|

市場調查報告書

商品編碼

2073216

越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Vietnam Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

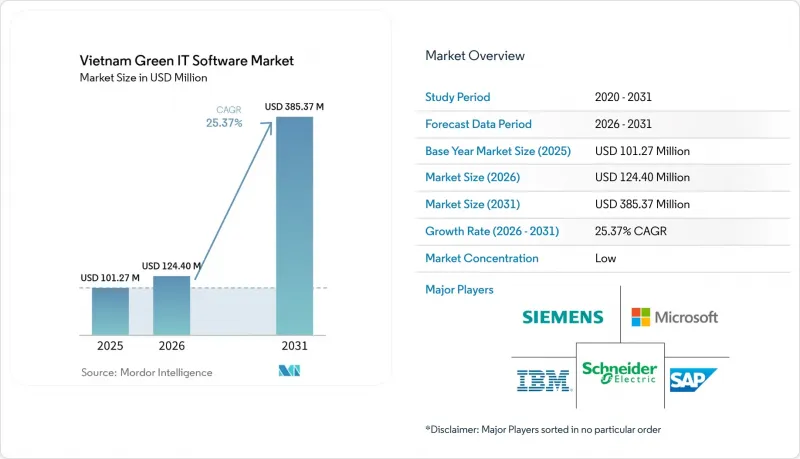

據 Mordor Intelligence 稱,越南綠色 IT 軟體市場在 2025 年的價值為 1.0127 億美元,預計到 2031 年將達到 3.8537 億美元,而 2026 年為 1.244 億美元,預測期(2026-2031 年)的複合年成長率為 25.37%。

本報告按交付方式(軟體和服務)、部署方式(雲端、本地部署、混合部署)、公司規模(大型企業和中小企業)、解決方案類型(碳管理和計算軟體等)以及最終用戶(資訊技術和電信、製造業、政府機構等)進行分類。市場預測以美元計價。

越南綠色IT軟體市場趨勢與洞察

促進碳和能源可追溯性法規的製定

越南國內排放交易試點計畫於2025年8月啟動,法律規範於2026年1月進一步完善,河內證券交易所根據第29/2026/ND-CP號法令成立了國家碳排放交易。隨後,第11/2026/TT-BNNMT號通知建立了國家碳排放登記系統,強制要求對配額和碳權額的發放、轉讓和註銷進行電子追蹤。這使得數位化記錄保存成為一項基本功能,而不僅僅是可選的行政工具。越南的綠色IT軟體市場正積極應對這項變化,因為該系統涵蓋的110家企業需要可審計的排放清單和可追溯的工作流程,而這些僅靠電子表格難以大規模實現。隨著該系統預計將於2029年全面實施,採購企業正在超越目前的報告要求,開發新的系統,為未來幾年更嚴格的合規週期做好準備。此外,由於登記系統的結構,基準資料不足會導致成本增加。這是因為正式的審計追蹤可以揭示錯誤,這可能對過去的報告期間造成風險。由於《2026年公司管治準則》中關於氣候管治的要求,市場需求進一步擴大,因為上市公司現在必須加強其董事會在環境監測和資訊揭露流程方面的課責。

雲端遷移和混合架構現代化

越南企業採用雲端技術已發展到一個新的階段,其意義不僅在於降低基礎設施成本,更在於支援ESG資料收集、工作流程整合和多站點報告。 2026年,實際的架構挑戰不再只是「雲端或本地部署」的選擇,而是如何將多重雲端柔軟性、本地託管、資料駐留和系統整合整合到單一的營運模式中。因此,越南綠色IT軟體市場對能夠與ERP系統整合,並在不影響報告連續性的前提下,將受監管資料儲存與分析工作負載分離的平台的需求日益成長。微軟將於2026年發布的Sustainability Manager表明,領先的企業供應商正在將永續發展功能直接整合到現有的業務軟體環境中,從而提升該領域的自動化和整合水準。這對越南買家意義重大,因為本地網路安全義務和全球母公司的報告要求往往並存,因此混合模式是最現實的選擇。因此,實施決策變得更加具有策略性,能夠支援合規性、互通性和架構柔軟性的供應商在越南綠色IT軟體市場中獲得了優勢。

