|

市場調查報告書

商品編碼

2073611

亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

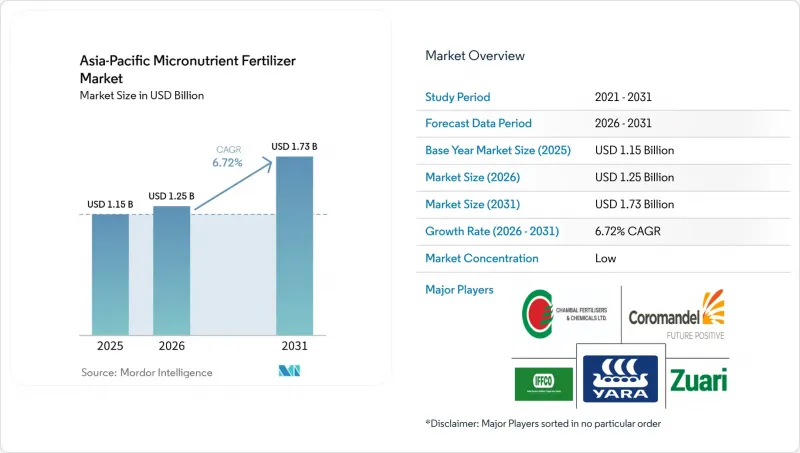

據 Mordor Intelligence 稱,亞太地區微量元素肥料市場在 2025 年的價值為 11.5 億美元,預計到 2031 年將從 2026 年的 12.5 億美元成長到 17.3 億美元,在預測期(2026-2031 年)內的複合年成長率為 6.72%。

本報告按產品(硼、銅、鐵、錳、鉬等)、應用方法(施肥/灌溉、葉面噴布等)、作物類型(田間作物、園藝作物等)和地區(澳洲、孟加拉、中國、印度等)進行細分。市場預測以價值(美元)和數量(公噸)表示。

亞太地區微量元素肥料市場的趨勢與洞察

中國的鋅補貼計畫旨在解決「隱性飢餓」危機

中國以營養為重點的補貼計畫正在將省級資金重新分配給鋅強化肥料,這種肥料不僅能提高作物產量,還能增加穀物中的微量元素濃度。這項措施透過重新定義基於穀物鋅含量的產品成功指標,並將公共衛生目標與農場實踐相結合,推動亞太地區微量元素肥料市場向更高價值的配方轉型。田間試驗顯示,葉面噴布噴施鋅生物強化肥料比土壤施用效果高出55.2%,促進了新一代葉面噴布產品的研發。鄰國正密切關注中國的這項計劃,並試圖複製其在公共衛生領域的成就,這將產生連鎖反應,並進一步催生對專業供應商的潛在需求。

澳洲保護性農業中的施肥和灌溉革命

在水資源匱乏的澳大利亞,藍莓和其他溫室水果作物的高密度種植優先考慮施肥和灌溉,以最大限度地減少浪費並精準控制施肥時間。這種轉變促使人們傾向於使用完全水溶性的螯合微量元素肥料,儘管價格較高,但這些肥料能夠顯著提高產量和品質。早期採用者報告稱,缺鐵性黃化病的發生率降低,出口漿果的硬度也提高,這推動了紐西蘭和東南亞溫室的後續投資。因此,施肥和灌溉種植面積的擴大是亞太地區微量元素肥料市場成長最快的應用領域的主要驅動力。

原物料價格波動限制了市場進入。

由於中國嚴格的環保法規導致礦場關閉,高等級硫酸鋅礦供應受限,推高了原物料成本,並影響了微量元素價格的波動。經銷商難以對沖庫存風險,被迫定期提價。這加劇了小規模農戶的現金流壓力,並阻礙了產品的推廣應用。螯合劑和奈米製劑等依賴高純度原料的產品面臨著不成比例的成本壓力,限制了這些高效能產品在亞太微量元素肥料市場的普及。

細分市場分析

預計到2025年,鋅將在亞太地區微量元素肥料市場佔據最大佔有率(34.2%),這主要得益於農業土壤中普遍存在的鋅缺乏問題,以及鋅在作物生長、養分吸收和產量提升方面發揮的關鍵作用。鋅在穀物、油籽和園藝作物中的廣泛應用,以及螯合劑、敷料和水溶性配方等產品的持續創新,提高了養分利用效率,都促進了這一領域的成長。此外,主要農業經濟體政府主導的土壤檢測計畫和平衡施肥方案的推廣,進一步推動了對鋅的需求,鞏固了其在亞太微量元素肥料市場的主導地位。

