|

市場調查報告書

商品編碼

2073214

印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Indonesia Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

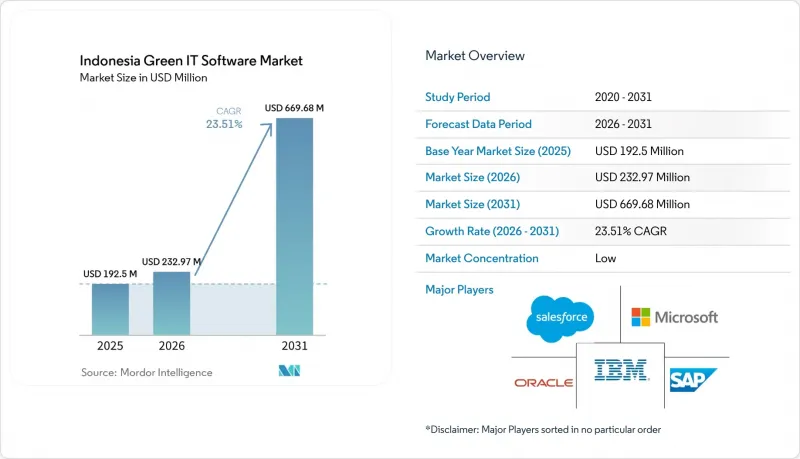

據 Mordor Intelligence 稱,印尼綠色 IT 軟體市場預計將從 2025 年的 1.925 億美元成長到 2026 年的 2.3297 億美元,到 2031 年達到 6.6968 億美元,2026 年至 2031 年的複合年成長率為 23.51%。

本報告按交付方式(軟體和服務)、部署方式(雲端、本地部署、混合部署)、公司規模(大型企業和中小企業)、解決方案類型(碳管理和計算軟體等)以及最終用戶(資訊技術和電信、製造業、政府機構等)進行分類。市場預測以美元計價。

印尼綠色IT軟體市場趨勢與洞察

推動印尼企業碳排放資訊揭露法規的製定

隨著資訊揭露期限納入明確的企業規劃週期,印尼綠色IT軟體市場正在加速發展。這縮短了企業以受控數位系統取代非正式報告程序所需的時間。 2026年2月,印尼金融服務管理局(OJK)啟動了《印尼金融服務管理局條例》(POJK 51/2017)的修訂討論。同時,印尼投資促進局(IAI)已於2025年7月通過了PSPK 1和PSPK 2,並於2025年8月11日生效,為企業向符合ISSB標準的資訊揭露實踐過渡提供了更清晰的路徑。從2027年1月開始,印尼主機板上市公司、主要銀行和海外銀行分店將分階段推廣永續發展軟體,這將使永續發展軟體從“可選支出項目”轉變為“有時效性的合規採購”,尤其對於那些仍然依賴分散記錄和人工匯總的企業而言更是如此。此外,印尼央行已在《印尼投資促進法》(TKBI)第三版中將資訊和通訊列為永續金融的“基礎領域”,這將使數位報告工具在綠色預算和資金籌措框架的討論中佔據更明確的地位。這一點至關重要,因為它使採購團隊能夠在向經營團隊、財務團隊和審計委員會論證軟體支出時,同時提供報告截止日期和基於分類的指南。事實上,印尼的綠色IT軟體市場正受益於一套監管週期,該週期評估的平台具備審計追蹤、跨多個營業單位的控制、場景感知的資料結構以及結構化的揭露工作流程,這些流程不僅在提交時可以維護,而且可以逐年維護。

企業正從基於電子表格的 ESG 追蹤轉向符合審計要求的軟體。

從基於電子表格的ESG追蹤方式向更廣泛系統領域的轉變,正在改變印尼綠色IT軟體市場,使其從一個僅提供基本報告的小眾市場發展成為一個更廣泛的系統類別,必須支援資料所有權、可追溯性、核准流程和可重複的揭露準備。雖然電子表格文件易於使用且易於部署,但當需要版本控制、資料處理歷程、跨營業單位整合、支援文件的保留以及清晰記錄誰在何時更改了哪些內容時,其弱點就顯露出來。隨著對保證要求的提高,排放資訊分散在財務、營運、採購、設施和供應商記錄中,這些記錄並非設計為在單一報告方法下協同工作,這使得手動操作既危險又容易出錯。 2026年1月,TruCarbon發表了TruCount,旨在滿足這項需求。這是一個專為印尼證券交易所(IDX)上市公司打造的平台,支援範圍1、範圍2和15個範圍3類別,並具備符合印尼金融服務管理局(OJK)標準的報告工作流程和預設的2025會計年度報告週期。該平台符合溫室氣體會計系統(GHG Protocol)、ISO 14064和GRI 305標準,顯示多重標準合規不再是只有前緣使用者才能享有的進階選項,而是一項基本要求。這種轉變使能夠將原始營運數據轉化為可用於審計的輸出數據的供應商獲得優勢,同時也減少了永續發展團隊在正式系統之外並行管理電子表格文件的需求。

