|

市場調查報告書

商品編碼

2073613

南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

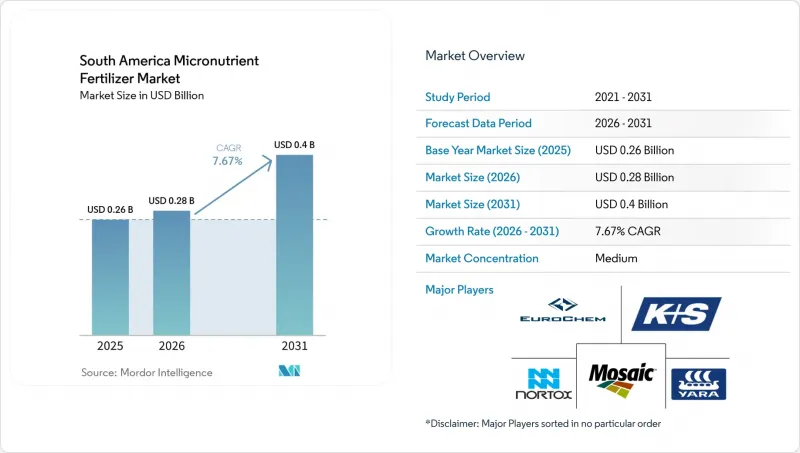

據 Mordor Intelligence 稱,2025 年南美微量元素肥料市場價值 2.6 億美元,預計到 2031 年將達到 4 億美元,而 2026 年為 2.8 億美元,預測期(2026-2031 年)的複合年成長率為 7.67%。

本報告按產品(硼、銅、鐵、錳、鉬、鋅及其他)、施用方法(施肥/灌溉、葉面噴布、土壤施用)、作物類型(田間作物、園藝作物、草坪/觀賞作物)和國家(阿根廷、巴西和其他南美國家)進行細分。市場預測以價值(美元)和數量(公噸)表示。

南美微量元素肥料市場的趨勢與洞察

鋅缺乏土壤的普遍存在推動了對土壤改良的需求。

廣泛的土壤檢測表明,巴西和阿根廷超過一半的農田中,DTPA可提取鋅的濃度低於臨界閾值,凸顯了持續補充鋅的結構性需求。光是在阿根廷潘帕斯草原地區,就有1,215萬公頃土地受到缺鋅影響。在巴西塞拉多地區,即使土壤中的總鋅含量看似充足,高pH值也會進一步降低鋅的生物效能。因此,由於蛋白質和穀物品質下降,出口溢價損失,生產者不得不投資於補鋅項目。通常,恢復最佳土壤條件需要兩個以上的生長季。由於土壤中鋅的恢復是一個漸進的過程,可預測的補鋅週期能夠穩定供應商的採購量。這種缺鋅問題的持續性支持了微量元素肥料市場的長期成長。

擴大大豆和玉米種植面積

巴西糧食產量預計將在2025年達到創紀錄的3.41億噸,這反映了大豆和玉米面積的持續擴張,目前這兩種作物佔種植面積的四分之三。大豆透過促進固氮作用增加了對鉬的需求,而玉米則吸收大量的鉀和磷,這往往會導致鋅和錳的繼發性缺乏。雜交玉米品種需要增加15%至20%的鋅才能最大限度地發揮其產量潛力,這進一步增加了每公頃對微量元素的需求。阿根廷的種植戶在邊際土地上擴張種植,面臨土壤有機質含量低的問題,進一步加劇了微量元素的流失。目前出口合約對微量元素含量有最低要求,進一步強化了商業性對均衡營養管理方案的需求。種植面積的擴大和品質標準的提高共同刺激了微量元素肥料市場的持續訂單。

小規模農戶對價格高度敏感

巴西和阿根廷約有60%的農場規模小於100公頃,許多農場依賴每噸約800美元的基礎硫酸鹽肥料,而螯合態肥料的價格通常超過每噸2000美元。融資項目優先考慮氮磷鉀複合肥,導致微量元素肥料資金不足。合作採購可以抵銷部分成本,但難以滿足土壤多樣化的需求。隨著大宗商品價格下跌,生產者會減少投入,即使螯合態微量元素肥料的農藝投資報酬率顯而易見,也會延後其應用。因此,供應商需要在高階定位和價格適中的入門級產品之間取得平衡,以維持其在微量元素肥料市場的滲透率。

