|

市場調查報告書

商品編碼

2073107

中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)Middle East and Africa Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

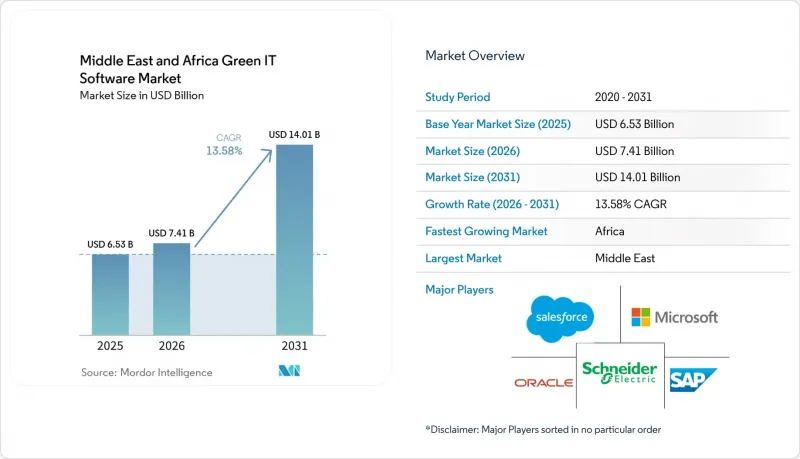

根據 Mordor Intelligence 預測,中東和非洲的綠色 IT 軟體市場規模將從 2025 年的 65.3 億美元和 2026 年的 74.1 億美元成長到 2031 年的 140.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 13.58%。

本報告按組件(軟體和服務)、應用(碳計量和排放報告等)、部署類型(雲端和本地部署)、組織規模(大型企業和中小企業)、最終用戶(製造業、零售業和電子商務等)以及地區進行細分。市場預測以美元計價。

中東和非洲綠色IT軟體市場的趨勢和洞察

強制性永續發展報告與審計合規壓力

強制揭露氣候變遷資訊已在中東和非洲的整個綠色IT軟體市場引發短期採購熱潮。這是因為遵守合規期限如今具有直接的法律和營運意義。阿拉伯聯合大公國的氣候變遷架構以及埃及於2026年2月針對非銀行金融機構所製定的措施,都鼓勵企業實施能夠整理排放數據、協助檢驗並創建經得起正式審查的記錄的系統。埃及金融監理機構已強制要求資本超過1億英鎊(204萬美元)的非銀行金融機構進行範圍1和範圍2的披露以及第三方檢驗,並要求其在2026年6月前完成合規。對供應商至關重要的是,買家不再將永續發展軟體視為獨立的報告層,因為市場趨勢日益傾向於能夠整合到日常審計、財務和管治營運中,同時最大限度地減少人工重複處理的系統。因此,在中東和非洲 (MEA) 地區的綠色 IT 軟體市場,人們越來越傾向於選擇能夠在單一環境中處理揭露工作流程、證據追蹤和不斷變化的報告義務的平台。

擴大雲端原生ESG和能源分析的應用。

到2025年,中東和非洲綠色IT軟體市場中,雲端平台將佔據71.33%的佔有率,而這個主導地位遠超單純的訂閱模式。該地區的許多買家是在資訊揭露義務實施後才進入該領域,因此他們更傾向於無需長期基礎設施建設、能夠快速運作且可與現有企業系統整合的交付模式。這也解釋了為何中東和非洲綠色IT軟體市場在初始部署階段仍然偏好SaaS(軟體即服務)工具,尤其是在資訊揭露要求收緊後才成立永續發展團隊的情況下。在雲端原生環境中,能源分析的第二個需求領域正在興起,因為可以從分散的業務地點收集使用數據,並將其轉換為標準化報告,供經營團隊和外部負責人使用。隨著買家群體的擴大,雲端工具仍將保持吸引力,因為它們可以加速從採購到部署的流程,即使內部永續發展資料處理系統仍在建置中。

