|

市場調查報告書

商品編碼

2073597

中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)China Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

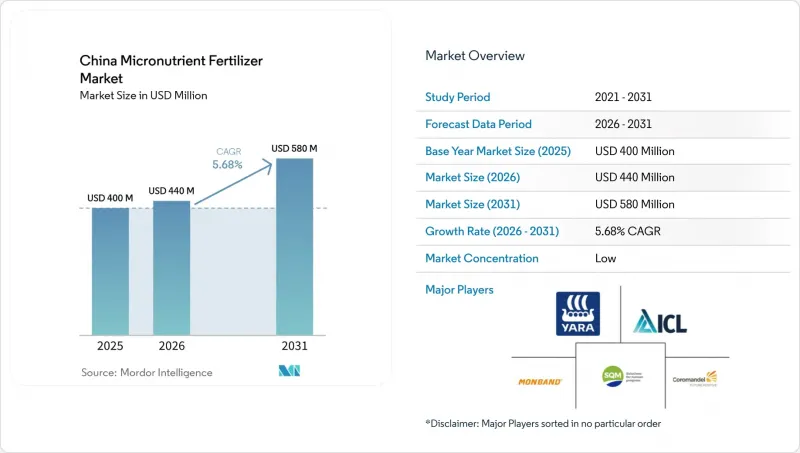

根據 Mordor Intelligence 預測,中國微量元素肥料市場規模預計將從 2025 年的 4 億美元成長到 2026 年的 4.4 億美元。

本報告按產品(硼、銅、鐵、錳、鉬、鋅及其他)、施用方法(施肥/灌溉、葉面噴布、土壤施用)和作物類型(田間作物、園藝作物、草坪/觀賞作物)進行分類。市場預測以價值(美元)和數量(公噸)表示。

中國微量元素肥料市場趨勢與洞察

精密農業的引進正在加速對微量營養素的需求。

中國的農業技術革命正透過最佳化施肥地點和時間的可變施肥系統,推動微量元素肥料的需求成長。政府支持的智慧農業舉措已使全部區域的智慧農業技術普及率達到27.6%,從而催生了對可與GPS導航噴霧器相容的精準配製微量元素肥料的需求。這項技術變革使農民能夠根據土壤分析數據,為每個田地施用最佳量的微量元素,從而提高施肥效率和總用量。物聯網感測器和無人機監測系統的整合,實現了微量元素施用量的即時調整,尤其適用於需要精準管理鋅和硼的高價值作物。隨著精密農業普及,農民透過有針對性的養分管理方案而非均勻施肥來最佳化產量潛力,因此每公頃微量元素的用量也不斷增加。

強制性土壤養分分析計劃

中國農業部將於2025年實施的《土壤檢測指令》要求農民在申請化肥補貼前必須進行經認證的土壤養分分析,這將從根本上改變微量元素的購買模式。由於農民需要證明土壤存在養分缺乏才能獲得政府補貼,因此這項政策轉變勢必會催生對特定土壤的微量元素推薦的需求。這項強制性檢測將尤其有利於提供土壤分析服務和定製配方能力的微量元素供應商,因為農民正在尋求集檢測、推薦和產品供應於一體的綜合解決方案。各省的執行力度有所不同,河南、山東等主要糧食產區實施了最嚴格的合規要求。這個法律規範正在將微量元素肥料從“可有可無的投入”轉變為“必須有記錄的必需品”,從而支持所有作物類型和施用方式的永續銷售量成長。

都市化導致耕地面積減少

由於都市化發展的壓力,中國可耕種面積不斷減少,儘管農業集約化程度不斷提高,但仍對微量元素肥料的銷售量成長構成結構性阻力。土地轉為工業用地和住宅用地,每年導致約20萬公頃農業生產面積損失,直接縮小了土壤施用微量元素產品的潛在市場。這種限制迫使業界轉向高附加價值解決方案,以最大限度地提高每公頃的養分利用效率,而不是簡單地增加總施用量。沿海地區的土地壓力最為嚴重,導致剩餘農地集中化,並轉向規模更大、效率更高的農業經營模式,強調批量採購和精準施肥技術。雖然這種土地限制看似矛盾,但實際上卻支撐了對高品質微量元素產品的需求,因為農民在面積面積減少的情況下力求實現最大產量,但最終卻限制了整個市場的成長潛力。