雲端安全、資料架構和碳核算領域人才短缺。

越南綠色IT軟體市場的主要實際障礙並非認知度低,而是缺乏能夠建立系統、管理資料品質並將報告規則轉化為可執行工作流程的人才。儘管越南的目標是培養70萬名資訊通訊技術(ICT)專業人才,但預計到2025年,勞動人口仍將維持在55萬左右,僅有30%的畢業生被認為能夠立即勝任企業的工作。同時,綠色人才的競爭日益激烈,ESG(環境、社會和治理)專業的薪資比類似的IT職位高出15%至25%。這種人才短缺不僅限於企業永續發展團隊;越南還需要約15萬名專業人員來支持其排碳權市場,這使得製造業、金融業和科技業的雇主之間對有限的人才資源展開了直接競爭。這種人才短缺阻礙了軟體的售後實施,因為企業仍然需要能夠建立資產登記冊、檢驗資料、整合系統和管理持續報告週期的人員。因此,即使客戶接受度依然很高,許可證使用率、專案進度和業務擴張帶來的收入也受到了負面影響。

細分市場分析

2025年,軟體在越南綠色IT軟體市場中佔比達66.45%。這顯示早期投資主要集中在平台所有權而非外包。企業最初傾向於使用碳管理工具、ESG報告系統和永續發展數據平台,因為這些產品最能滿足其提交、審計和客戶報告等迫切需求。對於需要直接管理資料輸入和審核流程的受監管企業和出口導向企業而言,這一趨勢尤其明顯。基於授權的軟體也適用於初始購買階段,因為許多企業當時正處於建立首個正式溫室氣體清單和內部管治架構的階段。本質上,買家尋求的是能夠收集來源資料、儲存審計追蹤並支援未來與企業系統整合的工具。

預計到2031年,服務業將以26.88%的複合年成長率成長,這標誌著越南綠色IT軟體市場進入第二階段,即在初始購買之後,實施支援的價值將顯著提升。這項需求的驅動力源自於企業內部ESG分析能力、碳計量知識和技術整合技能的不足,使得外部支援對許多公司至關重要。 SAP的永續發展人工智慧代理將於2026年部署,這也反映了軟體和諮詢工作流程的整合,尤其是在報告生成、模擬和合規文件方面。在此背景下,本地實施合作夥伴的重要性日益凸顯,ESEC與IBM Envizi的合作便是全球平台與越南本地實施能力相結合的絕佳例證。簡而言之,隨著合規要求的日益細化,未來的收入成長不僅來自實施項目,還將來自管理彙報、審計支援、平台調優和持續整合工作。

預計2025年,越南綠色IT軟體市場中,基於雲端的採用率將達到57.81%。這主要源自於企業需要從多個設施收集數據,並整合跨業務部門的報告。雲端模式尤其適用於排放和能源數據,因為企業通常需要即時或近即時地了解所有地點、供應商和報告團隊的數據。雲端模式還支援更快的更新、更方便的協作以及與現代企業應用程式更好的整合。因此,對於那些從零開始建立永續發展系統,而非僅僅擴展現有本地工具的企業而言,雲端已成為首選。由此可見,越南綠色IT軟體市場正朝著「雲端優先」的設計方向發展,其中可擴展性和遠端存取是價值創造的核心。

預計到2031年,混合部署將以26.33%的複合年成長率成長,使其成為企業在平衡全球報告標準與越南資料處理法規方面最具戰略意義的架構選擇。純雲端模式在小型資料庫和資料居住法規嚴格的情況下可能會帶來一些問題。另一方面,完全本地部署模式可能會降低供應商協作和大規模分析的柔軟性。混合架構提供了一種折衷方案,既能將敏感資料儲存在本地,又能利用更廣泛的雲端資源進行分析、自動化和工作流程調整。微軟的永續發展產品藍圖和越南的網路安全政策都支持這種模式,買家越來越需要能夠同時滿足企業和本地合規要求的系統。因此,在越南綠色IT軟體市場,部署選擇不再只是IT偏好,而是更廣泛的風險和合規策略的一部分。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 碳和能源可追溯性的監管進展

- 雲端遷移和混合架構現代化

- 綠色資料中心和能源效率法規

- 來自CBAM和ESG法規的出口導向合規壓力

- 工業園區脫碳和ESG數位化

- 人工智慧驅動的高密度數位基礎設施能源最佳化

- 市場限制因素

- 雲端安全、資料架構和碳核算領域人才短缺。

- 資料本地化和遵守外國供應商規定的複雜性

- 可擴展部署中的電網和基礎設施限制

- 中小企業採購負責人的預算敏感度。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 按解決方案類型

- 碳管理和運算軟體

- ESG報告和合規軟體

- 永續性資料管理平台

- 脫碳規劃軟體

- 能源和資源最佳化軟體

- 最終用戶

- 資訊科技/通訊

- 銀行業、金融服務業及保險業

- 製造業

- 能源公用事業

- 零售與電子商務

- 政府

- 醫療保健和生命科學

- 建築和基礎設施

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric SE

- Microsoft Corporation

- IBM Corporation

- SAP SE

- Workiva Inc.