傳統IT環境中永續性數據的品質較差

中東和非洲綠色IT軟體市場面臨的最大障礙往往並非軟體本身的需求,而是新工具需要利用的數據品質低。許多傳統的ERP、設施管理和運營系統並未針對資產層面的用電量進行追蹤,也未構建用於可靠排放計算的元資料,迫使團隊依賴手動流程和分散的文件。在永續發展、財務、IT和營運等部門各自負責資料鏈部分環節的行業,這個問題尤其突出,因為缺乏明確的責任分類會導致即使軟體預算已獲批准,部署仍可能延誤。因此,中東和非洲綠色IT軟體市場在採購和全面營運之間仍然存在顯著的實施差距,尤其是在首次部署的情況下。隨著買家逐漸意識到資料品質對於快速實現合規效益至關重要,能夠提供更優質範本、連接器、管治工作流程和部署支援的供應商更有可能引導潛在客戶取得真正的成功。

細分市場分析

構成比到2025年,軟體將佔據68.29%的市場佔有率,繼續穩居中東和非洲綠色IT軟體市場的領先地位。這一主導地位反映了買家對ESG、碳會計和能源分析平台的偏好,這些平台可以建構在現有的ERP和報告環境之上,而無需進行大規模的系統替換。由於許多公司仍處於早期應用階段,能夠整合到現有工作流程中的軟體模組仍然極具吸引力,尤其是在財務、IT和永續發展部門,因為在這些部門,加速實現價值至關重要。此外,大多數組織進入該領域是出於資訊揭露和資料管理的需求,而這些需求通常可以透過平台而非硬體或基礎設施投資來滿足,這也有利於軟體領域的發展。

預計2026年至2031年間,服務業將以15.12%的複合年成長率成長,成為中東和非洲綠色IT軟體市場成長最快的類別。這一成長主要得益於實施、整合、支援和維護服務,因為當資料分散在格式和所有權規則各異的系統中時,例如傳統ERP系統、雲端系統和設施系統,買家需要這些服務。 DXC透過其在埃及的卓越中心、沙烏地阿拉伯的SAP學院以及招募的300多位SAP專家,擴展了全部區域SAP方面的能力。這表明,除了軟體需求之外,對認證實施能力的需求也在不斷成長。即使不計算新的數據,中東和非洲綠色IT軟體市場的服務規模也明顯體現在企業需要記錄資料譜系、管治流程和保證方法,才能產生符合審計要求的報告。這一趨勢還表明,許多買家仍然需要實際操作支持,因為僅靠標準功能不足以應對複雜的多營業單位實施。

到2025年,ESG報告和揭露將佔應用收入的35.23%,成為中東和非洲綠色IT軟體市場最大的應用領域。這一結果與當前的監管環境相符,因為該地區許多短期義務主要側重於資訊揭露的準備、證據處理和報告系統,而非直接的排放目標。因此,買家繼續採用能夠集中指標、標準化輸出並支援內部和外部報告週期的平台。這確保了資訊揭露工具在早期採用中仍然至關重要,尤其對於上市公司、受監管實體以及有跨國報告需求的公司而言更是如此。

預計到2031年,碳會計和排放報告將以14.09%的複合年成長率成長,這表明中東和非洲的綠色IT軟體市場正從基本的合規性轉向更積極主動的衡量和規劃。 SAP的「2026永續發展控制塔」更新增強了人工智慧對監管合規性和數據映射的支持,滿足了買家對能夠將排放資訊轉化為更具可操作性的營運資料集的工具的需求。隨著企業將碳排放可見度與電力成本管理、冷卻效率和基礎設施效能連結起來,能源監控和最佳化也變得越來越重要。由於出口商和供應商對檢驗的上游數據的需求不斷成長,人們對供應鏈永續性管理的興趣也日益濃厚。同時,該地區許多地方的廢棄物和水資源相關應用仍處於起步階段。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 強制性永續發展報告與審計合規壓力

