|

市場調查報告書

商品編碼

2073599

印度微量元素肥料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Micronutrient Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

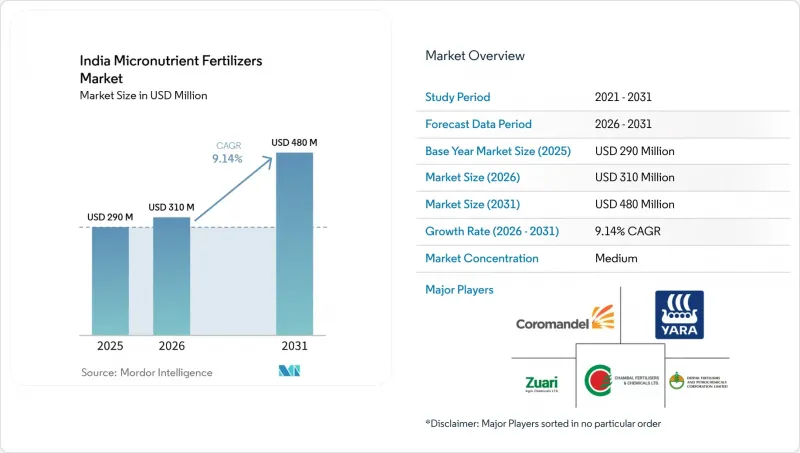

根據 Mordor Intelligence 預測,印度微量元素肥料市場規模將從 2025 年的 2.9 億美元成長到 2026 年的 3.1 億美元,然後在 2031 年達到 4.8 億美元,2026 年至 2031 年的複合年成長率為 9.14%。

本報告依產品類型(硼、銅、鐵、錳、鉬、鋅等)、應用方法(施肥/灌溉、葉面噴布等)及作物類型(田間作物、園藝作物等)分類。市場預測以價值(美元)和數量(公噸)表示。

印度微量元素肥料市場的趨勢與洞察

集約化農業地區土壤微量元素的消耗。

在旁遮普邦、哈里亞納邦和北方邦西部,水稻、小麥和棉花的連續輪作導致鋅、硼和鐵的蘊藏量速度超過了自然補充速度,儘管關鍵營養元素的施用量增加,但產量成長仍然放緩。根據土壤健康卡的數據,目前旁遮普邦78%的耕地和哈里亞納邦65%的耕地有缺鋅現象。經濟學家估計,這些缺鋅造成的年產量損失相當可觀。由於預計補充鋅肥可使小麥增產200-400公斤/公頃,水稻增產300-600公斤/公頃,各地區政府正在加強農業推廣活動。根據《肥料控制令》(FCO)強制要求對微量元素進行標籤標註,並擴大檢測能力,為品質保證奠定了基礎,這對印度的微量元素肥料市場具有結構性益處。

增加政府對強化型NPK複合肥料的補助(NBS-2)

自2024年12月起,添加微量元素的磷酸二銨(DAP)和複合肥料(NPK)可直接獲得農民補貼,零售價格因此降低了40-50%。這使得馬哈拉斯特拉邦、卡納塔克邦、安得拉邦和泰米爾納德邦的肥料採用率從2022年的15%提高到2024年的28%。國家肥料標準(NBS)框架內的預算撥款從2023-24會計年度的7950億印度盧比(約合96.2億美元)增加到2024-25會計年度的8750億印度盧比(約合105億美元),支持印度農民混合合作社(IFFCO)和科羅曼德爾肥料公司等產能提高其35%。透過基層農業信用合作社進行數位化追蹤降低了肥料濫用的風險,而強制性的《肥料控制令》(FCO)標準確保每袋售出的肥料都含有有效含量的鋅、硼或鐵。由於補貼將提前發放,預計未來兩季市場擴張將最為顯著,但即使在補貼期結束後,人們對均衡營養的意識也可能持續存在。

在二三級農產品市場分銷假冒仿冒品產品。

在比哈爾邦、北方邦和奧裡薩邦,偽裝成微量元素肥料的劣質粉末佔供應量的15-20%,這些地區的農業市場幾乎被小規模經銷商壟斷。實驗室檢測表明,這些產品的金屬含量比標示值低30-50%,導致作物歉收,並抑制了消費者購買正品的意願。由於缺乏檢查人員和經認證的檢測機構,《肥料控制條例》的執行受到阻礙。主要生產商已引入QR碼認證,但智慧型手機普及率的差異和數位素養的低阻礙了其應用。在認證系統擴展和對經銷商的審查得到加強之前,仿冒品的湧入預計將在短期內使印度微量元素肥料市場的複合年成長率下降1.2個百分點。

細分市場分析

預計到2025年,鋅製劑將佔據印度微量元素肥料市場35.9%的佔有率,凸顯其在解決該國最普遍的土壤養分缺乏問題方面發揮的關鍵作用。市場需求依然強勁,尤其是在稻米、小麥和玉米種植中,施用鋅肥可直接提高產量和養分利用效率。此外,土壤檢測力度的加大和平衡施肥方案的推廣也進一步鞏固了鋅製劑市場的地位。