預計2026年至2031年間,硼肥的複合年成長率將達到9.2%,成為成長最快的產品類別。這一成長主要得益於水果、蔬菜、油籽和種植作物種植面積的擴大,這些作物都需要硼肥來促進開花、授粉、結果和提高品質。此外,施肥、灌溉和葉面噴施等養分管理技術的日益普及,也推動了各種種植系統對水溶性和專用硼肥的需求。同時,鐵、銅和錳等微量元素持續滿足作物特定的營養需求,確保亞太地區微量元素肥料市場擁有均衡的產品系列,涵蓋高銷售產品和高附加價值產品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 大田作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 中國的鋅補貼旨在解決「隱性飢餓」危機。

- 澳洲保護性園藝的施肥和灌溉革命

- 印度的「土壤健康卡」旨在推廣系統的微量元素檢測。

- 數位平台加速了微量營養素的精準利用。

- 特色作物的擴張正在推動客製化需求。

- 消費者對強化食品的需求正在推動農場層面的生物強化。

- 市場限制因素

- 原物料價格波動阻礙了市場進入。

- 信貸限制阻礙了高階產品的推出。

- 仿冒品損害農民的聲譽。

- 港口瓶頸延誤了螯合微量營養素的出口。

第5章 市場規模與成長預測

- 產品

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 使用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 地區

- 澳洲

- 孟加拉

- 中國

- 印度

- 印尼

- 日本

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太國家

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- Yara International ASA

- Chambal Fertilisers and Chemicals Limited

- Zuari Agro Chemicals Limited

- Coromandel International Limited

- Indian Farmers Fertiliser Cooperative Limited

- Compo Expert GmbH(Grupa Azoty SA)

- Haifa Negev Technologies Ltd.(Haifa Group)

- ICL Fertilizers(ICL Group Ltd.)

- Kingenta Ecological Engineering Group Co., Ltd.

- Nutrien Ltd.

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Gujarat State Fertilizers and Chemicals Limited

- OMEX Agriculture Ltd.(OMEX Group)

- Valagro SpA(Syngenta Group)

- Balchem Plant Nutrition(Balchem Corporation)

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the asia-Pacific micronutrient fertilizer market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.25 billion in 2026 to reach USD 1.73 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031).

This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, and More), Application Mode (Fertigation, Foliar, and More), Crop Type (Field Crops, Horticultural Crops, and More), and Geography (Australia, Bangladesh, China, India, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Asia-Pacific Micronutrient Fertilizer Market Trends and Insights

China's Zinc Subsidies Target Hidden Hunger Crisis

China's nutrition-centric subsidy scheme reallocates provincial funds toward zinc-enriched fertilizers that lift grain micronutrient density instead of merely boosting yields. The initiative reframes product success metrics around grain zinc content and aligns public health goals with farm-level practices, pushing the Asia-Pacific micronutrient fertilizer market toward value-added formulations. Field evidence shows foliar zinc delivers 55.2% higher biofortification efficacy than soil application, spurring R&D into next-generation foliar sprays. Multiplier effects arise as neighboring countries monitor China's program to replicate its public health gains, unlocking additional addressable demand for specialized suppliers.

Australia's Fertigation Revolution in Protected Horticulture

Water-scarce Australia prioritizes fertigation to minimize waste and fine-tune nutrient timing for high-density blueberries and other greenhouse fruit crops. This shift favors fully water-soluble chelated micronutrients that command premium pricing yet deliver measurable yield-and-quality gains. Early adopters report reductions in iron chlorosis episodes and improved firmness in export berries, catalyzing copy-cat investments in New Zealand and Southeast Asian greenhouses. Rising fertigation acreage, therefore, underwrites the fastest-growing application segment of the Asia-Pacific micronutrient fertilizer market.

Raw-Material Price Volatility Constrains Market Accessibility

China's mine closures under stringent environmental mandates curtail the supply of high-grade zinc sulfate ores, lifting feedstock costs and cascading into micronutrient price swings. Distributors struggle to hedge inventories, forcing periodic price hikes that strain smallholders' cash flow and hinder uptake. Chelated and nano formulations, which rely on purer inputs, bear disproportionate cost pressure, narrowing the adoption of these high-efficacy options within the Asia-Pacific micronutrient fertilizer market.