- 擴大雲端原生ESG和能源分析的應用。

- 人工智慧驅動的碳核算和工作負載最佳化

- 跨國公司對供應商的可追溯性要求

- 能源成本波動與強制性IT效率提升

- 數位主權與本地資料託管的發展

- 市場限制因素

- 傳統IT環境下永續性資料品質的局限性

- 缺乏熟練的ESG和碳數據專家

- ERP、雲端和物聯網堆疊之間整合的複雜性。

- 預算優先排序和核心收入軟體

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 科技趨勢

- 監理情勢

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 實施和整合服務

- 支援和維護服務

- 透過使用

- 碳計量和排放報告

- 能源監控與最佳化

- 環境、社會和管治(ESG) 報告和揭露

- 供應鏈永續管理

- 綠色IT資產和資料中心的最佳化

- 其他用途

- 部署模式

- 基於雲端的

- 現場

- 按組織規模

- 大公司

- 小型企業

- 最終用戶

- 資訊科技/通訊

- 銀行業、金融服務業及保險業

- 製造業

- 政府/公共部門

- 能源公用事業

- 醫療保健和生命科學

- 零售與電子商務

- 其他最終用戶

- 按地區

- 中東

- 波灣合作理事會(GCC)

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Microsoft Corporation

- IBM Corporation

- Schneider Electric SE

- Oracle Corporation

- Salesforce, Inc.

- Wolters Kluwer NV

- Sphera Solutions, Inc.

- Cority Software Inc.

- Enablon North America Corp.

- Benchmark Gensuite, LLC

- Intelex Technologies ULC

- Diligent Corporation

- Workiva Inc.

- FigBytes Inc.

- Envirosuite Limited

- ESG Book GmbH

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Plan A Solutions GmbH

- Normative AB

- Sweep SAS

- Eniscope Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and Africa Green IT Software Market size is projected to expand from USD 6.53 billion in 2025 and USD 7.41 billion in 2026 to USD 14.01 billion by 2031, registering a CAGR of 13.58% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Application (Carbon Accounting and Emissions Reporting, and More), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), End User (Manufacturing, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Middle East and Africa Green IT Software Market Trends and Insights

Mandatory Sustainability Reporting and Audit Readiness Pressure

Mandatory climate disclosure has already become a near-term buying trigger across the Middle East and Africa Green IT Software Market because compliance deadlines now carry direct legal and operational consequences. The UAE climate framework and Egypt's February 2026 decision for non-banking financial institutions both pushed enterprises toward systems that can organize emissions data, support verification, and produce records that withstand formal review. Egypt's Financial Regulatory Authority required Scope 1 and Scope 2 disclosures, along with third-party verification, for non-banking financial institutions with capital above EGP 100 million (USD 2.04 million), with compliance due by June 2026. What matters for vendors is that buyers are no longer treating sustainability software as a separate reporting layer, because they increasingly want systems that can fit into audit, finance, and governance routines with less manual rework. This is why the MEA Green Information Technology software market is seeing a stronger preference for platforms that can handle disclosure workflows, evidence trails, and changing reporting obligations in one environment.

Rising Cloud-Native ESG and Energy Analytics Adoption

Cloud-based platforms held 71.33% of the 2025 Middle East and Africa Green IT Software Market, and that lead reflects more than simple subscription economics. Many regional buyers entered the category after mandatory reporting requirements had already been introduced, so they favored delivery models that could go live quickly and connect with existing enterprise systems without a lengthy infrastructure build. This also explains why the Middle East and Africa Green IT Software Market continues to lean toward software-as-a-service tools for first deployments, especially where sustainability teams were created after disclosure requirements had already started to tighten. A second layer of demand is emerging for energy analytics, as cloud-native environments can collect usage data across dispersed operations and turn it into repeatable reports for management teams and external reviewers. As the buyer base widens, the appeal of cloud tools is likely to remain strong because they give organizations a faster path from procurement to operational use, even when internal sustainability data processes are still being built.