細分市場分析

預計到2025年,鋅將佔據中國微量元素肥料市場最大的佔有率(34.6%),這主要得益於農業土壤中普遍存在的鋅缺乏問題,以及鋅在促進作物生長、養分吸收和提高產量方面的重要作用。鋅的需求依然強勁,尤其是在穀物、油籽和園藝作物領域。此外,螯合鋅和水溶性鋅製劑的日益普及提高了養分利用效率。政府主導的土壤檢測舉措和精準養分管理計畫進一步擴大了全部區域的鋅肥消費量。

預計2026年至2031年間,硼肥的複合年成長率將達到8.9%,成為成長最快的產品類別。這一成長主要得益於水果、蔬菜和其他高價值作物種植面積的擴大,硼在這些作物的開花、授粉、坐果和作物品質方面發揮著至關重要的作用。此外,施肥和灌溉系統以及專業營養方案的日益普及也進一步推高了對硼肥的需求,尤其是在集約化園藝生產地區。同時,鐵、銅、錳、鉬等其他微量元素也持續為解決作物特定營養缺乏問題做出貢獻,推動了中國微量元素肥料市場的整體成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 大田作物

- 園藝作物

- 平均施肥量

- 主要營養素

- 田間作物

- 園藝作物

- 主要營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 精密農業的日益普及正在加速對微量營養素的需求。

- 強制性土壤養分檢測計劃

- 政府補助有利於螯合劑

- 長江Delta地區高科技溫室的擴張

- 特色水果出口快速成長

- 國內硫酸鋅生產已實現規模經濟。

- 市場限制因素

- 都市化導致耕地減少

- 微量金屬污染的允許限值和噴灑速率

- 原物料價格波動

- 農民對投入成本上升的價格敏感性

第5章 市場規模與成長預測

- 產品

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 使用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介。

- Yara International ASA

- ICL Group Ltd

- Hebei Monband Water Soluble Fertilizer Co. Ltd

- Sociedad Quimica y Minera de Chile SA

- Coromandel International Ltd.

- Kingenta Group

- Sinochem Holdings Corp. Ltd.

- ChemChina

- Grupa Azoty SA

- The Mosaic Company

- Nutrien Ltd.

- Haifa Chemicals Ltd.

- Tradecorp International SA(Rovensa Group)

- Anhui Huaheng Biotechnology Co., Ltd.

- Sichuan Shucan Chemical Co., Ltd.

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the china micronutrient fertilizer market size is estimated at USD 440.0 million in 2026, up from USD 400.0 million in 2025. This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, and Others), by Application Mode (Fertigation, Foliar, and Soil), and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

China Micronutrient Fertilizer Market Trends and Insights

Precision-Farming Adoption Accelerates Micronutrient Demand

China's agricultural technology revolution drives micronutrient fertilizer demand through variable-rate application systems that optimize nutrient placement and timing. Government-backed smart agriculture initiatives have achieved 27.6% adoption of intelligent agriculture technologies across production areas, creating demand for precision-formulated micronutrient blends compatible with GPS-guided applicators . This technological shift enables farmers to apply micronutrients at field-specific rates based on soil testing data, increasing both application efficiency and total consumption volumes. The integration of Internet of Things sensors and drone-based monitoring systems allows real-time adjustment of micronutrient applications, particularly for high-value crops requiring precise zinc and boron management. Precision farming adoption correlates with higher per-hectare micronutrient usage as farmers optimize yield potential through targeted nutrition programs rather than blanket applications.

Mandated Soil Nutrient Testing Programs

China's Ministry of Agriculture soil testing directive, effective 2025, requires certified soil nutrient analysis before farmers can claim fertilizer subsidies, fundamentally altering micronutrient purchasing patterns. This policy shift creates mandatory demand for soil-specific micronutrient recommendations, as farmers must demonstrate nutrient deficiencies to access government support programs. The testing mandate particularly benefits micronutrient suppliers offering soil analysis services and customized blending capabilities, as farmers seek integrated solutions combining testing, recommendation, and product supply. Provincial implementation varies in enforcement rigor, with major grain-producing regions like Henan and Shandong showing the strictest compliance requirements. This regulatory framework transforms micronutrient fertilizers from optional inputs to documented necessities, supporting sustained volume growth across all crop types and application methods.

