|

市場調查報告書

商品編碼

2073297

日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Japan Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

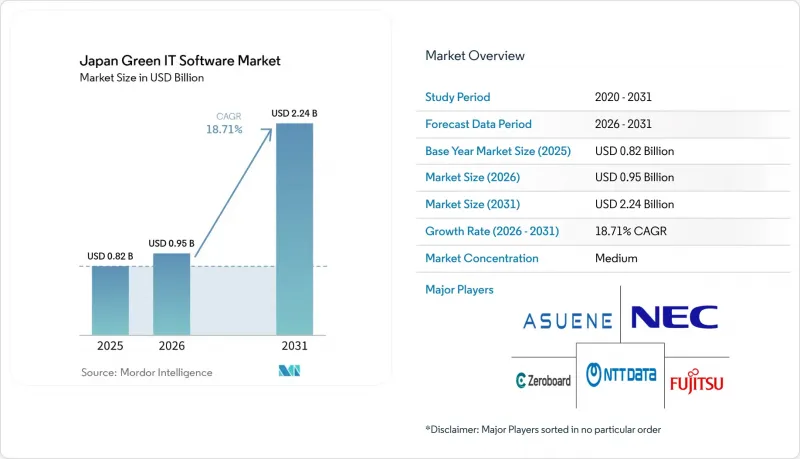

據 Mordor Intelligence 稱,2025 年日本綠色 IT 軟體市場價值 8.2 億美元,預計到 2031 年將達到 22.4 億美元,2026 年至 2031 年的複合年成長率為 18.71%。

本報告按交付方式(軟體和服務)、部署方式(雲端、本地部署、混合部署)、解決方案類型(碳管理和運算軟體等)、企業規模(大型企業和中小企業)以及最終用戶產業(資訊科技和電信、製造業等)進行細分。市場預測以美元計價。

日本綠色IT軟體市場的趨勢與洞察

更嚴格的Gx資訊揭露和審計要求

在資訊揭露和審計要求日益提高的推動下,合規主導的採購模式在日本綠色IT軟體市場,尤其是在大規模上市公司和主要工業集團中,正變得越來越突出。買家不再僅僅追求儀錶板和排放視覺化功能,而是尋求能夠支援跨多個報告週期的可複現文件、內部控制和第三方審核的系統。這促使企業選擇能夠維護營運、財務和供應鏈部門之間一致排放記錄的平台。這種壓力也有利於那些能夠透過將碳數據與更廣泛的永續發展工作流程整合來減輕重複報告負擔的供應商。因此,除了基本的報告功能外,產品在審計追蹤、記錄可追溯性和檢驗支援等領域的功能深度也變得越來越重要。

資料中心提高能源效率的壓力越來越大

資料中心對能源效率的需求,正在日本綠色IT軟體市場催生一個新興且密切相關的成長領域。這源自於營運商對能源績效和使用日益嚴格的審查。隨著人工智慧相關運算需求的不斷成長,能源可視性、工作負載規劃和報告對於成本管理和企業脫碳工作變得愈發重要,這一問題的影響範圍已超越了設施管理。因此,市場對軟體的需求正在轉向能夠將能源數據、使用趨勢和碳排放整合到單一營運視圖中的工具。 NTT於2026年3月正式確立了涵蓋整個軟體生命週期的二氧化碳計算規則,進一步將討論範圍從硬體效率擴展到軟體開發和使用本身的碳排放特徵。此舉進一步擴大了能夠衡量整個IT環境中內建軟體的營運能源績效和相關排放的數位工具的市場作用。

整合舊有系統的複雜性

在日本綠色IT軟體市場,整合舊有系統仍是最主要的限制因素之一。這是因為許多公司仍在運作過時的ERP、生產和設施管理系統,這些系統並非基於開放且持續的資料交換理念建構。在以製造業為中心的環境中,這個問題尤其突出,因為排放資訊通常分散在多個彼此獨立的地點,例如材料清單、生產記錄、公用設施文件和現場系統。這導致實施延遲、定製成本更高,以及在選擇供應商時面臨更大的實施風險。 NTT Data Kansai發布的「BIZXIM CFP」透過專注於從生產管理數據中直接提取碳足跡來應對這一挑戰,這表明工業領域仍需要進行大量的調整。因此,擁有更強大的連接器庫和更卓越的實施經驗的供應商更有可能縮短銷售週期,並降低依賴傳統作業系統的客戶的早期解約率。