細分市場分析

2025年,鋅佔南美微量元素肥料市場31.4%的佔有率,預計將成為成長最快的肥料,2026年至2031年的複合年成長率將達到7.0%。覆蓋1215萬公頃的改良性施肥應用鞏固了鋅在市場上的主導地位。受出口合約中嚴格的穀物品質標準的推動,對鋅基微量元素肥料的需求預計將穩步成長。儘管鉬的市場規模較小,但隨著大豆種植面積的增加,人們對固氮效率的關注度日益提高,鉬的成長速度也正在加快。銅、鐵和錳則滿足了特定作物細分市場的需求,例如智利的果樹、阿根廷的小麥以及高pH值大豆種植區。硼仍然是咖啡和芒果等開花作物必不可少的元素。儘管成本較高,但先進的螯合技術,特別是 EDDHA,在高 pH 值地區正獲得越來越多的關注,這表明人們正在從鹼性硫酸鹽轉向更高價值的化學產品。

隨著人們對次生營養缺乏症的認知不斷提高,種植者擴大採用多種微量元素配方來減少隱性產量損失。提供鋅、錳、硼複合產品的供應商正透過交叉銷售獲得綜效。巴西的法規加速了國內產能的擴張,而本地螯合劑的生產可望縮小價格差異,並促進產品的推廣應用。同時,與奈米封裝和緩釋製劑相關的專利活動可望逐步提高養分利用效率,進一步豐富產品線,並支持長期市場價值成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 田間作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 土壤缺鋅現象普遍存在,推動了土壤改良的需求。

- 擴大大豆和玉米種植面積

- 精密農業的引進與土壤檢測的普及

- 《2050年國家化肥規劃》中關於促進國內供應的獎勵

- 用於專門食品咖啡和水果出口的優質微量營養素混合物。

- 甘蔗乙醇叢集引進施肥和灌溉基礎設施

- 市場限制因素

- 小規模農戶對價格非常敏感。

- 物流瓶頸推高了配送成本。

- 工業金屬供應量依產品類型分類的差異。

- 出口市場螯合物殘留物的審查

第5章 市場規模與成長預測

- 依產品

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 透過應用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 按作物類型

- 大田作物

- 園藝作物

- 草坪和觀賞植物

- 國家

- 阿根廷

- 巴西

- 其他南美國家

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- BMS Micro-Nutrients NV

- Grupa Azoty SA(Compo Expert GmbH)

- EuroChem Group

- Haifa Group

- ICL Group Ltd

- Inquima LTDA

- K+S Aktiengesellschaft

- Nortox SA

- The Mosaic Company

- Yara International ASA

- Nutrien

- SQM SA

- TIMAC Agro Brasil(Groupe Roullier)

- Koch Agronomic Services(Koch Industries Inc.)

- FertGrow

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the south america micronutrient fertilizer market size was valued at USD 0.26 billion in 2025 and estimated to grow from USD 0.28 billion in 2026 to reach USD 0.40 billion by 2031, at a CAGR of 7.67% during the forecast period (2026-2031).

This report is Segmented by Product (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, and Others), by Application Mode (Fertigation, Foliar, and Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Country (Argentina, Brazil, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

South America Micronutrient Fertilizer Market Trends and Insights

Widespread Zinc-Deficient Soils Driving Corrective Demand

Extensive soil tests reveal that more than half of Brazilian and Argentine croplands exhibit DTPA-extractable zinc levels below critical thresholds, underscoring a structural requirement for sustained zinc supplementation . These deficiencies span 12.15 million hectares across the Argentine Pampas alone . High-pH conditions in Brazil's Cerrado further diminish zinc bioavailability, even when total soil zinc appears sufficient. Resulting protein and grain-quality penalties erode export premiums, prompting growers to invest in corrective zinc programs that typically require two or more seasons to restore optimal status. Because soil zinc recovery is slow, a predictable replacement cycle stabilizes purchasing volumes for suppliers. The enduring nature of the deficiency anchors the long-term growth of the micronutrient fertilizer market.

Expansion of Soybean and Corn Acreage

Brazil's record grain harvest, projected at 341 million metric tons for 2025, reflects the continued expansion of soybean and corn acreage that today represents three-quarters of the planted area . Soybeans lift molybdenum demand by facilitating nitrogen fixation, while corn's high uptake of potassium and phosphorus often triggers secondary zinc and manganese deficiencies. Hybrid corn varieties require 15-20% more zinc to realize full yield potential, intensifying per-hectare micronutrient needs. Argentinian growers pushing into marginal lands face soils with lower organic matter, magnifying micronutrient depletion. Export contracts that now specify trace-element minimums reinforce the commercial necessity of balanced nutrient programs. Together, acreage gains and quality standards ignite recurring orders across the micronutrient fertilizer market.