Arable-Land Shrinkage Due to Urbanization

Urban development pressure reduces China's cultivable land area, creating a structural headwind for volume-based micronutrient fertilizer growth despite intensification efforts. Land conversion to industrial and residential uses removes approximately 200,000 hectares annually from agricultural production, directly reducing the addressable market for soil-applied micronutrient products. This constraint forces the industry toward value-added solutions that maximize nutrient efficiency per hectare rather than expanding total application volumes. Coastal provinces experience the most severe land pressure, driving consolidation of remaining farmland into larger, more efficient operations that favor bulk purchasing and precision application technologies. The land constraint paradoxically supports premium micronutrient products as farmers seek maximum yield from reduced acreage, but ultimately limits total market expansion potential.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies Favor Chelated Formulations

- Expansion Of High-Tech Greenhouses in Yangtze Delta

- Trace-Metal Contamination Limits Application Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc accounted for the largest China micronutrient fertilizer market share, 34.6% in 2025, supported by widespread zinc deficiencies in agricultural soils and its essential role in enhancing crop growth, nutrient uptake, and yield performance. Demand for zinc remains particularly strong in cereals, oilseeds, and horticultural crops. Additionally, the increasing adoption of chelated and water-soluble zinc formulations is improving nutrient-use efficiency. Government-led soil testing initiatives and precision nutrient management programs are further boosting zinc fertilizer consumption across key agricultural regions.

Boron is anticipated to be the fastest-growing product segment, with a projected CAGR of 8.9% during 2026 to 2031. This growth is driven by the expanding cultivation of fruits, vegetables, and other high-value crops, where boron is critical for flowering, pollination, fruit set, and crop quality. The rising adoption of fertigation systems and specialty nutrient programs is further increasing demand for boron-based fertilizers, particularly in intensive horticultural production areas. Meanwhile, other micronutrients such as iron, copper, manganese, and molybdenum continue to address crop-specific nutrient deficiencies, contributing to the overall growth of the China micronutrient fertilizer market.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

List of Companies Covered in this Report:

- Yara International ASA

- ICL Group Ltd

- Hebei Monband Water Soluble Fertilizer Co. Ltd

- Sociedad Quimica y Minera de Chile SA

- Coromandel International Ltd.

- Kingenta Group

- Sinochem Holdings Corp. Ltd.

- ChemChina

- Grupa Azoty S.A.

- The Mosaic Company

- Nutrien Ltd.

- Haifa Chemicals Ltd.

- Tradecorp International S.A. (Rovensa Group)

- Anhui Huaheng Biotechnology Co., Ltd.

- Sichuan Shucan Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-farming adoption accelerates micronutrient demand

- 4.6.2 Mandated soil nutrient testing programs

- 4.6.3 Government subsidies favoring chelated formulations

- 4.6.4 Expansion of high-tech greenhouses in Yangtze Delta

- 4.6.5 Rapid growth of specialty fruit exports

- 4.6.6 Domestic production of zinc sulfate reaches scale economies

- 4.7 Market Restraints

- 4.7.1 Arable-land shrinkage due to urbanization

- 4.7.2 Trace-metal contamination limits application rates

- 4.7.3 Volatility in raw-material prices

- 4.7.4 Farmer price-sensitivity amid rising input costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Yara International ASA

- 6.4.2 ICL Group Ltd

- 6.4.3 Hebei Monband Water Soluble Fertilizer Co. Ltd

- 6.4.4 Sociedad Quimica y Minera de Chile SA

- 6.4.5 Coromandel International Ltd.

- 6.4.6 Kingenta Group

- 6.4.7 Sinochem Holdings Corp. Ltd.

- 6.4.8 ChemChina

- 6.4.9 Grupa Azoty S.A.

- 6.4.10 The Mosaic Company

- 6.4.11 Nutrien Ltd.

- 6.4.12 Haifa Chemicals Ltd.

- 6.4.13 Tradecorp International S.A. (Rovensa Group)

- 6.4.14 Anhui Huaheng Biotechnology Co., Ltd.

- 6.4.15 Sichuan Shucan Chemical Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球微量元素肥料市場報告

2026年全球微量元素肥料市場報告 微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)

微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)