|

市場調查報告書

商品編碼

2073271

美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)United States Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

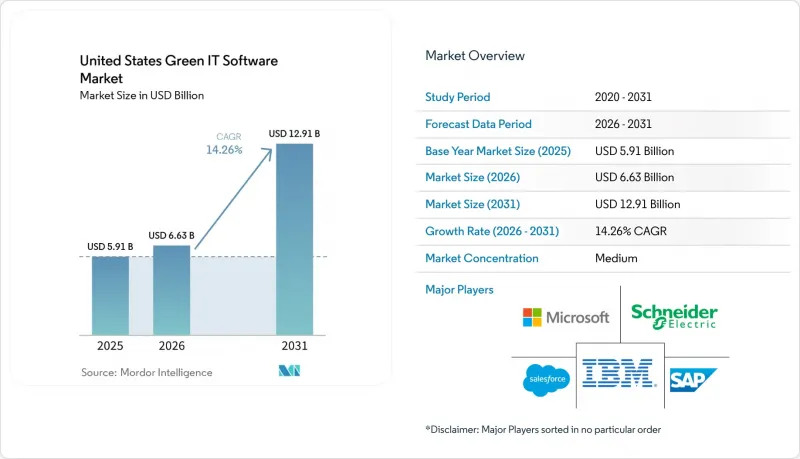

根據 Mordor Intelligence 預測,美國綠色 IT 軟體市場預計將從 2025 年的 59.1 億美元成長到 2026 年的 66.3 億美元,到 2031 年達到 129.1 億美元,2026 年至 2031 年的複合年預計成長率為 14.26%。

本報告按交付方式(軟體和服務)、部署方式(雲端等)、解決方案類型(碳管理和運算軟體等)、組織規模(大型企業和中小企業)以及最終用戶產業(資訊科技和電信、製造業等)進行分類。市場預測以美元計價。

美國綠色IT軟體市場的趨勢與洞察

從範圍 1 到範圍 3 的報告自動化面臨監管壓力

在美國綠色IT軟體市場,加州是企業採購最明顯的短期促進因素。這是因為加州空氣資源委員會(CARB)於2026年2月26日通過了SB 253法案的首個實施細則,將2026年8月10日設定為符合條件的加州企業提交範圍1和範圍2排放的首個截止日期。該法案的適用範圍不僅限於總部位於加州的企業。由於收入標準適用於在加州營運的企業,因此目標買家群體廣泛,不受行業或地理的限制。隨著範圍3義務於2027年生效,許多買家選擇在2026年採取行動,因為建構和測試供應商資料系統、控制結構和內部審查流程以達到審計就緒標準需要時間。這種時間安排推動了對能夠在單一受控環境中管理排放清單、供應商提交資料、證據追蹤和符合框架要求的輸出的軟體的需求。儘管美國證券交易委員會(SEC)提案在2026年5月廢除氣候相關資訊揭露規則,但大型企業仍迫切需要可重複使用的報告系統,因為它們仍然面臨來自投資者、貸款人、客戶和董事會的揭露要求。因此,那些能夠使工作流程與公認的排放計算方法和檢驗要求一致的供應商正在獲得市場認可,因為買家正在尋找能夠在強制性和自願性報告場景下都能繼續使用的工具。

變革企業人工智慧,實現永續智慧的持續應用

人工智慧正在推動美國綠色IT軟體市場的轉型,使其從簡單的數據收集轉向能夠持續監控、解讀和組織永續發展資訊的軟體。 2025年6月, 銷售團隊發布了淨零雲平台的Agentforce,該軟體配備了一個人工智慧代理,能夠撰寫揭露內容、監控範圍1、範圍2和範圍3的清單,並在報告週期內(而非之後)識別問題。 2026年5月,SAP宣布其永續發展人工智慧代理商將於2026年底正式發布,旨在協助解決平均排放因子波動的問題,同時探索脫碳方案。這改變了買家的預期。永續發展團隊不再只是需要儲存歷史資料的軟體;他們需要能夠識別資料缺口、比較不同方案、縮短報告週期並支援全年內部決策的系統。能夠將人工智慧功能與管治管理、可追溯性以及與財務和營運系統的整合相結合的供應商正在獲得競爭優勢。這些功能在不影響審計嚴謹性的前提下,減輕了人工工作的負擔。