High Price Sensitivity Among Smallholders

Roughly 60% of Brazilian and Argentine farms operate on less than 100 ha, and many rely on basic sulfate formulations costing around USD 800 per metric ton, while chelated alternatives often exceed USD 2,000 per metric ton. Credit programs prioritize NPK fertilizers, leaving micronutrients underfinanced. Cooperative purchases offset some costs, but struggle to align diverse soil needs. During commodity price dips, growers trim discretionary inputs, delaying chelated micronutrient adoption even when agronomic ROI is evident. Suppliers must therefore balance premium positioning with affordable entry-level offerings to sustain penetration in the micronutrient fertilizer market.

Other drivers and restraints analyzed in the detailed report include:

- Precision-ag Adoption and Soil Testing Penetration

- National Fertilizer Plan 2050 Incentives for Domestic Supply

- Logistics Bottlenecks Inflating Delivered Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc accounted for 31.4% of the South America micronutrient fertilizer market zinc in 2025 and posted the fastest growth, with a 7.0% CAGR through 2026-2031. Corrective applications across 12.15 million hectares support its sustained leadership in the market. Demand for zinc-based micronutrient fertilizers is projected to expand steadily, driven by stringent grain-quality specifications in export contracts. Molybdenum, though smaller, accelerates as soybean acreage rises, elevating attention to nitrogen-fixing efficiency. Copper, iron, and manganese cater to crop-specific niches such as Chilean fruits, Argentine wheat, and high-pH soybean soils. Boron remains essential in flowering crops such as coffee and mango. Advanced chelation, notably EDDHA, gains traction in high-pH zones despite higher prices, signaling an ongoing shift from basic sulfates toward value-added chemistries.

Growing awareness of secondary deficiencies pushes growers to adopt multi-micro mixes that mitigate hidden yield losses. Suppliers that bundle zinc with manganese and boron capture cross-selling synergies. As Brazilian regulation fast-tracks domestic capacity, local chelate production may narrow price gaps, smoothing the adoption curve. Concurrently, patent activity in nano-encapsulation and controlled-release formats promises step-wise improvements in nutrient-use efficiency, further enriching the product landscape and supporting long-term market value growth.

Complete Report Scope:

- By Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- By Application Mode

- Fertigation

- Foliar

- Soil

- By Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- By Country

- Argentina

- Brazil

- Rest of South America

List of Companies Covered in this Report:

- BMS Micro-Nutrients NV

- Grupa Azoty S.A. (Compo Expert GmbH)

- EuroChem Group

- Haifa Group

- ICL Group Ltd

- Inquima LTDA

- K+S Aktiengesellschaft

- Nortox S.A.

- The Mosaic Company

- Yara International ASA

- Nutrien

- SQM S.A.

- TIMAC Agro Brasil (Groupe Roullier)

- Koch Agronomic Services (Koch Industries Inc.)

- FertGrow

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Widespread zinc-deficient soils driving corrective demand

- 4.6.2 Expansion of soybean and corn acreage

- 4.6.3 Precision-ag adoption and soil-testing penetration

- 4.6.4 National Fertilizer Plan 2050 incentives for domestic supply

- 4.6.5 Premium micronutrient blends for specialty coffee and fruit exports

- 4.6.6 Sugarcane ethanol clusters adopting fertigation infrastructure

- 4.7 Market Restraints

- 4.7.1 High price sensitivity among smallholders

- 4.7.2 Logistics bottlenecks inflating delivered cost

- 4.7.3 Volatile by-product supply of industrial metals

- 4.7.4 Export-market scrutiny of chelate residues

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 By Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 By Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 By Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BMS Micro-Nutrients NV

- 6.4.2 Grupa Azoty S.A. (Compo Expert GmbH)

- 6.4.3 EuroChem Group

- 6.4.4 Haifa Group

- 6.4.5 ICL Group Ltd

- 6.4.6 Inquima LTDA

- 6.4.7 K+S Aktiengesellschaft

- 6.4.8 Nortox S.A.

- 6.4.9 The Mosaic Company

- 6.4.10 Yara International ASA

- 6.4.11 Nutrien

- 6.4.12 SQM S.A.

- 6.4.13 TIMAC Agro Brasil (Groupe Roullier)

- 6.4.14 Koch Agronomic Services (Koch Industries Inc.)

- 6.4.15 FertGrow

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOs

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球微量元素肥料市場報告

2026年全球微量元素肥料市場報告 微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)

微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)