Other drivers and restraints analyzed in the detailed report include:

- Digital Platforms Accelerate Precision Micronutrient Applications

- Specialty-Crop Expansion Drives Customized Demand

- Credit Constraints Limit Premium Product Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc accounted for the largest Asia-Pacific micronutrient fertilizer market share, 34.2% in 2025, supported by widespread zinc deficiencies across agricultural soils and its critical role in crop growth, nutrient uptake, and yield improvement. The segment benefits from strong adoption across cereals, oilseeds, and horticultural crops, while continued product innovation in chelated, coated, and water-soluble formulations is enhancing nutrient-use efficiency. Growing government-led soil testing initiatives and balanced fertilization programs across major agricultural economies are further supporting zinc demand and reinforcing its leadership position in the Asia-Pacific micronutrient fertilizer market.

Boron is anticipated to be the fastest-growing product segment, with a projected CAGR of 9.2% during 2026 to 2031. This growth is fueled by the increasing cultivation of fruits, vegetables, oilseeds, and plantation crops, which require boron for flowering, pollination, fruit set, and quality improvement. The rising adoption of fertigation and foliar nutrient management practices is boosting demand for soluble and specialty boron formulations across various cropping systems. Meanwhile, micronutrients such as iron, copper, and manganese continue to address crop-specific nutrient deficiencies, ensuring a balanced portfolio of high-volume and value-added products in the Asia-Pacific micronutrient fertilizer market.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

- Geography

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Yara International ASA

- Chambal Fertilisers and Chemicals Limited

- Zuari Agro Chemicals Limited

- Coromandel International Limited

- Indian Farmers Fertiliser Cooperative Limited

- Compo Expert GmbH (Grupa Azoty S.A.)

- Haifa Negev Technologies Ltd. (Haifa Group)

- ICL Fertilizers (ICL Group Ltd.)

- Kingenta Ecological Engineering Group Co., Ltd.

- Nutrien Ltd.

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Gujarat State Fertilizers and Chemicals Limited

- OMEX Agriculture Ltd. (OMEX Group)

- Valagro S.p.A. (Syngenta Group)

- Balchem Plant Nutrition (Balchem Corporation)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 China's Zinc Subsidies Target Hidden Hunger Crisis

- 4.6.2 Australia's Fertigation Revolution in Protected Horticulture

- 4.6.3 India's Soil Health Cards Drive Systematic Micronutrient Testing

- 4.6.4 Digital Platforms Accelerate Precision Micronutrient Applications

- 4.6.5 Specialty-Crop Expansion Drives Customized Demand

- 4.6.6 Consumer Demand for Fortified Foods Spurs Farm-Level Biofortification

- 4.7 Market Restraints

- 4.7.1 Raw-Material Price Volatility Constrains Market Accessibility

- 4.7.2 Credit Constraints Limit Premium Product Adoption

- 4.7.3 Counterfeit Products Erode Farmer Confidence

- 4.7.4 Port Bottlenecks Delay Chelated Micronutrient Exports

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Geography

- 5.4.1 Australia

- 5.4.2 Bangladesh

- 5.4.3 China

- 5.4.4 India

- 5.4.5 Indonesia

- 5.4.6 Japan

- 5.4.7 Pakistan

- 5.4.8 Philippines

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 Chambal Fertilisers and Chemicals Limited

- 6.4.3 Zuari Agro Chemicals Limited

- 6.4.4 Coromandel International Limited

- 6.4.5 Indian Farmers Fertiliser Cooperative Limited

- 6.4.6 Compo Expert GmbH (Grupa Azoty S.A.)

- 6.4.7 Haifa Negev Technologies Ltd. (Haifa Group)

- 6.4.8 ICL Fertilizers (ICL Group Ltd.)

- 6.4.9 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.10 Nutrien Ltd.

- 6.4.11 Deepak Fertilisers and Petrochemicals Corporation Limited

- 6.4.12 Gujarat State Fertilizers and Chemicals Limited

- 6.4.13 OMEX Agriculture Ltd. (OMEX Group)

- 6.4.14 Valagro S.p.A. (Syngenta Group)

- 6.4.15 Balchem Plant Nutrition (Balchem Corporation)

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球微量元素肥料市場報告

2026年全球微量元素肥料市場報告 微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)

微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)