素整合到單一穀物中,簡化大規模穀物農場的物流。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章執行摘要

第3章:本報告的內容

第4章:主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 氣候變遷導致土壤微量元素耗竭

- 可控制環境農業中心的發展

- 對政府平衡施肥補貼的審查

- 推出一種適用於乾旱地區的特殊組合藥物。

- 擴大主食強制添加鋅的範圍

- 再生農業認證體系的興起

- 市場限制因素

- 影響進口成本的高度波動外匯制度

- 薩赫勒地區和非洲之角的分散分銷網路

- 螯合劑本地生產能力不足

- 隨著補貼逐步取消,農民對價格的敏感度

第5章 市場規模與成長預測

- 產品

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 使用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 地區

- 奈及利亞

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Yara International ASA

- ICL Group Ltd

- Unikeyterra Tarim Sanayi ve Ticaret AS

- Kynoch Fertilizer(Maizey Investments Ltd)

- Gavilon South Africa(MacroSource, LLC)

- Azra Group Tarim AS

- BASF SE

- Haifa Chemicals Ltd

- Koch Industries Inc.

- Sociedad Quimica y Minera de Chile SA(SQM SA)

- Coromandel International Ltd(Murugappa Group)

- Valagro SpA(Syngenta Group Co., Ltd.)

- BMS Micro-Nutrients NV

- Brandt Consolidated Inc.

- Grupa Azoty SA

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the middle east and Africa micronutrient fertilizers market size in 2026 is estimated at USD 205.22 million, up from 2025's USD 190.48 million, with 2031 projections showing USD 298.11 million, growing at a 7.75% CAGR over 2026-2031.

This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, and More), by Application Mode (Fertigation, Foliar, and More), by Crop Type (Field Crops, Horticultural Crops, and More), and by Geography (Nigeria, Saudi Arabia, South Africa, Turkey, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Middle East and Africa Micronutrient Fertilizers Market Trends and Insights

Climate-Induced Soil Micronutrient Depletion

Soils across the Middle East and Africa are losing zinc, boron, iron, and manganese at an accelerating pace as hotter temperatures and more frequent sandstorms shear away fertile layers. Turkey's National Soil Health Program documented zinc and boron deficits in 65% of farmland in 2024 and showed a 23% deterioration over the last decade . Laboratory work at King Abdullah University of Science and Technology revealed that sustained soil temperatures above 45 °C cut zinc bioavailability by up to 40% in calcareous fields . This nutrient drain triggers yield losses of 15% to 30% and forces growers to adopt chelated blends that remain soluble in alkaline, moisture-scarce conditions. Continued regional warming and erosion mean corrective micronutrient strategies will stay central to farm profitability well past 2030. Satellite imagery corroborates expanding barren patches that align closely with documented micronutrient gaps.

Growth of Controlled-Environment Agriculture Hubs

Gulf nations are channeling unprecedented capital into vertical farms, hydroponic clusters, and climate-controlled greenhouses to improve food self-sufficiency. Saudi Arabia's NEOM blueprint assigns 10,000 hectares to indoor systems that depend on fully automated fertigation capable of dosing liquid chelates with sub-milliliter accuracy. The United Arab Emirates National Food Security Strategy mobilized USD 2 billion for similar facilities that consume three to five times more micronutrients per hectare than open fields because of higher plant densities and rapid crop cycles . Suppliers respond by formulating ultra-pure liquids that resist precipitation in recirculating lines and by installing cold-chain storage to prevent thermal degradation. As GCC producers scale output for premium local retail and export channels, demand for tech-enabled micronutrient solutions is set to intensify across adjacent markets such as Oman and Bahrain. These large-scale projects also anchor new agritech start-ups that bundle nutrient analytics software with fertigation hardware, enlarging the addressable customer base for specialty chelates.