與傳統ERP和設施管理系統整合的複雜性。

在美國綠色IT軟體市場,整合仍然是最大的營運障礙。這是因為核心永續性數據仍儲存在過時的ERP、採購、設施和建築管理系統中,這些系統在設計之初並未考慮排放報告功能。許多買家需要連接多個交易系統才能計算出可操作的碳排放或創建可揭露的記錄,而這項工作會延長部署時間並增加整體成本。 2024年9月, Oracle在其現有的Fusion Cloud Applications Suite中發布了Oracle Fusion Cloud Sustainability,透過將資料收集和報告功能整合到已儲存企業交易資料的軟體環境中,直接應對了這項挑戰。 IBM的Envizi Supply Chain Intelligence也旨在透過將ERP交易資料整合到Scope 3運算中,並在有更準確的來源資料時優先使用供應商特定資料而非總體平均值來解決這個問題。儘管有這些改進,但資料品質和系統相容性仍然因實施環境而異,因此,整合工作的負擔仍然是部署速度的主要瓶頸。由於實施公司希望縮短引進週期並減少與外部資料的交互,因此此限制為管理 ERP 層或擁有強大的現成連接器的供應商帶來了持久的優勢。

細分市場分析

預計到2031年,服務業將以19.26%的複合年成長率成長,成為美國綠色IT軟體市場中成長最快的細分領域。這一成長反映出,隨著資訊揭露義務日益細化,對實施支援、資料架構建置、報告設計和變更管理的需求不斷成長。許多大型採購公司在軟體大規模部署之前,仍需要外部協助,將排放流程與ERP、採購和設施資料整合。由於供應商資料項目、品質保證準備和內部管治流程在初始部署後通常需要持續支持,因此服務業的重要性仍然很高。同時,預計到2025年,軟體收入將佔總收入的46.41%,這表明授權平台仍然是企業管理永續發展數據和報告項目的基礎。

軟體仍然是部署基礎的核心,因為控制層、工作流程邏輯和證據管理都內建在產品中,而非作為諮詢服務提供。 2025年9月,Workiva發布了智慧財務、GRC和永續發展解決方案,這些方案均採用人工智慧驅動的自動化技術,用於建立揭露文件、進行基準測試、評估重要性、進行同儕比較以及建立合規工作流程。這表明,即使對服務的需求依然強勁,供應商仍在不斷提升軟體的價值。隨著自動化技術的進步,服務支出可能會從重複性任務轉向更高附加價值的領域,例如管治治理結構、制定脫碳計畫以及準備應對審計。這一趨勢有助於解釋為何服務業務快速成長,而軟體仍是主要的收入來源。因此,美國綠色IT軟體產業正在從純粹的授權模式轉變為軟體與交付相結合的模式。

預計到2025年,基於雲端的採用將占美國綠色IT軟體市場營收的63.94%,並在2031年之前以16.12%的複合年成長率成長,使其成為美國綠色IT軟體市場規模最大、成長最快的採用模式。這種雙重地位表明,買家的偏好正趨向於雲端原生永續架構,而不是經歷初始遷移階段。大型企業需要跨業務部門、區域和報告框架的持續同步,而雲端環境比孤立的本地系統更容易實現這一點。雲端採用還支援人工智慧驅動的永續功能所需的「始終運作」資料饋送,以便檢測異常、分析場景並進行週期性審查。因此,雲端採用現在與工作流程設計、系統互通性以及託管選擇緊密相關。