- Watershed Technology, Inc.

- Persefoni AI, Inc.

- Sweep SAS

- Normative AB

- EcoVadis SAS

- Diligent Corporation

- Sphera Solutions, Inc.

- Plan A

- Greenly

- Novisto Inc.

- Cority Software Inc.

- Enablon North America Corp.

- Siemens AG

- Honeywell International Inc.

- Johnson Controls International plc

第7章 市場機會與未來展望

According to Mordor Intelligence, the vietnam green IT software market size was valued at USD 101.27 million in 2025 and estimated to grow from USD 124.40 million in 2026 to reach USD 385.37 million by 2031, at a CAGR of 25.37% during the forecast period (2026-2031).

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and More), and End User (Information Technology and Telecom, Manufacturing, Government, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Green IT Software Market Trends and Insights

Regulatory Push for Carbon and Energy Traceability

Vietnam's domestic emissions trading system pilot started in August 2025, and the regulatory framework became much more concrete in January 2026 when Decree No. 29/2026/ND-CP established a domestic carbon exchange operated by the Hanoi Stock Exchange. Circular No. 11/2026/TT-BNNMT then established the national carbon registry and required electronic tracking for the issuance, transfer, and cancellation of quotas and credits, thereby making digital recordkeeping a functional requirement rather than an optional administrative tool. The Vietnam Green IT Software Market is responding to this shift because 110 covered installations now need auditable emissions inventories and traceable workflows that spreadsheets cannot easily support at scale. Full implementation is expected in 2029, so buyers are not only reacting to today's filings but also preparing their systems for a tighter compliance cycle over the next few years. The registry structure also raises the cost of weak baseline data, because errors can become visible across a formal audit trail and create exposure tied to prior reporting periods. Climate governance requirements under the Corporate Governance Code 2026 further broaden the demand base, as listed companies now face stronger board accountability for environmental oversight and disclosure processes.

Cloud Migration and Hybrid Architecture Modernization

Enterprise cloud adoption in Vietnam has reached a point where it supports ESG data collection, workflow integration, and reporting across multiple sites, rather than simply lowering infrastructure costs. The practical architecture question in 2026 is not simply cloud versus on-premise, but how to combine multi-cloud flexibility, local hosting, data residency, and systems integration in a single operating model. That is why the Vietnam Green IT Software Market is seeing a stronger pull for platforms that can connect with ERP systems and separate regulated data storage from analytics workloads without breaking reporting continuity. Microsoft's 2026 Sustainability Manager release shows how large enterprise vendors are building sustainability features directly into existing business software environments, raising the baseline for automation and integration across the category. This matters for buyers in Vietnam because local cybersecurity obligations and global parent reporting requirements often coexist, and a hybrid model is the most workable path in that setting. As a result, deployment decisions are becoming more strategic, and software vendors that can support compliance, interoperability, and architecture flexibility are gaining an advantage in the Vietnam Green IT Software Market.

Talent Shortage in Cloud Security, Data Architecture, and Carbon Accounting

The main practical barrier for the Vietnam Green IT Software Market is not awareness, but the shortage of people who can configure systems, manage data quality, and translate reporting rules into usable workflows. Vietnam targeted 700,000 ICT professionals, but the workforce stood near 550,000 in 2025, and only 30% of graduates were considered immediately ready for enterprise roles. At the same time, green hiring is becoming more competitive, with ESG specialist roles commanding a 15-25% salary premium over similar IT positions. The labor challenge is broader than corporate sustainability teams, as Vietnam also needs around 150,000 specialized workers to support the carbon credit market, placing manufacturing, finance, and technology employers in direct competition for the same small talent pool. That shortage slows deployment after software is purchased, because companies still need staff who can build inventories, validate data, connect systems, and manage ongoing reporting cycles. The result is a drag on license utilization, project timelines, and expansion revenue, even when customer intent to adopt remains strong.

Other drivers and restraints analyzed in the detailed report include:

- Green Data Center and Energy Efficiency Mandates

- Export-Oriented Compliance Pressure from CBAM and ESG Rules

- Data Localization and Compliance Complexity for Foreign Vendors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 66.45% of the Vietnam Green IT Software Market share in 2025, which shows that the first wave of spending centered on platform ownership rather than outsourced delivery. Companies moved first toward carbon management tools, ESG reporting systems, and sustainability data platforms because these products are closest to immediate filing, audit, and customer reporting needs. This pattern was especially clear among regulated operators and export-facing enterprises that needed direct control over data inputs and approval steps. License-based software also fits the early buying cycle because many companies were still establishing their first formal greenhouse gas inventories and internal governance structures. In practice, buyers wanted tools that could capture source data, preserve audit trails, and support future integration with enterprise systems.