Volatile Foreign-Exchange Regimes Impacting Import Costs

Sharp currency swings elevate landed costs for chelated inputs that rely on Euro- and Dollar-denominated raw materials. The Nigerian Naira slid 68% in 2024, forcing distributors to raise shelf prices by up to 60% for European-sourced. Turkish Lira volatility prompted suppliers to shorten credit terms, eroding affordability for smallholders who depend on seasonal financing. Hedging fees add another 8% to 12% to product pricing, while port congestion triggers demurrage that further bloats costs. Although some companies negotiate local-currency contracts for packaging and logistics, the chelate ligands themselves remain pegged to foreign exchange, locking in residual exposure. This volatility forces importers to hold buffer inventories, tying up working capital that could otherwise fund market development.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidy Realignment Toward Balanced Fertilization

- Emergence of Specialty Chelated Blends for Arid Soils

- Fragmented Distribution Networks in the Sahel and the Horn of Africa

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc captured 34.4% share of the Middle East and Africa micronutrient fertilizers market in 2025 because it corrects widespread soil deficiencies and underpins regional grain fortification mandates. The segment's leadership comes from the dual need to close yield gaps and raise the nutritional value of staple foods.

Molybdenum is forecast to grow the quickest at an 8.8% CAGR through 2031 as legume expansion and nitrogen-fixation programs accelerate its uptake. Iron and manganese blends continue to serve greenhouse tomatoes and peppers, where color and shelf life hinge on balanced levels of these trace elements. Copper demand is rising in Morocco's olives due to its combined nutritional and disease-control properties, and boron remains critical for fruit-quality management in Turkey and Mediterranean vegetables. Suppliers are bundling multi-micronutrient coatings that merge these elements into single granules, simplifying logistics for large cereal farms.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- Geography

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

List of Companies Covered in this Report:

- Yara International ASA

- ICL Group Ltd

- Unikeyterra Tarim Sanayi ve Ticaret A.S.

- Kynoch Fertilizer (Maizey Investments Ltd)

- Gavilon South Africa (MacroSource, LLC)

- Azra Group Tarim A.S.

- BASF SE

- Haifa Chemicals Ltd

- Koch Industries Inc.

- Sociedad Quimica y Minera de Chile S.A. (SQM S.A.)

- Coromandel International Ltd (Murugappa Group)

- Valagro S.p.A. (Syngenta Group Co., Ltd.)

- BMS Micro-Nutrients NV

- Brandt Consolidated Inc.

- Grupa Azoty S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 EXECUTIVE SUMMARY

3 REPORT OFFERS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Climate-Induced Soil Micronutrient Depletion

- 4.6.2 Growth of Controlled-Environment Agriculture Hubs

- 4.6.3 Government Subsidy Realignment Toward Balanced Fertilization

- 4.6.4 Emergence of Specialty Chelated Blends for Arid Soils

- 4.6.5 Expansion of Zinc-Enriched Staple Food Fortification Mandates

- 4.6.6 Rise of Regenerative Agriculture Certification Schemes

- 4.7 Market Restraints

- 4.7.1 Volatile Foreign-Exchange Regimes Impacting Import Costs

- 4.7.2 Fragmented Distribution Networks in Sahel and Horn of Africa

- 4.7.3 Limited Local Production Capacity for Chelated Formulations

- 4.7.4 Farmer Price Sensitivity Amid Subsidy Phase-Outs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 Geography

- 5.4.1 Nigeria

- 5.4.2 Saudi Arabia

- 5.4.3 South Africa

- 5.4.4 Turkey

- 5.4.5 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 ICL Group Ltd

- 6.4.3 Unikeyterra Tarim Sanayi ve Ticaret A.S.

- 6.4.4 Kynoch Fertilizer (Maizey Investments Ltd)

- 6.4.5 Gavilon South Africa (MacroSource, LLC)

- 6.4.6 Azra Group Tarim A.S.

- 6.4.7 BASF SE

- 6.4.8 Haifa Chemicals Ltd

- 6.4.9 Koch Industries Inc.

- 6.4.10 Sociedad Quimica y Minera de Chile S.A. (SQM S.A.)

- 6.4.11 Coromandel International Ltd (Murugappa Group)

- 6.4.12 Valagro S.p.A. (Syngenta Group Co., Ltd.)

- 6.4.13 BMS Micro-Nutrients NV

- 6.4.14 Brandt Consolidated Inc.

- 6.4.15 Grupa Azoty S.A.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球微量元素肥料市場報告

2026年全球微量元素肥料市場報告 微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)

微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)