市場正逐步轉向硼基產品,預計2026年至2031年間的複合年成長率將達到10.6%。水果、蔬菜、油籽和種植作物種植面積的擴大推動了對硼的需求,硼在開花、授粉、結果和作物生長中發揮著至關重要的作用。此外,專用微量元素混合物和適用於滴灌施肥的配方日益普及,為傳統鋅產品以外的市場創造了新的成長機會。含鐵、銅、錳和鉬的肥料在解決印度多樣化農業系統中作物和區域特有的營養缺乏問題方面繼續發揮著重要的補充作用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:執行摘要和主要發現

第3章:本報告的內容

第4章:主要產業趨勢

- 主要農作物種植面積

- 大田作物

- 園藝作物

- 平均施肥量

- 微量營養素

- 田間作物

- 園藝作物

- 微量營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 集約化農業區土壤微量元素的消耗

- 延長政府對強化型NPK複合肥料的補助(NBS-2)

- 特殊螯合劑在園藝叢集中的快速擴散

- 根據總理農業灌溉計劃(PMKSY)微灌計劃,擴大施肥和灌溉基礎設施。

- 印度一家農業科技新創公司開發出新型奈米和微量營養素產品

- 因微量元素增產而獲得的排碳權溢價

- 市場限制因素

- 在二三級農產品市場分銷假冒仿冒品產品。

- 鋅和硼精礦開採價格的波動

- 東部和東北部各州農民的意識水平較低

- 微量營養素向內陸地區大宗運輸存在物流瓶頸。

第5章 市場規模與成長預測

- 產品

- 硼

- 銅

- 鐵

- 錳

- 鉬

- 鋅

- 其他

- 使用方法

- 施肥和灌溉

- 葉面噴布

- 土壤

- 作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- Coromandel International Limited

- Chambal Fertilizers and Chemicals Limited

- Indian Farmers Fertiliser Cooperative Limited

- Deepak Fertilizers and Petrochemicals Corporation Limited

- Zuari Agro Chemicals Limited

- Rashtriya Chemicals and Fertilizers Limited

- Aries Agro Limited

- Tata Chemicals Limited

- Mangalore Chemicals and Fertilizers Limited

- Nagarjuna Fertilizers and Chemicals Limited

- BASF India Limited

- Compo Expert India Private Limited

- Haifa Chemicals Ltd

- Yara Fertilisers India Private Limited

- Sociedad Quimica y Minera de Chile SA(SQM)India Private Limited

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the india micronutrient fertilizers market size is projected to grow from USD 290.0 million in 2025 to USD 310.0 million in 2026 and is forecast to reach USD 480.0 million by 2031 at 9.14% CAGR over 2026 to 2031.

This report is Segmented by Product Type (Boron, Copper, Iron, Manganese, Molybdenum, Zinc, and More), by Application Mode (Fertigation, Foliar, and More), and by Crop Type (Field Crops, Horticultural Crops, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

India Micronutrient Fertilizers Market Trends and Insights

Rising Soil Micronutrient Depletion Across Intensively Farmed Districts

Continuous rice-wheat and cotton cycles in Punjab, Haryana, and Western Uttar Pradesh have depleted zinc, boron, and iron reserves faster than natural replenishment, resulting in reduced yield gains despite increased macronutrient use. Soil Health Card data show that 78% of Punjab's and 65% of Haryana's cultivated soils now test zinc-deficient . Economists estimate significant annual output losses associated with these gaps. Corrective zinc applications deliver 200-400 kg per-hectare wheat gains and 300-600 kg rice gains, prompting district authorities to intensify extension outreach. Mandatory micronutrient labeling under the Fertilizer Control Order (FCO) and expanded lab testing capacity serve as a backstop for quality assurance, making the driver structurally positive for the India micronutrient fertilizers market.

Government Subsidy Extension for Fortified NPK Blends (NBS-2)

Beginning December 2024, micronutrient-fortified DAP and NPK grades will qualify for direct farm-gate support, reducing retail prices by 40-50% and increasing adoption in Maharashtra, Karnataka, Andhra Pradesh, and Tamil Nadu from 15% in 2022 to 28% in 2024 . The budgetary outlay under the NBS window increased from INR 795 billion (USD 9.62 billion) in 2023-24 to INR 875 billion (USD 10.5 billion) in 2024-25, encouraging manufacturers such as IFFCO and Coromandel to expand their blending capacity by 35%. Digital tracking through Primary Agricultural Credit Societies reduces the risk of diversion, and the mandatory Fertilizer Control Order (FCO) specifications ensure that every bag sold contains functional levels of zinc, boron, or iron. The subsidy is front-loaded, so the bulk of market lift is projected within the next two seasons, though balanced nutrition awareness will persist beyond the payout period.