排放數據分散在各子公司和供應商處。

排放數據碎片化仍是印尼綠色IT軟體市場推廣應用的主要障礙。這是因為印尼大型集團公司通常透過獨立的子公司、工廠、分銷部門和供應商網路運營,這些機構之間共用統一的報告結構。每個業務部門可能採用不同的ERP配置、審核流程或資料管理規範,導致企業甚至在開始收集供應商的範圍3資料之前,資料匯總就已經延誤。當企業試圖將用電量、燃料消耗、採購記錄、物流活動和補充文件整合到單一的、可審計的報告文件中時,這個問題會更加突出,因為該文件必須對經營團隊和外部審計人員都可靠。根據2024年的一項製造業調查,印尼企業面臨數據意識低、資料收整合本高、內部抵制標準化以及系統間缺乏互通性等問題,這也解釋了為什麼在早期階段,推廣應用所需的時間比預期更長。這些挑戰增加了企業對服務的依賴,加重了推廣應用程式的負擔,並迫使軟體供應商花費更多時間在資料映射和檢驗上,而不是用於增值規劃和分析能力。在互通性改善之前,能夠簡化資料擷取、異常處理和檢驗的供應商將繼續比那些假定來源系統已經組織好、一致且集中管理的工具更具優勢。

細分市場分析

至2025年,軟體將佔印尼綠色IT軟體市場規模的66.18%。這是因為平台授權成為受監管企業採購的首選,這些企業需要結構化的管理層來管理永續發展數據。許多買家從碳計量和報告模組入手,因為這些工具創建了基礎記錄,後續服務、品質保證準備工作和相關應用程式都可以使用這些記錄,而無需年復一年地重建相同的資料集。這一趨勢與印尼綠色IT軟體市場的現狀相符,該市場仍然需要在一個正式的系統(而非分散的內部文件)中收集、分類、儲存和檢索排放信息,這仍然主導搜尋的關鍵因素。買家優先考慮軟體的另一個原因是,軟體可以幫助他們建立一個強大的營運基礎,該基礎可以持續用於年度報告週期、內部管治審查以及需要可重複方法的不斷發展的揭露標準。因此,即使在最初的採用浪潮過去之後,實施工作變得更加複雜,並且越來越多的團隊開始使用同一平台,以許可為主導的交易仍然是預算的重要組成部分。

預計到2031年,服務市場將以25.06%的複合年成長率成長。這是因為企業在首次購買後需要遷移支援、組織架構建置、品質保證準備、培訓、工作流程設計以及持續的系統改進。早期採用該平台的企業已經意識到,永續發展報告依賴於資料管理、審核流程、支援性文件和審核準備。僅靠軟體無法實現這些目標,除非供應商和合作夥伴協助建立營運流程。因此,在印尼綠色IT軟體市場,儘管軟體仍然是主要的收入來源,但實施、資料映射、證據管理和揭露支援的重要性正在商業性凸顯。在2025年9月的平台擴展中,Workiva為準備IFRS S1和IFRS S2報告週期的財務、管治、風險、合規和永續發展團隊增加了基於代理的人工智慧、整合資料自動化和智慧永續發展工具。該產品的發展方向反映了軟體和服務之間界限的模糊化,其意義在於將引導式分析和工作流程支援整合到平臺本身,而不是將支援視為完全獨立的服務。

預計到2025年,基於雲端的部署將佔據57.23%的市場佔有率,並佔印尼綠色IT軟體市場佔有率的57.23%。這主要歸功於企業優先考慮快速部署、降低初始基礎設施投資、便捷的遠端存取以及跨多個營業單位更有效率的協作。對於在印尼各島嶼營運的企業而言,基於雲端的交付模式也有助於集中收集來自工廠、辦公室、分店、倉庫和供應商的數據,這些機構的營運條件各不相同,且通常按照不同的內部時間表進行報告。此模式也非常適合定期規則更新,因為供應商可以自訂模板、計算邏輯、係數庫和報告字段,從而無需每次客戶需要變更時啟動大規模的內部IT專案。此外,對於那些永續發展團隊、財務團隊、內部稽核部門和經營團隊使用者更傾向於在同一系統上工作,而不是交換多個本地文件(這會增加管理風險)的買家來說,這種模式也十分適用。這些優勢解釋了為什麼雲端仍然是印尼綠色 IT 軟體市場中許多首次購買者的預設部署路徑,尤其是在速度和易於協作比擁有完整的本地基礎設施更重要的情況下。