細分市場分析

2025年,日本綠色IT軟體市場中,軟體佔比高達68.41%。這反映出企業用戶對自主可審計的數位化工作流程的明顯偏好。這一趨勢與市場現狀相符,即企業希望直接管理排放記錄、報告流程和合規文檔,而非僅依賴託管支援。這也有利於那些能夠在客戶環境中維護配置、工作流程管理和資料所有權的供應商。同時,服務業預計將在2026年至2031年間以23.22%的複合年成長率成長,表明隨著部署從試點階段過渡到全面運營,實施、保障準備和持續支持的重要性日益凸顯。因此,這種市場構成比表明,儘管軟體仍然是採購的核心,但隨著企業尋求以一致且檢驗的方式利用這些平台,服務的重要性也日益凸顯。

服務領域的商機取決於軟體採購後的實際工作—供應商入駐、協調內部團隊、建立文件以及支援迭代報告週期中的審核流程。這意味著需求不再局限於安裝協助,而是擴大包括幫助企業將資料收集轉化為資訊披露和可審計記錄的準備工作。能夠將軟體訂閱與結構化保障支援結合的供應商,更有能力保障收入,並防止客戶將工作流程過度分散到多個合作夥伴。 Zeroboard 為應對更嚴格的揭露要求而推出的保障支援包,顯示供應商的角色已超越了單純的軟體提供。此支援包支援一種雙層結構:軟體是記錄系統的層級構造,而服務則幫助客戶維護使用、通過檢驗並隨著時間的推移擴展平台的功能。

預計到2025年,雲端平台將佔日本綠色IT軟體市場63.41%的佔有率,並將以19.96%的複合年成長率持續成長至2031年。這確立了雲端作為規模最大、成長最快的部署模式的地位。這種雙重作用反映了大規模組織需要跨分散式設施、多個業務部門和整個供應商網路進行集中存取的現實。這也體現了雲端對於那些無法承擔碳會計和永續發展報告專用基礎設施部署成本的中小型企業而言,在成本和易用性方面的優勢。雖然對於管理要求更為嚴格的組織而言,本地部署系統仍然至關重要,但混合模式作為適用於高度敏感用例的中間選擇,正日益受到關注。因此,市場的發展方向並非單一的統一架構,而是致力於在規模、速度和管治之間取得平衡的部署方案。

此外,一些成功的企業案例也表明,大型、地域分散的用戶可以透過標準化跨多個地點的資料擷取來推動雲端技術的普及。例如,Asuene 在 SMBC 集團 3000 多個分行實施的措施(例如利用 AI 驅動的 OCR 技術從水電費帳單中資料提取)就體現了雲端模式如何減輕複雜營運環境中的報告負擔。然而,最大的區別在於,雲端模式正逐漸從簡單的託管模式轉向能夠在高度監管的環境中維護審計完整性和資料管理。因此,隨著銀行、政府和醫療保健等行業的越來越多的買家尋求在不犧牲對高度敏感的身份資訊和記錄的嚴格控制的前提下利用雲端的效率,混合部署正變得具有重要的戰略意義。從這個意義上講,日本綠色 IT 軟體市場的發展重點正逐漸從純粹的雲端遷移轉向用於可重複合規操作的可靠架構設計。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人們對GX的資訊揭露和審計的期望日益成長。

- 資料中心提高能源效率的壓力越來越大

- 向基於雲端的永續發展工作流程過渡

- 主要客戶對範圍 3 資料的請求

- 人工智慧驅動的碳排放和能源分析自動化

- 軟體整合以減少IT浪費和授權集群

- 市場限制因素

- 整合舊有系統的複雜性

- 網路安全與資料管治問題

- 資訊科技專業人員短缺,尤其關注永續性。

- 中小企業在地化和稽核準備方面面臨的挑戰

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 基於雲端的

- 現場

- 混合

- 按解決方案類型

- 碳管理和運算軟體

- ESG報告和合規軟體

- 永續性資料管理平台

- 脫碳規劃軟體

- 能源和資源最佳化軟體

- 按公司規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- IT/通訊

- 製造業

- 銀行、金融服務和保險(BFSI)

- 政府/公共部門

- 能源公用事業

- 衛生保健

- 零售與電子商務

- 建築和基礎設施

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Asuene Inc.

- Zeroboard Inc.

- Fujitsu Limited

- NEC Corporation

- NTT DATA Corporation

- Hitachi, Ltd.

- Ricoh Company, Ltd.

- Panasonic Holdings Corporation

- Toshiba Digital Solutions Corporation

- IBM Japan, Ltd.

- SAP Japan Co., Ltd.

- Microsoft Japan Co., Ltd.

- Oracle Corporation Japan

- Salesforce Japan KK

- Schneider Electric Japan Holdings Ltd.

- Honeywell Japan Ltd.

- Accenture Japan Ltd.

- Nomura Research Institute, Ltd.