Counterfeit and Spurious Product Circulation in Tier-2/3 Agri-Inputs Markets

Subpar powders masquerading as micronutrient blends account for 15-20% of the supply in Bihar, Uttar Pradesh, and Odisha, where small dealers dominate input retail. Lab tests reveal that metal contents are 30-50% below the labels, causing crop failures that discourage legitimate purchases. Limited inspectorates and a lack of accredited laboratories hinder enforcement under the Fertilizer Control Order. Large producers have added QR code verification, and the smartphone penetration gaps and poor digital literacy are slowing down take-up. Until authentication scales and dealer audits tighten, counterfeit leakage will shave 1.2 percentage points off the India micronutrient fertilizers market CAGR in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Specialty Chelated Formulations by Horticulture Clusters

- Emerging Nano-Micronutrient Products from Ag-Tech Startups

- Logistics Bottlenecks for Bulk Micronutrient Movement to Land-Locked Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc formulations accounted for 35.9% of the India micronutrient fertilizers market share in 2025, highlighting their critical role in addressing one of the country's most prevalent soil nutrient deficiencies. Demand remains particularly strong in the cultivation of rice, wheat, and maize, where zinc application is directly associated with improved yields and enhanced nutrient-use efficiency. The segment's position has been further reinforced by the expansion of soil-testing initiatives and balanced fertilization programs.

The market is gradually shifting toward boron-based products, which are projected to register a CAGR of 10.6% during 2026-2031. The increasing cultivation of fruits, vegetables, oilseeds, and plantation crops is driving demand for boron, which plays a vital role in flowering, pollination, fruit set, and crop development. Additionally, the growing adoption of specialty micronutrient blends and fertigation-compatible formulations is creating new growth opportunities beyond traditional zinc products. Fertilizers containing iron, copper, manganese, and molybdenum continue to play an important supporting role in addressing crop- and region-specific nutrient deficiencies across India's diverse agricultural systems.

Complete Report Scope:

- Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

List of Companies Covered in this Report:

- Coromandel International Limited

- Chambal Fertilizers and Chemicals Limited

- Indian Farmers Fertiliser Cooperative Limited

- Deepak Fertilizers and Petrochemicals Corporation Limited

- Zuari Agro Chemicals Limited

- Rashtriya Chemicals and Fertilizers Limited

- Aries Agro Limited

- Tata Chemicals Limited

- Mangalore Chemicals and Fertilizers Limited

- Nagarjuna Fertilizers and Chemicals Limited

- BASF India Limited

- Compo Expert India Private Limited

- Haifa Chemicals Ltd

- Yara Fertilisers India Private Limited

- Sociedad Quimica y Minera de Chile S.A. (SQM) India Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 EXECUTIVE SUMMARY & KEY FINDINGS

3 REPORT OFFERS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Rising Soil Micronutrient Depletion Across Intensively Farmed Districts

- 4.6.2 Government Subsidy Extension for Fortified NPK Blends (NBS-2)

- 4.6.3 Rapid Adoption of Specialty Chelated Formulations by Horticulture Clusters

- 4.6.4 Expansion of Fertigation Infrastructure under Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) Micro-Irrigation Scheme

- 4.6.5 Emerging Nano-Micronutrient Products from Indian Ag-Tech Start-Ups

- 4.6.6 Carbon-Credit Premium for Micronutrient-Driven Yield Boosts

- 4.7 Market Restraints

- 4.7.1 Counterfeit and Spurious Product Circulation in Tier-2/3 Agri-Inputs Markets

- 4.7.2 Volatility in Mined Zinc and Boron Concentrate Prices

- 4.7.3 Limited Farmer Awareness in Eastern and North-Eastern States

- 4.7.4 Logistics Bottlenecks for Bulk Micronutrient Movement to Land-Locked Regions

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Coromandel International Limited

- 6.4.2 Chambal Fertilizers and Chemicals Limited

- 6.4.3 Indian Farmers Fertiliser Cooperative Limited

- 6.4.4 Deepak Fertilizers and Petrochemicals Corporation Limited

- 6.4.5 Zuari Agro Chemicals Limited

- 6.4.6 Rashtriya Chemicals and Fertilizers Limited

- 6.4.7 Aries Agro Limited

- 6.4.8 Tata Chemicals Limited

- 6.4.9 Mangalore Chemicals and Fertilizers Limited

- 6.4.10 Nagarjuna Fertilizers and Chemicals Limited

- 6.4.11 BASF India Limited

- 6.4.12 Compo Expert India Private Limited

- 6.4.13 Haifa Chemicals Ltd

- 6.4.14 Yara Fertilisers India Private Limited

- 6.4.15 Sociedad Quimica y Minera de Chile S.A. (SQM) India Private Limited

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲微量元素肥料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)美國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)歐洲微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)中國微量元素肥料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)微量元素肥料:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球微量元素肥料市場報告

2026年全球微量元素肥料市場報告 微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)

微量元素肥料市場報告:趨勢、預測與競爭分析(至2031年)