預計到2031年,混合部署將以24.38%的複合年成長率成長,因為一些公司傾向於使用基於雲端的分析和報告,同時又需要對敏感的業務和財務數據進行更嚴格的控制。根據政府法規71/2019和特定產業的監管結構,資料居住要求催生了一些實際案例:雲端工具被用於資料聚合、工作流程管理和最終披露的創建,而部分輸入資料則保留在企業內部或本地託管。這種架構對於受監管機構、政府組織以及內部安全規則要求嚴格隔離原始業務資料和更廣泛報告存取權限的大型企業尤其重要。因此,當管治規則優先考慮本地基礎設施時,本地系統仍然至關重要。然而,隨著混合模式日趨成熟、更易於檢驗,並被風險管理和合規團隊廣泛接受,本地系統的相對重要性將會降低。部署模型的多樣性表明,在印尼的綠色IT軟體產業,便利性並非唯一的決定因素。公司還會考慮主權、審計合規性、整合工作的負擔以及高度敏感來源資料的管理系統。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 印尼企業碳排放資訊揭露監理進展

- 企業從基於電子表格的ESG追蹤轉向符合審計要求的軟體

- 針對具有本地化報告工作流程的供應商的採購選擇標準

- 對整個多層製造供應鏈中範圍 3 可視性的需求日益成長。

- 人工智慧驅動的排放因子排放和資料清洗

- 綠色金融要求與可衡量的數位化報告掛鉤

- 市場限制因素

- 各子公司和供應商的排放數據各不相同。

- 中型企業永續發展分析師短缺

- 與現有ERP和採購系統整合所帶來的負擔

- 雲端採用中的資料主權和保密性問題

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 按解決方案類型

- 碳管理和運算軟體

- ESG報告和合規軟體

- 永續性資料管理平台

- 脫碳規劃軟體

- 能源和資源最佳化軟體

- 按最終用戶行業分類

- 資訊科技/通訊

- 銀行業、金融服務業及保險業

- 製造業

- 能源公用事業

- 零售與電子商務

- 政府

- 醫療保健和生命科學

- 建築和基礎設施

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Salesforce, Inc.

- Microsoft Corporation

- Oracle Corporation

- Wolters Kluwer NV

- Workiva Inc.

- Nasdaq, Inc.

- IBM Corporation

- Sphera Solutions, Inc.

- Cority Software Inc.

- Intelex Technologies ULC

- Enablon SAS

- Diligent Corporation

- IBM Japan, Ltd.

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Greenly SAS

- Normative AB

- Sweep SAS

- Terrascope Pte. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the indonesia green IT software market size is expected to increase from USD 192.50 million in 2025 to USD 232.97 million in 2026 and reach USD 669.68 million by 2031, growing at a CAGR of 23.51% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and More), and End User (Information Technology and Telecom, Manufacturing, Government, and More). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Green IT Software Market Trends and Insights

Regulatory Push for Corporate Carbon Disclosure in Indonesia

The Indonesia Green IT Software Market is moving faster because mandatory disclosure dates now fall within a defined corporate planning cycle, which shortens the time companies have to replace informal reporting routines with governed digital systems. In February 2026, OJK opened a consultation on amendments to POJK 51/2017, while IAI had already adopted PSPK 1 and PSPK 2 in July 2025 and formally launched on August 11, 2025, providing companies with a clearer transition path toward ISSB-aligned disclosure practices. The staged rollout from January 2027 for main board issuers, large banks, and overseas bank branches turns sustainability software from a discretionary line item into a dated compliance purchase, especially for enterprises that still rely on fragmented records and manual consolidations. Bank Indonesia also noted that TKBI Version 3 classifies information and communication as an enabling sector within sustainable finance, thereby giving digital reporting tools a clearer place in green budgeting discussions and financing frameworks. This matters because procurement teams now have both a reporting deadline and a taxonomy signal when they justify software spending to management, finance teams, and audit committees. In practice, the Indonesia Green IT Software Market is benefiting from a regulatory cycle that rewards platforms with audit trails, multi-entity controls, scenario-ready data structures, and structured disclosure workflows that can be maintained every year rather than assembled only at filing time.