Services are projected to expand at a 26.88% CAGR through 2031, indicating a second phase in the Vietnam Green IT Software Market in which implementation support becomes more valuable after the initial purchase. The demand is driven by gaps in internal ESG analytics capacity, carbon accounting know-how, and technical integration skills, making outside help necessary for many companies. SAP's sustainability AI agent rollout in 2026 also shows that software and advisory workflows are converging, especially for reporting preparation, simulation, and compliance documentation. Local delivery partners are becoming increasingly important in this context, and ESEC's IBM Envizi partnership is a strong example of how global platforms are packaged with local implementation capabilities in Vietnam. That means future revenue growth should come not only from setup projects, but also from managed reporting, audit support, platform tuning, and recurring integration work as compliance needs become more detailed.

Cloud-based deployment accounted for 57.81% of the Vietnam Green IT Software Market in 2025, supported by the need to collect data from multiple facilities and consolidate reporting across business units. Cloud models are well-suited to emissions and energy data because companies often need real-time or near-real-time visibility across sites, suppliers, and reporting teams. They also support faster updates, easier collaboration, and better integration with modern enterprise applications. This has made the cloud the default path for companies building sustainability systems from scratch rather than extending older local tools. The Vietnam Green IT Software Market has therefore leaned toward cloud-first designs where scalability and remote access are central to value creation.

Hybrid deployment is projected to expand at a 26.33% CAGR through 2031, making it the most strategic architecture choice for companies balancing global reporting standards with Vietnamese data-handling rules. A pure cloud model can raise concerns when local storage or data residency rules are strict, while a fully on-premises model can reduce flexibility for supplier collaboration and large-scale analytics. Hybrid architecture offers a middle path by keeping sensitive data onshore while still using broader cloud resources for analytics, automation, and workflow coordination. Microsoft's sustainability product roadmap and Vietnam's cybersecurity direction both support this pattern, as buyers increasingly want systems that meet both corporate and local compliance requirements. As a result, deployment choice in the Vietnam Green IT Software Market is no longer a narrow IT preference, but part of a broader risk and compliance strategy.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End User

- Information Technology and Telecom

- Banking, Financial Services, and Insurance

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare and Life Sciences

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- Schneider Electric SE

- Microsoft Corporation

- IBM Corporation

- SAP SE

- Workiva Inc.

- Watershed Technology, Inc.

- Persefoni AI, Inc.

- Sweep SAS

- Normative AB

- EcoVadis SAS

- Diligent Corporation

- Sphera Solutions, Inc.

- Plan A

- Greenly

- Novisto Inc.

- Cority Software Inc.

- Enablon North America Corp.

- Siemens AG

- Honeywell International Inc.

- Johnson Controls International plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Push for Carbon and Energy Traceability

- 4.2.2 Cloud Migration and Hybrid Architecture Modernization

- 4.2.3 Green Data Center and Energy Efficiency Mandates

- 4.2.4 Export-Oriented Compliance Pressure From CBAM and ESG Rules

- 4.2.5 Industrial Park Decarbonization and ESG Digitization

- 4.2.6 AI-Driven Energy Optimization in High-Density Digital Infrastructure

- 4.3 Market Restraints

- 4.3.1 Talent Shortage in Cloud Security, Data Architecture, and Carbon Accounting

- 4.3.2 Data Localization and Compliance Complexity for Foreign Vendors

- 4.3.3 Power Grid and Infrastructure Constraints for Scalable Deployment

- 4.3.4 Budget Sensitivity Among SMEs and Mid-Market Buyers

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End User

- 5.5.1 Information Technology and Telecom

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare and Life Sciences

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Microsoft Corporation

- 6.4.3 IBM Corporation

- 6.4.4 SAP SE

- 6.4.5 Workiva Inc.

- 6.4.6 Watershed Technology, Inc.

- 6.4.7 Persefoni AI, Inc.

- 6.4.8 Sweep SAS

- 6.4.9 Normative AB

- 6.4.10 EcoVadis SAS

- 6.4.11 Diligent Corporation

- 6.4.12 Sphera Solutions, Inc.

- 6.4.13 Plan A

- 6.4.14 Greenly

- 6.4.15 Novisto Inc.

- 6.4.16 Cority Software Inc.

- 6.4.17 Enablon North America Corp.

- 6.4.18 Siemens AG

- 6.4.19 Honeywell International Inc.

- 6.4.20 Johnson Controls International plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年) 2026年全球數位測量和圖解決方案市場報告

2026年全球數位測量和圖解決方案市場報告 2026-2030年全球數位化製造軟體市場

2026-2030年全球數位化製造軟體市場