- Mizuho Research and Technologies, Ltd.

- Persol Process and Technology Co., Ltd.

第7章 市場機會與未來展望

- 評估未開發的領域和未滿足的需求

According to Mordor Intelligence, the japan green IT software market size was valued at USD 0.82 billion in 2025 and is projected to reach USD 2.24 billion by 2031, growing at a CAGR of 18.71% from 2026 to 2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Solution Type (Carbon Management and Accounting Software, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Information Technology and Telecommunications, Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

Japan Green IT Software Market Trends and Insights

Tighter Gx Disclosure and Audit Expectations

Tighter disclosure and audit expectations are giving the Japan green IT software market a more compliance-led buying pattern, especially among larger listed companies and major industrial groups. Buyers are no longer looking only for dashboards or emissions visibility, they are looking for systems that can support repeatable documentation, internal controls, and third-party review across multiple reporting cycles. This is pushing software selection toward platforms that can keep one consistent emissions record across operating teams, finance teams, and supply chain functions. The pressure also favors vendors that can reduce the burden of duplicate reporting by linking carbon data with broader sustainability workflows. As a result, product depth in audit trails, record traceability, and verification support is becoming more important than basic reporting features alone.

Rising Data Center Power Efficiency Pressure

Power efficiency pressure in data centers is creating a separate but closely linked growth lane for the Japan green IT software market as operators face greater scrutiny on energy performance and utilization. The issue is widening beyond facility management because higher AI-related compute demand is making energy visibility, workload planning, and reporting more material to cost control and corporate decarbonization efforts. Software demand is therefore shifting toward tools that can connect energy data, utilization trends, and carbon outcomes in one operating view. NTT's March 2026 formalization of CO2 calculation rules for the full software lifecycle also broadened the discussion from hardware efficiency toward the carbon profile of software development and use itself. That development supports a wider market role for digital tools that can measure both operating energy performance and embedded software-related emissions across IT environments.

Legacy System Integration Complexity

Legacy system integration remains one of the clearest restraints on the Japan green IT software market because many enterprises still operate older ERP, production, and facility systems that were not built for open and continuous data exchange. The problem is most visible in manufacturing-heavy environments where emissions information often sits across part tables, production records, utility documents, and site-level systems that do not naturally connect. This slows deployment, raises customization costs, and makes implementation risk a bigger factor in vendor selection. NTT DATA Kansai's BIZXIM CFP launch reflected this challenge by focusing on direct carbon footprint extraction from production management data, which shows how much adaptation is still required in industrial settings. Vendors with stronger connector libraries and better implementation depth are therefore more likely to shorten sales cycles and reduce early churn in accounts that depend on older operational systems.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Cloud-Based Sustainability Workflows

- Scope 3 Data Demands From Large Customers

- Cybersecurity and Data Governance Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software represented 68.41% of the Japan green IT software market in 2025, which reflected a clear preference for owned and auditable digital workflows across corporate users. That preference fits a market where companies want direct control over emissions records, reporting steps, and compliance documentation rather than relying only on managed support. It also favors vendors that can keep configuration, workflow management, and data ownership inside the customer environment. Services, however, are projected to grow at 23.22% CAGR from 2026 to 2031, which shows that implementation, assurance preparation, and ongoing support are becoming more material as deployments move from pilot stage to operating scale. The mix therefore points to a market where software remains the core purchase, while services become more important as enterprises try to use those platforms in a consistent and verified way.

The services opportunity is being shaped by the practical work that follows software procurement, including onboarding suppliers, aligning internal teams, preparing documentation, and supporting review processes across repeated reporting cycles. This means demand is no longer limited to installation support, it increasingly includes readiness work that helps companies turn data collection into disclosures and auditable records. Vendors that can combine software subscriptions with structured assurance support are better placed to defend revenue and keep customers from fragmenting their workflow across too many partners. Zeroboard's assurance support package, launched for companies preparing for stricter disclosure requirements, illustrates how vendors are trying to widen their role beyond software alone. That supports a two-layer structure in which software anchors the system of record, while services help customers sustain usage, pass verification, and expand platform scope over time.

Cloud-based platforms held 63.41% of the Japan green IT software market size in 2025 and are also projected to grow at a 19.96% CAGR through 2031, which gives cloud a rare position as both the largest and fastest-growing deployment model. This dual role reflects the practical reality that large organizations need centralized access across dispersed facilities, multiple business units, and supplier networks. It also reflects a cost and usability advantage for smaller firms that cannot justify dedicated infrastructure for carbon accounting and sustainability reporting. On-premise systems still hold relevance in organizations with stricter control requirements, while hybrid models are gaining traction as a middle path for more sensitive use cases. The market is therefore not moving toward one rigid architecture, but toward deployment choices that balance scale, speed, and governance.