IBM 於 2026 年 1 月發布的 Envizi 排放運算 Excel 插件,展示如何將基於雲端的永續發展工具整合到現有使用者工作流程中,而無需使用者遷移到不同的作業系統環境。 2026 年 2 月,IBM 也在 Envizi 永續發展報告管理器中發布了 ESRS Omnibus 框架配置,體現了可更新以跟上不斷發展標準的託管雲端框架的優勢。在資料居住和基礎設施控制仍然至關重要的嚴格監管環境中,本地部署仍然發揮著重要作用。當企業希望採用雲端分析但需要對特定的員工、財務或營運資料集進行更嚴格的控制時,混合模式也同樣適用。例如,在規模方面,基於雲端的部署預計將在 2025 年佔據美國綠色 IT 軟體市場規模的 63.94%,這證實了可擴展的託管模型在部署方面已經佔據主導。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 監管機構施壓要求實現從範圍 1 到範圍 3 的報告自動化

- 在資料中心工作負載中實施雲端原生碳排放和能源最佳化

- 變革企業人工智慧,實現持續永續發展智慧

- 將軟體選擇與檢驗的ESG資料連結起來的採購要求。

- 公用事業價格的波動增加了人們對最佳化消費的需求。

- 上市公司和非上市公司在不同報告架構下的報告負擔分配。

- 市場限制因素

- 與傳統ERP和設施管理系統整合的複雜性。

- 供應商提供的資料品質差,導致範圍 3 自動化流程放緩。

- 對ESG資料平台網路安全和資料儲存位置的擔憂

- 儘管需要遵守相關規定,但中型企業在採購決策中表現出對預算的敏感度。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 基於雲端的

- 現場

- 混合

- 按解決方案類型

- 碳管理和運算軟體

- ESG報告和合規軟體

- 永續性資料管理平台

- 脫碳規劃軟體

- 能源和資源最佳化軟體

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- 製造業

- 銀行、金融服務和保險(BFSI)

- 政府/公共部門

- 能源公用事業

- 醫療保健和生命科學

- 零售與電子商務

- 建築和基礎設施

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Salesforce, Inc.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Schneider Electric SE

- Oracle Corporation

- Workiva Inc.

- Diligent Corp.

- Wolters Kluwer NV

- Persefoni AI, Inc.

- Watershed Technologies, Inc.

- EcoVadis SAS

- Intelex Technologies ULC

- Sphera Solutions, Inc.

- Benchmark Gensuite LLC

- FigBytes Inc.

- Measurabl, Inc.

- Cority Software Inc.

- Dakota Software Corporation

- EnergyCAP, LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states green IT software market size is expected to increase from USD 5.91 billion in 2025 to USD 6.63 billion in 2026 and reach USD 12.91 billion by 2031, growing at a CAGR of 14.26% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, and More), Solution Type (Carbon Management and Accounting Software, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Information Technology and Telecommunications, Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Green IT Software Market Trends and Insights

Regulatory Pressure for Scope 1 To Scope 3 Reporting Automation

California has become the clearest near-term trigger for enterprise buying in the United States green IT software market because CARB adopted initial implementing regulations for SB 253 on February 26, 2026, and set August 10, 2026 as the first disclosure deadline for Scope 1 and Scope 2 emissions for covered companies doing business in the state. The law reaches beyond companies headquartered in California because the revenue threshold applies to firms that do business in the state, which widens the addressable buyer base across sectors and operating regions. Scope 3 obligations will activate from 2027, so many buyers are acting in 2026 because supplier data systems, controls, and internal review processes take time to build and test at audit-ready quality. This timing is lifting demand for software that can manage emissions inventories, supplier submissions, evidence trails, and framework-ready outputs in one controlled environment. The SEC's proposal to rescind its climate-related disclosure rules in May 2026 has not removed the underlying need for repeatable reporting systems among large enterprises that still face disclosure expectations from investors, lenders, customers, and boards. Vendors that align workflows with accepted emissions accounting practices and verification requirements are therefore gaining ground because buyers want tools that remain usable across both mandatory and voluntary reporting settings.