Enterprise Shift from Spreadsheet-Based ESG Tracking to Audit-Ready Software

The move away from spreadsheet-based ESG tracking is changing the Indonesia Green IT Software Market from a basic reporting niche into a broader systems category that must support data ownership, traceability, approvals, and repeatable disclosure preparation. Spreadsheet files remain familiar and easy to start with, but they are weak when companies need version control, data lineage, cross-entity consolidation, supporting evidence retention, and a clear record of who changed what and when. Once assurance expectations rise, those manual steps introduce delays and error risk because emissions information is scattered across finance, operations, procurement, facilities, and supplier records that were not designed to work together under a single reporting method. TruCarbon addressed this need in January 2026 with TruCount, a platform built for IDX-listed companies that supports Scope 1, Scope 2, and 15 Scope 3 categories within OJK-aligned reporting workflows and a defined reporting window for the 2025 financial year. Its alignment with GHG Protocol, ISO 14064, and GRI 305 shows that multi-standard compatibility has become a baseline expectation rather than a premium option reserved for the most advanced users. That shift favors vendors that can turn raw operational inputs into audit-ready outputs, while also reducing the need for sustainability teams to maintain parallel spreadsheet files outside the formal system.

Fragmented Emissions Data Across Subsidiaries and Suppliers

Fragmented emissions data remains the main implementation barrier in the Indonesia Green IT Software Market because large Indonesian groups often operate through separate subsidiaries, plants, distribution entities, and supplier networks that do not share one reporting structure. Each operating unit may use a different ERP setup, approval routine, or level of data discipline, which slows consolidation even before companies begin supplier-facing Scope 3 collection. The problem becomes more apparent when enterprises try to align electricity use, fuel consumption, procurement records, logistics activities, and supporting documentation into a single auditable reporting file that management and external reviewers can both trust. The 2024 manufacturing study found that Indonesian firms faced limited data awareness, high collection costs, internal resistance to standardization, and insufficient interoperability across systems, which explains why first deployments often take longer than buyers initially expect. Those gaps increase service dependence, raise implementation effort, and force software vendors to spend more time on data mapping and validation than on higher-value planning or analytics functions. Until interoperability improves, vendors that simplify ingestion, exception handling, and validation will keep an advantage over tools that assume source systems are already clean, aligned, and centrally governed.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Scope 3 Visibility Across Multi-Tier Manufacturing Supply Chains

- Green Financing Requirements Tied to Measurable Digital Reporting

- Limited In-House Sustainability Analytics Talent Among Mid-Market Firms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 66.18% of the market in 2025, accounting for 66.18% of the Indonesia Green IT Software Market Size, because platform licenses were the first purchase for regulated enterprises that needed a structured control layer for sustainability data. Many buyers started with carbon accounting and reporting modules because those tools created a base record that later services, assurance preparation tasks, and adjacent applications could use without rebuilding the same dataset each year. This pattern fits the current stage of the Indonesia Green IT Software Market, where procurement is still led by the need to collect, classify, store, and retrieve emissions information in a formal system rather than in scattered internal files. Buyers also prefer software first because it creates a durable operating foundation that can remain in place across annual reporting cycles, internal governance reviews, and evolving disclosure standards that require repeatable methods. As a result, license-led deals still anchor budgets even as implementation work becomes more complex after the first deployment wave and as more teams begin using the same platform.

Services are projected to expand at a 25.06% CAGR through 2031, as enterprises now need migration support, organizational setup, assurance preparation, training, workflow design, and ongoing system refinement after the initial purchase. Companies that adopted platforms earlier are finding that sustainability reporting depends on data stewardship, approval routing, supporting documentation, and review readiness, which software alone cannot deliver unless a vendor or partner helps shape the operating process. This is why implementation, data mapping, evidence management, and disclosure support are becoming more commercially important inside the Indonesia Green IT Software Market, even though software remains the larger revenue pool. Workiva's September 2025 platform expansion added agentic AI, unified data automation, and Intelligent Sustainability tools aimed at finance, governance, risk, compliance, and sustainability teams preparing for IFRS S1 and IFRS S2 reporting cycles. That product direction matters because it shows how the line between software and services is narrowing, with vendors embedding guided analysis and workflow assistance into the platform itself instead of treating support as a fully separate offering.