Cloud adoption is also being reinforced by visible enterprise examples that show how large and geographically dispersed users can standardize data intake across many sites. Asuene's work with SMBC Group across more than 3,000 locations, including the use of AI-driven OCR for utility invoice data extraction, is one example of how cloud-based models can reduce reporting friction in complex operating environments. Even so, the strongest differentiation is beginning to shift from hosting model alone toward the ability to preserve audit integrity and data control in more regulated environments. That is why hybrid deployment is becoming strategically important in banking, government, and healthcare, where buyers want cloud efficiency without giving up tight control over sensitive identifiers and records. In that sense, the deployment story in the Japan green IT software market is becoming less about pure cloud migration and more about trusted architecture design for repeatable compliance work.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-Use Industry

- IT and Telecommunications

- Manufacturing

- Banking, Financial Services, and Insurance (BFSI)

- Government and Public Sector

- Energy and Utilities

- Healthcare

- Retail and E-Commerce

- Construction and Infrastructure

- Other End User Industries

List of Companies Covered in this Report:

- Asuene Inc.

- Zeroboard Inc.

- Fujitsu Limited

- NEC Corporation

- NTT DATA Corporation

- Hitachi, Ltd.

- Ricoh Company, Ltd.

- Panasonic Holdings Corporation

- Toshiba Digital Solutions Corporation

- IBM Japan, Ltd.

- SAP Japan Co., Ltd.

- Microsoft Japan Co., Ltd.

- Oracle Corporation Japan

- Salesforce Japan K.K.

- Schneider Electric Japan Holdings Ltd.

- Honeywell Japan Ltd.

- Accenture Japan Ltd.

- Nomura Research Institute, Ltd.

- Mizuho Research and Technologies, Ltd.

- Persol Process and Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tighter GX Disclosure and Audit Expectations

- 4.2.2 Rising Data Center Power Efficiency Pressure

- 4.2.3 Shift Toward Cloud-Based Sustainability Workflows

- 4.2.4 Scope 3 Data Demands From Large Customers

- 4.2.5 AI-Enabled Automation for Carbon and Energy Analytics

- 4.2.6 Software Consolidation to Reduce IT Waste and License Sprawl

- 4.3 Market Restraints

- 4.3.1 Legacy System Integration Complexity

- 4.3.2 Cybersecurity and Data Governance Concerns

- 4.3.3 Shortage of Sustainability-Focused IT Talent

- 4.3.4 Localization and Audit-Readiness Gaps for Smaller Firms

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power Of Buyers

- 4.8.2 Bargaining Power Of Suppliers

- 4.8.3 Threat Of New Entrants

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Solution Type

- 5.3.1 Carbon Management and Accounting Software

- 5.3.2 ESG Reporting and Compliance Software

- 5.3.3 Sustainability Data Management Platforms

- 5.3.4 Decarbonization Planning Software

- 5.3.5 Energy and Resource Optimization Software

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-Use Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 Manufacturing

- 5.5.3 Banking, Financial Services, and Insurance (BFSI)

- 5.5.4 Government and Public Sector

- 5.5.5 Energy and Utilities

- 5.5.6 Healthcare

- 5.5.7 Retail and E-Commerce

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Asuene Inc.

- 6.4.2 Zeroboard Inc.

- 6.4.3 Fujitsu Limited

- 6.4.4 NEC Corporation

- 6.4.5 NTT DATA Corporation

- 6.4.6 Hitachi, Ltd.

- 6.4.7 Ricoh Company, Ltd.

- 6.4.8 Panasonic Holdings Corporation

- 6.4.9 Toshiba Digital Solutions Corporation

- 6.4.10 IBM Japan, Ltd.

- 6.4.11 SAP Japan Co., Ltd.

- 6.4.12 Microsoft Japan Co., Ltd.

- 6.4.13 Oracle Corporation Japan

- 6.4.14 Salesforce Japan K.K.

- 6.4.15 Schneider Electric Japan Holdings Ltd.

- 6.4.16 Honeywell Japan Ltd.

- 6.4.17 Accenture Japan Ltd.

- 6.4.18 Nomura Research Institute, Ltd.

- 6.4.19 Mizuho Research and Technologies, Ltd.

- 6.4.20 Persol Process and Technology Co., Ltd.

7 MARKET OPPORTUNITIES ANDFUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年) 2026年全球數位測量和圖解決方案市場報告

2026年全球數位測量和圖解決方案市場報告 2026-2030年全球數位化製造軟體市場

2026-2030年全球數位化製造軟體市場