Limited Sustainability Data Quality across Legacy IT Estates

The biggest brake on the Middle East and Africa Green IT Software Market is often not software demand, but the poor condition of the data that new tools are expected to use. Many legacy ERP, facilities, and operations systems were never built to capture electricity use at the asset level or to organize the metadata needed for credible emissions calculations, leaving teams to rely on manual work and fragmented files. That problem is especially important in sectors where sustainability, finance, IT, and operations each control parts of the data chain, because unclear ownership can slow implementation even after software budgets are approved. As a result, the Middle East and Africa Green IT Software Market still carries a meaningful execution gap between procurement and full operational use, particularly in first-time deployments. Vendors that can provide better templates, connectors, governance workflows, and onboarding support are more likely to convert interest into successful use, as buyers increasingly recognize that data readiness determines how quickly compliance benefits can be realized.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Carbon Accounting and Workload Optimization

- Multinational Supplier Traceability Requirements

- Shortage of Skilled ESG and Carbon Data Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 68.29% of the 2025 component mix, keeping it firmly in the leading position in the Middle East and Africa Green IT Software Market. That lead reflects buyer preference for ESG, carbon accounting, and energy analytics platforms that can sit on top of existing ERP and reporting environments, rather than forcing a broad system replacement. Many enterprises are still in an early deployment phase, so the appeal of software modules that can be integrated into existing workflows remains strong, especially for finance, IT, and sustainability teams that need faster time-to-value. The software segment also benefits from the fact that most organizations first enter this category through disclosure or data management needs, which are usually addressed through platforms rather than hardware or infrastructure spending.

Services are projected to grow at a 15.12% CAGR from 2026 to 2031, making them the fastest-rising component category in the Middle East and Africa Green IT Software Market. This growth comes from implementation, integration, support, and maintenance work that buyers need when data sits across legacy ERP, cloud, and facility systems with different formats and ownership rules. DXC expanded SAP capabilities across the region through a center of excellence in Egypt, a SAP academy in Saudi Arabia, and the recruitment of more than 300 SAP professionals, which illustrates how demand for certified delivery capacity is rising alongside software demand. Even without calculating new values, the Middle East and Africa Green IT Software Market size for services is clearly supported by the need to document data lineage, governance routines, and assurance methods before enterprises can claim audit-ready reporting. The pattern also shows that many buyers still need hands-on support because out-of-the-box functionality alone is not enough for complex, multi-entity deployments.

ESG reporting and disclosure accounted for 35.23% of application revenue in 2025, making it the largest application area across the Middle East and Africa Green IT Software Market. That result is consistent with the current regulatory landscape, since most near-term obligations in the region have focused first on disclosure readiness, evidence handling, and reporting structure rather than on direct emissions-reduction targets. Buyers, therefore, continue to start with platforms that can centralize metrics, standardize outputs, and support internal and external reporting cycles. This keeps disclosure tools at the center of early adoption, particularly among listed firms, regulated institutions, and enterprises with multi-country reporting needs.

Carbon accounting and emissions reporting are forecast to grow at a 14.09% CAGR through 2031, indicating that the Middle East and Africa Green IT Software Market is moving from basic compliance toward more active measurement and planning. SAP's 2026 Sustainability Control Tower updates strengthened AI support for regulatory readiness and data mapping, which aligns with buyer demand for tools that can turn emissions information into a more usable operational dataset. Energy monitoring and optimization are also becoming more important as enterprises link carbon visibility with electricity cost control, cooling efficiency, and infrastructure performance. Supply chain sustainability management is attracting stronger interest as exporters and suppliers face growing requests for verified upstream data, while waste and water applications are still at an earlier stage across much of the region.