Cloud-based deployment accounted for 57.23% of the market in 2025, and it held 57.23% of the Indonesia Green IT Software Market Share because enterprises valued faster rollout, lower upfront infrastructure needs, easier remote access, and more efficient coordination across multiple business entities. For companies operating across Indonesia's islands, cloud delivery also supports centralized data collection from plants, offices, branches, warehouses, and suppliers operating in different contexts and often reporting on different internal timetables. The model suits recurring rule updates because vendors can adjust templates, calculation logic, factor libraries, and reporting fields without requiring a large internal IT project each time a client needs a change. It also fits buyers who want sustainability teams, finance teams, internal auditors, and management users to work in the same system rather than exchanging multiple local files, which increases control risk. These advantages explain why cloud remains the default entry route for many first-time buyers in the Indonesia Green IT Software Market, especially where speed and ease of coordination matter more than full local infrastructure ownership.

Hybrid deployment is projected to expand at a 24.38% CAGR through 2031, as some companies still need tighter control over sensitive operational or financial data, even when they prefer cloud-based analytics and reporting outputs. Data residency requirements under Government Regulation No. 71/2019 and sector-specific oversight create a practical case for keeping some inputs on-premise or in locally hosted environments while using cloud tools for consolidation, workflow management, and final disclosure assembly. This architecture is especially relevant for regulated institutions, state-linked organizations, and large enterprises with internal security rules that require stronger separation between raw operational data and broader reporting access. On-premise systems, therefore, remain relevant where governance rules favor local infrastructure, even if their relative weight should narrow as hybrid models become more mature, easier to verify, and more acceptable to risk and compliance teams. The deployment mix shows that convenience alone does not shape buying decisions in the Indonesia Green IT Software industry, because enterprises also weigh sovereignty, audit readiness, integration effort, and control over sensitive source data.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End User Industry

- Information Technology and Telecom

- Banking, Financial Services, and Insurance

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare and Life Sciences

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- SAP SE

- Salesforce, Inc.

- Microsoft Corporation

- Oracle Corporation

- Wolters Kluwer N.V.

- Workiva Inc.

- Nasdaq, Inc.

- IBM Corporation

- Sphera Solutions, Inc.

- Cority Software Inc.

- Intelex Technologies ULC

- Enablon SAS

- Diligent Corporation

- IBM Japan, Ltd.

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Greenly SAS

- Normative AB

- Sweep SAS

- Terrascope Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Push for Corporate Carbon Disclosure in Indonesia

- 4.2.2 Enterprise Shift From Spreadsheet-Based ESG Tracking to Audit-Ready Software

- 4.2.3 Procurement Preference for Vendors With Localized Reporting Workflows

- 4.2.4 Rising Demand for Scope 3 Visibility Across Multi-Tier Manufacturing Supply Chains

- 4.2.5 AI Assisted Emissions Factor Mapping and Data Cleansing

- 4.2.6 Green Financing Requirements Tied to Measurable Digital Reporting

- 4.3 Market Restraints

- 4.3.1 Fragmented Emissions Data Across Subsidiaries and Suppliers

- 4.3.2 Limited In-House Sustainability Analytics Talent Among Mid-Market Firms

- 4.3.3 Integration Burden With Legacy ERP and Procurement Systems

- 4.3.4 Data Sovereignty and Confidentiality Concerns in Cloud Deployment

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End User Industry

- 5.5.1 Information Technology and Telecom

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare and Life Sciences

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Salesforce, Inc.

- 6.4.3 Microsoft Corporation

- 6.4.4 Oracle Corporation

- 6.4.5 Wolters Kluwer N.V.

- 6.4.6 Workiva Inc.

- 6.4.7 Nasdaq, Inc.

- 6.4.8 IBM Corporation

- 6.4.9 Sphera Solutions, Inc.

- 6.4.10 Cority Software Inc.

- 6.4.11 Intelex Technologies ULC

- 6.4.12 Enablon SAS

- 6.4.13 Diligent Corporation

- 6.4.14 IBM Japan, Ltd.

- 6.4.15 Persefoni AI, Inc.

- 6.4.16 Watershed Technology, Inc.

- 6.4.17 Greenly SAS

- 6.4.18 Normative AB

- 6.4.19 Sweep SAS

- 6.4.20 Terrascope Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年) 2026年全球數位測量和圖解決方案市場報告

2026年全球數位測量和圖解決方案市場報告 2026-2030年全球數位化製造軟體市場

2026-2030年全球數位化製造軟體市場