Enterprise AI Shift Toward Continuous Sustainability Intelligence

AI is shifting the value of the United States green IT software market from simple data collection toward software that can monitor, interpret, and organize sustainability information on a continuous basis. Salesforce launched Agentforce for Net Zero Cloud in June 2025 with AI agents that can draft disclosure content, monitor Scope 1, Scope 2, and Scope 3 inventories, and surface issues during the reporting cycle rather than after it closes. SAP stated in May 2026 that its sustainability AI agents will reach general availability by the end of 2026 and will support side-by-side decarbonization scenario work while addressing the variability found in average emissions factors. This changes buyer expectations because sustainability teams no longer want software that only stores past-period data. They want systems that can flag data gaps, compare scenarios, compress reporting timelines, and support internal decision-making during the year. The advantage is moving toward vendors that can combine AI functions with governance controls, traceability, and integration into finance and operating systems, because those features reduce manual effort without weakening audit discipline.

High Integration Complexity With Legacy ERP and Facility Systems

Integration remains the clearest operational barrier in the United States green IT software market because core sustainability data still originates inside older ERP, procurement, facility, and building systems that were not designed for emissions reporting. Many buyers must connect several transactional systems before they can produce usable carbon calculations or disclosure-ready records, and that work can stretch implementations and raise total cost. Oracle launched Oracle Fusion Cloud Sustainability in September 2024 inside its existing Fusion Cloud Applications Suite, which directly addresses this issue by embedding data capture and reporting functions within software environments that already hold enterprise transactions. IBM's Envizi Supply Chain Intelligence also targets this problem by connecting ERP transactions to Scope 3 calculations and by prioritizing supplier-specific data over broad averages where better source data exists. Even with these improvements, data quality and system compatibility still vary widely across buyer environments, which means integration effort remains a real brake on adoption speed. This restraint gives a durable advantage to vendors that control the ERP layer or have strong pre-built connectors, because buyers want shorter implementation cycles and fewer external data handoffs.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Native Carbon and Energy Optimization Adoption in Data Center Workloads

- Procurement Requirements Linking Software Selection to Verified ESG Data

- Weak Supplier Data Quality Slowing Scope 3 Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are projected to grow at a 19.26% CAGR through 2031, which makes them the fastest-expanding part of this segmentation in the United States green IT software market. That growth reflects the need for implementation support, data architecture work, reporting design, and change management as disclosure obligations become more detailed. Many large buyers still need outside help to connect emissions workflows with ERP, procurement, and facility data before the software can operate at scale. Services also remain relevant because supplier-data programs, assurance preparation, and internal governance processes often require sustained support after initial implementation. At the same time, software held 46.41% of revenue in 2025, which shows that licensed platforms still anchor how enterprises govern sustainability data and reporting programs.

Software remains the installed-base core because the control layer, workflow logic, and evidence management all sit inside the product rather than inside a consulting engagement. Workiva introduced Intelligent Finance, GRC, and Sustainability in September 2025 with AI-enabled automation for disclosure drafting, benchmarking, materiality work, peer comparison, and compliance workflows, which shows how vendors are expanding software value even as services demand stays strong. As automation improves, service spend is likely to shift away from repetitive assembly work and toward higher-value areas such as governance setup, decarbonization planning, and assurance readiness. That pattern helps explain why services are growing quickly without displacing software as the larger revenue base. The United States green IT software industry is therefore evolving toward combined software and delivery models rather than a pure license-only structure.

Cloud-based deployment accounted for 63.94% of revenue in 2025 and is projected to grow at a 16.12% CAGR through 2031, which leaves it as both the largest and fastest-growing deployment model in the United States green IT software market. This dual position shows that buyer preference is consolidating around cloud-native sustainability architecture rather than moving through an early transition stage. Large enterprises need continuous synchronization across business units, geographies, and reporting frameworks, and cloud environments make that easier than isolated on-premise systems. Cloud deployment also supports the always-on data feeds that AI-enabled sustainability functions require for anomaly detection, scenario work, and in-cycle review. For that reason, cloud adoption is now tied as much to workflow design and system interoperability as it is to hosting choice.