Complete Report Scope:

- By Component

- Software

- Services

- Implementation and Integration Services

- Support and Maintenance Services

- By Application

- Carbon Accounting and Emissions Reporting

- Energy Monitoring and Optimization

- Environmental, Social, and Governance (ESG) Reporting and Disclosure

- Supply Chain Sustainability Management

- Green IT Asset and Data Center Optimization

- Other Applications

- By Deployment Mode

- Cloud-Based

- On-Premises

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End User

- Information Technology and Telecom

- Banking, Financial Services, and Insurance

- Manufacturing

- Government and Public Sector

- Energy and Utilities

- Healthcare and Life Sciences

- Retail and E-Commerce

- Other End Users

- By Geography

- Middle East

- Gulf Cooperation Council (GCC)

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- SAP SE

- Microsoft Corporation

- IBM Corporation

- Schneider Electric SE

- Oracle Corporation

- Salesforce, Inc.

- Wolters Kluwer N.V.

- Sphera Solutions, Inc.

- Cority Software Inc.

- Enablon North America Corp.

- Benchmark Gensuite, LLC

- Intelex Technologies ULC

- Diligent Corporation

- Workiva Inc.

- FigBytes Inc.

- Envirosuite Limited

- ESG Book GmbH

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Plan A Solutions GmbH

- Normative AB

- Sweep SAS

- Eniscope Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory Sustainability Reporting and Audit Readiness Pressure

- 4.2.2 Rising Cloud-Native ESG and Energy Analytics Adoption

- 4.2.3 AI-Enabled Carbon Accounting and Workload Optimization

- 4.2.4 Multinational Supplier Traceability Requirements

- 4.2.5 Energy Cost Volatility and IT Efficiency Mandates

- 4.2.6 Digital Sovereignty and Local Data Hosting Buildouts

- 4.3 Market Restraints

- 4.3.1 Limited Sustainability Data Quality Across Legacy IT Estates

- 4.3.2 Shortage of Skilled ESG and Carbon Data Specialists

- 4.3.3 Integration Complexity Across ERP, Cloud, and IoT Stacks

- 4.3.4 Budget Prioritization Versus Core Revenue Software

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Technology Outlook

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Support and Maintenance Services

- 5.2 By Application

- 5.2.1 Carbon Accounting and Emissions Reporting

- 5.2.2 Energy Monitoring and Optimization

- 5.2.3 Environmental, Social, and Governance (ESG) Reporting and Disclosure

- 5.2.4 Supply Chain Sustainability Management

- 5.2.5 Green IT Asset and Data Center Optimization

- 5.2.6 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End User

- 5.5.1 Information Technology and Telecom

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Manufacturing

- 5.5.4 Government and Public Sector

- 5.5.5 Energy and Utilities

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Retail and E-Commerce

- 5.5.8 Other End Users

- 5.6 By Geography

- 5.6.1 Middle East

- 5.6.1.1 Gulf Cooperation Council (GCC)

- 5.6.1.2 Turkey

- 5.6.1.3 Rest of Middle East

- 5.6.2 Africa

- 5.6.2.1 South Africa

- 5.6.2.2 Nigeria

- 5.6.2.3 Rest of Africa

- 5.6.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Microsoft Corporation

- 6.4.3 IBM Corporation

- 6.4.4 Schneider Electric SE

- 6.4.5 Oracle Corporation

- 6.4.6 Salesforce, Inc.

- 6.4.7 Wolters Kluwer N.V.

- 6.4.8 Sphera Solutions, Inc.

- 6.4.9 Cority Software Inc.

- 6.4.10 Enablon North America Corp.

- 6.4.11 Benchmark Gensuite, LLC

- 6.4.12 Intelex Technologies ULC

- 6.4.13 Diligent Corporation

- 6.4.14 Workiva Inc.

- 6.4.15 FigBytes Inc.

- 6.4.16 Envirosuite Limited

- 6.4.17 ESG Book GmbH

- 6.4.18 Persefoni AI, Inc.

- 6.4.19 Watershed Technology, Inc.

- 6.4.20 Plan A Solutions GmbH

- 6.4.21 Normative AB

- 6.4.22 Sweep SAS

- 6.4.23 Eniscope Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 2026年全球數位測量和圖解決方案市場報告

2026年全球數位測量和圖解決方案市場報告 2026-2030年全球數位化製造軟體市場

2026-2030年全球數位化製造軟體市場