IBM's January 2026 Excel add-in for Envizi Emissions Calculations shows how cloud-based sustainability tools can be inserted into established user workflows instead of forcing users into a separate operating environment. IBM also released ESRS Omnibus framework configurations in February 2026 inside Envizi Sustainability Reporting Manager, which reflects the advantage of managed cloud frameworks that can be updated as standards evolve. On-premise deployment still has a role in more regulated settings where data residency and infrastructure control remain important. Hybrid models are also relevant where companies want cloud analytics but need tighter control over selected employee, financial, or operational datasets. One sentence with direct scale relevance is that cloud-based deployment held 63.94% of the United States green IT software market size in 2025, which confirms that deployment leadership already sits with scalable hosted models.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- IT and Telecommunications

- Manufacturing

- Banking, Financial Services, and Insurance (BFSI)

- Government and Public Sector

- Energy and Utilities

- Healthcare and Life Sciences

- Retail and E-Commerce

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- Salesforce, Inc.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Schneider Electric SE

- Oracle Corporation

- Workiva Inc.

- Diligent Corp.

- Wolters Kluwer N.V.

- Persefoni AI, Inc.

- Watershed Technologies, Inc.

- EcoVadis SAS

- Intelex Technologies ULC

- Sphera Solutions, Inc.

- Benchmark Gensuite LLC

- FigBytes Inc.

- Measurabl, Inc.

- Cority Software Inc.

- Dakota Software Corporation

- EnergyCAP, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Pressure for Scope 1 to Scope 3 Reporting Automation

- 4.2.2 Cloud Native Carbon and Energy Optimization Adoption in Data Center Workloads

- 4.2.3 Enterprise AI Shift Toward Continuous Sustainability Intelligence

- 4.2.4 Procurement Requirements Linking Software Selection to Verified ESG Data

- 4.2.5 Utility Price Volatility Increasing Demand for Consumption Optimization

- 4.2.6 Fragmented Multi-Framework Reporting Burden Across Public and Private Firms

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity With Legacy ERP and Facility Systems

- 4.3.2 Weak Supplier Data Quality Slowing Scope 3 Automation

- 4.3.3 Cybersecurity and Data Residency Concerns for ESG Data Platforms

- 4.3.4 Budget Sensitivity Among Mid-Market Buyers Despite Compliance Need

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Solution Type

- 5.3.1 Carbon Management and Accounting Software

- 5.3.2 ESG Reporting and Compliance Software

- 5.3.3 Sustainability Data Management Platforms

- 5.3.4 Decarbonization Planning Software

- 5.3.5 Energy and Resource Optimization Software

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 Manufacturing

- 5.5.3 Banking, Financial Services, and Insurance (BFSI)

- 5.5.4 Government and Public Sector

- 5.5.5 Energy and Utilities

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Retail and E-Commerce

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Salesforce, Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 SAP SE

- 6.4.5 Schneider Electric SE

- 6.4.6 Oracle Corporation

- 6.4.7 Workiva Inc.

- 6.4.8 Diligent Corp.

- 6.4.9 Wolters Kluwer N.V.

- 6.4.10 Persefoni AI, Inc.

- 6.4.11 Watershed Technologies, Inc.

- 6.4.12 EcoVadis SAS

- 6.4.13 Intelex Technologies ULC

- 6.4.14 Sphera Solutions, Inc.

- 6.4.15 Benchmark Gensuite LLC

- 6.4.16 FigBytes Inc.

- 6.4.17 Measurabl, Inc.

- 6.4.18 Cority Software Inc.

- 6.4.19 Dakota Software Corporation

- 6.4.20 EnergyCAP, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Assessment

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年) 2026年全球數位測量和圖解決方案市場報告

2026年全球數位測量和圖解決方案市場報告 2026-2030年全球數位化製造軟體市場

2026-2030年全球數位化製造軟體市場